Does Good News on Inflation Promise Happier Times in 2023?

The Bureau of Labor Statistics October Producer Price Index (PPI) brought good news to an inflation-weary world. Maybe, just maybe, the report suggested, we will soon have roaring inflation behind us. And yes, this may mean the Fed can reduce pressure on the brake pedal as the economy slows. At least that is the growing opinion of some highly focused Fed watchers. Perhaps more importantly, maybe we will escape a hard-hitting recession in 2023.

Even though higher-priced energy was still hitting consumers hard, the all-item October PPI rose 8.0 percent, year-over-year, which is better than September’s 8.4 percent and August’s 8.7 percent and way better than July’s 9.7 percent. And within the all-item index, the services component fell for the first time in nearly two years.

Welcoming the improved picture, University of Michigan economist Justin Wolfers, in a Brookings Institution discussion of the report, said: “I am still unbelievably excited by seeing this. We may have seen not only the peak of inflation behind us, but glimmers of excitement that the crisis, we can see how and why and when it might end.”

In a more cautious assessment of the Fed’s efforts to tame inflation and slow the economy by limiting money supply growth, Will Compernolle, senior economist at FHN Financial in New York, said, "The Fed cares about producer prices to the extent they pass through to consumer prices. The most stubborn parts of CPI inflation in core services, like shelter, won't be influenced anytime soon from improvements in producer prices."

In short, the happier PPI seems to offer glimmers of hope for better days ahead with respect to additional interest rate hikes and perhaps to the avoidance of a recession.

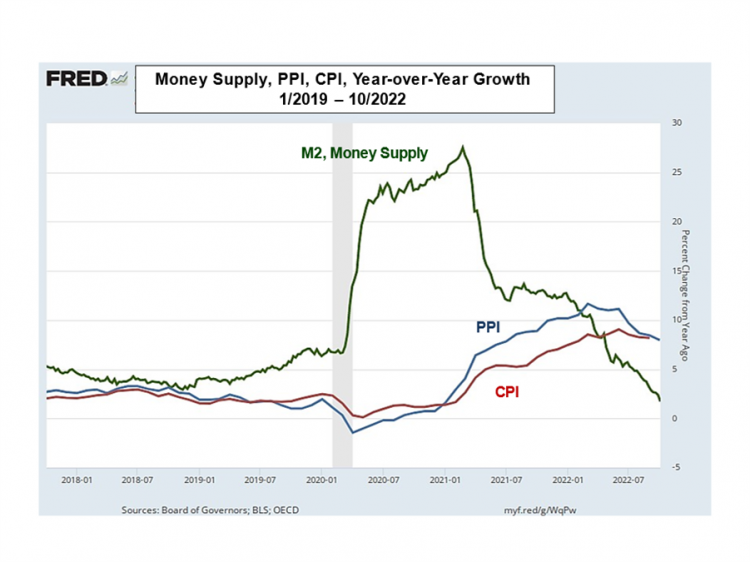

Typically, increases in money supply, all else equal, lead to rising producer prices that get passed along in the form of higher consumer prices. Federal Reserve data can show how these economic indicators all fit together by pulling into one chart the monthly year-over-year growth data for M2, a popular measure of the amount of money circulating in the economy, the PPI and the all-item Consumer Price Index (CPI). The most recent data, seen here, are for the period January 1, 2019, through October 30, 2022. I note that data for the October 2022 CPI have not been reported.

A quick glance at the green line, the M2 data, demonstrates the alarming growth and subsequent drop in money supply growth starting at the onset of the pandemic. Starting in mid-2020, this period is associated with the trillions of dollars that the government sent to consumers and businesses to cushion the economic consequences of pandemic-related shutdowns and layoffs. Since M2 began to slow around mid-2021, it has continued to fall and is now growing at less than 3 percent, annually. As seen here, it takes the better part of a year for the effects of changes in M2 to become fully registered in changes in the PPI and CPI.

This lagging relationship can be seen in the PPI’s growth path, the blue line, as it responds about 12 months after the M2 growth explosion. In early 2021, PPI growth begins to rise, subsequently peaking later in the year before it diminishes. The current October number is part of the lower growth trend. Similarly, CPI growth, as seen in the red line, tells us how quickly PPI inflation affects CPI-measured inflation.

Comparing all three data sets enables us, somewhat confidently, to make three key predictions: that the Fed’s reductions in money supply growth matter, that the hotter flames of inflation are behind us and, given the lags, we should expect to see CPI inflation approaching 2.5 percent or so by this time next year. Of course, we should warn that other major wars and energy disturbances could change everything.

But what does all this say about the prospects for more interest rate increases and the likelihood of a hard-hitting 2023 recession?

Of course, we can only guess. No one claims to understand the mind of the Fed. However, considering the data we have reviewed, the Fed will soften its boot on the brakes – suggesting rates will rise by less than 75 basis points at the December meeting and that increases become softer after that. As a result, the likelihood of having a hard recession in early 2023 with high unemployment will fall significantly. Instead, national economic growth, as measured by real GDP, will fall toward zero and become negative in 2023’s latter half, resulting in small but positive real GDP growth in 2023 overall.

Even though we live in turbulent times and get pestered with widely changing economic data, we can be comforted for now by evidence that points toward lower future inflation and, on the score, happier times for consumers.

Bruce Yandle is a distinguished adjunct fellow with the Mercatus Center at George Mason University, dean emeritus of the Clemson College of Business and Behavioral Sciences, and a former executive director of the Federal Trade Commission.