- | Government Spending Government Spending

- | Working Papers Working Papers

- |

Multistate Health Plans: Agents for Competition or Consolidation?

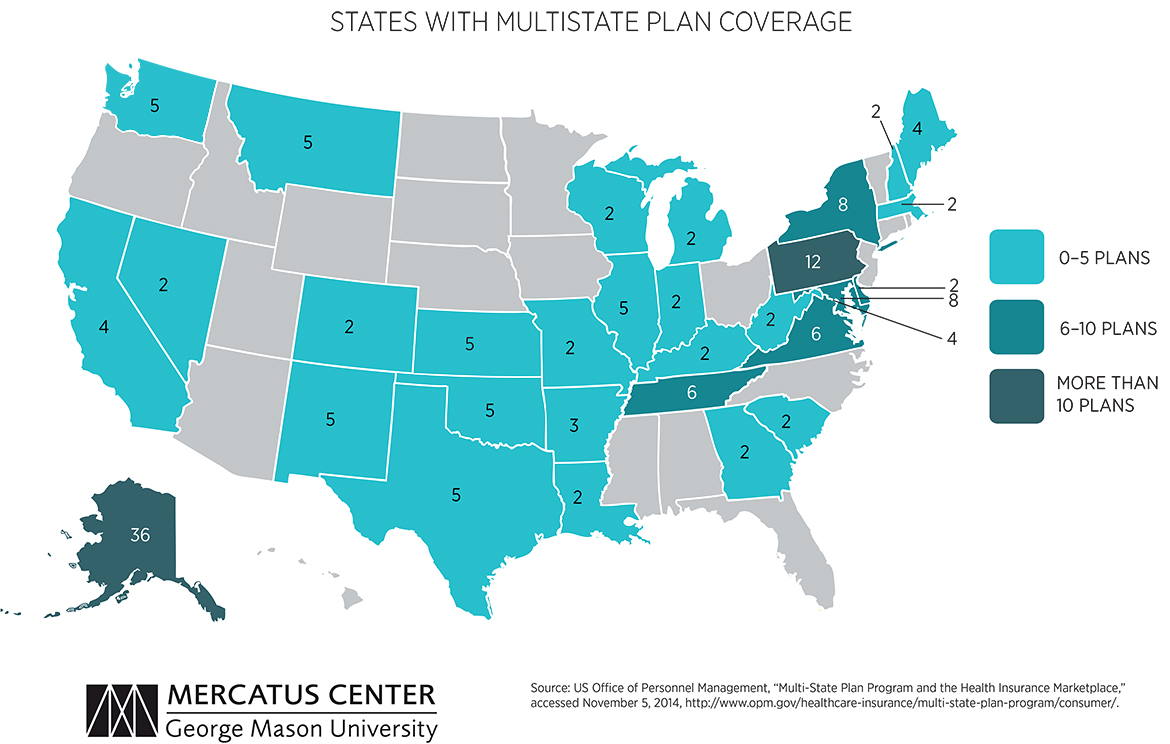

In a new study for the Mercatus Center at George Mason University, scholars Robert Emmet Moffit and Neil R. Meredith demonstrate that while the MSP Program grants new power to the OPM by setting standards designed to limit entry into the program, the law may decrease competition and increase consolidation in the health insurance market. Decreased competition in the health care market may lead to higher prices for consumers of health care and could revive calls for a public health insurance option.

A key goal of the Affordable Care Act (ACA) is to increase competition in the health insurance markets, expanding the range of consumer choice while controlling costs. To help achieve that goal Congress created the Multi-State Plan (MSP) Program, and gave the Office of Personnel Management (OPM)—the federal civil service agency—the task of increasing competition by contracting with at least two insurance companies. This marks the first time in US history that Congress has authorized a federal agency to administer an insurance program and field health plans to compete with all other private health plans in every state.

While the stated objective of this program is to expand competition by contracting with at least two insurance carriers, in reality the federal government has contracted with only one large insurer and there is no evidence that the program has expanded competition. Indeed, the program may increase concentration in the health insurance markets. The MSP Program does not appear to level the playing field in insurance markets, as was advertised when the ACA was passed.

In a new study for the Mercatus Center at George Mason University, scholars Robert Emmet Moffit and Neil R. Meredith demonstrate that while the MSP Program grants new power to the OPM by setting standards designed to limit entry into the program, the law may decrease competition and increase consolidation in the health insurance market. Decreased competition in the health care market may lead to higher prices for consumers of health care and could revive calls for a public health insurance option.

IMPACT ON HEALTH INSURANCE MARKETS

The MSP Program may have an anticompetitive effect on the health insurance marketplace, and it expands government regulatory authority.

- Increasing regulation. OPM will have significant authority over how insurers enter exchanges, adding to an already dense network of regulatory authorities in the new health care system.

- Leaving small insurers competitively disadvantaged. Large insurers will have a competitive advantage over smaller insurers since it will be easier for them to offer coverage in all the 50 states and the District of Columbia within four years, as the program requires.

- Leaving for-profit insurers competitively disadvantaged. Nonprofit insurers will have a competitive advantage over purely for-profit insurers because the law requires at least one of the two plans offered in an exchange to be from a nonprofit, precluding for-profits from entering until a nonprofit enters.

OPM ACTS AS NEGOTIATOR AND REGULATOR

OPM acts as both an insurance negotiator and an insurance regulator.

- Negotiator. OPM must contract with insurers in a manner similar to that of the Federal Employee Health Benefits Program. Insurers are eligible to contract with the government if they meet certain statutory requirements applicable to all “qualified health plans” under the ACA. OPM can set the premium by issuing a call to insurers to provide proposals. OPM has significant authority to negotiate terms and conditions for the benefit of enrollees.

- Regulator. Insurers must meet state standards and licensing requirements, but OPM can impose additional requirements or override state requirements. This may give a competitive advantage to insurers that can meet MSP Program requirements. For example, OPM’s requirement that insurers offer coverage in every state by the fourth year of the contract will make it difficult for all but the largest insurers to enter a health insurance exchange.

NEW ROLE FOR OPM IN HEALTH POLICY

As it implements administration goals, the MSP Program will alter OPM and expand its influence in national health policy.

- Further consolidation of markets. Health insurance markets are already heavily consolidated, and OPM’s authority to selectively contract may further consolidate the industry rather than increasing competition.

- OPM as a health insurance competitor. When OPM negotiates for federal employee health insurance, it acts as an employer. Under the MSP Program the federal agency will instead act as a competitor in the health insurance market—OPM will select a small group of insurers to compete directly with other health insurance plans, in effect changing the playing field in the insurance market.

- More congressional oversight. OPM will begin to have greater congressional oversight as additional committees in Congress find that the agency’s actions fall within their purview.

- Conflict between regulatory agencies. Friction will develop between OPM and the Department of Health and Human Services, as well as state agencies, over the direction and planning of state health insurance exchanges. Conflicts will be resolved by the White House since the president is the OPM director’s superior.

- A new public option? Using its contracting authority, OPM may be able to revive the “public option,” a policy goal predating the ACA’s passage that would have created a public health insurance plan to compete directly with private plans. OPM could revive the public option by restricting entry to the market and setting premiums that make it difficult for private plans to compete.

CONCLUSION

The MSP Program is supposed to increase competition in the health insurance markets, but it is unlikely to do so. In 2014, only one issuer participated in the program, and the program is designed to attract only large insurers in its initial implementation. Indeed, particularly if it fails to deliver on the promise of increased competition, the program may result in even greater concentration in the health insurance markets. If it fails to generate genuine competition, that failure may stimulate an effort to revive a “robust” public option, a key feature of the original version of health care reform legislation championed by the Obama administration and the congressional authors of the ACA. Increased competition in the health insurance market may prove elusive under the current law, to the detriment of consumers.