- | Financial Markets Financial Markets

- | Federal Testimonies Federal Testimonies

- |

Oversight of the Federal Housing Administration's Reverse Mortgage Program for Seniors

A reverse mortgage for seniors is a reasonable idea, but should not be guaranteed by the Federal government. It is an ownership decision and the Federal government must stop trying to micromanage this decision, particularly since there is an easy alternative that does not require government guarantees.

Chairman Biggert, Ranking Member Gutierrez and Members of the Subcommittee, thank you for inviting me to testify today. My name is Anthony B. Sanders. I am Professor of Finance at George Mason University in the School of Management and senior scholar at the Mercatus Center. I was previously Director of asset- backed and mortgage-backed securities research at Deutsche Bank and the co-author of “Securitization” (with Andrew Davidson) as well as numerous economic and finance publications on housing and the housing finance system.

EQUITY EXTRACTION IN HOUSING

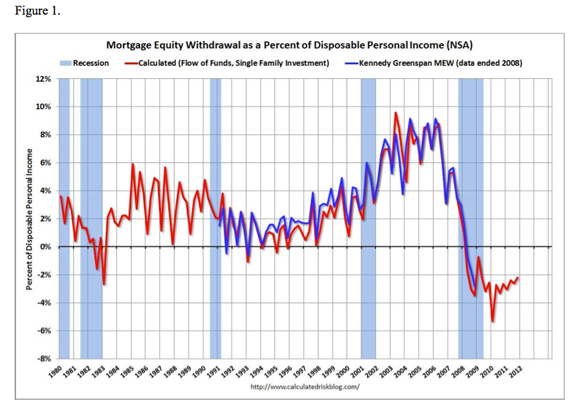

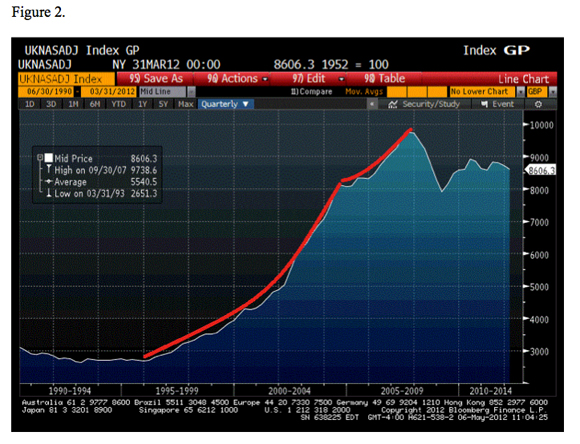

Beginning in 1995, American households began extracting equity from their housing in ever growing numbers (see Figure 1). This effectively removed the equity cushion and increased the loss severity on mortgages when the housing bubble burst.1 In the mid-to-late 1990s, the U.K. was trying to find a way to increase equity extraction from their housing market for seniors, ostensibly to diversify their senior’s investments towards bonds and equities and away from housing which tends to form bubbles that burst. The Bank of Scotland and Barclays used a shared appreciation mortgage structure that generated cash for seniors in exchange for forgoing a percentage of the appreciation of their house, enabling seniors to extract equity while staying in their homes.2 While it was enormously popular with seniors at first, complaints from consumer groups and family heirs removed some of the sparkle from this innovative approach to home equity extraction. But the real problem was that neither Bank of Scotland nor Barclays could successfully raise additional capital to fund this product by securitizing them.3 The rapid rise in housing prices in the UK (See Figure 2: from an index of 2,693.7 on December 31, 1995 to 9,738.6 on September 30, 2007 – almost a fourfold increase) resulted in seniors owing, for example, 75% of the gain in price of their house to the lender. But if house prices had dropped, the borrowers would have owed nothing and the lenders would have suffered losses. The loan balance can increase over time if an interest rate is charge on the equity extraction amount. The UK reverse mortgage (or shared appreciation mortgage) had little default risk since the borrower was receiving payments rather than making them. But default or acceleration could be triggered by failure to pay property taxes or maintain the dwelling (since the lender can have up to a 75% share in the appreciation). The latter is the moral hazard risk that borrowers, once they have their equity extraction, have less of an incentive to maintain their property.

THE FHA'S REVERSE MORTGAGE PROGRAM FOR SENIORS

The FHA has a similar reverse mortgage program for seniors to the UK SAM. With the home equity conversion mortgage (HECM), the borrower must still repay the amount owed to the lender. If the borrower has insufficient funds to pay off the HECM, the house is sold and the proceeds go to pay off the borrowed amount.4 So in this respect, the FHA’s HECM program is a UK SAM without saying so: house prices still determine the amount owed to the lender by the borrower as well as the amount that the borrower can extract.

FHA insurance for HECMs protects the lender rather than the borrower. In the event that the amount owed by the borrower exceeds the value of the property, the loss to the lender will be covered by FHA. But under the reverse mortgage program, any payments due the borrower are also protected. HUD has a legal obligation to make such payments in the event that the lender does not. So, HUD is “on the hook” for negative equity in a home (as well as defaults due to failure to pay property taxes and maintain property insurance).5

The costs to seniors, aside from the usual fees associated with lending are that FHA guaranteed HECMs may have an initial FHA Mortgage Insurance Premium (2% for HECM Standard product) as well as Annual FHA mortgage insurance (1.25% of reverse mortgage balance).6

The costs to taxpayers are the losses absorbed by HUD for the housing price shortfall, default and support. As our population ages and reverse mortgages become more common, we have to be careful about projected losses to taxpayers from yet another housing subsidy program.

THE FHA'S DILEMMA

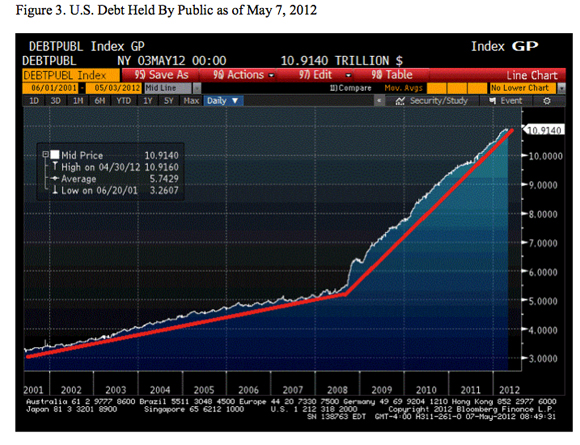

The FHA, HUD and the Federal government face enormous challenges going forward. Federal debt held by the public is currently $10.9 trillion which has increased $6 trillion since January 2007 and $4.6 trillion since President Obama took office on January 20, 2009 (See Figure 4). The Federal government has been running trillion dollar plus deficits and will continue to do so (See Figure 5) which will result in even more Federal debt. Student loan debt is over $1 trillion and growing, another federally guaranteed program.

On the housing finance front, Fannie Mae, Freddie Mac and the FHA have captured the mortgage insurance industry with over a 90% market share. Fannie Mae and Freddie Mac have cost taxpayers $170 billion thus far and counting.7 And we do not yet know the final costs of the 14 loan modification programs from the Administration, including the Attorneys General Settlement. The Administration and Congress are pressuring FHFA to allow Fannie Mae and Freddie Mac to perform principal write downs and the costs could be staggering.8

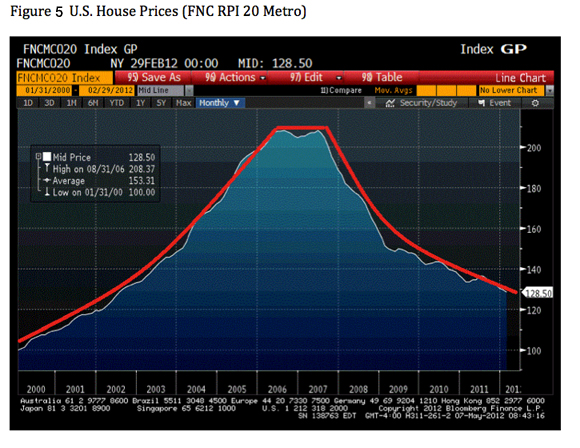

This brings us to the FHA. The FHA is deeply insolvent with insufficient capital. The FHA Is estimated to have a current net worth of –$12.05 billion and an estimated capital shortfall of $31–50 billion. The good news is that the total delinquency rate in March declined to 15.78% while the serious delinquency rate declined to 9.47%. But with the U.S. housing market is disarray and house prices continuing to decline in many markets (see Figure 6), the losses could mount for the FHA and American taxpayers even further. And with housing prices declining, the FHA continues to insuring and subsidizing 3.5% down payment mortgages.9

The question remains as to why the Federal government is guaranteeing and subsidizing reverse mortgages for seniors. Stated differently, why do taxpayers have to subsidize seniors who want to stay in their homes when the simple solution is to let seniors sell their home and either rent another dwelling or purchase a smaller dwelling that meets their needs?

I am not against reverse mortgages as an equity extraction tool. But I do not see any reason for the Federal government to guarantee and subsidize it. And we need to stop micromanaging the home ownership decisions for American households. The Clinton Administration tried it in 1995 with the National Homeownership Strategy that contributed to a housing bubble and burst.10 Now Fannie Mae, Freddie Mac and FHA are raising credit standards encouraging those who can’t get credit to rent.11 And now residential rents are rising rapidly in urban areas.12

SUGGESTIONS

At a minimum, the Federal government should get out of the reverse mortgage insurance and subsidization business, particularly since there is an easy alternative: seniors sell their home and buy a smaller dwelling or rent.

We have thrown enormous subsidies at the housing market and have tried to steer households into ownership, then renting and now steering seniors toward equity extraction. We need to think about how much of the housing market should be subsidized (mortgage interest deductions, subsidized mortgage insurance, low down payment loans, etc.). Clearly, the massive subsidization has distorted housing and housing finance market and changes should be made.

There are numerous proposals for ending the government housing monopoly.13 These include eliminating Fannie Mae and Freddie Mac or converting them to a public utility and reinsurance company. But no matter how we deal with the government housing monopolies, we must address how much we want to subsidize housing going forward.

SUMMARY

A reverse mortgage for seniors is a reasonable idea, but should not be guaranteed by the Federal government. It is an ownership decision and the Federal government must stop trying to micromanage this decision, particularly since there is an easy alternative that does not require government guarantees.

Appendix: Figures

Footnotes:

1 https://files.nyu.edu/sml8/public/Laufer_EquityExtractionDefault_111611…

2 http://www.telegraph.co.uk/finance/personalfinance/borrowing/mortgages/…

3 http://www.sciencedirect.com/science/journal/10511377/14/3

4 HUD announced on December 2, 2011 the extension of the $625,500 limit for Home Equity Conversion Mortgages (HECM) through calendar year 2012.

5 When the reverse mortgage loan balance gets to 98% or more of the "maximum claim amount", which is the maximum amount that can be collected, lenders are allowed to assign the loan to HUD and be paid the balance. HUD then assumes responsibility for making any additional payments that are due the borrower. HUD will also take over responsibility if, for some reason, the lender cannot make the required payments.

6 http://portal.hud.gov/hudportal/HUD?src=/program_offices/housing/sfh/he… and http://www.genworthreversemortgage.com/genworth/fees

7 http://www.washingtonpost.com/business/mortgage-giant-freddie-mac-asks-…- 12b-loss-in-q1/2012/05/03/gIQAkkplyT_story.html

8 http://confoundedinterest.wordpress.com/2012/05/03/cummings-letter-to-d…- should-do-principal-writedowns-please-be-careful/

9 http://confoundedinterest.wordpress.com/2012/04/27/fhas-instant-underto…- declining-home-price-environment/

10 http://confoundedinterest.wordpress.com/2012/05/01/homeownership-falls-…- great-leap-forward/

11 http://confoundedinterest.wordpress.com/2012/05/01/the-tightening-of-th… 12 http://www.latimes.com/business/la-fi-renters-nightmare-20120506,0,7137…

13 See https://www.mercatus.org/publication/house-cards, https://www.mercatus.org/events/reforming-gses-fannie- freddie-and-future, http://reason.org/news/show/trust-in-mortgage-backed-securities,

Related Content

- | Financial Markets Financial Markets

- | Books Books

House of Cards: Reforming America's Housing Finance System