Whether this is a fad or something deeper, behavioral economics is already making a noticeable impact on several regulatory fronts, most notably in consumer finance, enough to be labeled by some as the “new paternalism.”

Introduction

Over the last few decades, psychologists have challenged economists on the notion that people always make rational decisions. Economists, of course, recognize that people are not always perfectly rational. Modeling them as such often adds to the precision of the model’s result, without reducing its relevance. Put another way, economists assume that most of the time people act rationally enough that modeling them as perfectly rational does not get in the way of discovering new insights into human behavior.

Nevertheless, behavioral psychologists found this rational choice–based method wanting and have amassed a sizeable body of research demonstrating certain “anomalies” in laboratory studies that break from rational choice predictions. For example, behavioral psychologists Amos Tversky and Daniel Kahneman famously claimed that people are susceptible to certain biases that make them more risk averse to gaining wealth (and more risk seeking in losing it) than the standard rational choice model would predict. Furthermore, they claimed that framing choices in different ways elicits inconsistent behavior.

These ideas eventually coalesced into the field known as “behavioral economics” and have since made their way into public policy. An example of this is the Consumer Financial Protection Bureau (CFPB), which regulates consumer credit products, such as mortgages and credit cards, and consumer credit providers, such as banks, payday lenders, and cell phone providers. This agency was largely influenced by behavioral economics in setting its organizational mission and goals, such as protecting consumers from exploitation and manipulation by credit providers.

Despite these behavioral-based foundations (or perhaps because of them, as I will explain below), the CFPB has been criticized from both sides of the political divide for its aggressive bureaucratic expansion and failure to adhere to its original congressional mandate. Furthermore, the actions of the agency have directly led to the significant reduction in volume of certain credit products (e.g., residential mortgages, auto loans) in a manner that calls into question whether the agency is helping or harming consumers.

The purpose of this paper is to outline the impact of behavioral economics on public policy by examining its central influence on the CFPB. In particular, it explains how behavioral ideas have been converted into policies that fail to account for actual government practice, which has led to mixed results for consumers. While understanding just how people are susceptible to market influence is important, the premature application of behavioral economics to public policy risks undermining the goal of helping consumers.

What is Behavioral Economics?

Behavioral economics, simply put, is psychology applied to traditional economic concepts. What is novel about this approach is that it couches its critique in a language economists can understand. So, for example, when people are more likely to insure against risk because they fear losses more than they enjoy gains, behavioral economists position this outcome within the standard utility maximization framework employed by economists, but with the added flourish of describing such behavior as exhibiting “loss aversion.”

Best-selling books, including Nudge, Predictably Irrational, and Thinking, Fast and Slow, have provided the public with accessible entries into the world of behavioral economics. Be it by showing how we process information and awareness through two corresponding mental systems (Thinking, Fast and Slow) or exposing why we react differently while in a panicked state (Blink) or demonstrating how government can be used to improve our everyday choices (Nudge), these books represent a growing and popular topic of inquiry among academics, policymakers, and even the general public.

Whether this is a fad or something deeper, behavioral economics is already making a noticeable impact on several regulatory fronts, most notably in consumer finance, enough to be labeled by some as the “new paternalism.” For example, the CFPB implemented a provision that defined so-called “qualified mortgages,” a category of loans in which lenders adhere to certain parameters such as setting nonadjustable interest rates, determining the borrower’s ability to repay, etc. This is all predicated on the assumption that consumers do not understand what they are agreeing to—and that assumption, at the very least, constitutes a departure from the traditional justification for regulatory intervention, which is market failure.

This policy outcome, like others from the CFPB as noted below, can be traced back to behavioral roots. In this case, it is from the book Nudge, which outlines a number of possible “soft” interventions into the marketplace to correct for common mistakes people make. The authors of Nudge, Richard Thaler and Cass Sunstein, have done more than anyone else to bring behavioral economics from mere laboratory studies of human behavior out into the world of policy. In chapter 8 of Nudge, they criticize mortgage products with low introductory interest rates and balloon payments as being too complicated for consumers to understand. They argue that products with simpler terms and conditions (e.g., a 30-year fixed mortgage) make choices easier for consumers and thus provide the standard by which all alternatives should be compared.

The 2008 scribbling of two behavioral economists has become our new reality, as the financial industry must now work within regulations that penalize mortgage products that fail to adhere to federal guidelines. Qualified mortgages are restricted to those with fixed terms and interest rates. Mortgage products with features like adjustable rates and amortization fees are unlikely to pass muster. Banks can, of course, offer nonqualified mortgages, but they risk being sued by the borrower if they default, and there is a stigma associated with such a product label.

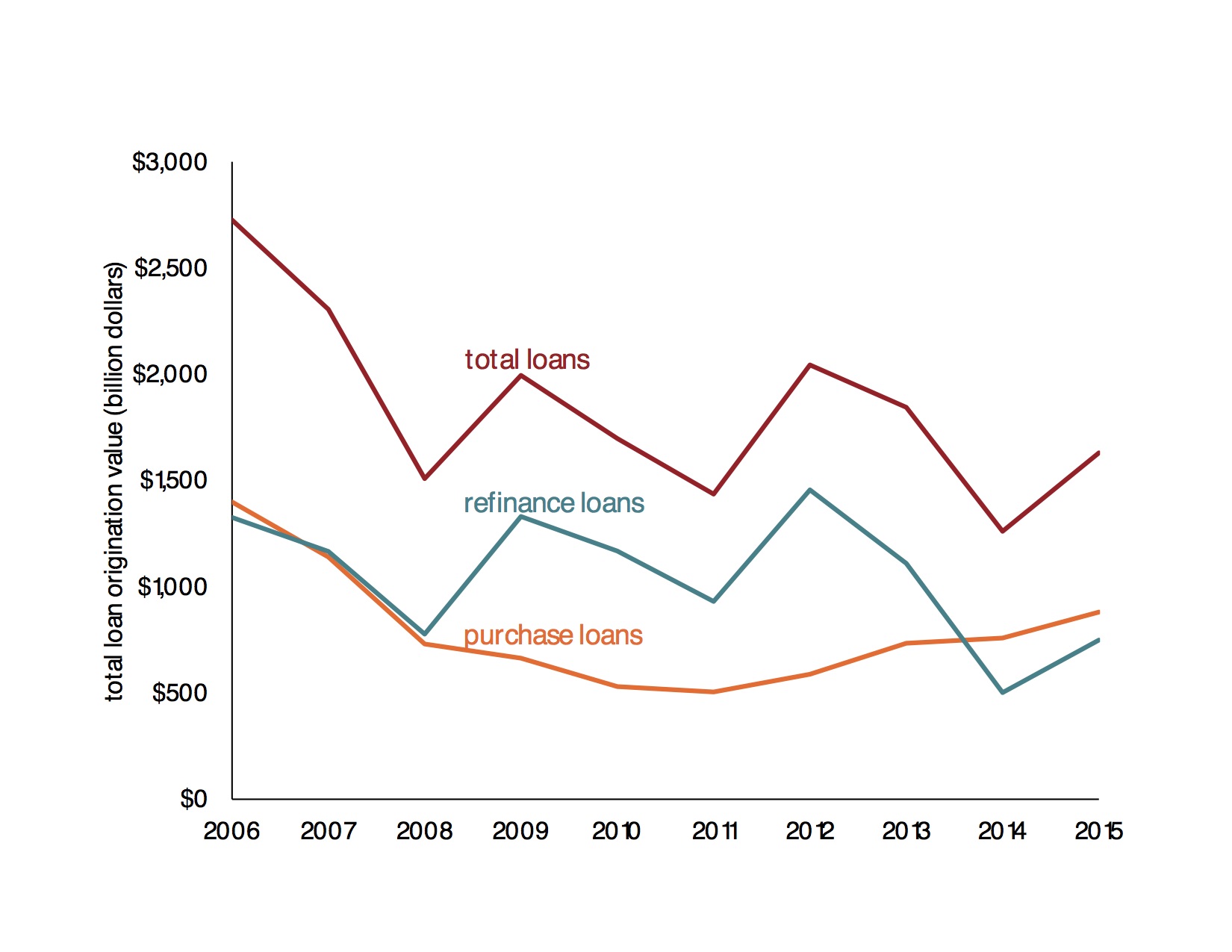

Moreover, much of the financial industry has reacted to the implementation of the rule by withdrawing from the mortgage market altogether. The figure below, generated from data provided by the Mortgage Bankers Association, shows a steep reduction in the volume of residential loans in 2013, as originally reported by RealtyTrac.com. This decline is most pronounced with refinancing mortgage loans. This trend is in tandem with the implementation of the Ability-to-Repay and Qualified Mortgage Rule on January 10, 2014, which formally defined “qualified mortgages.”

Figure 1. US Residential Loan Origination Trends

Source: Mortgage Bankers Association, “Annual Mortgage Origination Estimates,” February 2016.

The recent uptick in these originations indicates that the market may be finally adjusting to the new rules, though it is unclear whether volume will return to its previous level.

This may be all well and good for those who believe we should all consume “plain vanilla” products. But for those who understand—and indeed, conduct their business on—the flexibility that alternative credit products provide, the new regulations stifle credit markets in a way that most assuredly hurts not just the financial industry but consumers, too.

Behavioral Economics in the Consumer Finance Industry

These interventions into what behavioral economists describe as the “choice architecture” of the marketplace constitute a very real and problematic constraint for the financial industry, as the figure above illustrates. This stems from the work of the CFPB—one of Washington’s newest agencies and a major part of the larger Dodd-Frank Wall Street Reform and Consumer Protection Act—which regulates virtually any consumer practice in the financial industry. Even practices that the agency was explicitly told to ignore, such as auto lending, have become significant targets for the agency’s efforts.

That this new agency is so aggressive should be no surprise given its lack of congressional oversight or budgetary approval. Indeed, these features are so extraordinary that the constitutionality of the CFPB is now facing a challenge in the US Court of Appeals for the DC Circuit. While Congress is certainly no safety valve against bureaucracy, it can create limits to certain excesses, particularly when those excesses affect the interests of constituents. The fact that the CFPB need not concern itself with the interests of the market participants it regulates, or the full range of consumers these regulations ultimately impact, is in large part responsible for the mixed results.

What is novel about the agency is that its roots go deeply into the world of behavioral economics. Senator Elizabeth Warren, who was the driving force behind the agency’s inception, relied on behavioral assumptions in making her original case for the agency. Senator Warren later teamed up with well-known behavioral economist Oren Bar-Gill in an expanded law review article to make the case for the need for an agency dedicated to consumer finance. They cited cognitive shortcomings that people exhibit—including dealing poorly with complicated information, displaying inertia in switching to new products, and not providing for their true long-term interests—as justifications for such an agency. The agency would, therefore, be justified in targeting products based upon a preconceived notion of what is best for the consumer (as occurred in the example above with qualified mortgages).

What is “best” for the consumer is defined by the agency itself. Rulemaking has largely been opaque at best, not transparent, though one interesting fact is that Nudge coauthor Richard Thaler is an official member of the agency’s advisory board. In fact, many of the targets of Nudge have become the targets of the agency. In addition to complex mortgages, the agency has targeted add-on products like credit card insurance and overdraft protection. These latter products represent what behavioral economists call “shrouded fees,” which they claim are meant to mislead consumers into making unwise purchases.

In congressional testimony, law professor Todd Zywicki explained how the resulting decline in overdraft fees has also caused a precipitous decline in free checking accounts. Since the passage of Dodd-Frank, the number of banks offering free checking accounts has declined by half, with the accompanying result that banks have doubled the required account balance needed to maintain these checking accounts.

The underlying trouble with closing credit channels is that this does nothing to boost consumer income. Instead, it simply takes away “undesirable” choices, as defined by bureaucrats, without replacing those choices with more viable ones.

Overdraft protection in general has been a constant source of discussion within the CFPB and the Federal Reserve (Fed), where the CFPB is located. In 2010, the Fed required all banks to ask their customers to “opt in” to continue using overdraft services. Behavioral economists claimed that survey evidence indicated people do not really value the service and would not opt in if asked to use the service directly. But in fact, the opposite occurred, as those who most used the service were three times as likely to opt in as normal users. The regulation of overdraft protection has since passed on directly to the CFPB, which has only continued the trend the Fed started.

This example would seem to challenge the claim that people are not rational in their decision-making. Either people are using a service that does not benefit them because they are not rational, and therefore should become aware of this when given information required by regulators, or they were rational in using the service in the first place and would, therefore, obviously choose to opt back into the service when asked.

Some behavioral economists have instead argued that these supposed “high-value” users are only highly deluded and are now calling for restrictions on overdraft fees in general, despite the fact that other evidence shows closing off such channels encourages the use of payday lenders, another perennial target of the CFPB, or even loan sharks.

This exposes a larger issue with using behavioral economics as a platform for policy prescription—it is not clear ex ante what behavior is considered rational and what is not. Shifting the definition of what constitutes rational behavior undermines the scientific basis for behavioral remedies. The result is a series of just-so stories that can appeal to the very same biases behavioral economics seeks to redress (i.e., confirmation bias among regulators).

Why Should the Financial Industry Care?

The massive number of financial regulations that emerged from Dodd-Frank has perhaps obscured the growing influence of behavioral economics in this policy arena. But once adopted, regulations can become very hard to undo, particularly when they reflect a larger political movement, in this case propelled by a growing portion of the academy. Bottom line, behavioral economics is here to stay and will likely continue to drive regulatory reform in financial markets.

While this will be welcomed by some who appreciate a more nuanced framework for addressing consumer missteps, others will be troubled by the idea that an agency can target products based on bureaucrats’ ideas of what is best for the consumer. The examples above show how this heavy-handed approach, guided by academic thinking, can lead to poor outcomes—not only for the financial industry but for financial consumers as well.

The example of overdraft protection specifically demonstrates the growing influence of behavioral economics in this policy area. Use of overdraft protection declined in 2010, resulting in a loss of $2 billion to the industry itself. This is why a better framework is needed for dealing with consumer finance. Behavioral economics will most assuredly be part of the discussion. But that should be tempered by an understanding of how politics and regulatory reform work in practice and what constraints on government activity are needed to keep consumers’ true interests at heart.

The financial industry can provide help in this area in a number of ways. First, it can provide its own set of private nudges to help consumers make choices—but in a way that reflects the greater feedback and competitive pressures of the marketplace, as opposed to the less nuanced direction of government bureaucracy. To a large extent, the industry already does provide such nudges, but pointing to examples where “choice architecture” is clearly improved for the consumer could in part help challenge the notion that only government can improve people’s choices.

On that note, the financial industry should be prepared to show evidence that its consumers are indeed happy with the products they receive. Marketplace solutions have already arrived with rating sites like Angie’s List, Yelp, etc. But the industry has a still greater burden to bear. Instead, a product must coincide with what regulators believe to be appropriate products. Greater specificity from regulators in what they are looking for in the set of choices open to the consumer would be ideal, though they rarely pronounce this explicitly. Firms face the uncertainty of what regulators will “choose” for consumers based on the questionable advice of behavioral economists.

This brings us to regulators themselves. Regulators should be challenged on what criteria they use to define their “normal” consumer. Studying just how people arrive at their choices and what parts of the environment trigger different responses is fascinating work that can potentially lead to a better set of choices for consumers. But premature emphasis on policy solutions risks stretching this new work beyond its competence. After all, if people have limited abilities to make decisions, then we must understand not just the behavior of financial companies and financial consumers, but the behavior of financial regulators as well. Only when we study the “choice architecture” of all three can we begin to understand how to arrive at better choices in practice.