- | Financial Markets Financial Markets

- | Public Interest Comments Public Interest Comments

- |

Comment on the Small Business Lending Market

I appreciate the opportunity to respond to the Bureau of Consumer Financial Protection’s (CFPB) request for information on the small business lending market. The Mercatus Center at George Mason University is dedicated to bridging the gap between academic ideas and real-world problems and to advancing knowledge about the effects of regulation on society. This comment, therefore, does not represent the views of any particular affected party or special interest group but is designed to assist the CFPB as it considers whether—and, if so, how—to proceed with rulemaking regarding lending to small businesses. More generally, this comment seeks to assist the CFPB in embracing a regulatory approach that serves small businesses by fostering competition, innovation, and access.

To assist the CFPB in its examination of the small business credit market, I wish to share some preliminary results from a survey of small businesses conducted by the Mercatus Center and Hanover Research in December of 2016. The survey asked 445 respondents questions regarding their past experience seeking capital for their firm, their recent or current experiences seeking capital, their willingness to consider innovative methods of capital access in the future, and their opinions on the state of the small business capital market. The results are informative as to the state of small business access to capital and the expectations, concerns, and preferences of small businesses. I am happy to share the final survey report once it is completed.

Findings

General Observations about Small Business Capital Access

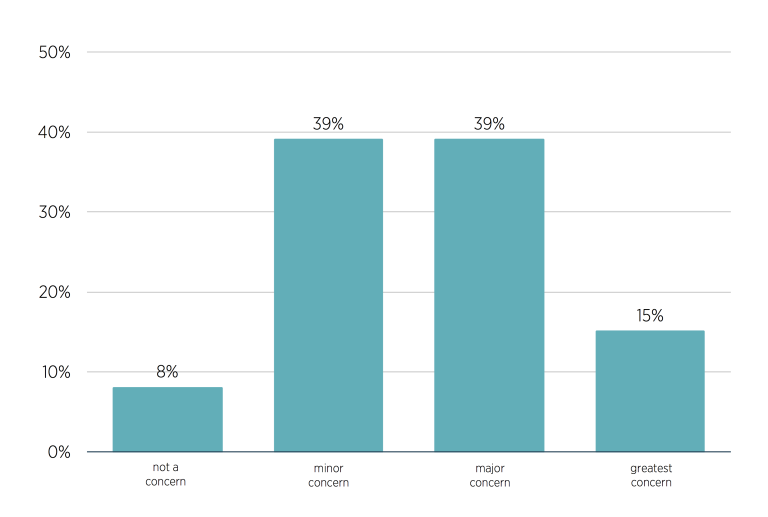

A majority of firms surveyed believe that the ability to access capital is either the firm’s greatest concern (15 percent) or a major concern (39 percent). A significant minority of firms (39 percent) consider the ability to access capital to be a minor concern, with a small percentage of firms (8 percent) considering it not a concern at all. (N = 445.) See figure 1.

Figure 1. How Big a Concern Is the Ability to Access Capital for the Company?

Source: Author’s rendering, based on data from the 2017 Survey on Small Business Capital Access.

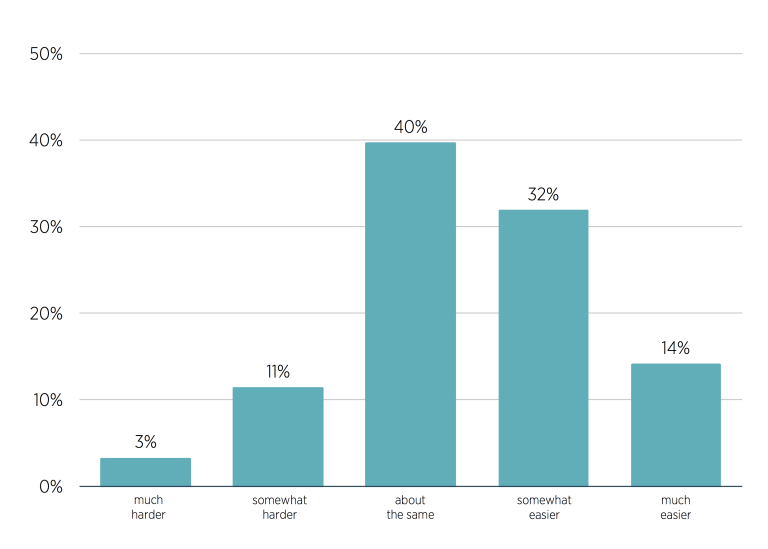

A plurality of firms (40 percent) believe that obtaining access to capital is about the same as it has been for the past five years, while 14 percent believe it has gotten harder and 46 percent believe it has gotten easier. (N = 445.) See figure 2.

Figure 2. Has Obtaining Access to Capital Become Easier or Harder Than in the Past Five Years?

Source: Author’s rendering, based on data from the 2017 Survey on Small Business Capital Access.

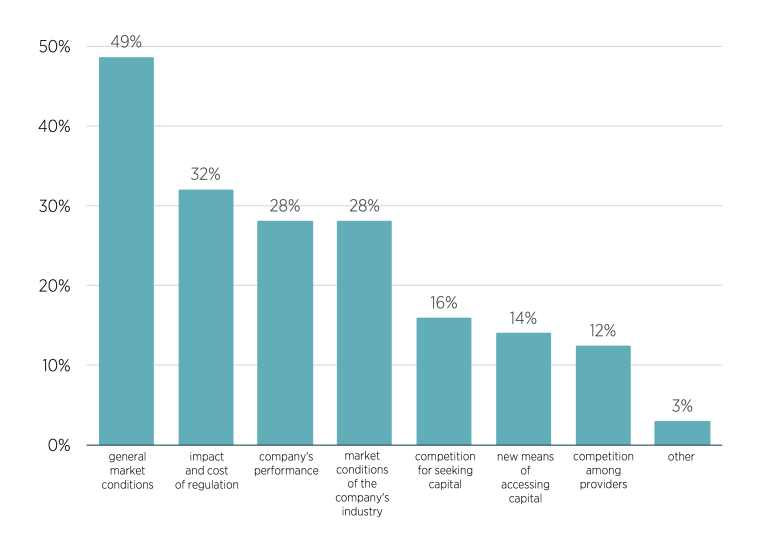

Regulation is the second most cited factor affecting the ability of firms to access capital (32 percent), coming behind general market conditions (49 percent) and ahead of market conditions for the company’s industry (28 percent) and the company’s performance (28 percent). (R = 807, N = 445.) See figure 3.

Figure 3. What Affects the Ability to Access Capital?

Source: Author’s rendering, based on data from the 2017 Survey on Small Business Capital Access.

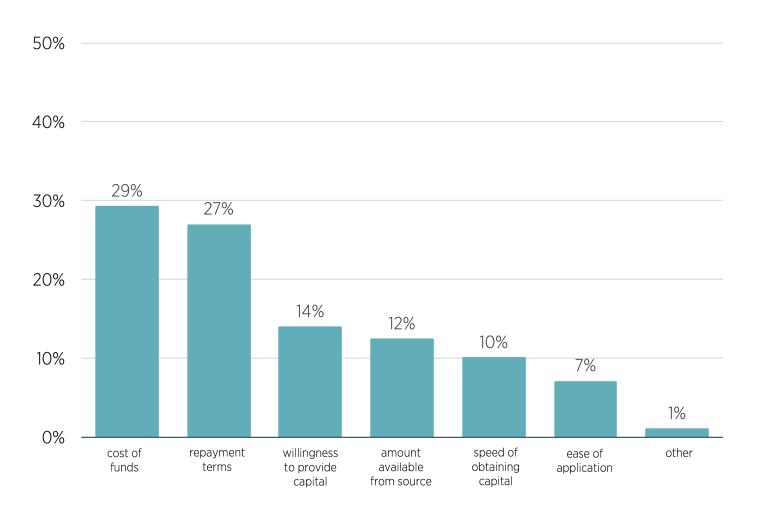

Firms care about the cost of capital, but that is not the only factor they consider when deciding how to obtain funds. Cost of funds is the most frequently cited factor listed by respondent firms (29 percent). However, other factors, including repayment terms that fit the firm’s needs (27 percent), willingness to provide capital (14 percent), amount of money available from the source (12 percent), and speed of obtaining capital (10 percent), were also listed. (N = 445.) See figure 4.

Figure 4. What Is Most Important to the Company When Deciding What Type of Capital to Seek?

Source: Author’s rendering, based on data from the 2017 Survey on Small Business Capital Access.

Observations on Firm-Specific Efforts to Raise Capital

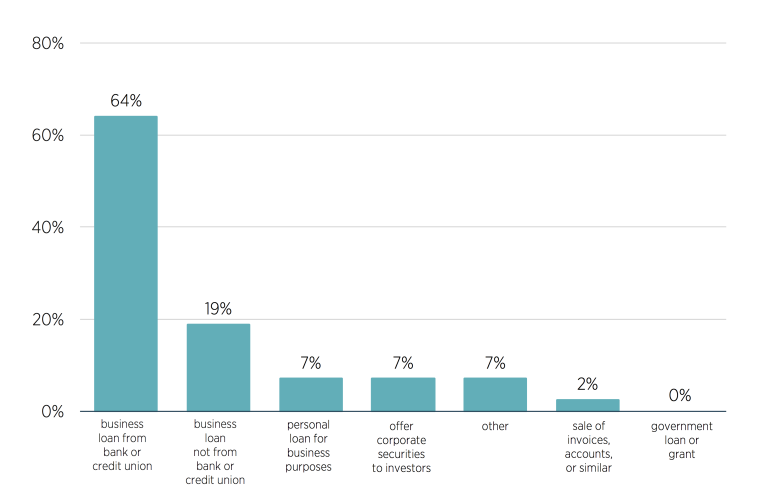

The market for small business capital is highly debt driven. Among respondent firms that recently sought capital, 64 percent sought a business loan from a bank or credit union, 19 percent sought a business loan from a nonbank lender, and 7 percent had an employee, officer, or owner seek a personal loan for business purposes. (R = 46, N = 43.) See figure 5.

Figure 5. What Type or Types of Outside Capital Did the Company Seek Most Recently?

Source: Author’s rendering, based on data from the 2017 Survey on Small Business Capital Access.

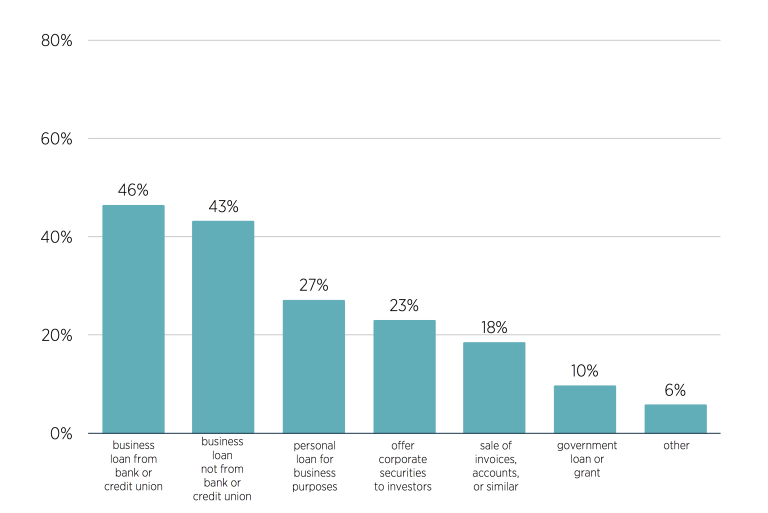

Among respondent firms currently seeking capital, 46 percent sought a business loan from a bank or credit union, 10 percent sought a business loan from the government, 43 percent sought a business loan from a nonbank lender, and 27 percent had an employee, officer, or owner seek a personal loan for business purposes. (R = 234, N = 136.) See figure 6.

Figure 6. What Type of Outside Capital Is the Company Seeking?

Source: Author’s rendering, based on data from the 2017 Survey on Small Business Capital Access.

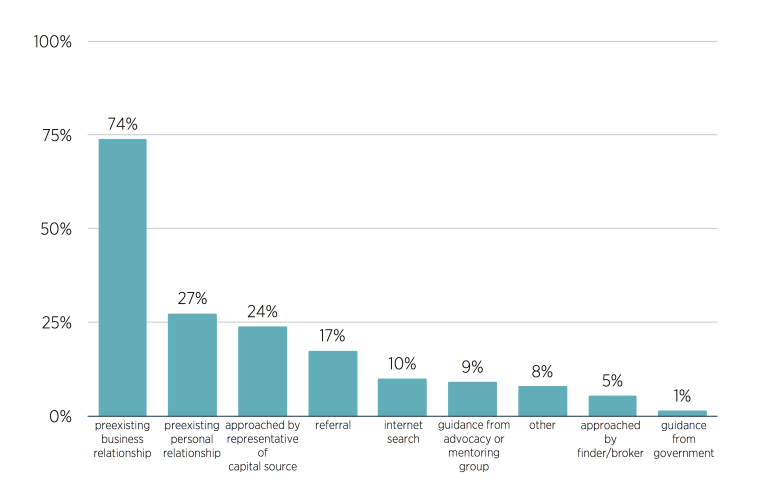

Firms rely heavily (though not exclusively) on existing relationships when deciding what source of capital to approach. Among respondent firms that recently sought capital, 74 percent targeted a source of capital on the basis of a preexisting business relationship; 27 percent on the basis of a preexisting personal relationship between an employee, officer, or owner of the firm and the capital source; and 17 percent on the basis of a referral. Further, 24 percent of firms targeted a source of capital because they were approached by a representative of the capital source, and 10 percent targeted a source based on an internet search. (R = 76, N = 43.) See figure 7.

Figure 7. How Did the Companies That Recently Sought Capital Determine What Source of Capital to Approach Initially?

Source: Author’s rendering, based on data from the 2017 Survey on Small Business Capital Access.

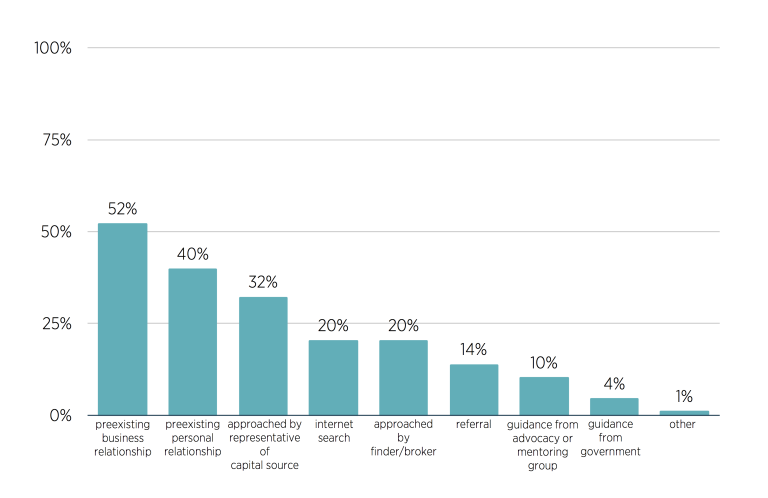

Among respondent firms currently seeking capital, 52 percent targeted a source of capital on the basis of a preexisting business relationship; 40 percent on the basis of a preexisting personal relationship between an employee, officer, or owner of the firm and the capital source; and 14 percent on the basis of a referral. Interestingly, firms currently seeking funds were more influenced by an approach from either a representative of the source of capital (32 percent) or a finder or broker (20 percent). Additionally, 20 percent of firms currently seeking funds reported that they determined the source they would target on the basis of an internet search. (R = 262, N = 136.) See figure 8.

Figure 8. How Did the Companies Currently Seeking Capital Determine What Source of Capital to Approach Initially?

Source: Author’s rendering, based on data from the 2017 Survey on Small Business Capital Access.

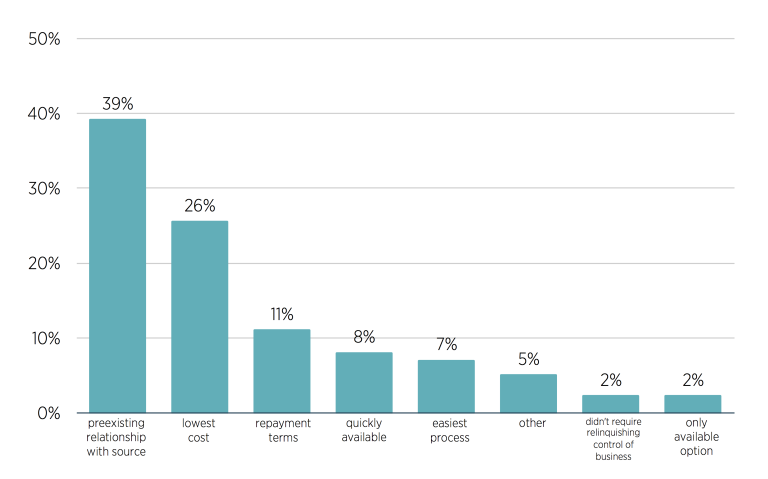

However, firms ultimately choose what type of capital to take on the basis of more practical criteria. Among respondent firms that recently sought capital, 39 percent ultimately chose the source based on the firm’s preexisting relationship, while 26 percent chose the lowest-cost option, and 11 percent chose the option that offered the best repayment terms. (N = 41.) See figure 9.

Figure 9. What Was the Main Reason the Companies That Recently Sought Capital Chose the Source of Capital They Ultimately Obtained?

Source: Author’s rendering, based on data from the 2017 Survey on Small Business Capital Access.

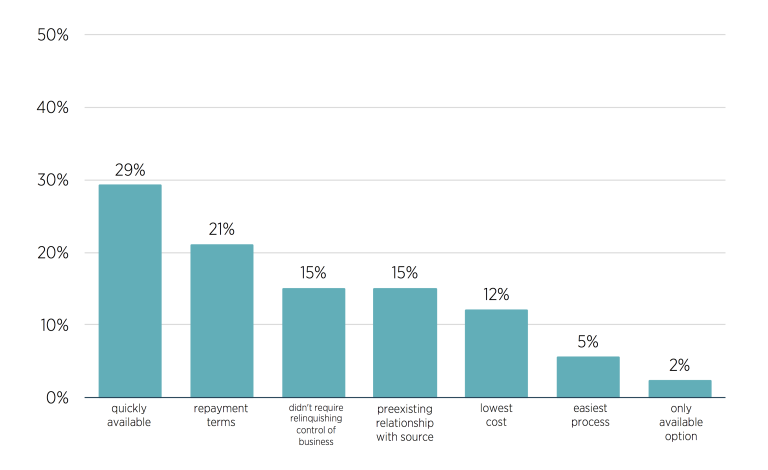

Among firms currently seeking capital, only 15 percent chose the source of funds based on a preexisting relationship, while 29 percent chose the source that was most quickly available, 21 percent chose the source that offered the best repayment terms, and only 12 percent selected the lowest-cost option. (N = 107.) See figure 10.

Figure 10. What Was the Main Reason the Companies Currently Seeking Capital Chose the Source of Capital They Ultimately Obtained?

Source: Author’s rendering, based on data from the 2017 Survey on Small Business Capital Access.

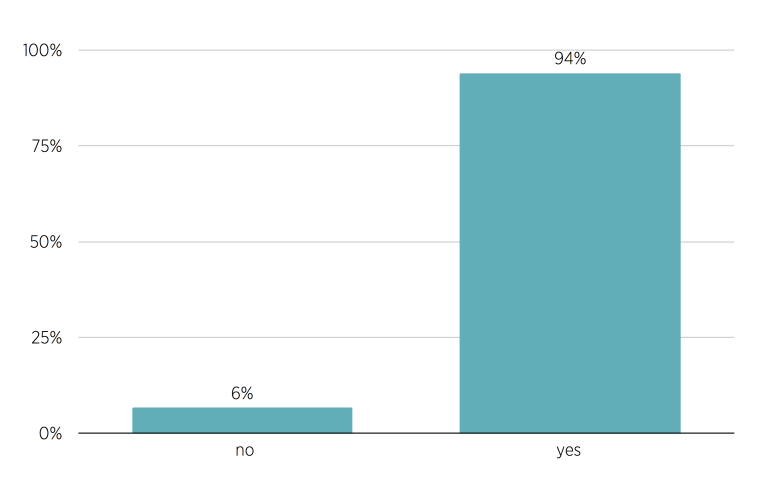

Firms report good, but not universal, success at obtaining capital from their initial target. Among firms that recently sought capital, 94 percent reported they were successful in obtaining capital from their initial source. (N = 43.) See figure 11.

Figure 11. Were the Companies That Recently Sought Capital Successful in Obtaining Capital from Their Initial Target?

Source: Author’s rendering, based on data from the 2017 Survey on Small Business Capital Access.

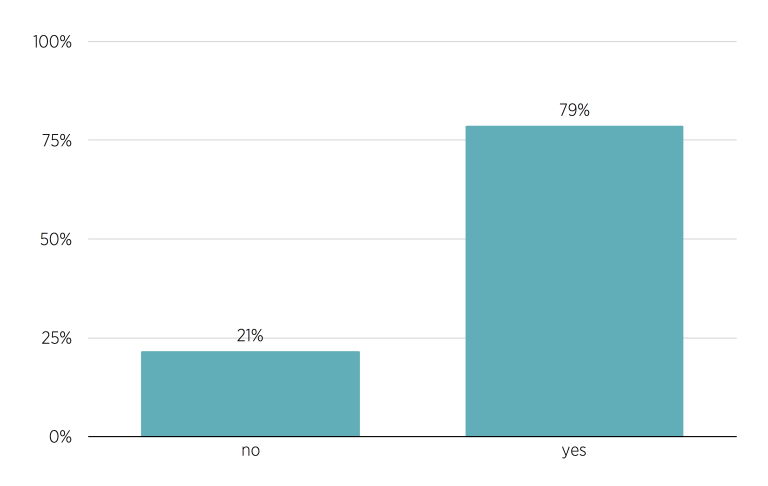

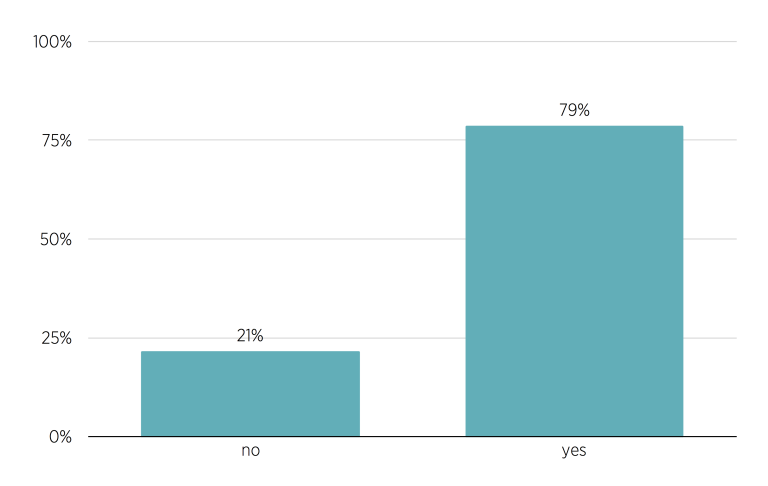

Among firms currently seeking capital, the success rate was lower, at 79 percent (N = 136). Among these firms, those seeking $100,000 or less had less success (65 percent, N = 40) obtaining capital from their initial target, compared with firms seeking between $100,000 and $500,000 (83 percent, N = 61) and those seeking over $500,000 (86 percent, N = 35). See figure 12.

Figure 12. Were the Companies Currently Seeking Capital Successful in Obtaining Capital from Their Initial Target?

Source: Author’s rendering, based on data from the 2017 Survey on Small Business Capital Access.

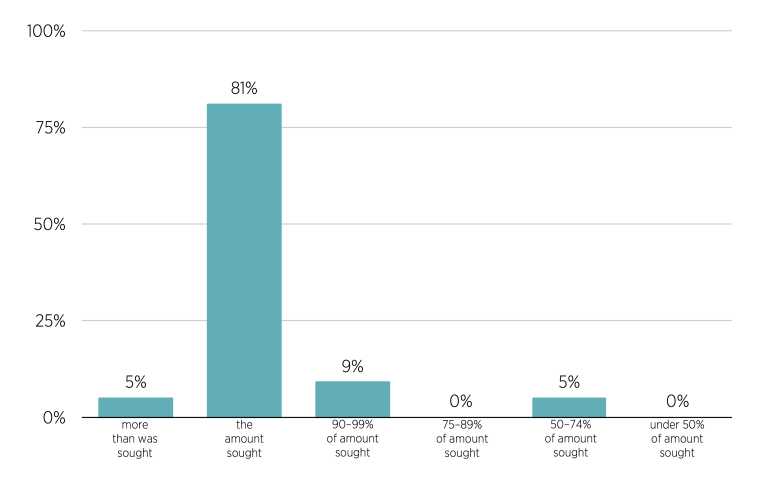

Firms that do receive capital are frequently, but not universally, able to get the amount they sought or close to it. Among firms that recently sought and obtained capital, 81 percent were able to obtain the amount they were looking for. An additional 9 percent were able to obtain between 90 and 99 percent of what they were looking for. Further, 5 percent of firms received more capital than they initially sought, while 5 percent were able to obtain only 50–74 percent of what they were looking for. (N = 41.) See figure 13.

Figure 13. How Much Capital Did the Firms That Recently Sought Capital Ultimately Receive in the Most Recent Effort?

Source: Author’s rendering, based on data from the 2017 Survey on Small Business Capital Access.

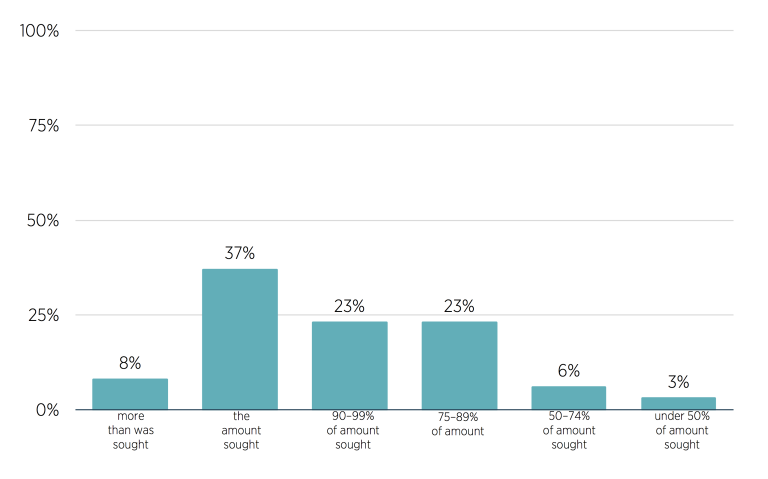

Among firms currently seeking and able to obtain capital, however, only 37 percent were able to obtain the amount they were looking for, with 23 percent able to obtain 90–99 percent and another 23 percent able to obtain 75–89 percent. In addition, 8 percent of firms received more than they initially sought, while 9 percent were able to obtain only 74 percent or less of what they sought. (N = 107.) See figure 14.

Figure 14. How Much Capital Did the Firms Currently Seeking Capital Ultimately Receive in the Most Recent Effort?

Note: Total respondents = 107.

Source: Author’s rendering, based on data from the 2017 Survey on Small Business Capital Access.

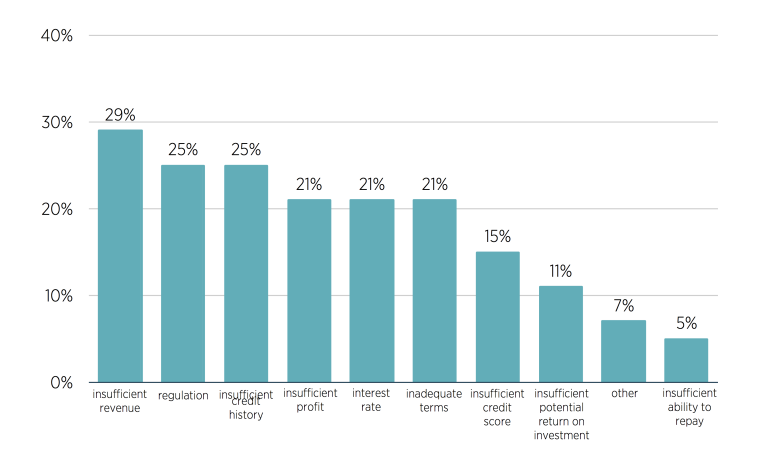

Regulation is a significant reason why some firms cannot access capital. Among firms that were not able to obtain some or all of the capital they sought, the most common reason given was that the firm had insufficient revenue (29 percent), but regulation preventing the source of capital from making a loan or investment (25 percent) and the firm having an insufficient credit history (25 percent) were the next most common reasons. (R = 114, N = 63.) See figure 15.

Figure 15. Why Was the Company Not Offered Some or All of the Capital Initially Sought?

Note: Total respondents = 63; total responses = 114. All respondents are currently seeking capital.

Source: Author’s rendering, based on data from the 2017 Survey on Small Business Capital Access.

Firm Interest in Innovative Means of Capital Access

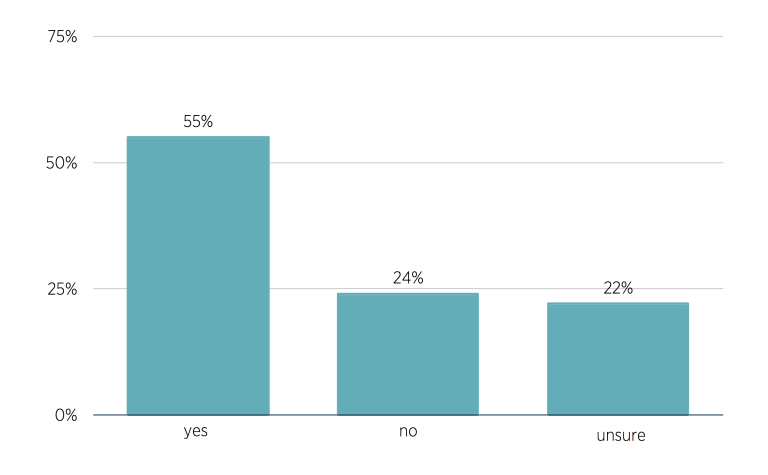

Firms are interested in innovative means of obtaining capital. A majority of firms (55 percent) would consider seeking capital in the future from a nonbank internet-based lender, 22 percent of firms are unsure, and 24 percent are not interested. (N = 445.) Firms that are currently seeking $100,000 or less were more open to the possibility (60 percent yes, 16 percent unsure) than firms seeking between $100,000 and $500,000 (56 percent yes, 13 percent unsure) or those seeking over $500,000 (55 percent yes, 14 percent unsure). (N = 180.) See figure 16.

Figure 16. Would the Company Consider Taking a Small Business Loan from a Nonbank Internet-Based Lender?

Source: Author’s rendering, based on data from the 2017 Survey on Small Business Capital Access.

Implications

These findings suggest several things about the small business credit market that the CFPB should consider as it evaluates whether regulation is appropriate. First, the cost of regulation matters. Among firms that were not able to access some or all of the capital they sought, regulation was tied as the second most commonly cited reason. The CFPB should keep this risk in mind because regulation, no matter how well meaning, could restrict access to financial capital.

Second, small businesses are often willing to pay for speed or convenience. Among firms currently seeking capital, cost was not the most cited factor for why a particular source of capital was chosen. This reflects the reality that cheap capital provided too late or with ill-fitting repayment terms is not as useful as more expensive capital available when it is needed and with good repayment terms. The CFPB should avoid fixating on cost as a measure of whether a type of capital is meeting the needs of small businesses and instead remember that small businesses are best positioned to know what characteristics are most important to them when they select capital.

Third, small businesses are looking for innovative solutions. A majority of firms surveyed were open to obtaining capital via a nonbank online lender, with the highest levels of interest among firms seeking relatively low amounts of money. The CFPB should avoid pursuing regulations that risk stifling innovation and entry into the small business capital market, as such regulations would deny firms the benefits of innovation, competition, and choice.

Conclusion

The survey data indicate that while small businesses are generally able to access at least some capital, some firms are excluded. There is a broad desire for new and innovative means of capital access. The CFPB, in its well-intentioned regulatory efforts, should be careful to avoid unduly burdening small businesses and the lenders who serve them.

Rule details

Agency: Bureau of Consumer Financial Protection

Proposed: May 10, 2017

Comment period closes: September 14, 2017

Submitted: September 6, 2017

Docket Number: CFPB-2017-0011