- | Government Spending Government Spending

- | Policy Briefs Policy Briefs

- |

POLICY SPOTLIGHT: Enacting True Tax Reform, Not Just Tax Cuts

In this Policy Spotlight series, Mercatus scholars provide a high-level overview of their positions on key issues facing our nation’s policymakers.

The dense and complicated United States tax code—and the specter of economic engineering it embodies—severely distorts individual and business decisions, hampers job creation, and constrains both economic growth and tax revenue. It is time for serious and comprehensive tax reform.

The US federal government needs a more coherent and sustainable revenue system. True tax reform is about more than just cutting tax rates or increasing revenue. Temporary tax cuts will fail to solve the inherent problems in the tax system. Predictable, stable tax policy that focuses less on directing private decision-making is an essential prerequisite to long-term economic growth.

Elements of a Successful Tax System

Research commonly points to four elements of a successful revenue system:

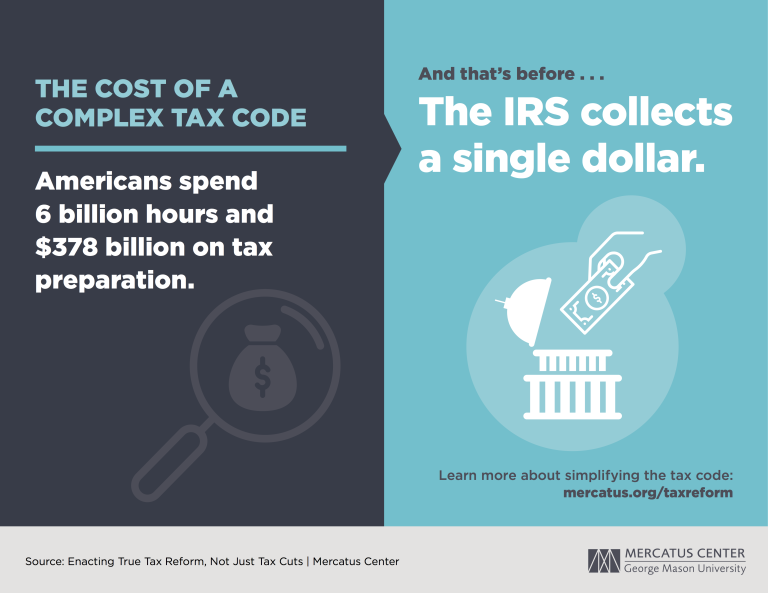

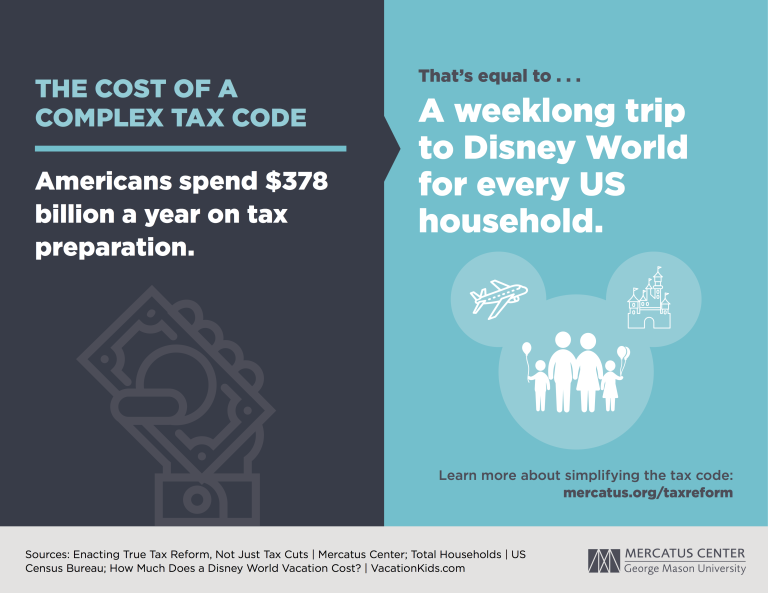

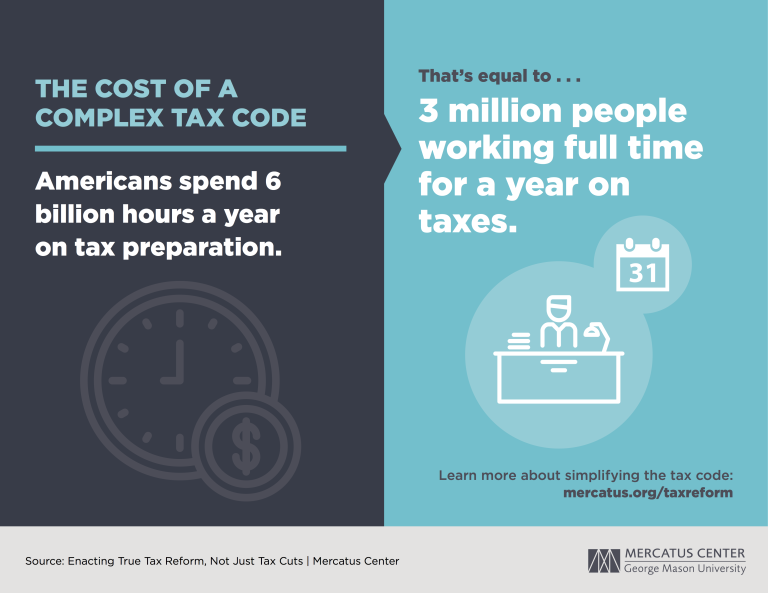

- Simple. A complex tax system makes compliance difficult and costly, as Americans spend an estimated 6 billion hours and up to $378 billion annually on tax preparation. Complexity also encourages tax avoidance. A simpler and more transparent tax code promotes compliance and increased revenues.

- Efficient. The current tax code impedes economic growth by distorting market decisions in areas such as work, saving, investment, and job creation. An efficient tax system could provide sufficient revenue to fund the government’s essential services with minimal distortion of market behavior.

- Equitable. Americans of all income levels believe the tax code is unfair. This perception is largely fueled by the code’s “loopholes”—provisions intended to benefit or penalize select individuals and groups. Tax fairness should reduce or eliminate provisions that favor one group or economic activity over another (such as the marriage tax penalty), especially among equal-income earners.

- Predictable. Short- and long-term tax certainty is necessary for robust economic growth and investment, and it enhances competitiveness.

Past “Reform” and Tax Cuts Were Deeply Flawed

The Tax Reform Act of 1986, the last major US tax reform, was remarkable for its bipartisan support and sweeping reforms. These reforms were undone almost immediately, however, because the legislation failed to address the revenue system’s institutional problems—special preferences such as the investment tax credit and mortgage interest deduction, which were untouched due to popular political support and lobbying by special interest groups.

The 2001 and 2003 Bush tax cuts were also deeply flawed in their design and implementation:

- The tax cuts were undertaken without any effort to reduce unsustainable government spending. In fact, spending exploded in the decade following their implementation. The result was massive, annual deficits.

- The initial slow phase-in and temporary nature of the Bush tax cuts made the policies less predictable and less potent.

- The tax cuts included exemptions, deductions, rebates, and credits with the goal of putting money back in the hands of consumers in hope that they would, in turn, purchase more goods and services. Consumers instead tended to pay off debt rather than spend, in large part because the tax rates were not reduced permanently.

Effective Tax Reform

History has shown that tax reforms seldom last, since special interests have large incentives to lobby Congress for tax breaks. Keeping the tax code as simple and transparent as possible—by taxing a broad base at low rates—will help limit the opportunities and incentives to reverse future tax reforms.

Simply cutting taxes allows policymakers to give voters something they want while appearing to rein in the size of government. This is a temporary illusion unless the tax cuts are combined with necessary reductions in spending—a far more difficult but also more important task.