- | Government Spending Government Spending

- | Data Visualizations Data Visualizations

- |

High Global Corporate Taxes vs. Low Territorial Corporate Taxes

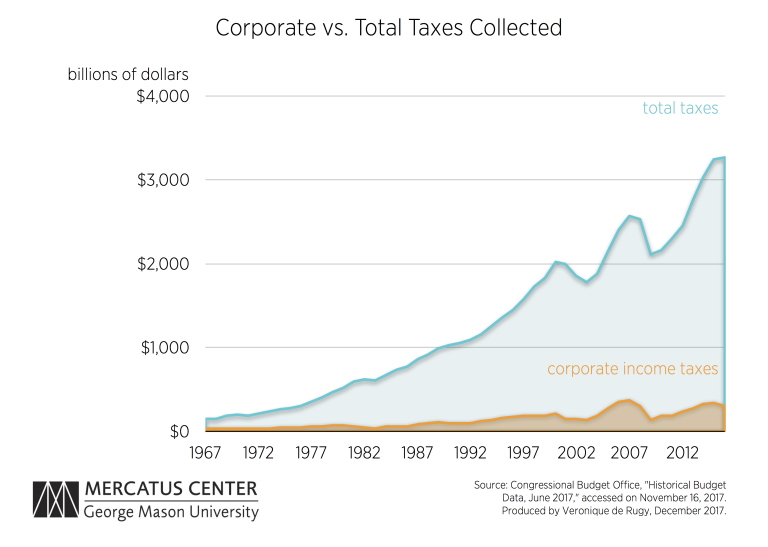

The charts show the growth of total federal tax revenue and corporate tax revenue as well as the proportion of total tax revenue from corporate taxes. Despite growing total revenues, corporate tax rates drive businesses to avoid paying by keeping money overseas.

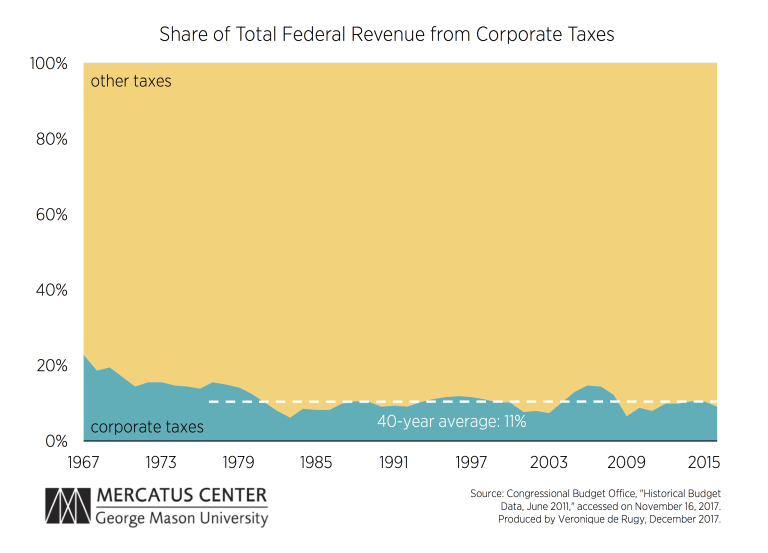

The share that corporate taxes contribute to total federal tax revenues has steadily declined over the past five decades. In 1967, almost one in four dollars of all federal tax revenues (23 percent) was collected through corporate taxes. By 2016, this number had fallen to 9 percent, or less than one in every ten dollars. The historical trend is shown in the figure below.

The worldwide corporate tax system employed by the US taxes corporate income no matter where in the world that income is earned, as opposed to a territorial system in which the government taxes only income earned within its own borders. The United States’ burdensome worldwide system is counterbalanced by a deferral provision that allows corporations to avoid paying taxes on their foreign-earned income as long as they keep that income abroad. Given the opportunity, that’s what companies have done, and as a result, about $2.8 trillion of income earned abroad remains stored outside of the country. That explains why, in spite of a high tax rate, the corporate income tax yields such low returns, as shown in the next figure.

Lowering the corporate tax rate from 35 percent to the 20 percent average for developed countries and switching to a territorial system would give an incentive to companies to bring more of their income to the United States.

Related Content

- | Government Spending Government Spending

- | Data Visualizations Data Visualizations

America's High Corporate Income Tax Rate Harms Global Competitiveness

- | Government Spending Government Spending

- | Policy Briefs Policy Briefs

If Congress Only Does One Thing, It Must Reform the Corporate Income Tax System

- | Government Spending Government Spending

- | Data Visualizations Data Visualizations

Reforming US Corporate Taxes