- | Government Spending Government Spending

- | Policy Briefs Policy Briefs

- |

Reforming Tax Preferences to Pay for Tax Reform

Complying with tax laws shouldn’t be complicated or punishing—paying taxes is punishing enough. But the current process for paying US taxes is anything but simple, and the price tag of that complexity can be enormous. According to a study from the Internal Revenue Service and the Treasury Department, corporations alone spent $104 billion—or 0.64 percent of GDP—complying with the tax code in 2012. That’s a ton of money, especially considering that corporate tax revenues amount to only about $500 billion a year.

The cost to individuals may be even higher. According to a 2013 study by Jason J. Fichtner and Jacob M. Feldman of the Mercatus Center at George Mason University, Americans face upwards of $1 trillion annually in hidden tax-compliance costs. Summarizing the study for U.S. News & World Report, Fichtner and Feldman note that “taxpayers spent more than six billion hours in 2011 complying with the tax code—that’s enough to create an annual workforce of 3.4 million people. If that workforce was a city, it would be the third largest city in the United States. If that workforce was a company, it would employ more individuals than Walmart, IBM, and McDonalds, combined.”

Why does income tax compliance cost so much? The cost is largely due to the fact that Internal Revenue Code, which includes some 80,000 pages of regulations, is riddled with exclusions, exemptions, deductions, preferential rates, and credits.

These tax preferences are used to subsidize a wide range of benefits, such as education, child care, health insurance, and many others. Tax preferences take the form of credits, deductions, special exemptions, and allowances and they usually result in a reduction in the amount of tax an individual or corporation owes. This is why, for the most part, their impact on the budget is measured in terms of revenue not collected. However, this loss in revenue is often perceived as equivalent to spending through the tax code, which is why tax experts refer to tax preferences as “tax expenditures.”

According to the Office of Management and Budget (OMB), in fiscal year (FY) 2018, there will be some 170 tax expenditures and they will add up to more than $1.56 trillion. That’s up from $37 billion in deductions and 50 tax expenditures in 1967. Different administrations define tax expenditures differently, and hence the list printed in the budget varies slightly from year to year and from administration to administration.

The main effect of these tax provisions is to narrow the tax base so there is less income to tax. Because of the significant amount of revenue loss they represent, both political parties regularly target them for elimination—but for different reasons. Democrats are interested in getting rid of handouts to the rich and to corporations, while Republicans see reducing tax expenditures as a potential way to offset the revenue loss from lowering marginal tax rates.

Unfortunately, there are a lot of misconceptions about tax expenditures. Policymakers need to thoroughly understand them in order to make informed decisions about which provisions should go and which ones should be preserved.

Misconceptions about Tax Expenditures

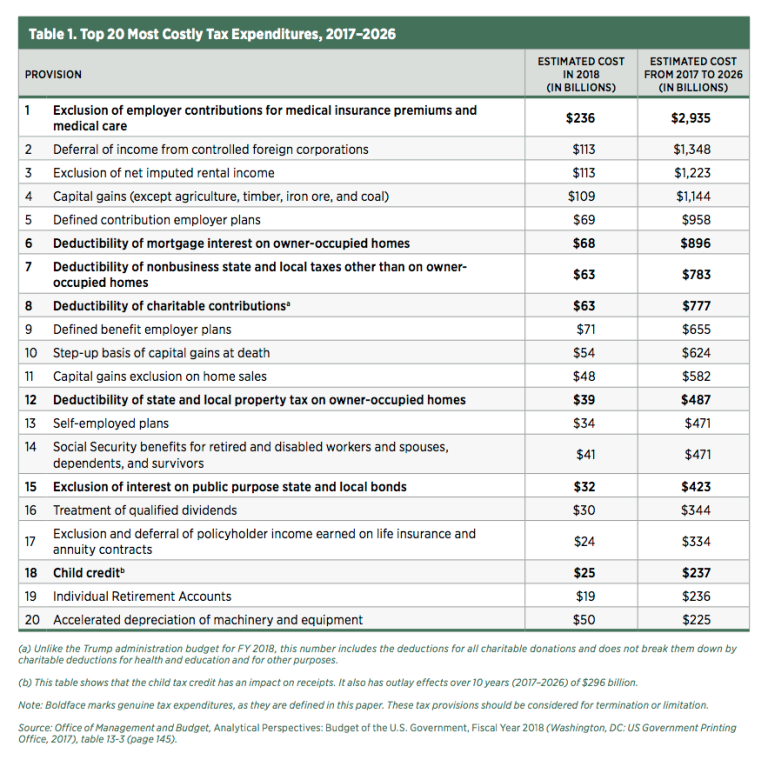

First, policymakers should be aware that a very few tax expenditures are responsible for the bulk of the effect of these provisions on federal revenue. Table 1 lists the top 20 tax expenditures in the FY 2018 budget. They amount to $1.3 trillion and represent 84 percent of the total revenue loss owing to tax expenditures reported by OMB.

Second, contrary to common belief, a vast majority of tax expenditures benefit individuals rather than corporations. Eighty-seven percent of the revenue loss listed in table 1 will benefit individuals. Only two provisions out of these 20 benefit corporations: the deferral of income from controlled foreign corporations (number 2) and the accelerated depreciation of machinery and equipment (number 20).

This means that the revenue and budgetary impacts of repealing all corporate tax preferences will be much smaller than is usually advertised. It also means that if revenue is what lawmakers are after, they will have to focus mostly on tax provisions for individuals.

Third, not all tax expenditures are equal. Income tax reform should lower tax rates, reduce the double taxation of income that is saved and invested, restore horizontal equity (i.e., ensure that taxpayers making the same income pay the same amount of taxes), and broaden the tax base. Many of these goals can be achieved by eliminating tax preferences that tilt the playing field in favor of politically connected interest groups.

For instance, tax provisions that are simply government handouts to well-connected special interests fall into this category, as do those that are meant to achieve social goals like child-rearing, homeownership, healthcare provision, and higher education. Both types of subsidies are distortionary and tilt the playing field in favor of those with political connections. They are tax expenditures in the proper sense of the term.

In addition, they create higher prices for the subsidized goods or services and cause a misallocation of resources as suppliers meet government-induced demand. The benefits from these subsidies also tend to flow disproportionately to higher-income earners, as in the cases of the state and local tax deductions and the mortgage interest deduction. Such provisions also muddy the water for honest public-policy conversations about the size of government. Tax expenditures in this category are set in bold in table 1.

By contrast, some tax provisions are meant to correct the distortions introduced by the double taxation frequently imposed on investment and savings income. This double taxation distorts market decisions and slows economic growth. Tax preferences intended to mitigate double taxation have a legitimate purpose and are not designed to compel behavior or benefit a specific special interest group. They are not tax expenditures, in spite of being labeled as such, and they should be maintained.

On the corporate side, legitimate tax provisions include the deferral of taxes on income earned overseas through foreign subsidiaries and affiliates. Because the United States has a “worldwide” taxation scheme, Americans are required to pay taxes to the US government on foreign-source income even if the income was already taxed in the country where it was earned. Moving to a territorial tax system, in which Americans are only expected to pay taxes to the country in which income is earned, would be ideal. Until that happens, allowing companies to defer the tax burden until the money is repatriated to the United States is better than nothing.

Similar provisions exist for individual income taxes. Most tax economists agree that income should be taxed either before it goes into a savings account or when it comes out, but not both times. Vehicles such as the Roth-style IRA or the traditional 401(k) exist to prevent the government from taxing people’s income twice. The same principle applies to capital gains and dividends, which enjoy a lower rate than other types of income to ease some of the double taxation that takes place because the income was already taxed at the corporate level.

Provisions that allow businesses to deduct their capital expenses or other costs from their taxable income shouldn’t be eliminated either, because these are legitimate business expenses.

Tax Preferences for Individuals That Should Be Repealed or Limited

In the debate over how to fund tax reform, policymakers should target tax expenditures whose elimination would increase revenue or simplify the tax code. But, as I mentioned before, policymakers should be careful not to target provisions like those meant to reduce the double taxation of income.

For instance, equity of corporations subject to the corporate income tax suffers from a double taxation problem when it is redistributed to investors. Corporate earnings are taxed when they are earned. But if these earnings are retained or reinvested, then they increase the value of the company’s stock, and capital gains taxes are collected when that stock is sold—meaning the same earnings have been taxed twice. The same is true of income paid out as dividends. Capital gains and dividends are taxed at a preferential rate in order to mitigate this problem.

The same can’t be said of other tax provisions that are genuine tax expenditures. For instance, the exclusion for employer-provided fringe benefits, such as health insurance, is a prime example of a provision that should be repealed. It is distortionary, unfair, and—most importantly—a major contributing factor to the ever-growing cost of healthcare. Because it promotes overuse of insurance, it also dramatically decreases the amount of healthcare costs paid by consumers themselves as opposed to by a third party. Americans today pay only 12 percent of their healthcare expenses out of pocket, which weakens normal market forces. In addition, as Fichtner and Feldman have noted, it also results in profound horizontal inequity since “there is roughly a 30 percent price difference between employer-provided premiums and individual premiums.”

The federal deduction for state and local taxes is another genuine tax preference ripe for repeal. It obscures the true cost of state and local government policies by allowing taxpayers in high-tax states to deduct the burden of these polices from their federal tax bill. It is unfair to taxpayers in lower-tax states, who do not get to deduct as much from their taxable income as taxpayers in higher-tax states. But it is also unfair to lower-income taxpayers in all states, most of whom do not get to deduct their state and local tax bills since most of them do not itemize deductions. Finally, it makes taxpayers less vigilant about policy changes and the spending behaviors of their lawmakers. For instance, economists recognize that ending this deduction would result in lower state and local taxes and spending.

The child tax credit (CTC) is a perfect example of spending through the tax code that should be repealed. It is a refundable tax credit, meaning that taxpayers below a certain level of income will not just pay lower taxes but will receive money back from the Internal Revenue Service above and beyond any taxes owed. As a result, its overall budgetary impact is much higher than the number listed in in table 1. The revenue loss from the CTC is $237 billion over 10 years, but it will also bring an additional $296 billion in spending.

Tax credits, refundable or not, are mostly designed with social policy priorities in mind. Yet policy goals pertaining to childcare, education, or health are not best achieved through these tax provisions. The provisions have little positive effect on economic growth and are very inequitable, because they benefit only the taxpayers engaging in activities that the government labels as desirable.

The charitable tax deduction should also be repealed. It allows taxpayers to deduct their contributions to tax-qualified organizations up to certain amount. Many analysts see it as the cost of buying or encouraging something that is worthy of government support. Indeed, charitable donations fund civil society, which often offers a more efficient alternative to the government provision of welfare, funding for the arts, emergency relief after natural disasters, and even support for research institutions. However, the data fail to support the idea that the tax provision significantly encourages charitable giving.

These are only a few of the tax expenditures that could be repealed or limited. Table 1 lists an estimated $6.5 trillion (over 10 years) in genuine tax preferences that could be repealed and used to pay for tax reform. Even if the pressure of politics leads to a limitation rather than full repeal of a few of those preferences (the charitable contribution deduction, the mortgage interest deduction, or the exclusion for employer-provided fringe benefits), the reform will still have an effect on revenue that is significant enough to be worth considering.

Corporate Tax Expenditures That Should be Repealed

Many tax expenditures are designed for the sole purpose of subsidizing specific industries and deserve outright elimination. None of these appear in the top 20 list in table 1, but there are many examples in OMB’s corporate tax expenditures table.

For instance, it’s hard to find a more blatant example of a tax expenditure than the special deduction for Blue Cross and Blue Shield. The tax code provides $5.5 billion of special deductions over 10 years for many Blue Cross and Blue Shield companies, while failing to extend those privileges to their competitors. This tax preference should be repealed.

Other tax expenditures may not include the name of a specific company, but they still fall into the category of tax preferences ripe for repeal. The most expensive one is the deduction for US production activities. According to OMB, repealing this deduction would yield $199.7 billion in tax revenues over 10 years. The provision provides a 9 percent deduction for businesses with qualified production activities in the United States. According to the Tax Foundation, “Mathematically, it is equivalent to reducing the corporate income tax rate from 35 percent to 31.85 percent on income from qualified domestic production activities.” However, it is not applied to every industry.

The low-income housing tax credit subsidizes the construction of housing for poor tenants. Getting rid of this tax credit will yield an estimated $90 billion in federal tax revenues over 10 years, according to the OMB. As many scholars have shown, the program suffers many failures, and—contrary to what its name suggests—the subsidy helps developers and financial institutions more than the needy population it is supposed to benefit.

The tax credit for orphan drug research targets the cost of researching certain drugs for which only a small market is initially thought to exist. This privilege redirects resources away from drugs that could benefit a broader range of people. The 10-year estimate of tax revenue from eliminating this tax credit is $53.6 billion.

There are many more provisions that should be repealed, such as the energy production tax credit, the advanced nuclear power production tax credit, and the new markets tax credit. I estimate that eliminating all genuine corporate tax preferences, as opposed to provisions meant to alleviate the double taxation of income or allow the deduction of legitimate business costs, would free around $400 billion in revenue over 10 years.

Conclusion

In the search for more tax revenue to pay for fundamental tax reform, Congress should seek to repeal or limit genuine tax preferences. There are many more of these provisions on the individual side of the code than the corporate side, but reducing the genuine tax preferences in any part of the code would be an improvement. Such reforms could raise a significant amount of revenue to lower corporate and individual tax rates or pay for fundamental tax reform. Also, going forward, Congress should move away from using the tax code to grant privileges to special interests or pursue governing priorities like caring for children and providing healthcare. Both of these uses of the tax code are unfair, create economic distortions, and jeopardize policymakers’ ability to implement fundamental reform and move toward a better tax code.