- | Financial Markets Financial Markets

- | Public Interest Comments Public Interest Comments

- |

Simplifications to the Capital Rule Pursuant to the Economic Growth and Regulatory Paperwork Reduction Act of 1996

Thank you for the chance to comment on the notice of proposed rulemaking regarding the Simplifications to the Capital Rule Pursuant to the Economic Growth and Regulatory Paperwork Reduction Act of 1996. I am an economist at the Mercatus Center, a university-based research center at George Mason University. My comments do not reflect the views of any affected party, but do reflect my general concerns about the regulatory burden and unintended consequences of regulation.

I would like to address questions 14 and 15 posed in the notice of proposed rulemaking. Before that, however, I will discuss the growing regulatory burdens facing banks, and in particular the burdens that come from regulatory capital requirements.

The Growing Complexity of Bank Capital Regulation

Federal Deposit Insurance Corporation (FDIC) Vice Chairman Thomas Hoenig observed in an April 15, 2015 speech that “new risk-based capital rules” and “an ever-expanding Call Report” pose a costly challenge to community banks since many entries in the call report schedules concern activities that have no bearing on community banking. While those same call report schedules may be relevant for activities undertaken by larger banks, they are nonetheless costly to complete for larger banks too.

A relatively new methodology, available through an open-source platform called QuantGov, makes it possible to quantify the growing complexity of regulations by measuring regulatory restrictions, as well as word counts, within the various parts of the US Code of Federal Regulations (CFR). Regulatory restrictions include terms such as shall, must, may not, required, and prohibited.

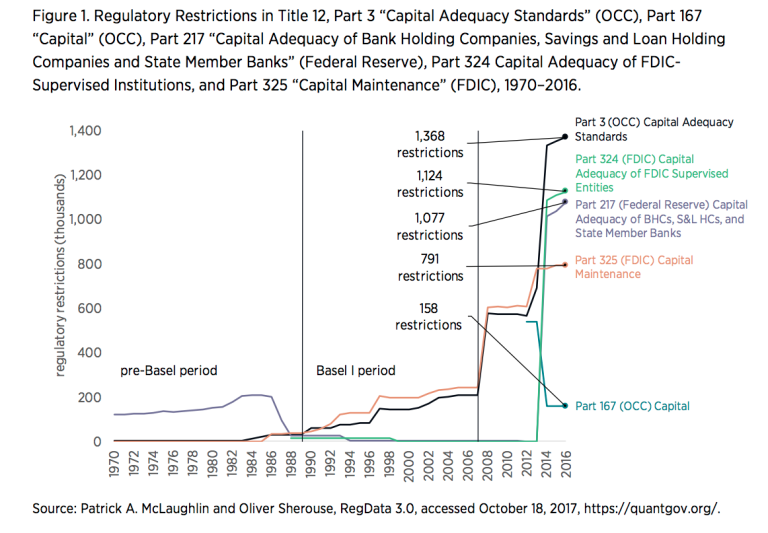

A key factor underlying the “ever-expanding call report” is the growing complexity of bank capital requirements arising from risk-based capital requirements. Figure 1 shows the number of regulatory restrictions in the three parts of the CFR affected by this notice of proposed rulemaking, namely Part 3 (for the Office of the Comptroller of the Currency [OCC]), Part 217 (for the Federal Reserve), and Part 324 (for the FDIC), all of which concern bank capital. The figure also depicts the number of regulatory restrictions for two other parts of the CFR that relate to bank capital—Part 167 (for the OCC) and Part 325 (for the FDIC). The legend displays the series titles sorted from the largest to the smallest number of restrictions in 2016.

The figure shows the increase associated with the implementation of Basel I capital adequacy standards and especially postcrisis reforms, including the implementation of the Basel III capital adequacy standards. By 2016, there were 1,368 restrictions in Part 3, 1,124 restrictions in Part 324, and 1,077 restrictions in part 217; Part 167 contained 158 restrictions while Part 325 had 791 restrictions.

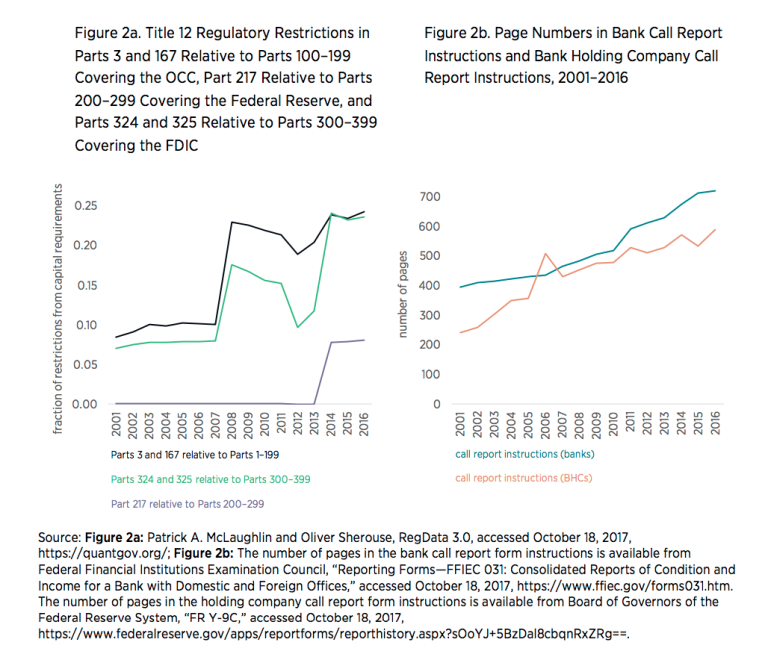

The volume of regulatory restrictions that concern bank capital for the OCC, the FDIC, and the Federal Reserve has also increased relative to the total number of regulatory restrictions for each agency, and the rise is also reflected in the “ever-expanding” call report. To show this, Figure 2a plots (1) the fraction of regulatory restrictions embedded in Title 12 Parts 3 and 167 relative to all OCC-related regulatory restrictions in parts 100–199, (2) the fraction of regulatory restrictions embedded in Title 12 Part 217 relative to all Federal Reserve–related regulatory restrictions in parts 200–299, and (3) the fraction of regulatory restrictions embedded in Title 12 parts 324 and 325 relative to all FDIC-related regulatory restrictions in parts 300–399. Figure 2b plots page numbers in bank call report instructions and page numbers in bank holding company (BHC) call report instructions.

Figure 2a shows that in 2001, the fraction of regulatory restrictions—measured by agency—devoted to capital requirements was about 8 percent for the OCC, 7 percent for the FDIC, and 0 percent for the Federal Reserve. By 2016, that fraction was about 24 percent for the OCC and FDIC and about 8 percent for the Federal Reserve. Meanwhile, Figure 2b shows that between 2001 and 2016 the number of pages in the instructions to fill out the bank call reports has grown by about 82 percent to 718 pages, while the number of pages in the instructions to fill out bank holding company call reports have grown by about 146 percent to 587 pages. Although a measure of compliance costs is not readily available from call report data, as the volume of regulatory restrictions increases, so does the complexity, and the costs associated with compliance likely rise as well.

These graphs suggest that bank capital regulation has become increasingly complex. Moreover, the argument that risk weighting of assets leads to better bank risk management is inconsistent with the empirical evidence that risk weighting could well have had unintended consequences that contributed to the 2007–2009 financial crisis.

Unintended Consequences of the More Complex Bank Capital Regulation

One justification for using risk weights is that it adjusts bank capital for the riskiness of a bank’s underlying asset holdings. However, the standardized approach to risk weighting typically involves assigning predetermined risk weights to assets that may not reflect the true risks of the bank’s assets. Meanwhile, an often-repeated claim holds that the leverage ratio contributes to bank risk taking, yet the same might be said about risk weights leading up to the most recent crisis.

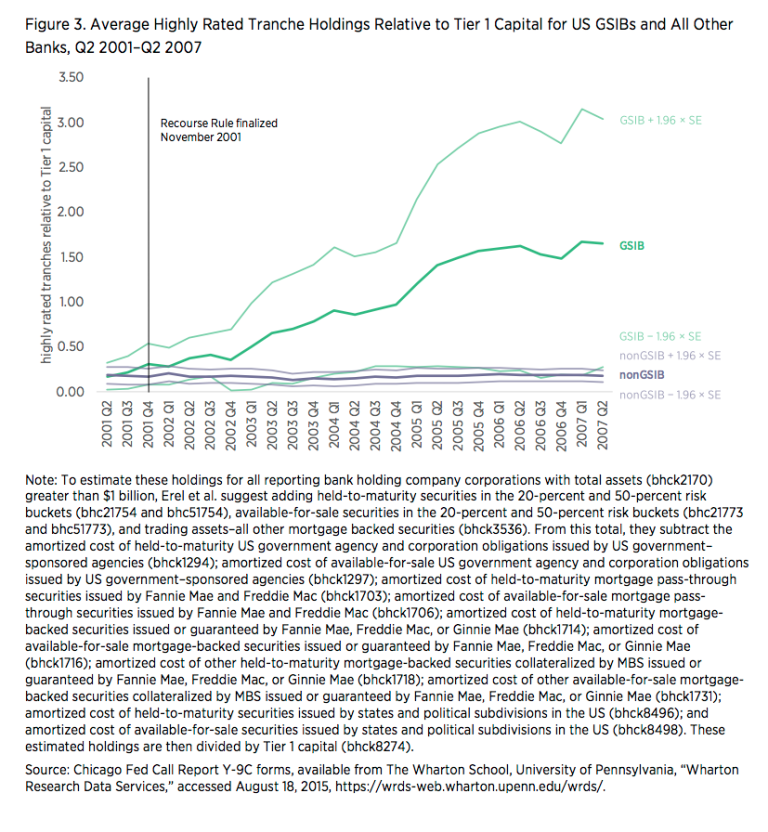

The Recourse Rule, finalized on November 29, 2001 by the Federal Reserve, FDIC, and OCC, altered capital requirements for bank holdings of highly rated, private label asset-backed and mortgage-backed security tranches and collateralized debt obligation tranches. The rule changed capital requirements for tranches with AAA or AA ratings by lowering their risk weights from 1 or 0.5 to 0.2, which meant that capital requirements for these assets fell from 8 or 4 percent to 1.6 percent. For A-rated tranches the risk weights were set at 0.5, which meant that the capital requirement equaled 4 percent.

In a recent working paper, I construct a measure of holdings of highly rated, private label securitization tranches by BHC—as suggested by Erel, Nadauld, and Stulz—from Q2 2001 to Q1 2009. I find that on average the largest BHCs that securitized assets held the most highly rated securitization tranches, whether measured relative to total assets or to Tier 1 capital, and their holdings rose after the Recourse Rule was finalized and until the crisis began to unfold. BHCs were not required to report such holdings before the Recourse Rule, so you might expect that reported holdings would rise after the rule was finalized. Still, given the similarity of reported holdings for both types of BHCs prior to the Recourse Rule being finalized and the flat pattern of holdings for other BHCs before and after the rule was finalized, the rising average holding for the largest securitizing BHCs after the rule was finalized would be consistent with the rule change spurring their holdings of highly rated tranches. Figure 3 depicts the average holdings of highly rated tranches relative to Tier 1 capital for US global systemically important banks (GSIBs) listed in FDIC’s Global Capital Index and Wachovia from Q1 2001 to Q2 2007, as well as for all other BHCs with at least $1 billion in total assets.

I also find that banks with greater holdings of highly rated tranches on average experienced large quarterly declines in distance-to-default—a measure of default risk—from Q1 2008 through the end of the sample, but not before that. Taken together, these findings imply that while more complex, risk-based capital rules were supposed to make banking organizations more resilient to financial distress, the risk-based rules could well have encouraged banks to hold the very sort of assets that featured prominently during the last financial crisis. With this background in mind, I will now address questions 14 and 15 from the notice of proposed rulemaking.

Response to Question 14 and Question 15: Why the Leverage Ratio Works

Question 14 asks whether an alternative to risk-based capital, such as the US GAAP leverage ratio, would be effective, while Question 15 asks whether there should be a reduction in the number of capital ratios. Based on findings in a forthcoming update of a coauthored working paper, I believe that strict reliance on the leverage ratio would be more effective than having multiple capital ratios, with many being defined relative to risk-weighted assets, which addresses question 14. Relying on the leverage ratio can serve to eliminate the need for other measures, which addresses question 15.

To see why my coauthor and I ask in a recent paper whether the benefits of raising the book equity-to-book asset leverage ratio from the 2014 minimum value of 4 percent to 15 percent would have benefits that outweigh the costs. Nearly 95 percent of the BHCs in our sample operate with more than twice the 2014 minimum amount of 4 percent. We use 15 percent because several recent studies have found that a rate roughly equal to 15 percent would be optimal. We find that in most cases, the marginal benefits exceed the marginal costs.

Drawing from a study of large UK banks by Miles, Yang, and Marcheggiano, we measure benefits in terms of a reduction in expected real GDP losses arising from a financial crisis, and the costs in terms of forgone lending arising from the higher interest rates that might arise if banks are compelled to fund with more equity. In our benchmark case, we make relatively weak benefit assumptions in that we assume the expected benefit of a higher leverage ratio per percentage point reduction in the probability of a crisis equals only 7.7 percent of one year’s GDP. Our benchmark also assumes the highest cost scenario from Baker and Wurgler in that an 11-percentage-point rise in the leverage ratio would result in lending rates rising by 99 basis points.

Moreover, the baseline estimates we adopt from Baker and Wurgler’s study come from a sample of nearly 4,000 banks, whereas other studies typically only include the largest holding companies. Also, since smaller banks tend to be more highly capitalized, our findings suggest smaller banks could comply with this regulation, which would have the benefit of greatly lowering their regulatory burden and the associated compliance costs.

Consider Instead a Market Equity-to-Book Short-Term Liability Ratio

While our study does not examine the possibility, since any solvent bank has assets greater than total liabilities, as well as short-term liabilities, an alternative might be to define the leverage ratio as an entity’s equity capital (and perhaps even long-term debt), measured at market value, relative to its short-term liabilities; for those that have no traded shares, market values could be estimated. Defining capital ratios in terms of liabilities would not be without historical precedent. Following the FDIC’s establishment in 1934, its staff determined that minimum capital ratios should equal at least 10 percent of deposits. Defining the capital ratio relative to (short-term) liabilities rather than assets obviates the need to discuss whether or not capital ratios should be risk-weighted, and how to weight the various asset classes. Also, relying on the market value, rather than the book value, of equity capital would more closely connect the proposed leverage ratio to market discipline.

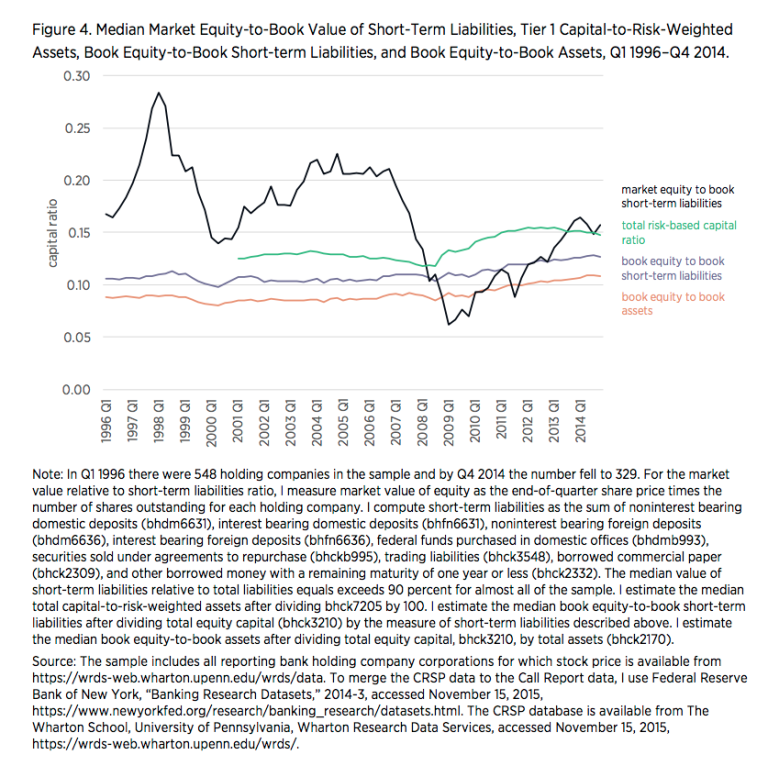

To see how different leverage ratios have performed over time, figure 4 depicts (1) the median ratio of total risk-based capital, about two-thirds of which is Tier 1 capital, relative to risk-weighted assets, (2) the median ratio of book equity to book assets, which is frequently discussed as an alternative to risk-based capital measures of capital adequacy, (3) the median market equity-to-book short-term liabilities ratio, and (4) the median book equity-to-book short-term liabilities ratio. The figure shows that at the median the market equity-to-book short-term liabilities has been the highest throughout the sample, except during the crisis period, often exceeding 15 percent. The drop during the crisis reveals the potential for market discipline, since you would expect stock prices for poorly performing BHCs to drop.

These findings highlight key problems with using accounting measures of capital, including Basel-type measures. For instance, book values may not serve as the most effective measures of a bank’s net worth, since they are reported with delay and can be revised. Although noisy, market values would reflect market perceptions concerning a bank’s performance in real time. Measuring market equity relative to short-term liabilities rather than assets also addresses the challenge of marking assets to market, which arises because many bank assets trade infrequently. Tracking the face value of short-term liabilities could simplify the process too.

To implement a market equity-to-book short-term liabilities capital requirement, one method would be to draw from the US model for calculating required reserves for banks. For the purpose of satisfying reserve requirements, banks currently have to measure reserves relative to the average amount of net transaction accounts. Reserve managers first determine required reserves during the reserve computation period, and subsequently must at least cover those required reserves during the reserve maintenance period.

During the reserve computation period, which under current regulations begins on Thursdays and ends two Wednesdays later, the reserve managers must calculate the daily average during the previous 14 days of net transaction accounts. Net transaction accounts equal total transaction accounts, which include those for which account holders can make withdrawals (e.g., demand deposits and negotiable orders of withdrawal) minus demand balances due from other banks and items in process of collection.

Once reserve managers determine the target amount they must maintain during the reserve computation period, they must then at least cover that target during the reserve maintenance period. The reserve maintenance period begins 17 days after the reserve computation period ends.

Drawing from this model of reserves management, a bank’s treasury staff might ensure that the market value of the bank’s equity, equal to the market price of shares multiplied by the total number of shares of common stock outstanding, might equal a fixed fraction of current short-term liabilities during some short-term period (e.g., a week, month, or quarter). For instance, if a bank on average or at the median has $100 billion in various forms of short-term debt during a particular period, and the capital requirement is 15 percent, then staff must ensure that the average or median market value of the bank’s shares equals $15 billion.

One objection to such a proposal would be that stock prices can move by large amounts. In our benefit-cost analysis of a higher leverage ratio, my coauthor and I show that returns on BHC shares on average between 1996 and 2014 varied about by about 90 percent as much as the market as a whole, such that for every percentage change in market returns, the value of BHC equity changes by about 90 percent of that change, meaning they tend to be less volatile than the market as a whole.

However, the risk of large declines in the share price, which could reflect the manifestation of poor bank investment decisions, would mean that using a market-valued measure of capital could foster market discipline. A larger equity capital buffer would also mean that the bank would have less incentive to take on risk. Banks that have their market value of equity relative to liabilities drop below the minimum would be at higher risk of default, which could trigger change through bank shareholder activism.

A recent study by Raluca Roman suggests that shareholder activism is common for banks, and that shareholder activism creates gains for shareholders in terms of a higher market value without affecting the bank’s operating returns, though it may increase bank risk in normal times. These findings apply mainly to smaller banks, as larger banks targeted by activists only experience higher market value. The study also shows, however, that shareholder activism did not contribute to the recent crisis, since market values were higher without any increases in risk-taking during crises. Overall, the findings suggest shareholder activism could serve to preserve firm value.

Consider Instead a Market Equity-to-Book Short-Term Liability Ratio

Overall, serious concerns about Basel-style capital requirements exist. Their complexity has a bearing on the regulatory burden that banks face. Criticisms that the leverage ratio contributes to risk taking may apply equally to risk-weighted measures of capital, as we saw for some GSIBs during the crisis. While there is evidence that increasing the equity-to-asset leverage ratio from 4 to 15 percent has benefits that outweigh the costs, there may still be concerns about whether book measures of equity capital foster market discipline. An alternative may be to establish a market equity-to-book short-term liability ratio, drawing from the required reserves model currently in place. This approach has the advantage of fostering market discipline through the use of market-based measures of capital while avoiding the debate over how to measure assets.

Rules details

Agency: Department of the Treasury, Office of the Comptroller of the Currency

Proposed: October 27, 2017

Comment Period Closes: December 26, 2017

Submitted: December 11, 2017

Docket ID: OCC-2017-0018

RIN: 1557-AE10

Agency: Federal Reserve System

Proposed: October 27, 2017

Comment Period Closes: December 26, 2017

Submitted: December 11, 2017

Docket Number: R-1576

RIN: 7100-AE37

Agency: Federal Deposit Insurance Corporation

Proposed: October 27, 2017

Comment Period Closes: December 26, 2017

Submitted: December 11, 2017

RIN: 3064-AE59