- | Housing Housing

- | Policy Briefs Policy Briefs

- |

Can a Federal Public Infrastructure Bank Improve Highway Funding?

Most road quality issues are at the local level, which is a municipal government responsibility. A national infrastructure bank would focus on building new infrastructure capacity rather than maintaining existing roads. It would not accelerate the filling of potholes on local streets.

Many politicians have expressed concern over the condition of US highways. They contend that a significant increase in federal highway spending is needed to improve highway performance. One suggestion is to create a national infrastructure bank that could direct additional resources toward highway construction. President Obama proposed establishing just such an institution, and President Trump’s nominee for Treasury secretary, Steven Mnuchin, has also suggested establishing an infrastructure bank as a way to fund additional highway and bridge construction.

Establishing a national infrastructure bank would expand the role the federal government plays in highway construction. While the federal government does have a role to play in the national transportation system, it would be a mistake to expand that role. It’s not simply a matter of building more roads to have an effective transportation system. Dollars must be channeled toward projects that have a high return. These decisions are better made at the state and local level. Establishing a national infrastructure bank would further concentrate transportation infrastructure decision-making in Washington and would do little to improve how policymakers use transportation dollars.

Public infrastructure banks are government institutions designed to lend funds to municipalities and private firms to finance the construction of highways and other infrastructure projects. As loans are repaid, the recycled funds are used to finance additional lending. The goal is to provide a sustainable source of funds for infrastructure investment, reducing the reliance on general funds.

This paper explains how infrastructure banks operate and points out their limitations. In order to make the idea of an infrastructure bank more concrete, the paper reviews some issues surrounding state infrastructure banks already in operation. The paper concludes with some suggestions about how the United States could improve highway funding and performance.

A National Infrastructure Bank

A national infrastructure bank is intended to expand funding and provide a more sustainable source of funds for infrastructure investment. It would also expand Washington’s role in project selection. Under President Obama’s proposal, the federal government would provide $10 billion to capitalize a national infrastructure bank. The bank would make loans at Treasury bond interest rates on projects costing at least $100 million ($25 million for rural projects). The bank would finance up to 50 percent of a project. The remaining sources of funding would come from city and state governments or the private sector. Loan repayments would serve as a source of funds to finance future infrastructure projects.

There are a number of issues associated with establishing a national infrastructure bank. The federal government already has several lending programs that serve the same purpose, which may make an infrastructure bank redundant. The Transportation Infrastructure Finance and Innovation Act authorizes the Department of Transportation to provide loans, loan guarantees, and standby lines of credit that can be used to finance highway and mass transit infrastructure projects. To date, the program has provided $23 billion in credit assistance for 61 major projects in 20 states. The Fixing America’s Surface Transportation Act approved December 4, 2015, provides the program with $1.435 billion of funds over the next five years. In addition, the Railroad Rehabilitation and Improvement Financing program provides similar credit facilities to railroads. Infrastructure bank proposals so far have failed to provide a justification for adding an additional agency given the existence of these federal lending programs.

Politically appointed infrastructure bank managers are likely to pressure staff to bias project evaluations toward projects with large political payoffs, such as projects in states with close elections. Studies have found a significant political bias problem for discretionary job training funds and the state spending pattern in the American Recovery and Reinvestment Act of 2009. An additional complication is that benefit-cost analysis of large infrastructure projects of the type a national infrastructure bank would finance is notoriously misleading, suggesting that even if politics are removed from the final selection decision, political forces will bias the analysis fed into the choice process.

Forecasting a proposed project’s construction cost and usage is difficult. On average, if analysts are objective in their estimates, we would expect forecast errors to be unbiased with unpredictable errors. Researchers Bent Flyvbjerg, Nils Bruzelius, and Werner Rothengarter examine estimates of large infrastructure project costs and benefits across an international sample of projects. They find systematic underestimation of costs and overestimation of benefits. Flyvbjerg and his coauthors conclude that political pressure on analysts results in a systematic bias to paint a rosy picture of costs and benefits. Another example of this kind of behavior can be seen in the optimistic economic forecasts produced by the White House Office of Management and Budget. In contrast, forecasts made by the Congressional Budget Office have been closer to private-sector projections. In other words, the errors are likely deliberate and result from pressure to achieve political goals.

Infrastructure investments impose costs on and provide benefits to the community in which they are located. So, by their very nature, infrastructure investment decisions are highly political and supported by local unions and construction companies. Politicians love to be at ribbon-cutting ceremonies. Because of this, there is pressure to overstate the net benefits of a project. Unlike private lenders who seek the highest risk-adjusted return on projects they fund, public decision makers in government or at a government infrastructure bank are likely to be influenced by politics as much as by hard economic facts. There is no reason to conclude that a national infrastructure bank would allocate funds to higher-return projects.

Using federal funds to subsidize what is mostly a state or local function, as would be the case with a federal infrastructure bank, distorts decision-making. The federal contribution encourages states and municipalities to take on infrastructure projects that could not stand on their own. The California bullet train is an example. Because the local community does not pay the full cost of a project, noneconomic projects—where total costs exceed total benefits—are often built. Although politics cannot be eliminated from the project-selection process, the primary way to reduce its role is to shift funding responsibility back to state and local governments, where the relationship between funding and beneficiaries is closer. Many infrastructure projects would not be built if the community had to pay the full cost, which means that the projects actually selected would provide higher returns.

Another drawback is that a national infrastructure bank would continue the focus on building new projects rather than maintaining existing highways and roads. Maintenance has a bigger impact on the economy than new highway construction, providing a higher rate of return. Furthermore, the rate of return on new construction has been declining and is generally less than the rate of return on private investment. Unfortunately, infrastructure banks direct funds to new construction.

Creating a national infrastructure bank would expand the transportation bureaucracy in Washington, encourage the construction of projects that don’t pass benefit-cost analysis, and increase project selection power in Washington. While there are infrastructure investments that have a multijurisdictional impact, such as seaports, Washington already has more than enough power and funds to handle these projects. A national infrastructure bank is the wrong kind of policy reform because it will make it more difficult to shift highway funding responsibilities back to the state and local level, where it is possible to select higher-return projects.

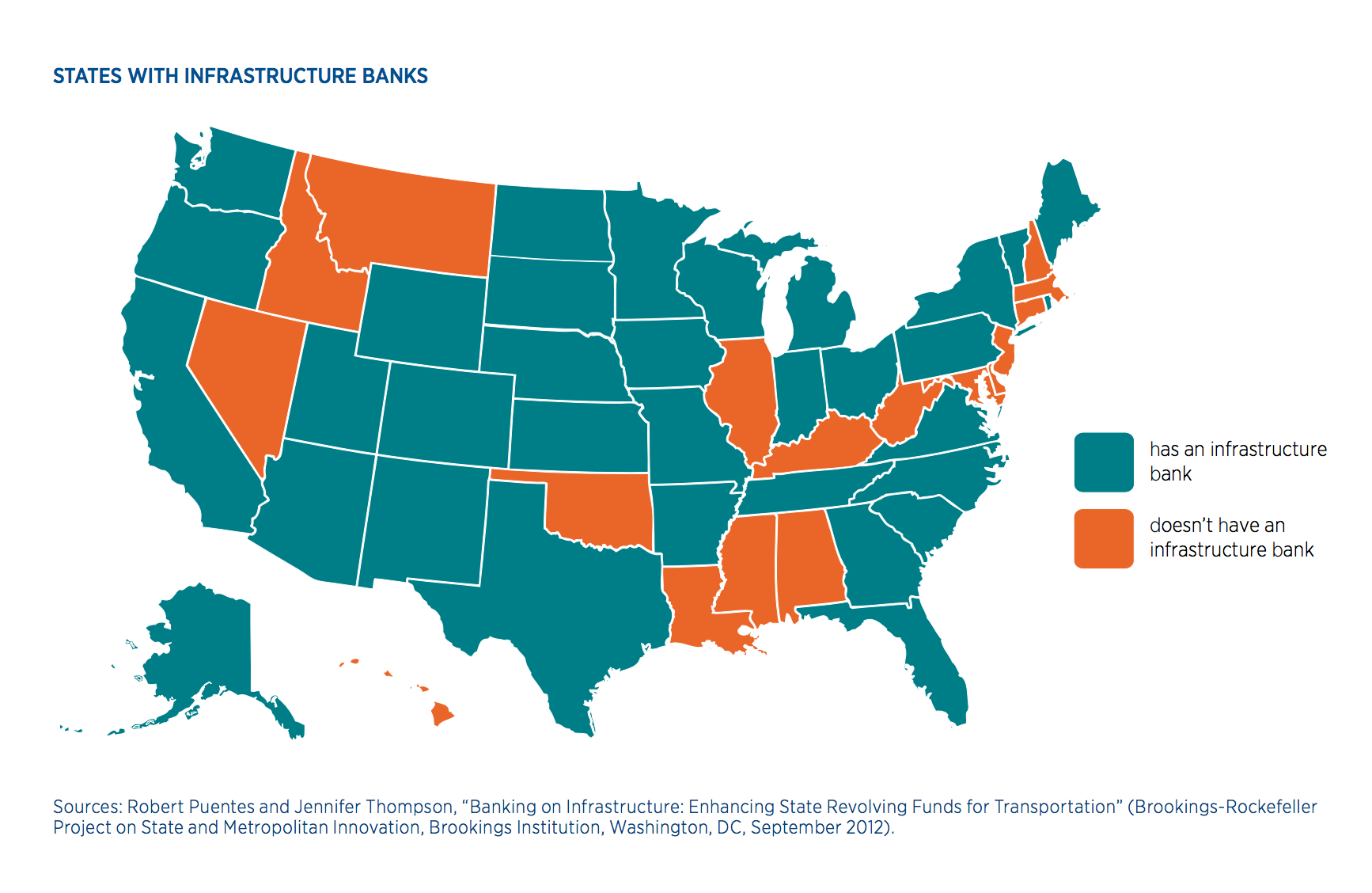

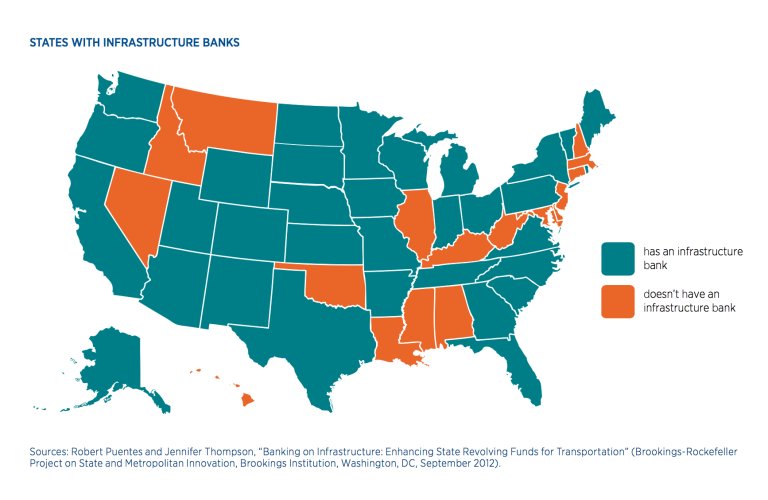

State Infrastructure Bank Experience

{kind=link}

Robert Puentes and Jennifer Thompson estimate that state infrastructure banks made 1,134 agreements worth about $7.4 billion with municipal governments between 1995 and 2012. States spent approximately $1.4 trillion on infrastructure over the 1996–2010 period, so SIB lending remains relatively small, about 0.5 percent of the total infrastructure spending. Per capita lending is less than $100 for all SIBs except Wyoming and South Carolina, at $329 and $601, respectively. Seventy percent of the agreements supported road construction. Other major areas financed included aviation (6.5 percent), water (4.4 percent), and transit (4.1 percent). Some agreements supported social and redevelopment projects.

Three-quarters of the SIB agreements are in eight states, suggesting many banks are not very active. One troubling fact is that 28 percent of the loans were interest free, which limits the sustainability of the bank.

SIBs have the option to leverage the initial public capital by borrowing at market interest rates. This enables SIBs to fund more projects. However, it can create long-term financial viability problems. For SIB loans to be attractive to municipalities, the interest rate must be below the municipal bond rate—the rate at which municipalities can borrow on their own. If SIBs borrow at market interest rates and lend at below-market rates, the capital of the SIBs will erode over time. In addition, to further protect bank capital, the SIB loan rates should be greater than the inflation rate. SIB lending has also been used to avoid state borrowing limits without seeking approval from voters.

Conclusions

Politicians have been toying with the idea of a national infrastructure bank since the 1990s. The principal goal of the institution would be to expand infrastructure spending. The establishment of such a bank would be a mistake. It would further centralize transportation decision-making in Washington, resulting in a less-efficient use of limited tax revenues.

Instead, greater funding responsibility and decision-making powers belong with state and local governments, since the management of highways, roads, and urban transit is primarily a state and local responsibility. To achieve such a shift, the federal gasoline tax could be replaced by higher state-determined gasoline taxes. Each state could then decide on the appropriate level of funding based upon its transportation needs. Local decision-making will improve the project-selection process. Communities that benefit from a project most should pay the full cost (or most of the cost). The federal government would still play a role in multijurisdictional projects, such as seaports.

It is important to place most funding responsibilities on state and local governments in order to provide incentives to fund projects with high net benefits. The attraction of an SIB is the ability to finance additional infrastructure as loans are repaid. However, taxpayers should be aware that it is tempting for SIBs to borrow in financial markets to expand lending. If the SIB loan rate is below the market interest rate or less than the inflation rate, the bank’s capital will contract. Rather than being self-financing, the SIB would require continued state funding.

The most recent data suggest that the quality of bridges in the United States has improved. This does not mean there are no projects worth undertaking, only that government officials need to be selective in projects they fund. It would make sense to focus on maintenance and to build new capacity in areas where population and economic activity has expanded. Most road quality issues are at the local level, which is a municipal government responsibility. A national infrastructure bank would focus on building new infrastructure capacity rather than maintaining existing roads. It would not accelerate the filling of potholes on local streets.