- | Housing Housing

- | Expert Commentary Expert Commentary

- |

Low Property Taxes and Obstructed Housing Supply Are a Bad Mix

Part Eleven of Kevin Erdmann's Housing Affordability Series

In parts nine and ten of this essay series, I used this basic accounting identity to think about property taxes as a way for the state to be a sort of silent partner in the ownership of residential property and to claim monopoly profits as taxes:

Net rental value after maintenance and expenses = Rate of return on investment × Price

Where housing is politically constrained so that property values are inflated, property taxes can be a relatively pure claim of monopoly profits. So, one could argue that a beneficial policy goal may be to raise property taxes in cities where property values are high.

Since property taxes tend to be associated with local jurisdictions, there is a great deal of variation across the country, and even across cities. As a portion of home values, average property taxes range from 0.3 percent in Hawaii to 2.1 percent in New Jersey. Within the New York City metropolitan area, there is just as much variation, with average property taxes ranging from 0.5 percent in Manhattan to more than 2 percent in several New Jersey counties.

Using this simple equation, price can be expressed as a function of rental value and rate of return. Further, rate of return can be broken out into several components: the market rate of return required for assets with similar risks, the expected future growth rate of rent on a unit, and the rate of property tax.

Market Rate of Return – Expected Growth in Rent + Property Tax = ( Net Rental Value / Price )

(Expected rent growth is subtracted from the rate of return because the cash return an investor requires is lower if the investment value is expected to grow. In other words, an investment with a face value of $1 and a dividend of 5 percent that is reinvested is the same as an investment with a starting face value of $1 that increases in value by 5 percent per year with no dividend.)

There are some cities where prices have become exceedingly high. Before the crisis, this was widely blamed on speculative, unsustainable markets. In my book Shut Out, I noted that, to the contrary, high home prices have been highly correlated with high rents. Prices hadn’t become unmoored from rents. They were high because of high rents.

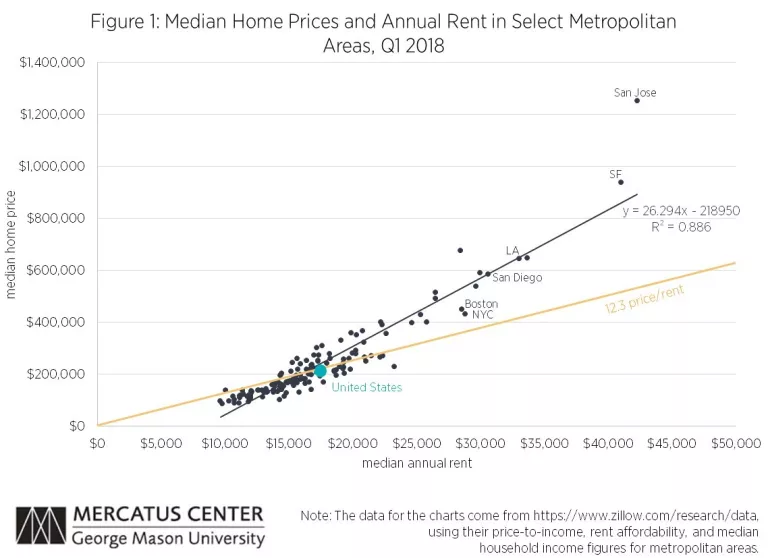

Confusion on this matter comes from the fact that when rents rise in a city, prices tend to rise even more. Figure 1 compares rents and prices among the largest metropolitan areas. The relationship between rent and price is extremely strong.

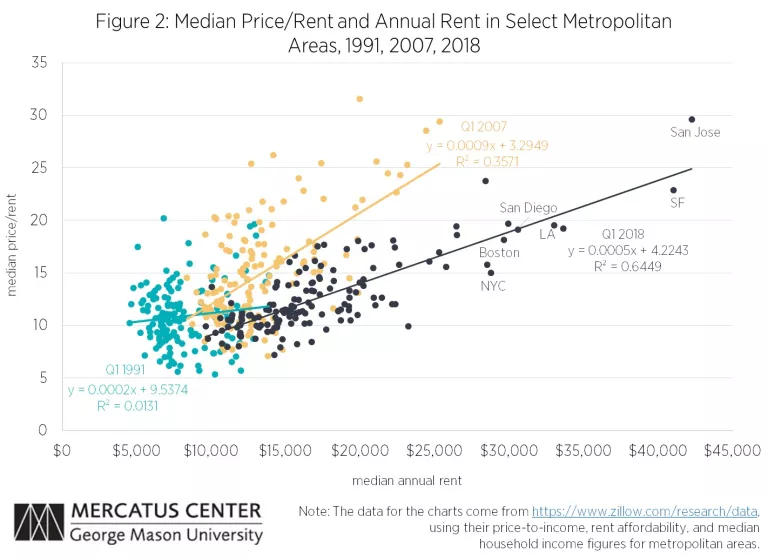

Figure 2 shows how, over the last twenty years, higher rents have become increasingly associated with higher price/rent ratios. This is because the shortage of urban housing has created localized rent inflation that is expected to continue into the future.

As shown in Figure 2, this wasn’t the case before the turn of the century. Before urban housing became so difficult to build, rents didn’t just keep rising in economically successful cities. Rents remained moderate as people moved to successful places and homes were built for them. Prices didn’t rise in expectation of future rising rents. The pattern of cities with persistently rising rents and prices that reflect future high rents has only developed recently.

For cities like San Francisco and Los Angeles, high rents that are expected to continue to rise are an important factor in home prices. The extreme volatility in prices common this century is a product of the combination of high rents, low rates of return on fixed income securities, and low property tax rates. The simple equation above can help to estimate the factors that cause local home prices to rise.

Let’s compare Dallas, Atlanta, and Los Angeles. We can estimate price, rent, and the rate of return on fixed income securities from market prices. Property tax rate estimates are also available. This leaves expected growth in rent as an unknown, which can be inferred from the other measures using the equation above. Estimates for each location are shown in Table 1.

(Data note: The data for median monthly rent and median home price are from https://www.zillow.com/research/data. To estimate net rent/price, annual maintenance and upkeep expense was estimated to be 35 percent of gross rent. Market return is estimated to be equal to the fixed 30-year mortgage rate.)

Fulton County, Georgia (Atlanta) has somewhat lower property taxes than Dallas, which probably accounts for much of the difference in home prices. In Atlanta, a new leveraged home buyer has similar total monthly costs as a home buyer in Dallas, but in Dallas, more of those costs flow to the local government instead of to the mortgage lender. Since the property tax can be described as a sort of silent ownership by the government instead by the homeowner, the value of those tax payments to the government is not part of the market value of the home. If we added the value the home has for both the owner and the government, homes in Atlanta and Dallas would have a similar total value.

Los Angeles has even lower effective property tax rates than Atlanta. But Los Angeles also has a constrained housing market where rents are expected to continue to rise. As the net effect of low market rates of return, high expected rent inflation, and low property taxes pushes toward zero, price (being in the denominator of our equation) pushes toward infinity. That is why the combination of factors is so destabilizing. That is why the median rent in Los Angeles is 76 percent higher than in Dallas, but the median price is 188 percent higher.

Yet while the first order effect of these factors is only on price, rents are pushed higher by local obstructions to supply. In an economy with low market rates on safe assets, localities with low property taxes will be especially vulnerable to political control.

It is more lucrative to work together to politically obstruct new supply and push future rents higher in Los Angeles than it is in Dallas. That is mostly due to factors under the control of Los Angeles voters: the local rate of property taxation and the rate of new building that can lower future rents. Quantitatively, if local political obstruction to new homes creates even a small shift in the expected growth of rents, it can greatly increase the market value of local properties.

It would seem that raising property taxes would make housing more expensive. They are, effectively, a tax on materials to build homes. But the binding constraint to affordable and reasonable housing in twenty-first century America isn’t material. It isn’t a lack of affordable physical space. It is the political obstruction to placing those materials in dense urban centers.

As Byron Lutz, whose work I referenced in my last essay, found, lower property taxes did increase the quantity of shelter consumed in places where housing supply is not obstructed. The corollary to that, that higher taxes would lower the consumption of shelter in those places, is true.

But there is little difference in the quality of life between an economy where the average household occupies 2,400 square feet versus one where the average household lives in 1,800 square feet. American households across the geographic landscape make significant tradeoffs with things like floor space in order to capture other amenities and values.

However, Lutz did find that “communities which experience a decrease in property tax burdens, and witness a surge in building activity as a result, increase the stringency of their land use regulation - a response likely to slow the growth in housing supply.”

We may have reached a point in our economic development as a nation where the negative second order effects of political obstruction to new supply are more important than the first order effects of the after-tax cost of a board foot of lumber. That is undoubtedly the case in the localities where affordability is the largest problem.

If that is the case, we may find ourselves with two ironic factors in housing affordability:

- Rising rents cause price/rent ratios to rise.

- Lowering taxes on homes can decrease their long-run supply and cause rising rents.

Photo credit: JOSH EDELSON/AFP/Getty Images.