Fall is arriving with two consecutive quarterly readings of negative real GDP growth: the −1.6 percent final estimate for Q1 2022 and −0.9 percent first estimate for Q2 2022. I note that gross output, which consists of activity across the economy’s full supply chain, rose 2.0 percent in the first quarter, the latest reading available and the weakest growth since Q2 2020. As with GDP, most of the output gain came from the services sector. The shrinking GDP has been accompanied by raging inflation and tight labor markets, not to mention continuing energy uncertainties stemming from the Russo-Ukrainian War as well as the lingering effects of the COVID-19 pandemic.

Federal Reserve (Fed) Chair Jerome Powell and the Federal Open Market Committee (FOMC) are once again center stage as the world waits to see what the next interest rate increase will bring and whether the US economy will be declared to be in a recession. The FOMC’s increase of its benchmark interest rate by 150 basis points since June and the promise of more increases seem to be effective, as preliminary readings indicate the economy is slowing. This is particularly visible in housing markets and construction activity, two interest-rate sensitive economic sectors. Just how much slowdown America will see is the larger question.

Is America in a recession—now referred to as the “r-word”—or should that concept even be applied to times as strange as these? Americans are still affected by a pandemic and major stimulus actions designed to offset the pandemic’s harm, and global energy supply uncertainties are disturbing energy markets. These circumstances all now form elements of a debate about the health of the US economy. The designation of US recessions is performed by the National Bureau of Economic Research (NBER), a private research center widely recognized as the country’s recession scorekeeper, not by government economists. The task has always been and must always be performed after the data are in hand for the period in question. Put another way, it will be months before anyone knows if Americans are currently living in a recession economy. Recessions are not declared on the run but after the fact.

The Inflation Hobgoblin That Will Not Go Away

Inflation is the hobgoblin that does not want to go away. June’s year-over-year Consumer Price Index (CPI) growth came in at 9.3 percent. It was followed by the June Producer Price Index, which showed an 11.3 percent year-over-year growth. July data brought a bit of relief; the CPI was up 8.5 percent year-over-year. The Fed’s preferred inflation measurement, the Personal Consumption Expenditures (PCE) index, in June increased 6.8 percent year over year, the largest increase in 40 years. Even when their more volatile components such as energy and food are pruned away, the consumer-level inflation readings were still far above the Fed’s 2.0 percent growth target, with the core PCE index increasing by 4.8 percent and the core CPI registering a 5.9 percent increase. Having already given financial markets two 75-basis-point increases in the overnight interest rate, the Fed seems to be dedicated to keeping a foot on the brakes in a classic central bank effort to bring down inflation.

Another important dimension of the economy must be included in the sketch I have just provided. Yes, inflation is roaring, but so is employment. Although total employment is still down more than 500,000 workers from prepandemic February 2020 with the unemployment rate resting at 3.6 percent, new additions to payrolls have averaged over 370,000 for the past four months. With jobs readily available and with checking accounts still a bit flush with government stimulus payments, consumers are spending, retail sales are up, travel activities are burgeoning, and restaurants are challenged to find servers to take care of their customers. This economy has two faces. One is frowning and worried about Fed actions to slow the economy, and the other still smiles but is bothered a lot by rising prices.

How This Report Is Organized

In this report, I will focus more closely on major facets of the macro economy. In the first section I use perhaps the simplest tool in the economist’s tool kit, circular flow analysis, in an effort to explain why Americans are plagued by the odd combination of high inflation, tight labor markets, and burgeoning consumer spending while the economy contracts. I will also provide summaries of expected GDP growth for the year ahead and beyond. In the next section, I look closely at the misery index, created by economist Arthur Okun, which combines the unemployment and inflation rates to give an overall measure of consumer well-being, and I discuss the index’s recent performance and what happens when policymakers can, in effect, choose which of the index’s two components they will increase. In the section that follows, I focus on inflation as a tax to cover the cost of the “free” stimulus and other government benefits that were provided to ease the pandemic’s pain.

The report contains a special section focusing on the Mercatus Center’s leading research on monitoring and measuring regulatory activities across the nation. Written by Stephen Strosko, this section describes some powerful new analytical tools that have been developed by the Mercatus Policy Analytics Project for quantifying and visualizing the reach of government regulation and restrictions. Finally, the report concludes with a couple of book reviews.

Taking a Closer Look

In 1803, economist Jean-Baptiste Say put forth a strong argument that in market economies, supply creates its own demand. On the basis of common sense, observations, and reason, Say pointed out that when workers and factor owners produce goods and services that go to markets, the pay of workers and owners is based directly on what they produce. Pay day means that all workers and owners taken together can head to the market and buy what they just produced, paying for their purchases with their earnings from producing the goods in the first place.

From Say to Circular Flow

Say’s insight led to the development of economists’ simple circular flow analysis that puts households (which are the suppliers of labor, land, and capital) at one side of the flow and producers (which buy and hire inputs in order to produce output) at the other side of the circle. One can measure the system’s GDP by putting a meter on the flow of goods and services that are produced, the product of the system, or measure the income GDP counterpart by metering the flow of income to households when production occurs.

The simple circular flow analysis becomes more complicated when money enters the picture and even more complicated again when government and a money printing press enter. When those elements are added, the real link between production and earnings is severed. It is then possible for households to have money income when they produce nothing and, thus, for inflation to enter the picture. Stepping away from this simple analysis, one can see how pandemic stimulus money did just that. One can imagine other complications that affect the circular flow when transportation of inputs and outputs is added to the picture. Breakdowns or interruptions in transportation can yield supply chain issues that, given the supply of money circulating, can yield inflation.

From Inflation to Recession

America is currently experiencing a serious bout of inflation from at least two sources, the printing press and supply chain interruptions, and steps being taken by the Fed to extinguish the inflationary fires will likely push the economy into recession territory. As already mentioned, the price of consumer goods is rising nearly across the board at a record pace. The CPI increased by 8.5 percent year over year in July, well ahead of June’s 5.3 percent year-over-year gain in wages and salaries now being recorded. Working people, on average, are getting poorer. Of the prices of goods being tracked in the CPI, the skyrocketing price of gasoline is taking an especially heavy toll on everyone who drives a car to work or carpools children to school. Thus, the FOMC is now hitting the economy’s brakes by raising interest rates. It is promising that a slower economy is on the way, one which travels at a safer speed and leaves Americans with less inflation. It is also praying, figuratively or otherwise, that the country will not skid into a recession.

I want to be clear on what economists mean when using the r-word. As defined by the NBER, a recession is “a significant decline in economic activity that is spread across the economy and that lasts more than a few months.” To determine whether that definition is met, NBER experts review history and examine lots of data. A dating committee observes the economy’s ups and downs, identifies the most recent peak of real economic growth and the period of decline that follows, and marks the date of the trough where growth starts climbing upward again. The peak-to-trough period marks the recession’s duration.

Since 1948, there have been 11 NBER-designated recessions, with the longest occurring in 2007–2009 (18 months peak to trough) and the shortest in 2020 (just 2 months). Generally speaking, with the 2020 pandemic offering an exception to the rule, any NBER-classified recession contains at least two quarters of negative real GDP growth. The 11 recessions can be placed into two categories: those caused primarily by Fed action to reduce inflation (which may be called deliberate recessions) and those that resulted from external shocks such as 9/11, the Arab oil embargoes, and COVID-19 shutdowns and layoffs. Of course, recessions may be caused by a combination of Fed action and external shocks. This will be the case if 2022 or 2023 delivers a recession.

What to Expect and When to Expect It

According to Bureau of Economic Analysis (BEA) data, the United States experienced −1.6 percent real GDP growth in 2022’s first quarter. The first recession shoe may have already dropped; the other became untied on July 28 when the BEA released the first estimate for second-quarter growth. The estimate was −0.9 percent growth, which of course can be revised when more data are available. The small negative growth estimate was expected. On July 7, Goldman Sachs announced that its forecasters were expecting to see −0.7 percent second-quarter growth. Ongoing estimates maintained by the Federal Reserve Bank of Atlanta called for −1.2 percent GDP growth for second quarter on July 8, 2022. I note that Wells Fargo economists are calling for −0.2 percent growth for all of 2022. I should point out that the Federal Reserve Bank of New York GDP forecasting model now sees −0.6 percent growth for 2022, −0.5 percent for 2023, and 0.4 percent growth for 2024. Thankfully, these negative growth forecasts are relatively small. Ongoing GDP growth estimates maintained by the Federal Reserve Bank of Atlanta had called for −1.2 percent growth for second quarter. Taken together, they suggest that the country has entered a time of near-zero real GDP growth and that it will remain in troubled waters until early 2023.

Exactly how concerned should Americans be about that?

This is the trickier question. First, they should recognize that the difference between very weak GDP growth and the slightly negative contraction shown in the earlier-mentioned forecasts is of interest to keepers of economic records, who like to talk in terms of recessions, but not of grave concern for ordinary people who are worried about the practical realities of meeting payrolls, keeping jobs, paying off debt, and buying groceries and gasoline. Yes, some people who are on shakier ground will be hurt, and all prefer positive gains in prosperity to negative ones, but a low-level recession is not a disaster for most Americans.

What if things get nasty? What if the combination of the Russo-Ukrainian War, a more severe energy crisis, and persistent Fed braking do enough to force the economy fully off the tracks? Yes, any of these things can happen, but there is one safeguard to keep in mind: unlike with any other recessionary period, US consumers, businesses and other organizations today hold huge amounts of stimulus-provided cash in checking accounts. At the end of July these balances summed to $5.0 trillion, as compared with $1.6 trillion in February 2020, which at that time was a peak value. There is a large shock absorber waiting to be exercised, should it be needed.

It’s an odd situation, because that huge shot of helpful cash contributed to the spike in inflation, and thus any potential recession, in the first place. Trillions of dollars in stimulus flowed through the economy. Some people could afford to work less. (Even now, the share of working-age people employed in the United States is less than the December 2019, prepandemic share.) Other people used the extra dollars to bid for a limited stock of automobiles, trucks, washing machines, or anything else they desire. Inflation followed. Now, the US economy is out of balance with an unusual set of twins: record low unemployment and record high inflation brought on by an unusual combination of stimulus money and supply chain breakdowns. Yet a lot of the stimulus money is still resting and could perhaps help lessen the pain of a recession it helped to spur.

Recession ahead? I think so. Severe? Not likely. Mild and short lived, instead. That said, Americans should keep their seatbelts fastened.

How Do You Want Your Misery?

Inflation or Unemployment: Which Misery Will It Be?

The most recent data for US unemployment and inflation tell us that the misery index is again riding high, and that means most people are a little lower in the saddle. The index is the sum of the CPI and unemployment rate, and it hit 12.7 percent in June, following increases of 12.2 percent in May and 11.8 percent in April. Now, it seems, the Fed is attempting to rein in inflation by allowing the unemployment rate to head north. If the Fed is successful, one component of misery will be exchanged for another.

Okun invented the index in the 1970s after serving in President Lyndon Johnson’s White House and later observing the stagflation that followed President Richard Nixon’s 1971 decision to sever the linkage between the US dollar and gold. Since the index’s first becoming a popular measure of well-being, improvements or reversals in the index have come to be seen as an indicator of a president’s political prospects.

When President Joe Biden came into office, the index stood at 7.7 percent. Before that, it had hit 15.0 percent in March 2020 in association with the COVID-19 shutdowns, and then it began falling. It is now headed north again, up by 5.0 percentage points since Biden took office. At this point, the misery index under Biden’s watch ranks fourth highest among those to exist during any administration since 1948. (The index went up 9.2 points when President Nixon was in office, 7.0 points during the Carter administration, and 5.7 points during the Eisenhower years. It fell during the Clinton, Obama, and George W. Bush years and hardly budged during the Trump administration.)

Of course, there are different underlying situations and stories associated with each presidential period, and these should be considered. For example, some presidents had to cope with past periods of high inflation and high unemployment followed by disruptions caused by Arab oil embargoes and policies taken to ease the associated pain. In some cases, the inflation component of the index was energized by central bank decisions to increase the supply of money in the economy—something the Fed has done recently to cover Congress and the president’s stimulus spending.

There are other parallels today. For example, rising oil prices are again causing trouble. But with the current 3.6 percent unemployment rate, almost all the increase in the index is coming from the inflation component, and that component includes far more than oil prices.

Even America’s low unemployment rate is creating some forms of misery. Consider the thousands of flight cancellations stemming from the inability to staff airports and planes, or the unhappiness that comes when restaurant owners must close dining rooms for lack of servers.

Some scholars argue, on the basis of empirical studies, that if given a choice, consumers would rather have more inflation than higher unemployment. Clearly, the pain from unemployment is concentrated among the jobless whereas inflation tends to spread the misery across a vast number of people (while hitting lower-income people the hardest). This tradeoff lies at the foundation of the consternation over the Fed’s efforts to hammer down inflation by slowing the economy, which will inevitably increase unemployment.

Ultimately, the misery index reminds Americans of the importance of avoiding inflation in the first place. After all, inflation is fundamentally a monetary phenomenon, and humans control the flow of money into the economy and, therefore, the flow of misery.

Is Inflation Really Necessary?

With President Biden jawboning petroleum company executives, telling them to lower gasoline prices now, and talking about employing the Defense Production Act to force petroleum companies to open the oil valves wider and produce more gasoline—this after earlier opposition to expanded petroleum production in the interest of environmental protection—one is reminded that there is no such thing as a government-provided outcome, environmental or otherwise, without cost. Consumer outrage at $5.00 per gallon gas is evidently strong enough to get the attention of a president known for his commitment to improving the condition of the planet.

It’s another version of that old saw famously associated with Nobel laureate and economist Milton Friedman: “There is no such thing as a free lunch.” Today, inflation is putting a price tag on past political actions that only sounded free at the time.

Friedman, known for his wit and unwavering free-market critique of public policy, was making a simple point: If society’s scarce resources are being used to prepare this proverbial lunch—even if it’s to orchestrate cleaner air or some other worthwhile goal—then one can be certain that some people, somewhere, are paying the bill, voluntarily or otherwise.

Unwavering in his support of the freedom to choose, Friedman once led a march during the Vietnam War with much younger men and women protesting the draft and calling for an all-volunteer army. It was not defense policy that motivated him as much as the cost imposed when individuals have no choice but to go off to war without being fully compensated. Eventually, of course, his message was received, and the laws were changed. Today, the United States has an all-volunteer military.

This said, the free-lunch politics of most other issues are such that promises get attention and, when placed in front of the people and their representatives, approval. Through a pageant of presidents from Obama to Trump to Biden and in face of economic difficulties, Americans have been promised and have received subsidies and checks from the federal government that entered their bank accounts as if by magic.

At the same time, Americans were promised that only higher-income individuals would face tax increases to help pay for the checks. Yes, it sounded a lot like a free lunch. But now, with all that extra cash circulating, every American is facing 9 percent or better inflation, no matter their income level. No amount of planning and promising could negate Friedman’s rule, and the bill for the free lunch hits most Americans each time they go shopping. But because lower-income people spend a larger share of their income on consumption, the “inflation income tax” is more painful.

Of course, political promises that sound like free lunches come in all kinds of forms. During the Trump administration, animosity toward China regarding respect for intellectual property rights and other trade matters led to the imposition of tariffs on a large variety of Chinese goods imported by the United States. The purpose, one could argue, was to provide “free” trade protection to corporate investors who were complaining about China’s abusive actions. No doubt, plenty of investors had legitimate gripes, but the tariffs’ real costs were consistently downplayed by the administration. Indeed, President Trump regularly told the American people that the Chinese were paying the cost of the tariffs, not American consumers.

All along, those involved in these matters had to know that American consumers would be picking up the tab for the higher-priced Chinese goods. There is no such thing as free enforcement of trade policies on unwilling partners. Now, it seems, with inflation alarms ringing loudly, President Biden is giving serious consideration to removing some of the Trump-imposed tariffs, all in the interest of lifting the burden that was not so long ago imposed through active policymaking on American consumers.

Yes, sometimes the check for a free lunch is slow to come, but eventually the buck will stop, and someone will have to pay the bill.

RegData Regulatory Spotlight: New Tools to Explore Public Policy

Stephen Strosko

Technical Director, Policy Analytics Project, Mercatus Center at George Mason University

As the legal landscape of the world continues to become more complex and intertwined, innovative tools are needed to decipher and quantify this complexity. Last quarter, the developers at the Mercatus Center released new data and tools aimed at assisting in reducing this landscape’s complexity. The following section briefly describes the new data and tools and then walks through an example of how they can be used to draw meaningful policy insights by looking at the energy sector.

One of the most popular data products released by the QuantGov team at the Mercatus Center is State RegData. State RegData quantifies the number of regulations at the state level and has been cited extensively in both policy and academic research. Self-titled, “State RegData—Definitive Edition, Regulations,” the 2022 release of State RegData is an improvement over previous iterations in that it provides data on every US state that has a regulatory or statutory code in publication for the year 2022, totaling more than 146,000 documents.

In addition, “State RegData—Definitive Edition, Regulations” introduces historical agency and regulator data and cluster-level analysis. Because every state has a different makeup of regulators and agencies, clusters allow researchers to group similar regulators into easy-to-use categories such as “banking, insurance, and securities.” These categories can then be used in cross-state comparisons. Finally, just like previous iterations, “State RegData—Definitive Edition, Regulations” provides information on regulatory complexity, the association between regulations and different economic industries, and basic regulatory restriction counts.

Previously, State RegData allowed users to have only a one-dimensional view of a state’s data. If researchers were interested in the total amount of regulatory restrictions related to a certain economic industry, they could retrieve this information. But at the end of the day, only a simple single-line chart could be created with that information. With “State RegData—Definitive Edition, Regulations,” adding the ability to dive into metrics on the basis of specific state regulators produces more powerful data and, therefore, the need for more powerful tools.

RegHub.ai, the marquee tool of the QuantGov platform, provides three main tracks for users to interact with data and documents associated with “State RegData—Definitive Edition, Regulations.” Users can search for documents by using custom keyword searches to identify documents relevant to the question at hand. These searches can be further filtered by jurisdiction, year, document type, and topic, and search results can even be downloaded. Users can also download documents in precompiled ZIP folders that can be immediately used to seed unique research and analysis. A third option allows users to download data—everything from high-level summary data points to custom data requests that are retrieved on-command from any QuantGov database.

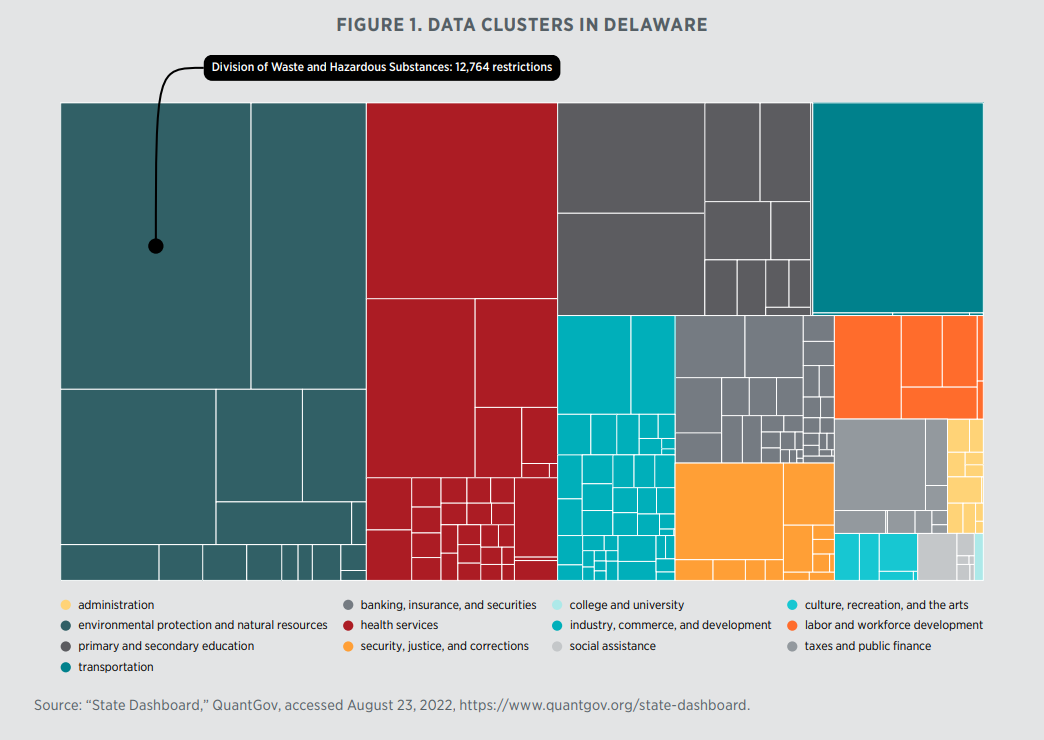

The new data and tools can easily be combined to retrieve interesting information about different policy-related questions. The energy sector is fruitful ground for this exploration. For example, a user from Delaware might be interested in exploring the data in an environmental protection and natural resources cluster, which encompasses regulations that affect producers in the energy sector. Using the QuantGov interactive state dashboard, the user can easily drill down into Delaware’s energy cluster data and see the largest regulators. The Division of Waste and Hazardous Substances is responsible for 12,764 regulatory restrictions and is by far the largest regulator in this cluster (see figure 1).

Using the RegHub tool, a user could examine the underlying data more closely by using the custom data downloader. For example, while using this tool, the user could input the following variables:

Country: “United States,”

Jurisdiction: “Delaware”

Document Type: “Regulations”

Unit: “Document”

Series: “Total Restrictions by Agency”

Agency Cluster: “Environmental Protection Cluster”

Doing so would allow for a custom CSV download of data and metadata for the individual regulatory documents. For further analysis, the user could download the documents themselves and analyze the text directly through the document downloader on RegHub.

Being able to directly link those ebbs and flows of regulatory action to specific regulatory documents and other metadata that RegHub provides (such as document complexity, the relationship between the document and specific economic industries, the relationship between the document and other jurisdictions, etc.) immediately opens a variety of avenues that lead to deep and meaningful research that can have long-lasting policy impact.Yandle’s Reading Table

In 1977, chair of the Council of Economic Advisers, Brookings Institution economist Charles L. Schultze, published a bombshell of a book, The Public Use of Private Interest. The book is based on a series of lectures Schultze had delivered the year before at Harvard. Its purpose was to show how, by channeling and harnessing market forces, government could become more effective and efficient in achieving its goals. The book focuses on federal regulation, and its description set the stage:

"According to conventional wisdom, government may intervene when private markets fail to provide goods and services that society values. This view has led to the passage of much legislation and the creation of a host of agencies that have attempted, by exquisitely detailed regulations, to compel legislatively defined behavior in a broad range of activities affecting society as a whole—health care, housing, pollution abatement, transportation, to name only a few. Far from achieving the goals of the legislators and regulators, these efforts have been largely ineffective; worse, they have spawned endless litigation and countless administrative proceedings as the individuals and firms on who the regulations fall seek to avoid, or at least soften, their impact (emphasis added)."Schultze was not optimistic about the prospects for what might be termed market-enlightened regulatory reform.

Now, 45 years later, another Brookings economist, Clifford Winston, has given readers a more extensive treatment of how government might more successfully employ market forces to serve the public interest in his Gaining Ground: Markets Helping Government. Reaching beyond economic issues, Winston addresses broader social goals, such as reducing poverty and perceived labor market inequities, and shows how harnessing market forces could improve public policies in those areas too. One might optimistically expect Winston’s review of the topic to report significant progress after considering Schultze’s assessment, but I must quickly note that Winston, like Schultze, is not optimistic about the prospects for improving things. One might wonder why, after 45 years, so little progress seems to have been made and why the idea of making public use of market forces to achieve government goals is perhaps seen as being even more problematic now than in 1977. I offer more on this later.

On a personal note, I should point out that Schultze’s earlier book was not a heavily documented academic treatise like the Winston volume, but its contents fed lots of conversation among members of the White House staff. At the time the book was published, I was a senior economist on the staff of the Council on Wage and Price Stability working with a small group—about eight other economists, as I recall—led by James C. Miller III. We were reviewing and commenting on newly proposed federal regulations and attempting to apply market logic in making the final rules more cost-effective. That small group, then called the Regulatory Analysis Review Group, was the forerunner to what is today the Office of Information and Regulatory Affairs, which is part of the Executive Office of the President.

For more than four decades since then, economists, lawyers, and policy analysts have worked to bring to bear market logic on public-sector actions. All who have been a part of this enterprise understand the difficulties involved; any successes involve overcoming the overwhelming forces of rent-seeking behavior. Those involved generally accept the notion that market forces playing through the political process, what may be called the forces of public choice, drive toward outcomes that redistribute income in favor of regulated individuals or industries. This notion leads to the general conclusion that one should not expect to find efficiency when reviewing past government actions, but rather redistribution to rent-seekers who successfully use the political process in their search for increased wealth. To expect otherwise is to look for love in all the wrong places.

Winston’s Book and Evolving Regulatory Theory

Winston’s book might helpfully be viewed as a vastly expanded and annotated version of the earlier Schultze treatise. Indeed, it is even more than that, for Winston’s extensive survey of empirical work—with 31 pages of references—is a report on Winston’s ongoing Brookings enterprise that will continue to provide scientific evidence for the possibilities of using private interests to service public purposes. I note that Winston spills no ink in discussion of theories of government and so does not deal with the seemingly popular notion that elected officials are primarily motivated to serve the public interest, that upon taking their oaths office, they are marginally transformed from being ordinary mortals who more often than not are understood to serve their own interests, somehow specified, yet in their rebirth will walk away from the special interest groups that may have indeed helped them gain office in the first place.

Yet George J. Stigler’s competing idea that the behavior of politicians is best understood by following the money generated for special interest groups that gain political favors might better explain why market-based efficiency-enhancing rules and regulation get short shrift when political behavior is examined closely. Even during Stigler’s day, and certainly since then, those who have struggled with regulatory reform have learned that politicians face a heavy opportunity cost when they try to divert their energies away from serving the special interests that keep them in office and toward serving the public interest.

Put another way, there is no meaningful political constituency or voting block that struggles to make the world more competitive. Indeed, just the reverse seems to prevail. The important political interest groups seem dedicated, more often than not, to eliminating competition, to having resources redistributed in their direction, and to regaining ground that, in their opinion, is richly deserved. On occasion, of course, it is possible that improving efficiency through the use of the market process coincides with achieving a special interest group’s rent-seeking desires. President Carter’s 1975 promise to deregulate natural gas pricing to get Louisiana’s nomination vote may be an example. Massachusetts Senator Teddy Kennedy’s successful effort to champion airline deregulation, because doing so provided massive gains to ordinary Americans, could be another example. The removal of tariffs on China-produced solar panels by President Biden so that a US industry can improve its output and profitability, if successful, could be another example.

How Winston Sees the Challenge and How the Book Is Organized

Rather than heralding how economics might address today’s swirling political cauldron, the book is more defensive of the role economics now plays in the process. Early on, the book notes that economists and any who speak favorably of capitalism are generally not respected in Washington’s progressive world. In a way echoing Schultze, Winston speaks to the challenges faced by those who wish to apply economic logic to regulatory decision-making—or to any part of government. He points out that the ongoing Washington policy debate

"does not account for the accumulated empirical evidence on the efficacy of market forces and government policies to accomplish the nation’s goals. This book fills that gap by synthesizing the available evidence and by arguing that, in contrast to current dissatisfaction with markets, American society has gained ground when government has allowed markets to help accomplish . . . economic and social goals, especially when government policies have made little progress in achieving those goals. I further argue that society could gain even more ground if government removed constraints, which would enable markets to play a greater role in the process."

Winston’s timely and provocative book has four major parts. I point out that each part contains common components as well as excellent analytical tables. Part 1 addresses how attention to market forces could help improve achievement of economic goals. Chapters in that part address antitrust and anticompetitive behavior and improved flows of information and deal with external costs such as pollution, traffic congestion, and airport noise and with the enhancement of innovation and discovery of improved technologies. Part 2 focuses on achievement of social goals and considers poverty, discrimination in labor markets, and—an old topic—enhanced production of merit goods, which means goods and services that are deemed to be socially desirable by authority figures. The book’s third part offers a synthesis for the reader to consider, an effort by the author to explain why market forces, after so many years of study and analysis, occupy an inferior seat at the table when policy choices are being considered. Finally, the last part of the book provides a hard-hitting analysis of federal government failures to deal effectively with the COVID-19 pandemic, in spite of the fact that recent such public health experiences have made it clear that the nation was ill prepared for dealing with precisely such an emergency. Here Winston applies lessons learned from his account of past regulatory failures and discusses how what must be “termed amazing market responses” that led to rapid identification, production, and delivery of COVID-19 vaccinations emerged, in spite of dismal White House leadership and confusion within the ranks of the nation’s chief healthcare agencies.

Final Thoughts

Winston has provided an excellent and extensive treatment of the US regulatory state, one that is replete with summaries of empirical work that shed important light on the relative effectiveness of countless regulatory efforts and how market forces might be employed to improve outcomes. The work obviously represents a dedicated effort on the author’s part, an effort that will be continuing along with his productive professional career. Upon reading the book, one is not left with the feeling that better days are in the offing for market-based reforms. However, one is left with the feeling that the evidence and logic Winston has assembled will have a useful and future valuable effect in the ongoing regulatory struggle.

A Breath of Fresh Air

Are you tired of receiving what seems to be an endless stream of terrible news—wars, shootings, climate change, COVID-19, inflation, January 6 hearings—and wishing that someone would have something positive and perhaps even inspiring to say about human behavior? If so, you will enjoy the breath of fresh air found in Lawrence Reed’s 2016 book Real Heroes: Inspiring Stories of Courage, Character, and Conviction.

Reed, noted for his unusual ability to describe the beneficial forces of free markets and president of the Foundation for Economic Education has organized a collection of 40 short vignettes that capture the essence of people who, in Reed’s opinion, lived truly heroic lives. And what does it take to make Reed’s hero cut? Reed addresses the question in the book’s introduction and describes critical characteristics of those who exhibit heroic behavior. His first and most important characteristic is character, which he describes as the sum of choices people have made across their lives. As he sees it, people of high character do not cut moral corners when making decisions—or they do so less often than nonheroes. Character is not sacrificed for “money, attention, power, or other ephemeral gratifications.”

What Does It Take to Be a Hero?

Going further, Reed indicates that his heroes “embody traits like honesty, gratitude, intellectual humility, personal responsibility, self-discipline, inventiveness, entrepreneurship, vision, compassion, an optimism.” Wow! That’s saying a lot. But embodying such traits is not enough. Reed’s heroes must display these traits continually across a lifetime. He is not looking for individuals who may have performed one or a handful of truly extraordinary acts. Reed’s heroes show sustained character, and as Reed points out sustained character is essential to liberty. And that is just the first essential characteristic. There are more.

Added to character are courage and conviction. Reed’s heroes are not timid. They bravely keep going when more timid souls turn back, and their courage relates to taking on physical as well as moral challenges. And this introduces conviction. The real hero will bravely take a moral stand because it is the right thing to do.

Having laid a foundation that describes the behavior of real heroes, Reed offers short biographical sketches for his 40 favorites. The panoply of heroes reaches from time before Christ to the current period, and in each case, Reed offers his personal justification for each hero included. The parade begins with Marcus Tullius Cicero, born in 106 BC a short distance from Rome, who went on to become a brilliant lawyer and prosecutor. He then was elected to public office and, in 63 BC, elected to Rome’s highest office, coconsul. In the republic at the time, the highest office was shared by two elected individuals, each with a one-year term of office, and each able to veto the other’s opinion.

Cicero’s oratorical ability brought him the support of the Senate at the time, which enabled Rome temporarily to put down the rise of a military dictatorship. His brilliant leadership led to his being given the title Father of the Country. Yet long before his time, centuries of corruption and political power struggles had laid a foundation for Julius Caesar’s emerging grasp for power, for Caesar’s assassination, and, in spite of Cicero’s brilliant but fatal opposition, for Mark Antony’s successful effort to become dictator. Antony ordered Cicero’s murder.

Reed highlights Cicero’s defense of liberty, constitutional government, due process, habeas corpus, and the teaching of private virtues. Reed points out that if he could have an hour with Cicero, he would thank him for daring leadership and for his articulation of principles of liberty. As with each of his short vignettes, Reed offers “lessons learned” and points out that Cicero displayed moral courage and a strong commitment to defend liberty.

Beginning with Cicero, Reed’s collection of heroes reaches to the current time and includes highly recognizable historic figures such as Adam Smith, Edmund Burke, Harriet Tubman, and George Eastman. But there are also surprises such as poet and hymnwriter Fanny Crosby, boxer Joe Louis, and Olympic gold medal winner Jesse Owens, which is what makes reading the collection rewarding. Consider Fanny Crosby, for example. Born in Putnam County, New York, in 1820, Crosby lost her sight as a small infant, but this did not limit her prodigious effort to write thousands of poems, write more hymns (over 9,000) than any previous composer, and live a life dedicated to the support of liberty and democracy. Indeed, perhaps an example of compensation for blindness, Crosby demonstrated a formidable ability to memorize. By age 15, she had memorized the first five books of the Old Testament and the first four gospels in the New Testament. While studying at the New York Institution for the Blind, she learned to play the guitar, piano, organ, and harp.

While in her 20s, Crosby became a mission worker in New York and ministered to countless people afflicted in a cholera epidemic. As a successful hymn writer, Crosby focused on spreading the gospel, hoping that she would change lives for the better. Widely recognized for her talent and good works, Crosby was invited countless times to visit the White House. She is said to have met 21 presidents in her lifetime. As he does for each of the heroes, Reed summarizes Crosby’s amazing life and identifies two lessons to be learned from it: The first is to count your blessings—Crosby counted her blindness as a blessing—and the second is to develop a work ethic—Crosby would often write several hymns in a single day.

Prudence Crandall, another of Reed’s heroes, generated a major controversy on April 1, 1833, in Canterbury, Connecticut. The issue? With private money, Crandall had opened a boarding school for young women of color, this as an addition to her existing female school. In effect, Crandall opened the first integrated school in America, but not without a major outcry from community members. Before the controversy would end, Crandall would be arrested, endure three court cases, and see her school vandalized. Whereas slavery no longer existed in Connecticut, racism was alive and well.

But who was Crandall, and why did she care about educating young black girls? She had been reared in a Quaker home and had attended a Quaker boarding school herself. She dreamed of becoming a teacher in her own school. She was also a tough and determined woman. Vilified by the community for accepting black students and suffering losses as parents of white students turned away, Crandall held true to her convictions, dug her heels in, and decided to focus exclusively on educating black female students.

With financial support coming from wealthy individuals who agreed with her dream, she opened her school doors wide and accepted students from throughout New England. With growing outrage stirring the political scene, the Connecticut legislature responded by passing a law that made it illegal for any black student to attend any Connecticut school without first having permission of local citizens. Crandall fought enforcement of the law successfully, given that her prospective students were US citizens and could travel and engage wherever they might wish. But whereas she won in court, she lost in the community, which refused to provide vital services to the school and students. Ultimately, she was driven out, and she finally moved to Kansas, where she continued to do good works.

So what are the two lessons called to our attention in the Crandall story? Larry Reed says the first is to fight prejudice, which Crandall referred to as the “mother of abominations,” and the second is to remember government’s proper place.

A Final Thought on Reed’s Collection

Through the collection of short bios, the reader encounters powerful personalities who, in spite of all kinds of hardships, even including prison sentences, kept their eyes on the prize and worked to make the world a better place. As Reed points out, there are real heroes all around us, and as he suggests, it is possible that one of us may become heroic.

Listen to a conversation with Bruce discussing this Economic Situation Report on the Mercatus Policy Download here.