- | Corporate Welfare Corporate Welfare

- | Expert Commentary Expert Commentary

- |

The Export-Import Bank Subsidizes the Already Wealthy

Without congressional reauthorization, the Export-Import Bank, which guarantees loans to the overseas customers of thousands of American companies, is slated to close this summer. The future of the institution is driving a wedge between free-market and pro-business Republican lawmakers. The New York Times Room for Debate recently posed this question: "Should Congress save the Export-Import Bank, or let it expire?"

The New York Times Room for Debate posted this question, "Should Congress save the Export-Import Bank, or let it expire?"

Without congressional reauthorization, the Export-Import Bank, which guarantees loans to the overseas customers of thousands of American companies, is slated to close this summer. The future of the institution is driving a wedge between free-market and pro-business Republican lawmakers.

Should Congress save the Export-Import Bank, or let it expire?

Veronique de Rugy provided the following response:

The case against the Export-Import Bank is simple: The government has no business subsidizing gigantic and well-connected American corporations, well-heeled foreign buyers, or the international financiers that profit from the loans.

The Export-Import Bank represents the kind of crony capitalism that is wrong whether its beneficiaries produce green or dirty energy, or whether the firms that receive government privileges are small or massive. What’s more, it doesn’t make economic sense.

Defenders of the bank tout several misleading claims about how it is critical to promote small businesses, jobs, and exports, but the data shows otherwise.

Less than 20 percent of Export-Import Bank lending has benefited “small” businesses — which the bank uniquely and broadly defines as companies with up to 1,500 employees or some $21 million in revenues. More than 99 percent of the small firms in America receive no support from the bank at all.

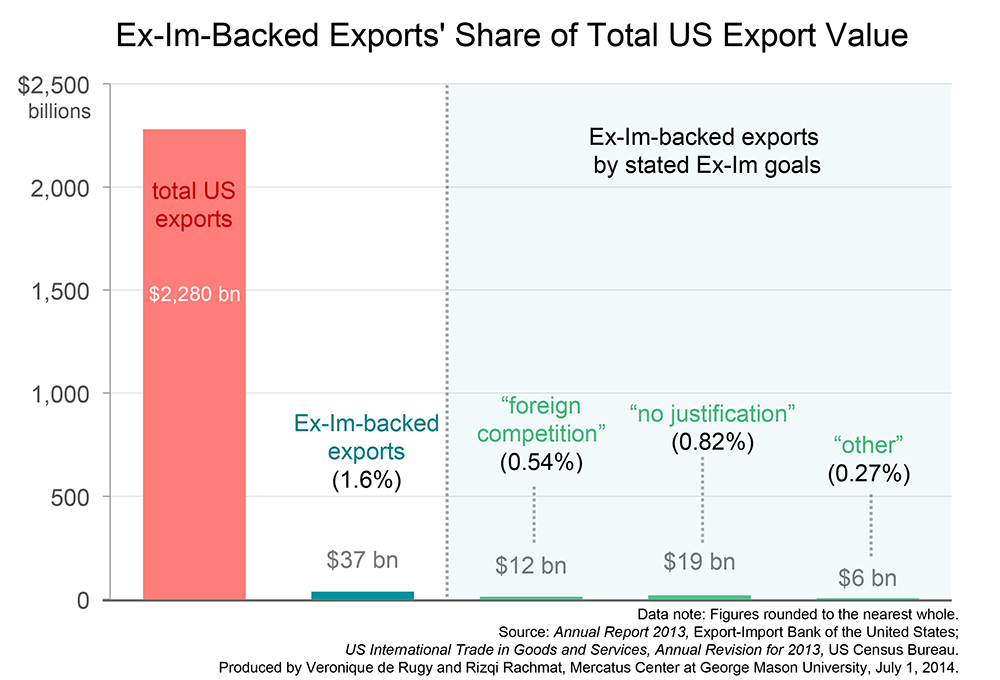

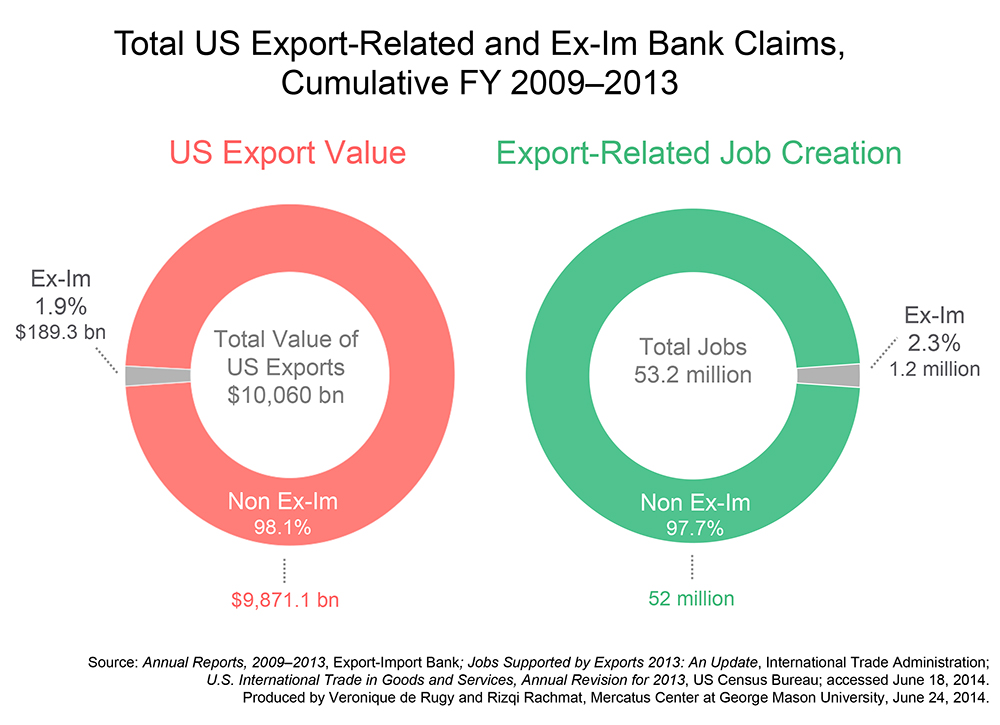

The bank's largesse backs only around 2 percent of all U.S. exports and jobs annually. But trade economists have long reported that the Export-Import Bank doesn't actually increase the net number of jobs and exports; these jobs and exports would exist regardless.

{kind=link}

{kind=link}

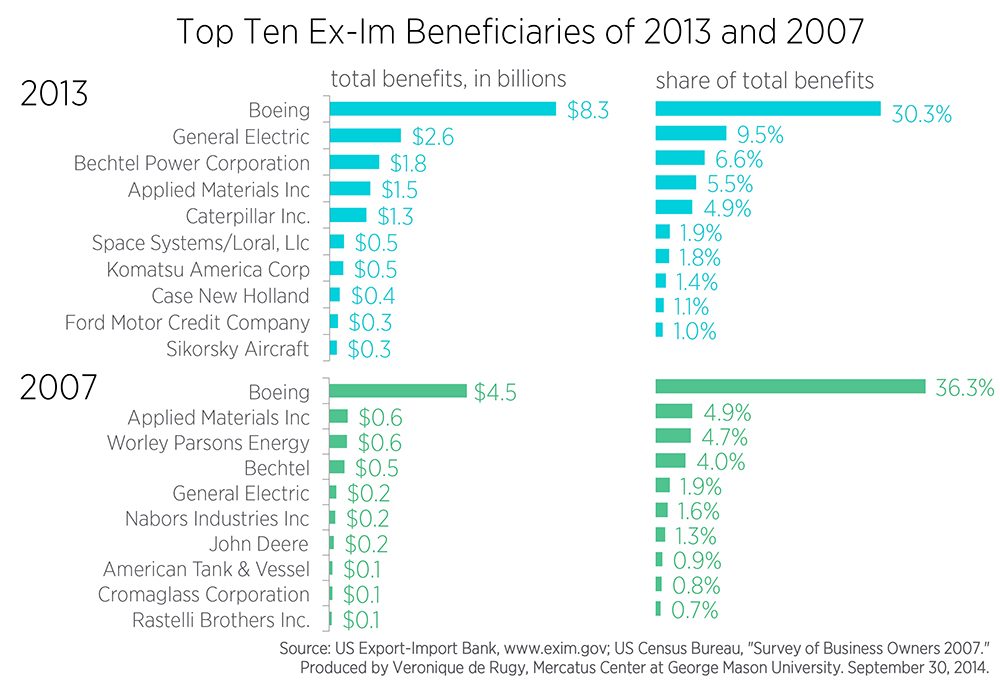

Also, about 65 percent of Export-Import Bank financing increases the profits of ten huge U.S. corporations — including GE, Caterpillar, and Boeing — while transferring their risks onto taxpayers.

{kind=link}

Big foreign buyers make out handsomely as well. Between 2007 and 2013, the bank's top buyer was Pemex, a Mexican state-owned petroleum company with a healthy market capitalization of $416 billion, that nevertheless won $7 billion in U.S. taxpayer-backed financing over those years.

The Export-Import Bank loans these foreign corporations enjoy are much cheaper than the abundant private market financing available. The U.S. government subsidies give them an edge over American competitors — a veritable cherry on top.

But large private U.S. financiers like JP Morgan Chase and Citibank win big, as well, by collecting large fees and interest rates on billion-dollar loans while transferring the risks to the taxpaying public. This kind of Wall Street favoritism isn’t just unfair: It’s systemically dangerous.

The Export-Import Bank isn’t for the little guys, and it doesn’t improve trade or increase the number of jobs — it’s government assistance for big businesses and wealthy private lenders.