- | Monetary Policy Monetary Policy

- | Expert Commentary Expert Commentary

- |

How Futures Markets Could Lead to Better Monetary Policy

Results from a Real World Experiment

Market monetarist economists argue that the most important cause of the Great Recession was a sharp drop in nominal GDP (NGDP) between 2008 and 2009. If true, it would be helpful to policymakers if a market forecast of NGDP growth were available in real time.

In order to learn more about how policymakers might access such a forecast, the Mercatus Center and Hypermind created an NGDP prediction market, where traders can win prizes if they are relatively successful in forecasting NGDP growth over a 12-month period.

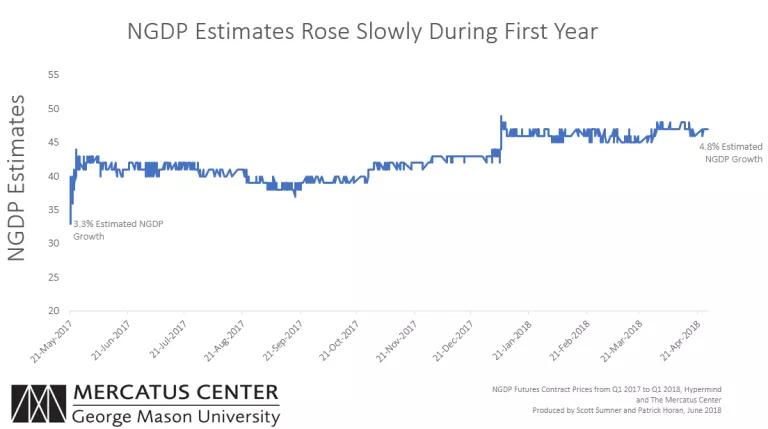

The market included two contests: the first (Year 1) measured NGDP growth from the first quarter of 2017 through the first quarter of 2018 and concluded in April. The second contest, which measures NGDP growth from the first quarter of 2018 through the first quarter of 2019, is ongoing and will be open to participants through next April.

The prizes come from donated funds, so traders do not risk their own money. Nonetheless, participants have an incentive to trade in such a way as to maximize their chance of winning prizes. If almost all traders behave this way, the market price should reveal the consensus forecast of nominal GDP growth. The following graph shows the price of Hypermind NGDP contracts in the Year 1 market, which increased gradually during late 2017 and early 2018:

When the contract matured at the end of April 2018, the price was 48, reflecting a NGDP growth rate of 4.8 percent between the first quarter of 2017 and the first quarter of 2018. This was slightly higher than the roughly 4.1 percent NGDP growth forecast back in the summer of 2017. If these numbers seem high, remember that NGDP includes inflation as well as more commonly reported “real” GDP growth.

Patrick Horan, who manages the Program on Monetary Policy at the Mercatus Center, asked some of the most successful traders a series of questions, including which factors they found most useful in making predictions. The answers showed a wide range of approaches to forecasting. Many traders looked at the consensus private sector forecast of real GDP growth and inflation, while others looked at “nowcasts” produced daily by the Federal Reserve banks of New York and Atlanta. Of course, this begs the question of how the consensus forecast is derived in the first place.

Some traders mentioned policy changes, such as the recent corporate tax cuts. Some looked at recent economic data or asset price movements that might lead to changes in NGDP growth. Several indicated that they consciously took contrarian positions, one because he felt many pundits were too pessimistic about the effects of President Trump’s polices, while another argued that traders were misjudging the stance of Fed policy—assuming it was more contractionary than the actual policy stance.

These different approaches reveal one advantage of market forecasts, which aggregate a wide range of perspectives, yielding the “wisdom of the crowds."

This is in contrast to decision-making by committee, which can become subject to “groupthink." Many participants on the Federal Open Market Committee tend to look at the economy in roughly the same way, using similar models (such as the Phillips Curve) and focusing on similar indicators.

It’s too soon to evaluate the effectiveness of NGDP prediction markets. In recent years, NGDP growth has been fairly stable at roughly 4 percent, and not surprisingly, the price of NGDP contracts has not shown a great deal of volatility. The price of the 2018-19 contract is currently trading at 4.5 percent, slightly below the 2017-18 growth rate, but still a bit stronger than the average growth rate from 2009-17.

In my view, the value of the NGDP prediction market will become apparent when the US next enters a recession. I expect this prediction market to perceive economic weakness before the Fed does. Thus, the creation of an NGDP futures market can be considered a sort of precautionary move.

As an analogy, consider the NASA supported program that searches for asteroids with orbits that might strike Earth. Thus far, the program has been a waste of money; no threatening asteroids have been discovered. If and when a dangerous asteroid is spotted, however, the program may become extremely valuable. Just ask the dinosaurs.

Related Content

- | Monetary Policy Monetary Policy

- | Expert Commentary Expert Commentary

Congressional Report on Monetary Policy Embraces Monetarist Ideas

- | Academic & Student Programs Academic & Student Programs

- | Monetary Policy Monetary Policy

- | Research Papers Research Papers

The Promise of Nominal GDP Targeting

- | Monetary Policy Monetary Policy

- | Expert Commentary Expert Commentary

Embrace of Monetary Policy Rule Strongest Ever by Fed Chair

- | Monetary Policy Monetary Policy

- | Expert Commentary Expert Commentary