- | Financial Markets Financial Markets

- | Expert Commentary Expert Commentary

- |

“Record Bank Profits” May Not Mean “Record Bank Performance”

Profits for the banking industry as a whole may be experiencing “record highs,” but what’s happening at the industry level may not reflect what’s happening for individual banks, many of which are openly concerned with rising costs resulting from an increased regulatory burden.

Why this matters: If we want to understand what bank regulatory policy should look like, it helps to understand the costs and benefits of those regulations. If bank regulations are too costly, they may hamper economic growth and make it harder for consumers and businesses to get credit. If bank regulations are misaligned, they might even encourage risky activity that leads to another financial crisis.

The bottom line:

- Banking industry profits will generally rise over time simply because the economy tends to grow over time, not because all banks are performing better than ever before

- While banking industry profits are at record high levels, that doesn’t tell us much about individual bank performance

- Measures like return on equity or return on assets tell you about individual bank performance; simple industry aggregate dollar based measures of profits do not

- Aggregate measures are likely to be unhelpful in making a policy decision, since they can mask dramatic differences that exist among individual banks (some of whom might be struggling under higher compliance costs, while others might not)

Since the crisis, bankers have complained about regulatory burdens rising. Some of those complaints may not make sense, while others may. Further complicating the debate over regulatory burdens is the common refrain in policy circles about whether bankers are earning “record profits.” In reality, that claim is misleading.

The logic behind the “record profit” fallacy holds that because the banking industry as a whole has generated greater net income than ever before, post-crisis regulatory burdens cannot be causing too many problems.

To really gauge performance, though, you should not merely look at dollar value measures for the entire industry. Instead, you should divide those profits relative to other dollar value measures like total banking assets or total bank equity.

Better still, do the same exercise using bank level data. Doing so does not suggest banks are experiencing any sort of “record performance.” Moreover, you would not expect all banks to experience the same performance. That means in every quarter, some banks will perform relatively well, while others will perform relatively poorly. Bank performance and the entire distribution of performance will also vary over time.

To shed some light on appropriate ways to asses bank performance before and after the crisis, I use simple bank level call report data to show that banks have not performed better than their peak in 2006; and considering what happened after the observed peak values, generating record profits should not be an aim of policy-making. I then show why the “record bank profits” phenomenon is meaningless by comparing total net income and total assets from the Federal Deposit Insurance Corporation’s (FDIC’s) historical data, and nominal GDP. Each series hit “record values” at the end of the sample.

On Bank Performance

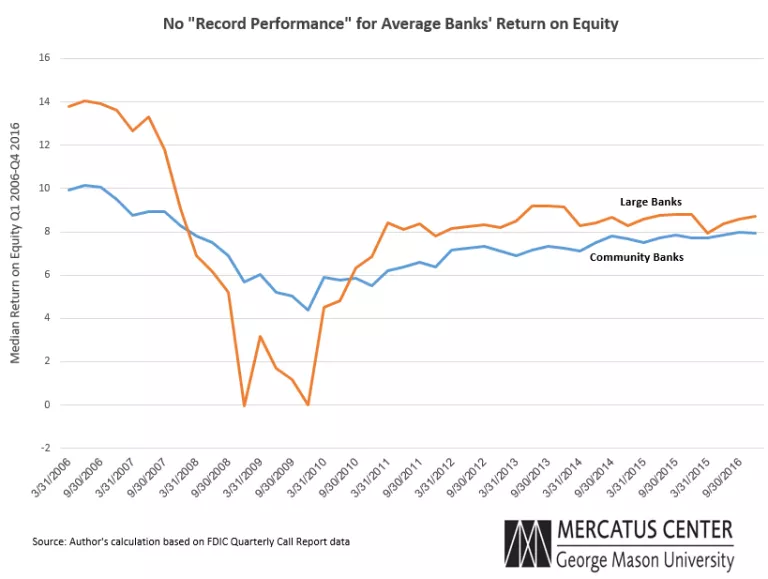

To start, two simple ways to estimate bank performance using call report data include return on equity (ROE) and return on assets (ROA). A bank’s ROE equals the annualized net income as a percent of average total equity, while its ROA equals net income after taxes and extraordinary items as an annualized percent of average total assets. Some summary statistics are available from the FDIC’s Quarterly Banking Profile, but they can also be generated from bank call report data. I use bank call report data to compute the median ROE for large banks with at least $50 billion in total assets, as well as FDIC-defined community banks; the patterns for ROA, while omitted for the sake of brevity, look similar. The median ROE for all banks in the sample resembles the time path of the median ROE for community banks.

Figure 1

Two key take-home points deserve some mention. First, Figure 1 shows that while median ROE have recovered from their low value during the crisis, banks have not experienced any “record performance.” Second, median ROE for large banks tends to exceed that for community banks (and all banks).

That means community bankers may have a point when they complain about regulatory burdens.

Indeed, FDIC Vice-Chairman Thomas Hoenig has been highlighting this problem over the last several years, which in part explains his proposal to change the way banks in the US are regulated.

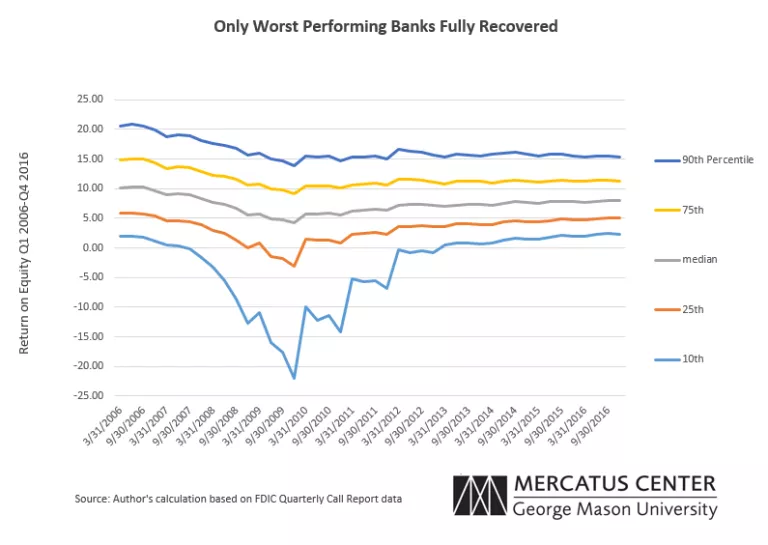

While Figure 1 shows what’s happening at the median, or middle value in the entire distribution, a summary view from the entire distribution is also informative.

Figure 2 shows that across the distribution of banks, the 90th percentile bank’s performance has been mostly flat since 2009, and below the highs experienced in 2006. At the lower percentiles, banks have shown signs of recovery, but have not outperformed the values observed in 2006.

Only the poorest performing banks in Figure 3 have recovered in the sense that the 2016 10th percentile ROEs and ROAs are about equal to the 2006 values, but the values are relatively low. The distribution of outcomes has narrowed since the crisis.

Figure 2

Overall, the bank level data does not reveal any sort of “record performance.” These measures are constructed from accounting data and would reflect bank staff decisions about lending and securities holdings, general economic conditions, and factors that reflect costs, perhaps even compliance costs (although the call report data do not separate compliance costs).

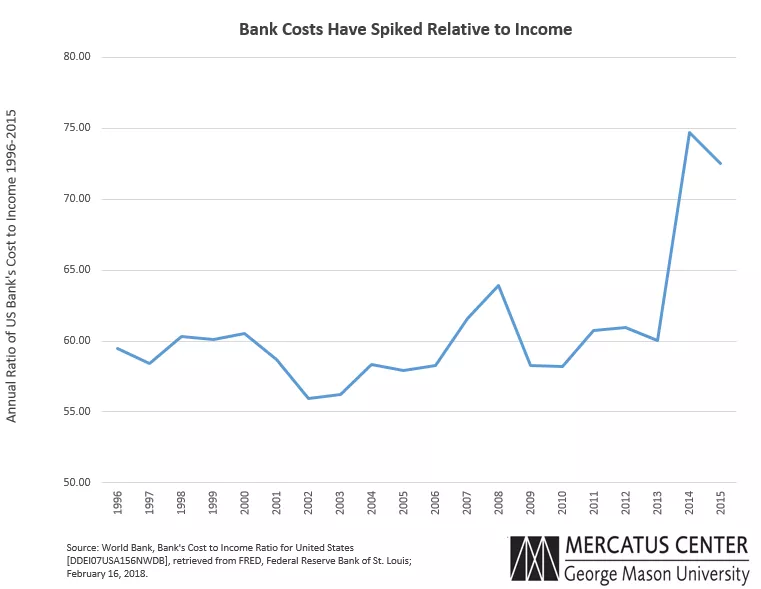

An alternative and aggregate measure available from the Federal Reserve Bank of St. Louis’s FRED database is the cost-to-income ratio for US banks based on Bank Scope data, depicted in Figure 3. The one notable feature in the graph is the spike in costs relative to income in 2014 and 2015. As an aggregate measure, the figure does not specify why the rise has taken place, but it does suggest that costs are higher relative to income, and might also support bankers’ claims about the more challenging economic environment. Having discussed these measures of bank performance, I can now address the “record profit” fallacy.

Figure 3

The "Record Profit" Fallacy

The “record profit” fallacy typically arises from looking at simple (unscaled) time series measures of dollar values such as total loans or total profits. The problem may originate after the FDIC issues press releases concerning the Quarterly Banking Profile. While the press releases may not mention “record profits,” media mentions of the press releases often do.

For example, one report looked at total industry profits and total commercial industrial loans; here, the problem lies with aggregation, as you would not expect this to be true for all banks. Another example reports large bank profits as well as an aggregate across large banks, although the report is more balanced as it mentions that the same pattern is not observed for ROE or ROA. If these are the only data summaries that you rely on, only summary statistics on bank ROE and ROA are relevant for understanding bank profitability. Still, to really get at this issue, an even better but more rigorous approach can be found in this recent working paper, which finds that banks underperformed relative to the bond market as a whole.

To understand the problem, “record profits” may simply arise because aggregate economic activity measured by (nominal or real) GDP tends to grow over time. Ordinarily, you should expect (nominal or real) GDP this year to be greater than GDP last year. With a larger economy, there’s more scope for bank lending, from which banks can generate more earnings.

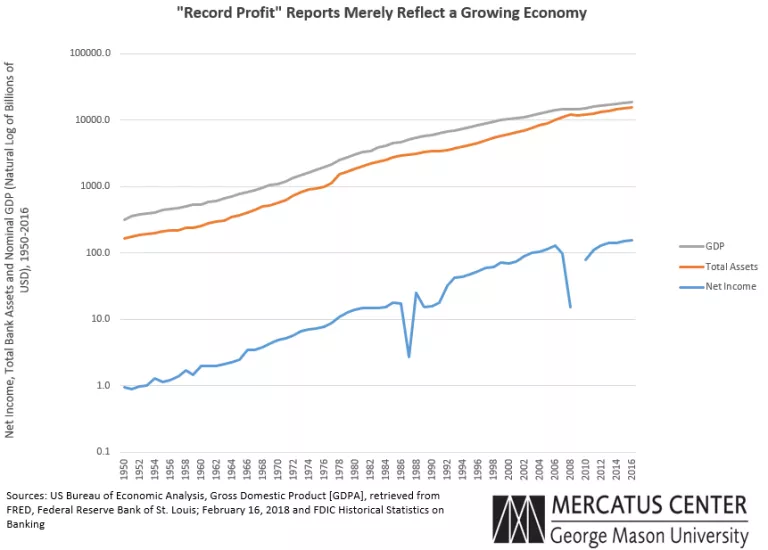

Figure 4 depicts the natural log of billions of dollars of annual nominal GDP, as well as Total Assets and Net Income from the FDIC’s historical statistics database. These are nominal values because that’s how the figures are typically reported in the media or in policy debates. You get the same result qualitatively if you deflate the figures by a measure of the price level, like the Consumer Price Index for All Urban Consumers.

Figure 4

The take-home point from Figure 4 is simply that each of the series reached record values at the end of 2016, and reflects that the economy is larger now than it’s ever been. However, the figure has limited value in terms of welfare implications, since the figure ignores what’s happening at the micro level. Just as you wouldn’t expect to answer a question about whether people are richer by looking at GDP, you shouldn’t expect to answer a question about whether banks are more profitable by looking at aggregate banking industry profits. All told, you can gladly ignore talk of “record bank profits.”

Conclusion

When it comes to making policy decisions that affect individuals or individual entities, the analysis done to justify the decision will ordinarily be more effective if it is based on individual or individual entity-level data rather than on aggregate data. That’s because the details matter. So when a question such as “does regulation hurt banks?” arises, you should begin to answer that question with bank level data, not aggregate data. And on an issue such as profitability, an appropriate measure summarizes performance (like ROE and ROA, if not more complex measures), not just dollar values.