- | Government Spending Government Spending

- | Federal Testimonies Federal Testimonies

- |

Restoring Equity and Fairness to the Social Security Windfall Elimination Provision (WEP) and Government Pension Offset (GPO)

Testimony before the House Committee on Ways and Means, Subcommittee on Social Security

My testimony focuses on two key issues. First, I will explain how the current-law Windfall Elimination Provision (WEP) is overly complex and unfair. Second, I will discuss how reforming the Social Security benefit formula would improve the simplicity and fairness of the WEP, while still maintaining the original public policy purpose. Additionally, though most of my testimony focuses on the WEP, a related provision, the Government Pension Offset (GPO), has similar complexity and fairness problems that should be addressed.

Good morning, Chairman Johnson, Ranking Member Becerra, and members of the subcommittee. Thank you for inviting me to testify today.

My name is Jason Fichtner, and I’m a senior research fellow at the Mercatus Center at George Mason University, where I research fiscal and economic issues, including Social Security. I am also an affiliated professor at Johns Hopkins University, Georgetown University, and Virginia Tech, where I teach courses in economics and public policy. Previously I served in several positions at the Social Security Administration (SSA), including deputy commissioner of Social Security (acting) and chief economist. All opinions I express today are my own and do not necessarily reflect the views of my employers.

I’d like to begin by thanking Chairman Johnson and Ranking Member Becerra for the leadership you provide this committee to ensure that important public policy issues involving Social Security get the attention and debate they deserve and also to ensure that ideas and viewpoints from all sides are aired in a collegial and respectful manner. It is truly a privilege for me to be here testifying before you today.

My testimony focuses on two key issues. First, I will explain how the current-law Windfall Elimination Provision (WEP) is overly complex and unfair. Second, I will discuss how reforming the Social Security benefit formula would improve the simplicity and fairness of the WEP, while still maintaining the original public policy purpose. Additionally, though most of my testimony focuses on the WEP, a related provision, the Government Pension Offset (GPO), has similar complexity and fairness problems that should be addressed.

From this discussion, I hope to leave you with the following takeaways:

- The original public policy intent of the WEP and GPO is to ensure fair treatment between workers with earnings covered by Social Security and workers with earnings that are not covered by Social Security. It is important to maintain this fair treatment between covered and non-covered workers. Hence, a repeal of WEP and GPO would violate the principles of fairness and equity that these provisions were intended to protect.

- Unfortunately, given data limitations at the time the current WEP and GPO provisions were established in law, the WEP and GPO create an overly complex structure rife with what economists call perverse incentives. This can sometimes result in higher replacement rates for some people with high lifetime combined earnings than those with low lifetime earnings. Further, the complexity and lack of transparency in the current WEP and GPO provisions can hinder people’s ability to accurately plan for retirement and potentially cause undue hardship for retirees.

- Much good could come from a relatively straightforward change that would make the Social Security benefit formula a proportional, or prorated, benefit formula based on the replacement rate derived from the current method of determining the primary insurance amount (PIA) but applying it only to the years of covered earnings. This change would allow for the use of one benefit formula for all Social Security beneficiaries, would be simple to understand, and would be fairer than the current system, while maintaining the original intent of fairness and equity of the WEP and GPO provisions.

Original Intent of Ensuring Fairness and Equity Between Covered and Non-Covered Workers

Social Security retirement and disability benefits are funded via a payroll tax on covered earnings. The system is designed with a progressive benefit formula that provides a higher replacement rate for lower-income earners than for higher-income earners. The result is that monthly Social Security benefits represent a larger share of lifetime earnings for lower-income workers than higher-income workers. This does not mean that a lower-income worker’s monthly benefit amount is higher in nominal dollars than a higher-income worker, but rather that the replacement rate is higher. For a simplified example, a lower-income worker whose final year of income before retirement was $25,000 and who receives $12,000 per year as a Social Security benefit ($500 per month) would have a replacement rate based on the final year of earnings of 48 percent ($12,000 / $25,000). Conversely, a higher-income earner whose final year of earnings was $100,000 and who receives $24,000 per year from Social Security ($2,000 per month) would have a replacement rate of 24 percent ($24,000 / $100,000).

For workers with entire careers in covered employment (employment subject to the Social Security payroll tax), lower lifetime wage earners receive a higher replacement rate than higher lifetime wage earners. But problems arise when workers have earnings from non-covered employment, such as earnings received through state and local governments in careers such as public school teachers, police officers, or firefighters. Though not without fault, the use of replacement rates is useful to illustrate how Social Security is a progressive system. The use of replacement rates, however, is not necessarily a good tool for measuring benefit or program adequacy.

The Social Security Act of 1935 initially exempted state and local government employers from mandatory participation. This exemption was because of constitutional questions as to whether the federal government could impose a payroll tax on state and local governments. Some state and local governments wanted their employees covered by Social Security, while others did not. Presently, all 50 states have agreements with the federal government to allow some state and local employees to be covered by Social Security. However, not all state and local public employees are currently covered.

More than 5 million state and local workers in the United States do not pay Social Security taxes on the earnings from their state and local government employment. This amounts to approximately 28 percent of all state and local government workers. If these workers have an entire career in state and local government that is not covered by Social Security, there is no problem with the WEP or GPO. However, many of these state and local government employees still qualify for some Social Security benefits, either because they have employment history in both covered and non-covered employment, or because they work simultaneously in two or more jobs that include covered and non-covered employment. For example, a professor in the State of Texas or the Commonwealth of Massachusetts (two of the states whose public workers are not necessarily covered under Social Security) will spend the academic year teaching, but may spend summers working for extra income in covered employment outside the university. A professor’s career may also span multiple universities with some of those years spent at a private university, such as Johns Hopkins, which is covered by Social Security. These employees could be affected by the WEP and receive Social Security benefits that are calculated in a way that results in an unfair benefit amount. About 1.6 million Social Security beneficiaries were affected by the WEP as of the end of 2014.

As explained by Brown and Weisbenner (2013):

If Social Security benefits were calculated as a simple linear function of lifetime earnings, it would be possible to calculate the retirement benefit for a worker with partial coverage by simply applying the standard benefit formula only to those earnings covered by Social Security. However, the Social Security benefit formula was explicitly designed to be nonlinear in order to offer a higher replacement rate (i.e., a higher ratio of Social Security benefits to average indexed monthly earnings over one’s lifetime) for individuals with lower earnings. For workers with earnings that are not covered by the Social Security system, using only covered earnings in the standard benefit formula would result in a higher replacement rate on these covered earnings than they would receive if all of their earnings were covered. In order to adjust for this, the Windfall Elimination Provision (WEP) was enacted as part of the 1983 Social Security Amendments. This provision is meant to downward-adjust the Social Security benefits of affected workers in order to eliminate the “windfall” that arises when, for example, an individual with high lifetime earnings (based on both covered and uncovered earnings) would appear as if he or she were a low earner when evaluated solely based on covered earnings.

In sum, while the WEP is intended to ensure that Social Security beneficiaries are treated fairly and that benefits are provided only for years in which people paid into the Social Security system, the result is that the replacement rate for some people with high lifetime combined earnings is higher than those with low lifetime earnings. The WEP mistakenly treats some high-income earners as if they were low-income earners. To see how this might come about, consider the following examples.

Table 1. Example of a Stylized Social Security Benefit Note: For 2016, the first $856 of AIME is multiplied by 90 percent; AIME between $856 and $5,157, by 32 percent; and the remaining AIME, by 15 percent.

Note: For 2016, the first $856 of AIME is multiplied by 90 percent; AIME between $856 and $5,157, by 32 percent; and the remaining AIME, by 15 percent.

Source: Author calculations based on “Benefit Formula Bend Points,” Social Security Administration, accessed March 17, 2016.

Table 1 shows that for workers who turn age 62 in 2016 with 35 years of covered employment and begin receiving Social Security retirement benefits at their full retirement age (FRA), they would receive a monthly benefit of $1,136 if their average annual lifetime earnings were $24,000 (a 57 percent replacement rate); $1,456 if their average annual lifetime earnings were $36,000 (a 49 percent replacement rate); or $2,623 if their average annual lifetime earnings were $100,000 (a 31 percent replacement rate).

Now consider the same workers but who have 20 years of non-covered employment and 15 years of covered employment. Even if combined average annual lifetime earnings is the same, for the years in which they worked in non-covered employment, Social Security treats those years as $0 years for purposes of calculating the average indexed monthly earnings (AIME). For the worker with average adjusted annual income of $24,000 each year, 20 of the 35 years are considered $0. Hence, the resulting average annual earning adjusted for wage growth is $10,285 ($24,000 x 15 / 35). Without the WEP adjustment, here in table 2 are the PIAs and replacement rates for these workers.

Table 2. Example of a Stylized Social Security Benefit with 35 Years Employment: 15 Covered and 20 Non-Covered, No WEP Adjustment Note: For 2016, the first $856 of AIME is multiplied by 90 percent; AIME between $856 and $5,157, by 32 percent; and the remaining AIME, by 15 percent.

Note: For 2016, the first $856 of AIME is multiplied by 90 percent; AIME between $856 and $5,157, by 32 percent; and the remaining AIME, by 15 percent.

Source: Author calculations based on “Benefit Formula Bend Points,” Social Security Administration, accessed March 17, 2016.

As can be seen, the $24,000 per year worker is viewed by Social Security as a lower wage $10,000 per year worker, and the non-WEP adjusted monthly benefit amount would be $771. While nominally less than the $1,136 that the $24,000 per year worker received under a full career of covered employment, the replacement rate for the worker with non-covered employment is now 90 percent as opposed to 57 percent. For the $100,000 per year worker, the replacement rate is now 46 percent as opposed to 31 percent. This worker now receives a “windfall” as the benefit replacement rate is higher than it would be relative to all earnings (covered and non-covered).

To correct for this potential “windfall,” the WEP adjusts the benefit formula. The first bend point is now reduced from 90 percent to as little as 40 percent. Using the same stylized workers as before, but now applying the WEP adjustment, here are the resulting PIAs and replacement rates in table 3.

Table 3. Example of a Stylized Social Security Benefit with 35 Years Employment: 15 Covered and 20 Non-Covered, with WEP Adjustment Note: For 2016, the first $856 of AIME is multiplied by 90 percent; AIME between $856 and $5,157, by 32 percent; and the remaining AIME, by 15 percent.

Note: For 2016, the first $856 of AIME is multiplied by 90 percent; AIME between $856 and $5,157, by 32 percent; and the remaining AIME, by 15 percent.

Source: Author calculations based on “Benefit Formula Bend Points,” Social Security Administration, accessed March 17, 2016.

Now the resulting replacement rates are generally less and more in-line with comparable workers with similar annual average lifetime earnings but with their entire careers in covered employment. The “windfall” has been eliminated. However, the WEP formula is complicated and hard to explain to beneficiaries. Further, the current Social Security Statement provides estimated monthly benefit amounts that are not adjusted for the WEP. While the Statement does include a note to all Statement recipients that they could be subject to the WEP and that their benefits may be reduced, the complexity of the program and the benefit formula result in beneficiaries likely first learning about the WEP only when they first receive a WEP-reduced monthly Social Security benefit check. For people relying on the Social Security Statement as a retirement planning tool, the current non-WEP adjusted information in the Statement could cause people to overestimate their financial readiness for retirement.

It is important to note at this point that eliminating the WEP will only return Social Security to its pre-WEP state and reinstate a windfall for those with both covered and non-covered employment. Hence, repeal is not advised. However, a “proportional” or prorated formula would improve fairness of the WEP while maintaining fairness and equal treatment. It would also be much easier for SSA to administer and explain to beneficiaries.

Unintended Consequences

Not only does the current WEP unequally treat beneficiaries with similar average annual lifetime earnings differently due to covered and non-covered employment, but the current WEP policy provides a perverse incentive for those in non-covered employment to seek secondary jobs in covered employment.

The Social Security progressive benefit formula is intended to provide workers who spend their careers in low paying jobs with a monthly benefit amount that replaces a higher proportion of their earnings than the benefit that is provided to workers with higher lifetime earnings. However, as I’ve discussed in this testimony, the benefit formula does not differentiate between those who worked in low-paying jobs throughout their careers and other workers who appear to be lower-income workers solely because they worked many years in jobs not covered by Social Security but had some jobs that were in covered employment.

This could provide a perverse incentive among workers in non-covered employment to seek some additional outside employment in jobs that are covered by Social Security for the sole purpose of gaming the Social Security system. Doing so would provide these workers with a Social Security benefit check upon retirement, in addition to the pension check earned via non-covered employment, with a higher replacement rate than would be due to a worker with only covered employment but with a similar annual lifetime income.

Policy Recommendations and Conclusion

When the current formula for the WEP was established as part of the 1983 Amendments to the Social Security Act, the Social Security Administration lacked the administrative records to accurately capture non-covered employment history. Hence, a proportional or prorated WEP wasn’t possible. However, as of January 2017, SSA will have 35 years of employment history including both covered and non-covered employment. Thus, we now have both the information and the tools necessary to reform the WEP and move to a prorated formula. President Obama’s FY 2017 Budget contains just such a proposal, and a similar bill has been introduced in the House by Ways and Means Committee Chairman Kevin Brady (R-TX) and Rep. Richard Neal (D-MA). These proposals are very similar, and both would slightly improve the solvency of the program, though the president’s proposal also addresses the GPO and begins in 2027, whereas the House bill would begin applying the new benefit formula in 2017.

To see how a “proportional” or prorated benefit formula would look, consider table 4 below which includes the same stylized workers used in the previous illustrations.

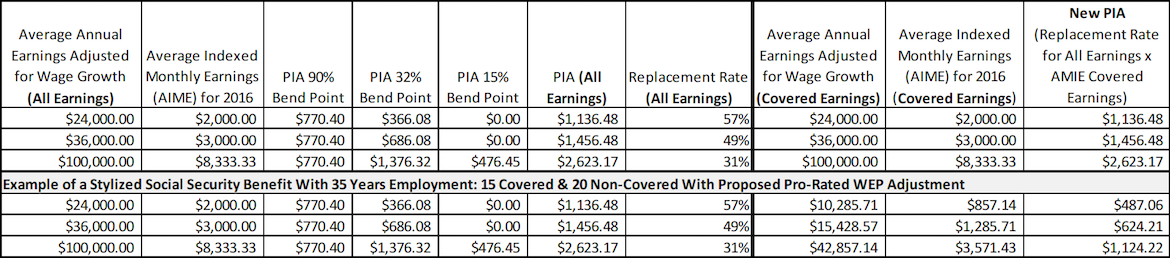

Table 4. Example of a Stylized Social Security Benefit with 35 Years All Covered Employment with Proposed Prorated WEP Adjustment Note: For 2016, the first $856 of AIME is multiplied by 90 percent; AIME between $856 and $5,157, by 32 percent; and the remaining AIME, by 15 percent.

Note: For 2016, the first $856 of AIME is multiplied by 90 percent; AIME between $856 and $5,157, by 32 percent; and the remaining AIME, by 15 percent.

Source: Author calculations based on “Benefit Formula Bend Points,” Social Security Administration, accessed March 17, 2016.

Under the proposed new formula, the AIME is computed as it is currently but for all earnings, covered and non-covered combined. The resulting PIA is then determined. The replacement rate of PIA divided by AIME is derived. Next, an AIME is computed for just the covered earnings. At this point the replacement rate is multiplied by the AIME for covered earnings only, resulting in the effective PIA.

For workers whose entire careers are in covered earnings, the resulting PIA is the same. However, for those with non-covered earnings, but with similar combined average annual lifetime earnings, now their covered earnings receive the same replacement rate as those whose entire careers were spent in covered employment. In other words, the replacement rate on covered earnings is now the same and treats both workers with identical lifetime earnings history equally, thus restoring some fairness to the system while still maintaining the original intent of the WEP to avoid a “windfall” to those with non-covered earnings.

The simplicity and fairness of the proposed new formula is that it would apply to all workers—those with both covered earnings only and those with both covered and non-covered earnings—making it easy for SSA to administer and for beneficiaries to better plan for retirement. Additionally, under the proposed new formula, the Social Security Statement could provide accurate monthly benefit amounts to better enable people to plan for their financial security in retirement.

It’s not often that a Social Security reform proposal comes forward that has bipartisan support and support from both Congress and the president. The original intent of the WEP and GPO still applies today; however, we now have the opportunity to get the formula right for the improvement of the Social Security program and its beneficiaries.

Thank you again for your time and this opportunity to testify today. I look forward to your questions.