- | Public Interest Comments Public Interest Comments

- |

Regulatory Capital Rule: Capital Simplification for Qualifying Community Banking Organizations

Thank you for the chance to comment on the “Regulatory Capital Rule: Capital Simplification for Qualifying Community Banking Organizations” notice of proposed rulemaking pursuant to section 201 of the Economic Growth, Regulatory Relief, and Consumer Protection Act (EGRRCPA). I am an economist at the Mercatus Center, a university-based research center at George Mason University, dedicated to advancing knowledge relevant to current policy debates. Staff at the Mercatus Center conduct independent analyses of agencies’ rules and proposals from the perspective of the public interest. My comments do not reflect the views of any affected party, but they do reflect my general concerns about the burden and unintended consequences of financial regulation, as well as my research interests, which identify effective policies to mitigate the risk of financial crises. Before I address specific questions raised in the notice of proposed rulemaking, I will begin with some general comments.

General Comments

Section 201 of EGRRCPA has called for replacing the existing complex, risk-based capital adequacy framework for community banks with a simple, tangible, equity-to-total-asset leverage ratio equal to 9 percent. The proposal has merits in that it would greatly simplify the process of determining capital adequacy for banks without weakening capital requirements. Indeed, James R. Barth and I estimate that by 2017, US Basel III capital adequacy regulations on average had generated over 157,000 more words than other parts of the US Code of Federal Regulations (CFR) that pertain to the Office of the Comptroller of the Currency and over 103,000 words more than other parts of the CFR that pertain to the Federal Deposit Insurance Corporation.

In another study, Barth and I examine whether increasing the leverage ratio from 4 to 15 percent has benefits, in terms of lowering the adverse effects of crises on US GDP, that exceed the costs that might arise from lower capital formation and lower GDP. We find that the benefits generally exceed the costs; in our baseline case, which makes fairly conservative assumptions about benefits but also assumes the highest costs, an optimal leverage ratio of 19 percent equates the marginal benefits and costs.

With that in mind, since subsection 201(b)(1) of EGRRCPA calls for agencies to “develop a Community Bank Leverage Ratio [CBLR] of not less than 8 percent and not more than 10 percent for qualifying community banks,” I would like to suggest that moving to 10 percent would have merits. One reason to justify increasing the leverage ratio to 10 percent rather than 9 percent lies with a key parameter used to calculate the cost of raising the leverage ratio: namely, a banking entity’s return on equity. The baseline 19 percent optimal leverage ratio discussed earlier assumes, among other things, that the rate of return on equity equals 12 percent. Using bank holding company (BHC)–level data, we also find that larger banking entities on average tend to have higher return on equity estimates than smaller banking entities. Therefore, since the CBLR would apply to smaller institutions (which tend to have lower rates of return on equity) and since using a lower rate of return on equity generates lower costs of increasing the leverage ratio relative to our baseline estimates, it seems reasonable to conclude that community banks could meet the upper-bound threshold proposed by subsection 201(b)(1) of EGRRCPA.

For instance, based on quarterly Schedule-RC-bank-level call report data from Q1 2006 to Q4 2016, the median return on equity equaled about 8 percent regardless of whether we defined community banks as those in holding companies with less than $10 billion in total assets or used the Federal Deposit Insurance Corporation’s definition of a community bank. That means estimates of the optimal CBLR based on the methodology we apply could well exceed the 10 percent minimum that is the upper bound of the range suggested under section 201 of EGRRCPA.

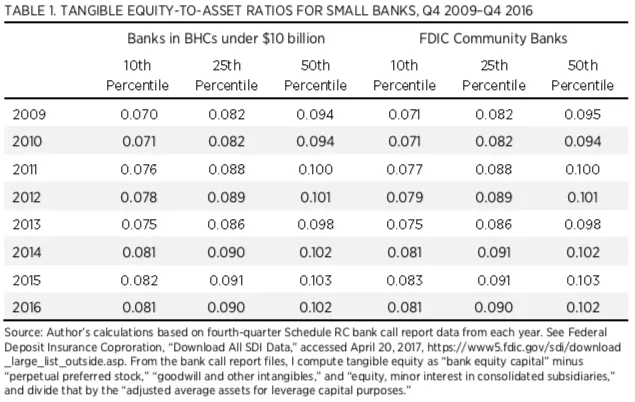

Moreover, table 1 shows that the tangible equity-to-asset ratio for the 10th percentile equaled 8 percent, for the 25th percentile it was 9 percent, and for the 50th percentile of small banks it was 10 percent by Q4 2016, whether I measure small banks as those with parent BHCs that have under $10 billion in total assets or whether I use the FDIC’s measure of a community bank. That means 75 percent of all banks are roughly operating at the minimum suggested by the notice of proposed rulemaking, while about half of the banks already operate at the 10 percent threshold, which is the upper bound of the range stated in subsection 201(b)(1) of EGRRCPA. So overall, many banks already satisfy the proposed regulation. I will now respond to questions 2, 4, 8, and 9 before concluding.

Response to Question 2

The agencies have proposed defining a qualifying community banking organization according to the following criteria:

- Total consolidated assets of less than $10 billion

Total off-balance-sheet exposures (excluding derivatives other than credit derivatives and unconditionally cancelable commitments) of 25 percent or less of total consolidated assets

Total trading assets and trading liabilities of 5 percent or less of total consolidated assets

Mortgage servicing assets of 25 percent or less of CBLR tangible equity

- Temporary difference deferred tax assets of 25 percent or less of CBLR tangible equity

The proposal could be justified in that it suggests differentiating capital adequacy guidelines according to a bank’s business model, whereby banks with seemingly riskier business models face the more complex capital adequacy guidelines. However, this proposal rests on the assumption that the more complex capital adequacy guidelines work more effectively than simpler guidelines. Moreover, the use of additional criteria beyond less than $10 billion in total consolidated assets would likely reduce the number of banks subject to the CBLR. Based on the research concerning the leverage ratio discussed above, applying the CBLR (equal to 10 percent) to any banking entity with under $10 billion in total assets would have benefits that outweigh the costs.

Response to Question 4

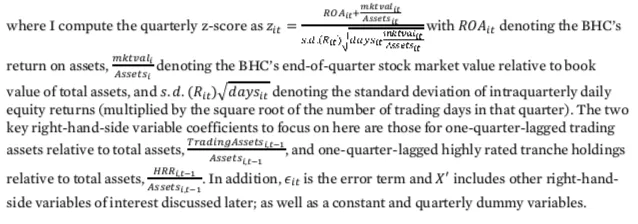

The agencies have proposed including a trading activity criterion to define a qualifying community banking organization. However, I would suggest excluding this criterion from the definition. I suggest doing so because a common postcrisis narrative holds that trading assets, generally, posed a system-wide threat to the financial system; yet building on recently published research, I can show such claims may be overstated. In particular, I can show that instead of trading assets as a whole, BHCs that reported a greater fraction of their portfolio as highly rated, private-label securitization tranches, either in their trading account or elsewhere on the balance sheet, ceteris paribus, experienced declines in the natural log of their z-score, a measure of corporate default risk.

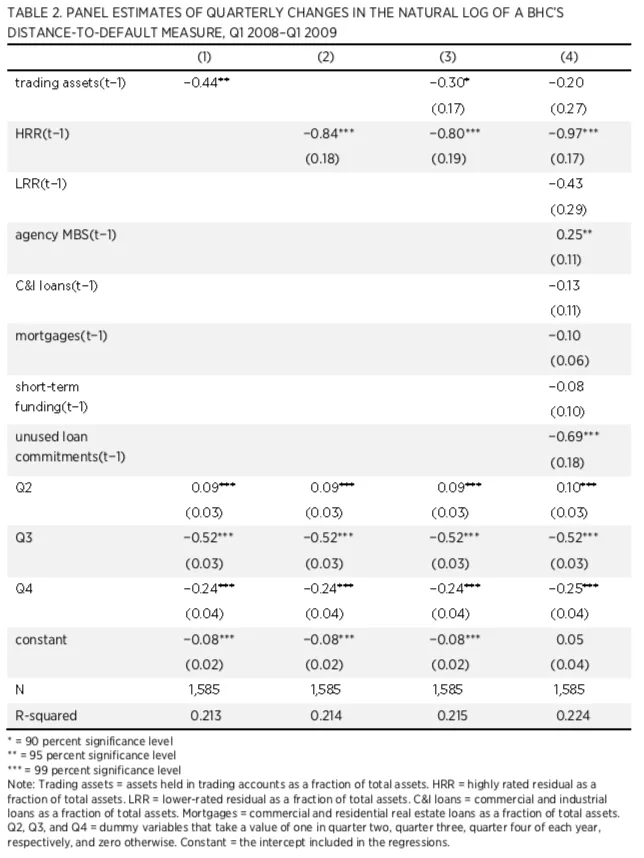

To see this, table 2 reports ordinary least squares (OLS) regression estimates of the association between quarterly changes in the natural log of a BHC’s z-score and various variables that might be associated with bank distress for an unbalanced panel of 348 BHCs. The equation used is

Column (1) reports coefficients from a simple OLS panel regression of changes in the natural log of the z-score against one-quarter-lagged trading assets as a share of total assets, while column (2) reports the same regression with the one-quarter-lagged estimates of the highly rated, private- label securitization tranches as a share of total assets replacing the trading asset share. If either the trading asset share or the highly rated, private-label securitization share is associated with increases in risk, then one would expect to find a negative coefficient for these variables. Column (3) reports coefficients from a regression that includes both variables at the same time. Lastly, column (4) reports coefficients from a regression that adds to the regression summarized in column (3) the following variables:

the one-quarter-lagged share of lower-rated securities; intuitively, lower-rated securities might be riskier than the higher-rated ones, and therefore, one might expect to find a more negative association with the changes in the natural log of the z-score than for the highly rated tranches

the one-quarter-lagged share of agency mortgage-backed securities (MBSs), originated by Fannie Mae and Freddie Mac; intuitively, if agency MBSs exhibit poor performance, they might be negatively associated with changes in the natural log of the z-score, but if the implicit government guarantee backing these securities were in effect, then they might be positively associated with changes in the natural log of the z-score

the one-quarter-lagged share of assets in commercial and industrial loans; as studies have found a negative association with BHC performance, intuitively one would expect a negative association with changes in the natural log of the z-score

the one-quarter-lagged share of assets in mortgages; as studies have found a negative association with BHC performance, intuitively one would expect a negative association with changes in the natural log of the z-score

one-quarter-lagged short-term wholesale funding as a fraction of total assets; intuitively, if greater short-term funding might be associated with greater-run risk, one would expect a negative association with changes in the natural log of the z-score

one-quarter-lagged unused loan commitments to support commercial and residential real estate lending as a fraction of total assets; as studies have found a negative association with bank performance, intuitively one would expect a negative association with changes in the natural log of the z-score

quarterly time dummy variables

Key Findings

The results in table 2 show the following:

- The one-quarter-lagged trading share has a negative association with changes in the natural log of the z-score, but the magnitude of the coefficient declines and the variability of the coefficient estimate rises as more variables are added; this finding suggests that since the crisis, trading assets may have been misclassified as a source of system-wide risk.

The one-quarter-lagged, highly rated, private-label tranche share has a negative association with changes in the natural log of the z-score and the magnitude of the coefficient is consistent across all three specifications, while the variability of the coefficient estimates are small; this finding corroborates other studies that show that some securitized assets were the source of system-wide risk.

The one-quarter-lagged share of lower-rated securities has a negative association with changes in the natural log of the z-score, but the magnitude of the coefficient is about half the size of that for the highly-rated tranche variable, while the coefficient estimates are more variable; this finding suggests that the highly rated, private-label tranches were in relative terms more damaging than the lower-rated tranches.

The one-quarter-lagged share of agency MBSs has a positive association with changes in the natural log of the z-score; this finding suggests that holdings of agency MBSs, most likely because of the associated government guarantees, kept BHCs away from default.

The one-quarter-lagged share of unused loan commitments has a negative association with changes in the natural log of the z-score; this finding is consistent with what previous studies had found.

The coefficient estimates for the other variables included in the specifications, aside from those for the quarter dummy variables, are relatively small in magnitude.

Response to Question 8

The agencies have proposed that advanced approaches banking organizations be excluded from the CBLR framework. Based on research discussed earlier concerning the leverage ratio, I would suggest that applying at least a 10 percent CBLR to advanced approaches banking entities would have benefits that outweigh the costs.

Response to Question 9

The agencies have asked about the advantages and disadvantages of a CBLR that closely aligns with the applicable reporting instructions to Schedules RC of the call report and HC of the Form FR Y-9C measure of equity. One view in the literature suggests that capital adequacy at the bank subsidiary level should remain the focus of efforts to regulate. If that were the approach taken by regulators, then it may matter less how the concepts in Schedule RC of the call report and Schedule HC of Form FR Y-9C link together. However, to the extent that the “source of strength” remains the approach taken by regulators, then it seems that bank subsidiary and BHC concepts should be linked as closely as possible. Otherwise, this may pose a challenge for determining capital adequacy, in a manner similar to how risk-based capital requirements have created ambiguity about capital adequacy such that investors turn instead to measures like tangible common equity, or market values of equity, when available.

Conclusion

Overall, I commend the regulators for their efforts to put forth a proposal to simplify capital adequacy standards. Simpler, higher measures of capital adequacy that investors can understand and verify will work effectively toward eliminating the “too big to fail” problem that has generated considerable debate. They can also work effectively toward eliminating the “too small to survive” problem that has historically posed a challenge to the broader economy in the United States.

Additional details

Agency: Department of the Treasury, Office of the Comptroller of the Currency

Comment Period Opens: February 8, 2019

Comment Period Closes: April 9, 2019

Comment Submitted: February 18, 2019

Docket ID: OCC-2018-0040

RIN: 1557-AE59

Agency: Federal Reserve System

Comment Period Opens: February 8, 2019

Comment Period Closes: April 9, 2019

Comment Submitted: February 18, 2019

Docket No. R-1638

RIN: 7100-AF29

Agency: Federal Deposit Insurance Corporation

Comment Period Opens: February 8, 2019

Comment Period Closes: April 9, 2019

Comment Submitted: February 18, 2019

RIN: 3064-AE91