- | Financial Markets Financial Markets

- | Policy Briefs Policy Briefs

- |

A Suggested Mortgage Amortization Structure: Fixed Amortization, Adjustable Principal

The 30-year fixed-rate mortgage provides borrowers with a valuable benefit: certainty in cash flow. But this certainty comes at quite a cost. I propose a mortgage amortization product that would promise relatively stable payments from borrowers while ridding lenders and investors of the problematic costs of fixed-rate mortgages. This mortgage product would have a floating, or short-term, rate, but some of the payment would be made (or discounted) in kind (in other words, by adjusting the principal of the loan). In this policy brief, I refer to this product as the fixed-amortization, adjustable-principal (FA/AP) mortgage.

A significant problem posed by real estate lending is interest rate risk. Historically, rates have ranged from less than 3 percent to more than 15 percent. Most interest rate risk comes from inflation, which is volatile. Mortgage rates with the expected inflation premium deducted have tended to range between about 1 percent and 5 percent.

Lenders can avoid interest rate risk by issuing adjustable-rate mortgages (ARMs), but ARMs expose borrowers to cash flow risks. If a borrower takes out a 4 percent mortgage and a Federal Reserve policy shift or a strong economic recovery pushes rates up to 5 percent or more, the borrower faces a double-digit percentage increase in mortgage expenses. Such an increase is not manageable in an expense that is regularly a quarter of household spending and that frequently is a much greater portion of household spending in expensive housing markets. Funding home purchases with ARMs, therefore, can be destabilizing.

Cash flow stability for borrowers, which fixed-rate mortgages provide, comes at the cost of interest rate risk for lenders. If market interest rates go up, the value of existing mortgages to banks goes down, because those mortgages are now receiving less interest income than new mortgages. With most debt instruments, such as Treasury bonds, this potential decline in value is offset by the potential decline in interest rates, in which case the market value of existing bonds rises. As a result, although the eventual value of a bond is unknown, at least the positive and negative potentials are balanced.

But mortgages in the United States can usually be prepaid without a penalty, so borrowers tend to refinance when rates go down. That means that lenders cannot easily hedge risks or match the maturity dates of their assets and liabilities, because nobody knows exactly how long mortgages will be on the books—the amount of time depends on borrower reactions to future interest rates. This uncertainty makes mortgage lending difficult, and it adds yet another premium to mortgage rates, because lenders require compensation for such problematic risks.

Frequently, the benefits of the government-sponsored mortgage agencies Fannie Mae and Freddie Mac are described in terms of how much they bring down interest rates for mortgage borrowers—they were able to decrease rates by about 0.25 percent before being taken into conservatorship. But conventional mortgage lending in the United States usually entails trading cash flow certainty for a much higher interest rate. For example, from 1984 to 2015, 30-year fixed-rate mortgage rates averaged 1.7 percentage points more than 1-year ARM rates. This premium is much higher than the approximately 0.25 percent savings the government-sponsored mortgage agencies provide.

This is a high price to pay for cash flow stability, and it is not necessary. Lenders and borrowers are concerned with different risks, and both sides should be able to take on the risks that they find manageable. The unmanageable risk for the borrower is cash flow. The unmanageable risk for the lender is valuation. One way to reduce both risks would be an adjustable 30-year amortized mortgage with a fixed payment rate and a fixed amortization. Such a mortgage could be done simply and can be understood with basic arithmetic. The mortgage would be pegged to an adjustable short-term interest rate. Supposing a one-year rate with an annual reset provides an intuitive way to think about it. In the case of a mortgage with a fixed 5 percent payment rate, for example, the borrower would always make payments as if the mortgage were a 5 percent fixed-rate mortgage. If the one-year floating rate in any given year were 6 percent, then the extra 1 percent of interest would be paid in kind by simply increasing the principal amount of the mortgage by 1 percent. In that case, the monthly payments would also increase by 1 percent to cover the now larger principal, even though the mortgage would still have a 5 percent fixed payment rate. If the one-year rate were 4 percent, then the principal would be reduced by 1 percent, and current and future payments would also be 1 percent lower. This would allow the lender to avoid costly interest rate risk while the borrower accepts changes in monthly payments that are much less volatile than they would be on a traditional ARM.

The Downsides of Fixed-Rate Mortgages

Under the status quo, borrowers pay fixed rates (with the 1.7 percent average premium) and may prepay their loans, and in exchange they face a largely win-win scenario: if inflation rises after they initiate their mortgage, they receive a windfall because their home experiences an inflationary rise in value while their mortgage remains fixed; if inflation declines after they initiate their mortgage, they periodically refinance, reducing their mortgage payments.

For example, borrowers who bought homes with long-term fixed-rate mortgages in the 1960s and early 1970s reaped huge gains as their home’s value and their income rose with inflation and the real cost of their mortgage payments dwindled year after year. At the same time, lenders and the government-sponsored mortgage agencies experienced losses. All along the way, borrowers have paid a premium ranging historically from about 0.5 percent to about 3.0 percent for fixed-rate mortgages. Although they secured these mortgages to provide cash flow stability, they were really paying a premium for asymmetrical exposure to potential windfall. The same potential exists for current home buyers, who can borrow at historically low rates. If inflation rises again, they can also reap a windfall.

This asymmetry is inequitable and destabilizing. It relies on borrowers’ ability to qualify for refinancing. But what if either their personal financial condition or mortgage market conditions deteriorate? Then, as in the years immediately after 2007, the most vulnerable households are hit with a dislocation where they are stuck with mortgages that have above-market interest rates.

This is not an optimal situation. Few home buyers purchase homes for the purpose of speculating on an inflation-induced windfall. If households could pay separate premiums for stable cash flows and for exposure to this speculative windfall, most would be willing to pay for stable cash flows, but few would be interested in paying for that speculation—certainly not a nearly 2 percent premium.

Why must these two benefits be bundled together? Borrowers could otherwise get relatively stable cash flows practically with no cost, and banks would happily give up that premium to avoid the risk of being on the losing side of that asymmetrical windfall.

Fixed-rate mortgages are nevertheless somewhat useful in that the real value of the mortgage payment declines over time because of inflation. If inflation averages 2 percent over the life of a 30-year fixed-rate mortgage, the last month’s payment will be worth only 55 percent of the initial month’s payment in real terms. Because individual incomes tend to rise slightly faster than the rate of inflation, mortgage payments as a percentage of household income usually decline even more.

Setting up a mortgage this way provides a sort of buffer underneath future household income. By committing to the mortgage, borrowers naturally defer consumption and increase real disposable income after mortgage costs over time. But this process does not reflect any balance of household needs if the decline in the real value of mortgage payments is a result of inflation rates over time. Why should the rate of household saving into home equity be tethered to random changes in inflation rates?

Furthermore, this setup places a lot of cash flow pressure on new borrowers because the costs are all loaded up front. For instance, compare the rates for the average 1-year fixed-rate mortgage and the average 30-year fixed-rate mortgage over the past 30 years—about 4.8 percent and 6.5 percent respectively. If a mortgage at the average 1-year rate, amortized over 30 years, takes 20 percent of household income, the fixed-rate mortgage takes 24 percent of household income. That is 4 percent of household income paid for a speculative option on inflation.

To accommodate their future needs, young families often prefer to purchase a home that is larger than they need in the present. However, the previously mentioned front-loading of mortgage expenses may prevent families from purchasing such a home. Furthermore, even if they are able to purchase such a home, they must pay more during the initial years of the mortgage, when their lower income relative to mortgage payments makes them least financially prepared to take on the risks attendant to borrowing (default, negative equity, etc.). Deferring larger mortgage payments to later periods, which FA/AP mortgages would do in some cases, would benefit these families by allowing them to purchase the house they prefer or, if they nevertheless decide to purchase a smaller house, by reducing the financial burden of the mortgage during the relatively risky initial years. In the former case, the burdens and risks of the mortgage would be no greater at origination (when they are the most taxing on borrowers) than they are with fixed-rate mortgages. In the latter case, some of the financial burden of the mortgage would be transferred to less risky points in the future, and the small increase in risk in later years owing to higher payments would generally come when families are financially more secure or when they have built some home equity.

Deferring costs is especially important for borrowers in cities where homes are expensive. Because fixed-rate mortgages have the expensive, embedded option of tactically refinancing with declining interest rates while being protected against higher interest rates, mortgages with riskier terms are more competitive in those markets. Borrowers are drawn to mortgages with riskier terms such as adjustable rates, balloon payments, and incentives to refinance frequently. Lenders do not have as much interest rate risk on those products, so they can offer those products at lower rates.

A fixed-amortization mortgage with adjustable principal would avoid these problems. It would eliminate the extra costs of fixed-rate mortgages. It would also lower the risks associated with making mortgages. Banks and investors would require smaller profits to fund those mortgages, because they would not be carrying the duration risk of fixed-rate mortgages. This would make less risky loan terms more competitive.

How Would the FA/AP Mortgage Work?

The mechanics of an FA/AP mortgage would be simple. In the case of a mortgage with annual rate resets, at each reset date the interest rate would be reset at the current one-year market mortgage rate. With a 1-year mortgage interest rate of 5 percent at the start of a $100,000 mortgage, an FA/AP mortgage with a 30-year amortization schedule would require monthly payments of $536.83. At the end of the year, the principal would be down to $98,525.

At that point, the interest rate would be reset to the new rate. The difference between the new interest rate and the payment rate would be added or subtracted to the principal, not to the payment rate. If the interest rate were 6 percent for the second year of the mortgage, the principal would be adjusted up by 1 percent, to $99,510 in the example, and the payment amount would also change by 1 percent, to $542. If the interest rate during the second year were 4 percent, the principal would be adjusted down by 1 percent, to $97,540, and the new payment amount would be $531. These payment amounts are the amounts required to continue the original 30-year amortization schedule, so the final maturity date of the mortgage would not change. Payments would adjust slightly up or down with changing interest rates, which correlate strongly with incomes and home prices. On average, though, the real payment level would decline over time, similarly to other mortgages.

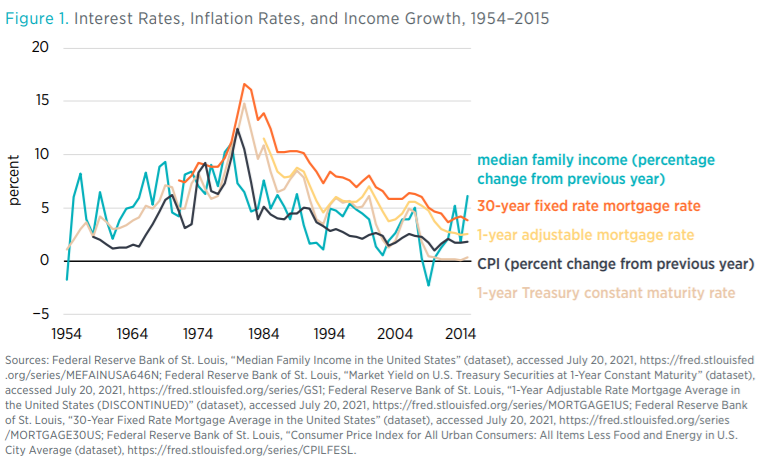

As shown in figure 1, interest rates, inflation rates, and rates of change in incomes tend to rise and fall together. Over time, a mortgage with payments that adjust slightly with short-term interest rates actually aligns more soundly with incomes and home values.

The real value of the mortgage payments over time still gradually falls in all cases. Adjustment of the principal instead of the payment rate would ensure that the changes in payments with an FA/AP mortgage would be very small and manageable compared to those with an ARM. For mortgage holders that have taxes and insurance paid through their mortgage servicer, the annual change in payments would be similar to the minor shifts that they currently see in the insurance and tax portion of their monthly payments.

With an FA/AP mortgage, the payment rate would be arbitrary and would not need to match the current market interest rate. This would be a primary advantage of the FA/AP mortgage. Much of the effort in constructing and selling mortgage products today is spent on creating an affordable payment for the borrower, given current market rates. Separating the payment rate from the interest rate removes that constraint, and the payment rate can be set to reflect other risks and constraints that are relevant to the borrower, the lender, and the property.

In the examples that follow, I use a payment rate of 5 percent, which is similar to the average adjustable rate of the past 30 years. Over that time, with a 5 percent payment rate, payments remain about the same on the average mortgage. Unless there is a new shift in Federal Reserve policy that causes inflation to run above target, one-year mortgage rates should run 5 percent or less, on average, for the foreseeable future. So today a 5 percent payment rate is expected to lead to declining payments over time.

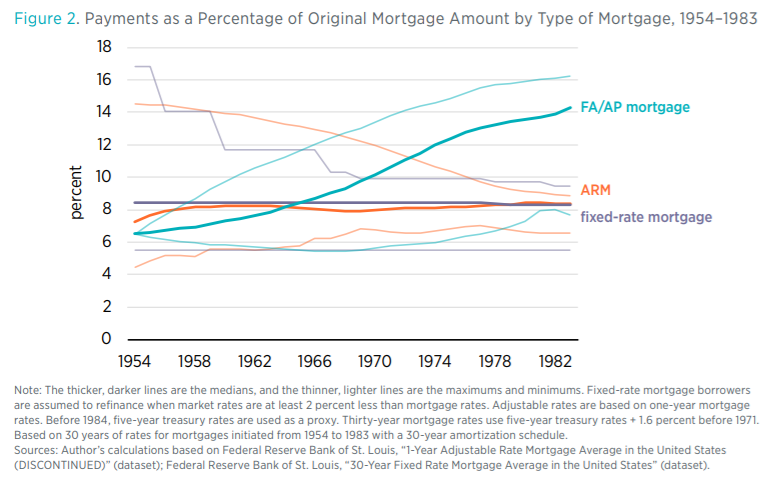

The following figures compare the expected median, minimum, and maximum measures of an ARM, a 30-year fixed-rate mortgage, and a (hypothetical) FA/AP mortgage initiated from 1954 to 1983. Figure 2 compares the nominal payments over time relative to the original mortgage amount. One can see the upward drift in payments, in nominal terms, in the FA/AP mortgage. This may be worrisome because the drift seems unbounded.

However, the FA/AP mortgage would have provided much more stability in its early years. Also, for the 1954 to 1983 period, interest rates were rising over the life of the mortgage and were well above 5 percent because of inflation. This is the sort of environment where FA/AP mortgages would help stabilize real payments over time by raising the payment level for the years near maturity. But for mortgages originated since 1983 (not shown in figure 2), interest rates have been declining, and they have generally been less than 5 percent in recent years, meaning that payments for the hypothetical FA/AP borrower would have been declining as well, and those borrowers would have built home equity more quickly.

To provide a sense of how mortgage payments evolved over time in inflation-adjusted terms, figure 3 compares mortgage payments as a percentage of household income over 30 years of amortization. In all years, the median-income family could purchase the median-price new home for between 19 percent and 23 percent of their income with an FA/AP mortgage. That percentage generally declined within a reasonable band, with median payments over the final 15 years typically remaining at about 10 percent of household income. At no time would payments for FA/AP mortgages relative to household income in the out years have risen above the range of payments required at the start.

Payments as a percentage of household income for both ARMs and fixed-rate mortgages generally fell to lower levels in their final years, but in exchange for this they required a much more extreme range of cash outflows in the early years. In terms of payments, although the FA/AP arrangement appears more risky in nominal terms, it is more stable in real terms.

Advantages of the FA/AP Mortgage for Financial Markets

FA/AP mortgages would have many advantages for financial markets. They would solve the problem in banking of the mismatch between assets and liabilities. Bank liabilities are mostly in the form of deposits, which generally have short durations (they can be withdrawn immediately or have short-term maturities). But mortgages have long and unpredictable maturities. This is the source of much banking risk. The book value of those mortgages, which are assets to the bank, can fluctuate with interest rates, and banks can be hit with balance sheet shocks when interest rates change. FA/AP mortgages, however, would act like they have short-term maturities. Their interest income would fluctuate parallel to the interest banks pay on deposits, largely mitigating the main risk that banks face. The fact that banks’ remuneration for changing interest rates would come in the form of adjusted book values instead of as cash payments is of little concern. Book value is what is important to banks. This change might also encourage banks to hold mortgages rather than securitize them, because they would be able to hold them without the duration risk and interest rate risk that current fixed-rate mortgages carry.

The prepayment problem would go away as well. Mortgage rates, on average, would be quite a bit lower, because they would be short-term rates instead of long-term rates, meaning that the profits required by banks and investors would be lower.

A key problem with the use of debt is that it tends to be nominally sticky. This means that when there are economic disruptions, inflation tends to decline, and borrower incomes do not rise as fast as expected, making it harder to pay off loans. Defaults and operational dislocations follow. With all mortgage products, there are expected cash payments, and when those deviate from expectations, defaults occur. But the principal of FA/AP mortgages would change along with changing inflation rates—in other words, the debt would be less nominally sticky. In some ways, this type of loan is just a subset of option ARMs, but with more stability in terms. These products are not unheard of. France, for instance, has several mortgage types with flexible payments and principal. Economist Glenn Pederson and coauthors have studied mortgages where the amortization schedule is adjusted instead of the payment (as opposed to FA/AP mortgages, which would hold the maturity date constant and change the payment). FA/AP mortgages might be made even safer if, as with the mortgages studied by Pederson and coauthors, they were to include some limited options for adjusting the maturity instead of the payment amount. For example, an FA/AP mortgage could be set to amortize over 25 years. Thus, if market rates were above the payment rate, instead of increasing the next year’s payments when the principal was adjusted up, the amortization could be adjusted out—within some limit; then, if the amortization period were to reach, say, 30 years, the amortization period could be fixed, and any future adjustments would be applied to the payment. The advantage of this is that payments would be fixed during the early years when the mortgage payments are highest in real terms. The potential for rising payments would be only in the later years when the mortgage payments would be smaller, in real terms. This would put a cap on the amortization while still allowing for the other advantages of the mortgage. But with a high-enough fixed payment rate, payments should rarely grow at a faster pace than incomes, even with a fixed amortization period.

The amortization schedule could also be changed when the payment rate is higher than the market interest rate. Instead of lowering future payments, borrowers could choose to shorten their amortization.

Finally, sources of home buying demand would be clearer. FA/AP mortgages would obviate the question of whether the demand for housing is changing because of changing household needs or changing intrinsic values or because of arbitrary inflation-related interest rate changes. FA/AP mortgages would cyclically smooth out demand because the payment rate could be the same regardless of whether mortgage rates were 4 percent or 7 percent.

When market rates are lower than the payment rate, other types of mortgages may be better at allowing borrowers to lower their initial payments. But fixed-rate mortgages still come with a premium, and ARMs come with greater interest rate risk. So at times when FA/AP mortgage borrowers would have a higher initial payment than that of fixed-rate mortgage borrowers, their principal and payments would decline each year. Meanwhile, ARMs avoid the fixed-rate premium, but potential low-rate environments might favor FA/AP mortgages, which should lower ex ante default risk. Lenders might also require lower maximum debt-to-income ratios for ARMs than they might for FA/AP mortgages in similar conditions because potential future changes in payments on FA/AP mortgages would be smaller.

Advantages of FA/AP Mortgages for Home Buyers

FA/AP mortgages would also have advantages for home buyers. The FA/AP mortgage would mimic a real security that grows in value with inflation, such as the house. (FA/AP mortgages would be structured sort of like Treasury Inflation-Protected Securities [TIPSs], except that FA/AP mortgages would be adjusted for both changing inflation and changing real rates.) It would allow the borrower to transfer the unrealized inflationary gains in the house to the lender in the form of unrealized interest expenses (an increase in principal that is paid through future payments). This kind of transfer would do a better job of matching liabilities (the mortgage) and assets (the home) for the borrower. Plus, the level of payment could easily be set greater than the long-term range of real interest rates. For instance, if the one-year mortgage rate were 5 percent, that rate might include a 3 percent real interest rate plus a 2 percent inflation premium because inflation would be expected to reduce the value of dollars by 2 percent over the course of the year. If the payment rate were also 5 percent, it would already be covering a 2 percent inflation expectation, so a mortgage set up in that context would have principal that, in terms of purchasing power, declines in value 2 percent over the year. If inflation were to rise to 4 percent, so that the mortgage rate is 7 percent the following year, then the principal would be increased by 2 percent. But that would still be 2 percent less than the inflation rate, and the principal would still have declined by 2 percent in real terms.

The FA/AP mortgage would also remove arbitrary cyclical factors from the decision to purchase a home. A person’s willingness and ability to purchase a home depends largely on current interest rates. Most of these rate changes are related to inflation expectations and cyclical fluctuations, which have little to do with the value of home ownership. The fixed payment structure of the FA/AP mortgage would create a steadier context for the owner’s or renter’s decision in terms that matter to households—cash flow. Fixed amortization and adjustable principal would not make a mortgage a perfect match for the real assets it is used to buy, but they would bring the mortgage much closer to being one.

There would be little need for tactical refinancing, which would save administrative costs in real estate financing. Mortgage issuance would generally be required only for purchases and cash-out refinancing. Using FA/AP mortgages should cut down on the number of mortgage originations because refinancing to get a lower interest rate would be unnecessary.

The FA/AP mortgage would reduce the initial cash demands compared to conventional fixed-rate mortgages, giving new buyers more financial flexibility to purchase a home meant for long-term residence without creating undue financial stress in the early years of the mortgage.

The FA/AP mortgage is conceptually simple and would be easy to compute. With annual resets, a market rate 1 percent less than the payment rate will lower future payments by 1 percent, for example. No complicated formulas are required to make such a basic inference.

There are some problems that FA/AP mortgages cannot solve, but even in these cases they may have benefits. The main time when FA/AP mortgages would have potentially added a new type of risk was the early 1980s, when interest rates rose significantly above inflation for several years. In that time, FA/AP mortgage principal would have grown at a rate faster than typical incomes or home prices. But other types of mortgages had problems during that time that FA/AP mortgages would have avoided. Fixed-rate mortgages had very high payments, and ARMs had payments that were very high and could fluctuate each year. In addition, the highly volatile interest rates on fixed-rate debt created chaos among lenders trying to manage interest rate risk. Even in that worst-case scenario, FA/AP mortgages would have created less systemic risk than the other forms of mortgages.

FA/AP mortgages cannot solve the problems of sharply falling home prices leading to large-scale defaults or of housing policies leading to high rents and high, volatile prices. They could not have directly mitigated the problems of late 2007 and 2008 as those problems developed, for example. But even in that scenario, FA/AP mortgages would have been stabilizing. The problem in late 2007 was, as much as anything, a liquidity problem. Some homeowners who had been able to get mortgages suddenly found themselves rejected by underwriters for a number of reasons. Because conventional mortgages front-load cash outflows, high home prices had driven many buyers to mortgages with risky terms as the only way to push monthly payments down to an affordable level. Probably the aspect of those mortgages that ended up being most disruptive was their use of irregular terms that presupposed frequent refinancing. When liquidity dried up for those mortgages, potential borrowers who had intended to go through the underwriting process found themselves locked out of the market, and a vicious cycle of declining mortgage funds, declining demand for home purchases, falling prices in credit-constrained neighborhoods, and defaults of underwater borrowers followed.

With FA/AP mortgages, the reduced need to refinance could have halted some of that vicious cycle. FA/AP mortgages also would have provided credit-constrained households with a natural process to rebuild equity more quickly—again, without the need for refinancing—when short-term interest rates fell after 2008. FA/AP mortgages would have naturally performed many of the functions that federal refinancing programs were intended to perform. A typical borrower who financed during the boom with a 5 percent FA/AP mortgage would by 2021 have had his or her principal reduced by more than 15 percent because of many years of low interest rates. Also, unlinking payment from interest rates might have enabled households dealing with economic disruptions to alter their payment schedules without bundling them with unstable mortgage terms.

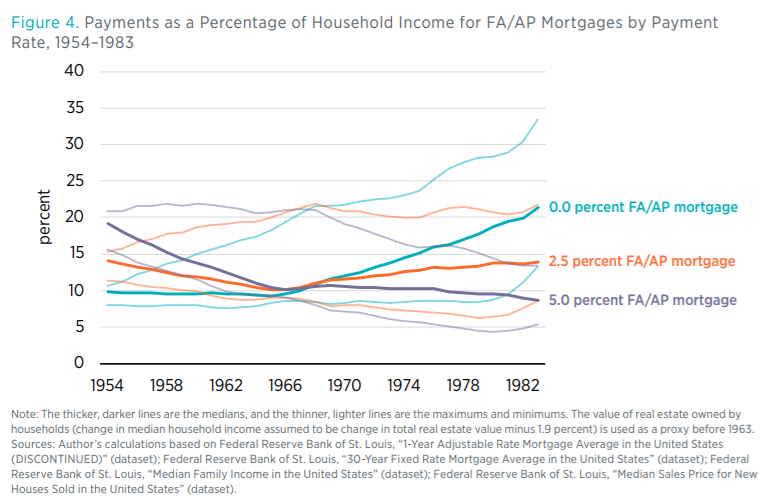

On this last point, the FA/AP framework for setting up a mortgage is surprisingly robust to different payment levels. Figure 4 compares the payments as a proportion of income over the life of a 30-year mortgage for a median-income household in a median-price home originated in the years 1954 to 1983.

Figure 4 compares a 5.0 percent, a 2.5 percent, and a 0.0 percent payment rate. These mortgages are still on a 30-year amortization schedule, so even the 0.0 percent payment rate will have a payment that equals 3.3 percent of the mortgage principal in the first year and grows from there until it pays the remaining balance in year 30. The 0.0 percent payment rate basically means that the principal and monthly payment grow each year at the one-year mortgage rate. That rate is a pretty good proxy for income growth. Since the turn of the century, short-term rates have been similar to the rate of rent inflation in many cities, so mortgages with this payment plan with a 0.0 percent payment rate would have a growth rate in payments similar to what a tenant would face, but the borrower would build equity, especially in cities with perpetually rising rents.

In 1954–1983, the 2.5 percent payment rate would have held mortgage payments stable as a percentage of income over the life of the average mortgage. In the low-rate environment that has developed in recent decades, the average borrower would have enjoyed a declining mortgage payment-to-income ratio, even with a low 2.5 percent payment rate.

A 5 percent payment rate is probably a conservative rate that would make these loans a reliably safe option, but in real terms these loans would be surprisingly stable, even at the 2.5 percent payment rate. Most of the risk of negative equity comes from volatile home prices, regardless of the type of mortgage. Prudent underwriting, mortgage insurance (where useful), and other safeguards would be important for FA/AP mortgages, just as they are with other types of mortgages.

Other Products

There are other kinds of mortgages and proposed mortgages with characteristics similar to those of the FA/AP mortgage. Wayne Passmore proposes a fixed–cost of funds index (COFI) mortgage, indexed to banks’ cost of funds, which may be better than a mortgage indexed to one-year mortgage rates. He also proposes setting the payment rate at the prevailing fixed 30-year rate. The payment would thus be fixed throughout the duration of the mortgage, and the spread savings could be used to pay down equity faster, cutting many years off the typical 30-year amortization schedule.

Because Passmore supposes a conservative payment rate, the principal would decrease in practically every conceivable outcome. Instead of allowing principal to rise in those rare cases where the payment rate is less than the COFI rate, the fixed-COFI mortgage would entail the borrower purchasing mortgage payment insurance, which would have a negligible cost because of the conservative payment rate. Any reduction of principal with the fixed-COFI mortgage would shorten the amortization schedule instead of reducing the payment amount.

The price-level-adjusted mortgage (PLAM) is another product with some features similar to those of the FA/AP mortgage. Like TIPS, PLAMs use a fixed real rate. The real rate (before inflation) is paid monthly, and the principal is adjusted upward, usually monthly, according to an inflation index. The monthly payment rises at the rate of inflation, so in real terms it remains the same over time. This is basically an FA/AP mortgage in which the payment rate and the interest rate are determined by the market rate on fixed-rate mortgages and the inflation rate.

Both fixed-COFI mortgages and PLAMs are similar to the FA/AP mortgage, but an FA/AP mortgage would be a further step in the direction of eliminating features that are somewhat arbitrary financial factors for the borrower. Why should borrowers’ payments be tied to a fixed rate that happened to be the market rate on the day they took on the mortgage? Why should mortgages be referenced to fixed rates that require tactical refinancing? These are concerns that home buyers would prefer to avoid.

Furthermore, FA/AP mortgages would need to reference only a single market rate, such as the one-year ARM rate, to adjust principal or payments (or both). PLAMs and fixed-COFI mortgages both reference fixed rates in some way, and PLAMs require lenders to take on some amount of interest rate risk as a result.

FA/AP mortgages could provide benefits relative to 30-year fixed-rate mortgages and various alternatives. Building on the experience of the COVID-19 pandemic, FA/AP mortgages easily could build in circuit breakers. Borrowers could be given the choice annually to apply underpayments and overpayments to either the amortization schedule (within certain parameters) or the monthly payment. Borrowers could potentially be given the option to forgo or lower payments for some period, as many have during the pandemic. These sorts of options could be easily implemented in mortgages that are already built to handle changing payments or amortization schedules without creating potential interest rate risks for the lenders.

This type of mortgage would be a boon to American home buyers. This proposal would also lower required bank income, because lenders would not need the high premium they receive for making fixed interest rate mortgages. This would reduce the portion of domestic income claimed by the financial sector.

The federal sponsorship of Ginnie Mae, Fannie Mae, and Freddie Mac has been an important element in the dominance of the 30-year fixed-rate mortgage. But a mortgage product that eliminates interest rate risk while maintaining stable cash flows for borrowers would be beneficial for everyone—borrowers, investors, and guarantors (either public or private).

Related Content

- | Mercatus Podcasts Mercatus Podcasts

A Conversation on Lending Standards and Access to Housing

- | Monetary Policy Monetary Policy

- | Research Papers Research Papers

Housing Policy, Monetary Policy, and the Great Recession

- | Monetary Policy Monetary Policy

- | Books Books

Shut Out