- | Government Spending Government Spending

- | Policy Briefs Policy Briefs

- |

Debt and Growth: A Decade of Studies

In the decade following the financial crisis of 2007–2008 and the subsequent European sovereign debt crisis beginning in late 2009, academics and economists have been exploring the relationship between government debt and economic growth. For example, in 2010 economists Carmen Reinhart and Kenneth Rogoff published their notable paper “Growth in a Time of Debt,” which became widely cited and influential among commentators, academics, and politicians in the debate surrounding austerity and fiscal policy in debt-burdened economies.

In this policy brief, we review the literature on the debt-growth relationship since the publication of “Growth in a Time of Debt” to evaluate the claim that high government-debt-to-GDP ratios have negative or significant (or both) effects on the growth rate of an economy. In addition, we assess the claim that there is a nonlinear threshold, around 90 percent of GDP, above which debt has a significant deleterious impact on growth rates. With several European countries taking action to successfully reduce their debt-to-GDP ratios in recent years, it is important for Americans to broaden their understanding of the potential negative effects of debt on growth potential, particularly in light of America’s current fiscal trajectory.

A large majority of studies on the debt-growth relationship find a threshold somewhere between 75 and 100 percent of GDP. More importantly, every study except two finds a negative relationship between high levels of government debt and economic growth. This is true even for studies that find no common threshold. The empirical evidence overwhelmingly supports the view that a large amount of government debt has a negative impact on economic growth potential, and in many cases that impact gets more pronounced as debt increases. The current fiscal trajectory of the United States means that in the coming 30-year period, the effects of a large and growing public debt ratio on economic growth could amount to a loss of $4 trillion or $5 trillion in real GDP, or as much as $13,000 per capita, by 2049.

Why Would a Large Federal Debt Have Negative Effects on the Economy?

Before delving into the existing literature on the relationship between government debt and economic growth, it is useful to briefly explore the economic explanations for why a large and growing debt burden could drag down the growth potential of the US economy. Economists have long noted several macroeconomic channels through which debt can adversely impact medium- and long-run economic growth. More recent observations suggest that large increases in the debt-to-GDP ratio could lead to much higher taxes, lower future incomes, and intergenerational inequity.

High public debt can negatively affect capital stock accumulation and economic growth via heightened long-term interest rates, higher distortionary tax rates, inflation, and a general constraint on countercyclical fiscal policies, which may lead to increased volatility and lower growth rates. Studies on the channels through which debt adversely impacts growth also find that when the debt-to-GDP ratio reaches elevated levels, the private sector seems to start dissaving. These findings contradict the Ricardian equivalence hypothesis, which holds that households are forward looking and increase their saving in response to increases in government borrowing.

As America’s federal debt burden continues to grow, the government must increase borrowing in order to fund its expansive spending programs. This increased government borrowing competes for funds in the nation’s capital markets, which in turn raises interest rates and crowds out private investment. With entrepreneurs in the private sector facing higher costs of capital, innovation and productivity are stifled, which reduces the growth potential of the economy. If the government’s debt trajectory spirals upward persistently, investors may start to question the government’s ability to repay debt and may therefore demand even higher interest rates. Over time, this pattern of crowding out private investment coupled with higher rates of interest will drive down business confidence and investment, which drags productivity and growth down even further.

A further cost resulting from increased government borrowing is the crowding out of public investment as growing interest payments consume an ever larger portion of the federal budget, leaving lesser amounts of public investment for research and development, infrastructure, and education. In fact, the Congressional Budget Office (CBO) predicts that by 2049, the cost of paying the interest on the nation’s debt will be the third-largest budgetary item after Social Security and Medicare, constituting almost 6 percent of GDP. The combination of reduced private investment and crowding out of public investment will have negative effects on social mobility as Americans find it harder to buy a home, finance a car, or pay for college. Reduced investment, lower productivity, and declining social mobility will continue to drive down the growth potential of the economy.

Finding the Tipping Point

“Growth in a Time of Debt” is the cornerstone study on the subject of debt and growth over the past decade. In order to determine the effects of government debt on growth, the authors compiled data covering 1946 to 2009 from the International Monetary Fund (IMF), the World Bank, and the Organisation for Economic Co-operation and Development (OECD) for 44 countries. The study finds that across both advanced and emerging economies, high debt-to-GDP levels (90 percent and greater) are associated with notably less growth. Countries with debt-to-GDP ratios greater than 90 percent have median growth roughly 1.5 percent lower than that of the less-debt-burdened groups and mean growth almost 3 percent lower.

Manmohan Kumar and Jaejoon Woo largely corroborate the findings of Reinhart and Rogoff. Covering 38 countries during 1970 to 2007, their study explores the impact of high public debt on long-run economic growth. Their analysis reveals an inverse relationship between initial debt and subsequent growth, controlling for other determinants of growth: on average, a 10 percentage point increase in the initial debt-to-GDP ratio is associated with a slowdown in annual real per capita GDP growth of around 0.2 percentage points. There is also some evidence of nonlinearity, with only high levels of debt (greater than 90 percent of GDP) having a significant negative effect on growth.

In the aftermath of the financial crisis, Mehmet Caner, Thomas Grennes, and Fritzi Koehler-Geib also authored a study that broadly corroborates the findings of Reinhart and Rogoff. Using World Bank data from 99 countries during 1980 to 2008, the authors assess whether there is a tipping point at which public debt starts to negatively affect growth levels. The main finding of their analysis is that the threshold where average long-run public-debt-to-GDP begins to affect growth is 77 percent for all countries in the sample. If public debt is above this threshold, each additional percentage point of debt costs 0.017 percentage points of annual real growth. However, these results are based on long-term averages over almost 20 years, so short-term deviations above the threshold may not negatively affect growth.

One study that challenges the methodology and findings of Reinhart and Rogoff is by Thomas Herndon, Michael Ash, and Robert Pollin. The authors replicated Reinhart and Rogoff’s study and found coding errors in the original study, which may have inaccurately represented the relationship between public debt and GDP growth for the countries in Reinhart and Rogoff’s sample. When properly calculated, the average real GDP growth rate for countries carrying a debt-to-GDP ratio greater than 90 percent is actually 2.2 percent, not −0.1 percent as published in Reinhart and Rogoff’s study. Average growth within the 90–120 percent category is 2.4 percent, reasonably close to the 3.2 percent growth in the 60–90 percent category. Further, GDP growth in countries with a debt-to-GDP ratio between 120 and 150 percent is lower, at 1.6 percent, but does not fall off a nonlinear cliff. So while Herndon, Ash, and Pollin find no evidence for a debt threshold around 90 percent of GDP, they find (as do other scholars) a nonlinear relationship between public debt and growth.

Cristina Checherita-Westphal and Philipp Rother assess the impact of high and growing government debt on economic growth. Using data from the annual macroeconomic (AMECO) database of the European Commission, the authors investigate the average relationship between government-debt-to-GDP ratios and per capita GDP growth rates in 12 European countries from 1970 to 2011. Their study finds a nonlinear impact on growth with a turning point—beyond which the government-debt-to-GDP ratio has a deleterious impact on long-run growth—at about 90 to 100 percent of GDP. What’s more, the negative growth effect of high debt may start at levels of around 70 to 80 percent of GDP. That is to say, the confidence interval is entirely negative at 90 to 100 percent of GDP and 70 to 80 percent is the region where the regression line crosses zero. Similar results are found in a panel data study of OECD countries. Stephen Cecchetti, Madhusudan Mohanty, and Fabrizio Zampolli examine the level of government debt, nonfinancial corporate debt, and household debt in 18 OECD countries from 1980 to 2010. They find that when public debt is around 85 percent of GDP, further increases in debt may begin to have a significant impact on growth: specifically, a further 10 percentage point increase reduces trend growth by more than 0.1 percentage points.

Pier Carlo Padoan, Urban Sila, and Paul van den Noord developed an analytical framework to examine how a combination of fiscal consolidation, structural reform, and financial backstops can help countries escape from the debt trap. Assessing data from 28 OECD countries from 1960 to 2011, the authors find that in all cases the estimated threshold effect is close to 90 percent, which is consistent with the findings of other researchers. Increasing public debt by 1 percentage point is associated with an average reduction of GDP growth by 0.012 percentage points in the following year, and it is associated with a reduction in average annual growth over the next five years by 0.028 percentage points.

Another study also uses the AMECO database, this time to review 12 European countries from 1990 to 2010. Using a dynamic threshold panel methodology, the authors analyze the nonlinear impact of public debt on GDP growth. The study finds that the short-run impact of debt on GDP is positive, but the impact decreases to near zero and loses significance beyond public-debt-to-GDP ratios of around 67 percent. For high debt ratios (greater than 95 percent), additional debt has a negative impact on economic activity.

Using the World Bank’s World Development Indicators database, António Alfonso and João Jalles use a panel of 155 countries from 1970 to 2008 to assess the links between growth, productivity, and government debt. The authors find a negative effect of the debt ratio for countries with debt levels greater than the 90 percent threshold and a slightly positive effect for countries with debt levels less than the 30 percent level. The growth impact of a 10 percent increase in the debt ratio is −0.2 percent for countries with debt-to-GDP ratios greater than 90 percent and 0.1 percent for countries with debt-to-GDP ratios less than 30 percent, and the debt ratio threshold is 59 percent of GDP. Using the same database, Alfonso and José Alves study the effects of public debt on economic growth for annual and five-year average growth rates, as well as the existence of nonlinear effects of debt on growth. Their analysis covers 14 European countries from 1970 to 2012, with results showing an impact of −0.01 percent for each 1 percent increase of public debt. In addition, the authors find an average debt ratio threshold of around 75 percent.

In a study on fiscal space and debt sustainability, Atish Ghosh and coauthors attempt to answer the question of how high public debt can rise without compromising fiscal solvency. Their study seeks to determine a “debt limit” beyond which fiscal solvency is in doubt, focusing on 23 advanced economies from 1970 to 2007. The authors find that the marginal response of the primary balance to lagged debt is nonlinear, remaining positive at moderate debt levels but starting to decline when debt reaches around 90 to 100 percent of GDP. These results are similar to the findings of a study mentioned earlier by Anja Baum, Cristina Checherita-Westphal, and Philipp Rother, and are broadly consistent with the findings of Reinhart and Rogoff. In contrast to these results, Andros Kourtellos, Thanasis Stengos, and Chih Ming Tan do not find any common debt threshold. The authors investigate the heterogeneous effects of debt on growth using public debt as a threshold variable for 82 countries during 1980 to 2009. Their findings suggest that the relationship between public debt and growth is mitigated crucially by the quality of a country’s institutions. All else being equal, higher public debt results in lower growth for countries with less democratic regimes, suggesting that the institutional framework of a country may be more important in determining growth potential than any given debt-to-GDP ratio.

Focusing on 12 European economies over 1980 to 2012, Pinar Topal reviews the growth implications of public debt using a dynamic panel threshold model. Like Baum, Ghosh, and their respective coauthors, Topal confirms evidence of a double threshold model. Her study finds that debt-to-GDP ratios below 71.66 percent have a positive and significant impact on growth, debt-to-GDP ratios between 71.66 percent and 80.21 percent have a negative impact on growth, and debt-to-GDP ratios greater than 80.21 percent have a negative impact that loses strength. Jernej Mencinger, Aleksander Aristovnik, and Miroslav Verbič also focus on the impact of growing public debt in European economies. Their study examines and evaluates the direct effect of higher indebtedness on economic growth for 25 EU countries from 1980 to 2010. The results across all models indicate a statistically significant nonlinear impact of public-debt-to-GDP ratios on the annual GDP per capita growth rate. The authors also calculate that the debt-to-GDP turning point, where the positive effect of accumulated public debt inverts into a negative effect, is between roughly 80 percent and 94 percent for the old member states. For EU states that have been recently admitted, the turning point is found to be a much lower 53–54 percent.

Markus Eberhardt and Andrea Presbitero, like Kourtellos, Thanasis, and Tan, do not find any common debt turning point. Assessing a large dataset of 118 countries from 1961 to 2012, the authors do find some support for a negative relationship between public debt and long-run growth across countries, but no evidence for a similar, let alone common, debt threshold within countries. So while they identify no common threshold, the long-run debt coefficients appear to be lower in countries with higher average public debt burdens. One study by Balázs Égert does find a threshold range, but one that is different than most ranges found in the existing literature. Using IMF and World Bank data, this study reviews the data of 44 countries from 1960 to 2010 and finds that the negative nonlinear relationship between debt and growth is very sensitive to modeling choices. The study also finds that the negative nonlinear effect kicks in at much lower levels of public debt than other studies suggest (between 20 percent and 60 percent of GDP).

In recent years, new studies on the debt and growth relationship have been added to the existing literature. One of these newer studies is by Juan Gabriel Brida, David Matesanz Gómez, and Maria Nela Seijas. Using a nonparametric approach based on data from 16 countries from 1977 to 2015, the study shows a negative relationship between debt and growth in line with most of the previous empirical literature. During the analyzed period, growth in economic output seems to be driven by debt-to-GDP levels, particularly around the 90 percent debt-to-GDP threshold. Conversely, using a dynamic heterogeneous panel data model, Alexander Chudik and coauthors do not find a common debt threshold. After observing data from 40 countries over a 45-year period, the authors find no evidence for a universally applicable threshold effect in the relationship between public debt and economic growth. Regardless of the threshold, however, the authors do find significant negative effects of public debt buildup on output growth.

Duygu Yolcu Karadam investigates the threshold effects in the debt-growth link for different types of debt covering a large dataset of 134 countries from 1970 to 2012. She finds the nonlinearity of the relationship between debt and growth to be dependent mostly on the debt’s structure. She concludes that the impact of public debt on growth turns from positive to negative gradually after some threshold has been reached. While negative growth effects appear at a public-debt-to-GDP ratio of 106.6 percent for the whole sample, for developing countries these effects occur at a much lower point, namely 88 percent public debt to GDP. Adopting a slightly different approach from previous studies, Caner, Qingliang Fan, and Grennes analyze how the interaction of public and private debt influences economic growth. Using an endogenous panel threshold model, the authors examine the data from 29 OECD countries from 1995 to 2014. They find the interaction between the public and private debt and economic growth to be negative and significant when debt reaches the level of 137 percent. The negative effect of public debt on economic growth is larger when private debt is larger.

Like Caner, Fan, and Grennes in their study on the interaction of public and private debt, Janus Lim investigates the rate of total debt accumulation and its effect on economic growth. Using a panel vector autoregression framework, the author investigates a causal link between the sum of public and private debt and growth. The study includes 41 countries from 1952 to 2016 and finds a negative relationship between the rate of total debt accumulation and economic growth, with a one standard deviation change in the former leading to a 0.2 percentage point contraction in the latter. As the author does not investigate the existence of a threshold in the data, the study does not present a common debt threshold estimate.

In recent years some studies investigating the effects of public debt on economic growth have failed to find any evidence of a causal link between public debt and growth. Jan Jacobs and coauthors investigate the causal relationship between public-debt-to-GDP ratios and economic growth rates for 31 EU and OECD countries. They find no causal link between public debt and growth, irrespective of the levels of the public-debt-to-GDP ratio. What is more, the authors actually find a causal relationship from growth to debt, suggesting that negative growth effects increase public debt levels by inflating long-term real interest rates. A second study, which corroborates the findings of Jacobs and coauthors, is by Eberhardt. The author employs extensive time series data from 27 countries and finds no evidence for a systematic long-run relationship between debt and growth.

The final study on the relationship between debt and growth may provide the most data-rich analysis. Vighneswara Swamy uses World Bank and IMF data from 252 countries from 1960 to 2009 to observe the cause-and-effect relationship between debt and growth. This study observes a negative relationship between government debt and growth. The point estimates of the range of econometric specifications suggest that a 10 percentage point increase in the debt-to-GDP ratio is associated with 0.23 percentage point reduction in average growth. A threshold ratio is found around 110 percent of GDP, with countries that have ratios in the 91–150 range showing a downward trend in growth and countries in the range of 151 or more showing a steeper downward trend. In answer to the question of cause and effect, the panel vector autoregression analysis indicates a negative correlation, suggesting that as government debt rises, growth tends to decline. For debt levels less than 60 percent, public debt tends to have a positive effect on growth, while debt levels between 61 and 90 percent tend to have no significant impact on growth, and debt levels above 90 percent have increasingly negative impacts on growth rates.

Table 1. Summary of Studies on the Relationship between Debt and Economic Growth

Study | Sample | Finding (Debt Effect) | Threshold |

Reinhart and Rogoff (2010) | 44 countries | negative | 90% |

Kumar and Woo (2010) | 38 countries | negative | 90% |

Caner, Grennes, and Koehler-Geib (2010) | 99 countries | negative | 77% |

Checherita-Westphal and Rother (2012) | 12 European countries | negative | 95% |

Herndon, Ash, and Pollin (2014) | 20 countries | negative | no common threshold |

Cecchetti, Mohanty, and Zampolli (2010) | 18 OECD countries | negative | 85% |

Padoan, Sila, and van den Noord (2012) | 28 OECD countries | negative | 82%–91% |

Baum, Checherita-Westphal, and Rother (2013) | 12 European countries | negative | 95% |

Alfonso and Jalles (2013) | 155 countries | negative | 59% |

Ghosh et al. (2013) | 23 advanced economies | negative | 90%–100% |

Kourtellos, Stengos, and Tan (2013) | 82 countries | negative in low-democracy regimes | no common threshold |

Alfonso and Alves (2015) | 14 European countries | negative | 75% |

Topal (2014) | 12 eurozone countries | negative | 71.6%–80.2% |

Mercinger, Aristovnik, and Verbič (2014) | 25 EU countries | negative | 80%–94% |

Eberhardt and Presbitero (2015) | 118 countries | negative | no common threshold |

Égert (2015) | 44 countries | negative | 20%–60% |

Brida, Gómez, and Seijas (2017) | 16 countries | negative | 90% |

Chudik et al. (2017) | 40 countries | negative | no common threshold |

Yolcu Karadam (2018) | 134 countries | negative | 106.6% |

Caner, Fan, and Grennes (2019) | 29 OECD countries | negative | 137% (public/private) |

Jacobs et al. (2020) | 31 OECD countries | no effect | N/A |

Eberhardt (2019) | 27 advanced economies | no effect | N/A |

Lim (2019) | 41 countries | negative | N/A |

Swamy (2019) | 252 countries | negative | 110% |

How Might Debt Drag Affect Future US Economic Growth?

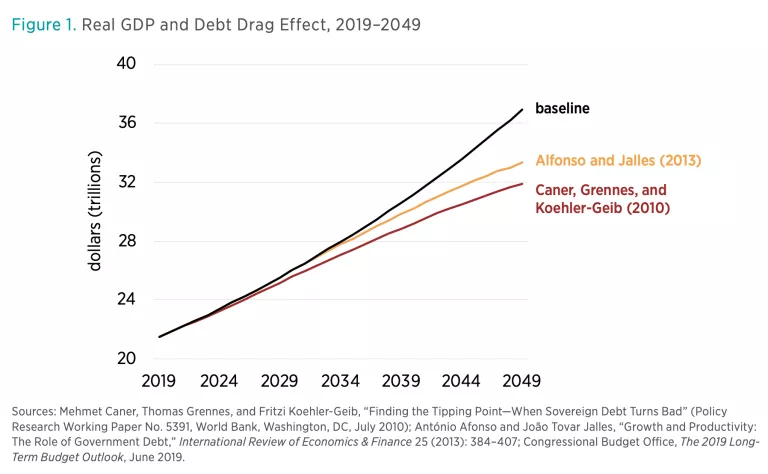

The CBO produces annual and updated long-term projections for US growth rates. For the purpose of predicting the negative effects of high public debt levels on growth rates, we use estimates from two of the studies in our literature review to project real GDP growth rates for 2019 to 2049. Specifically, we base our prediction on the studies by Caner, Grennes, and Koehler-Geib and by Alfonso and Jalles. The former study finds a lower debt threshold (77 percent) but a smaller debt drag effect on economic growth; the latter study finds a higher debt threshold (90 percent) but a slightly larger debt drag effect. The estimates of Alfonso and Jalles are also broadly consistent with the estimated debt drag findings of Kumar and Woo.

Figure 1 illustrates the differences in real GDP over 2019 to 2049. The black line represents the CBO baseline estimate, the orange line represents the projected real GDP under debt drag effects estimated by Alfonso and Jalles, and the red line represents projected real GDP under debt drag effects estimated by Caner, Grennes, and Koehler-Geib. The results demonstrate that over the coming 30-year period, the effects of a large and growing public-debt-to-GDP ratio on economic growth could amount to a loss of $4–$5 trillion in real GDP. In per capita terms, this would be the difference between a baseline real GDP per capita of $95,339 and a debt-drag-affected real GDP per capita of $82,376–$86,021. This range is around $9,000–$13,000 per capita less than the baseline, a significant drag in living standards for the average American.

Concluding Remarks

While not all of the 24 studies covered in this literature review find a common threshold, table 1 does show that 17 out of 24 studies do find a debt threshold, and half of the studies find a threshold somewhere between 75 and 100 percent. More importantly, the results of every study except two find a negative relationship between high levels of government debt and economic growth, even for studies that find no common threshold. So while the empirical results from a decade of studies find mixed evidence for a debt threshold of 90 percent as found by Reinhart and Rogoff, half of the studies do suggest a threshold somewhere between 75 and 100 percent. Aside from the threshold question, the empirical evidence overwhelmingly supports the view that large government debt has a negative impact on the growth potential of a debt-burdened economy. In many cases, this impact gets stronger as debt increases.

In light of the current public debt trajectory in the United States, these findings should be of concern to American policymakers and the American public at large. Diminished economic growth rates will have significant negative impacts on living standards for average Americans over time. Compared to a growth rate of 3 percent, a growth rate of 2 percent means that real GDP per person will be almost $20,000 lower after 20 years. With a federal-debt-to-GDP ratio of 106 percent in 2018, the US fiscal condition is already having a deleterious impact on the country’s growth potential. Policymakers need to stop kicking the fiscal can further down the road and act now to return sustainability to America’s federal budget and fiscal condition. Policymakers should consider implementing real institutional reform to change the debt trajectory, including meaningful budget rules that have broad scope, few and high-hurdle escape clauses, and minimal accounting discretion.