A growing number of economists hold the view that the US government’s growing debt is nothing to worry about. They believe this because real interest rates are not only historically low but are also forecast to stay low for a long time. As such, the government can carry high debt levels without worrying about debt sustainability. In addition, some economists argue that, in countries where low real interest rates and the negative interest-rate-minus-growth differential are sustained, the government can increase primary deficits without worrying about future costs.

This new fiscal paradigm rests on assumptions that do not apply to the fiscal issues facing the United States. For example, it requires the US government to balance its budget for several generations after a one-time increase in the size of the debt. However, the United States has repeatedly run a regular primary deficit of 5 percent of GDP and added even more deficit spending during crises. The paradigm also requires immense faith in the willingness of legislators to spend money in ways that produce high and consistent economic growth. Yet a review of the literature on the impact of government spending on growth reveals that, generally, such spending crowds out private-sector spending. The same is true in the relationship of debt to growth. In other words, even if interest rates stay low forever, growth could slow so much as to make the starting assumption moot. Finally, it is simply imprudent to count on low interest rates lasting forever.

However, a deeper fact should worry economists more than it does—namely, it is hard for government to make good policies when it swells so large that it has little practical choice but to depend on annual deficit financing. In particular, high and growing levels of public debt are likely to induce higher inflation while the growing burden of debt and deficit financing increases political pressure to continue pursuing inflationary policy. High debt levels also make inflation harder to control if it becomes persistent.

The “End of Inflation” Era Has Ended

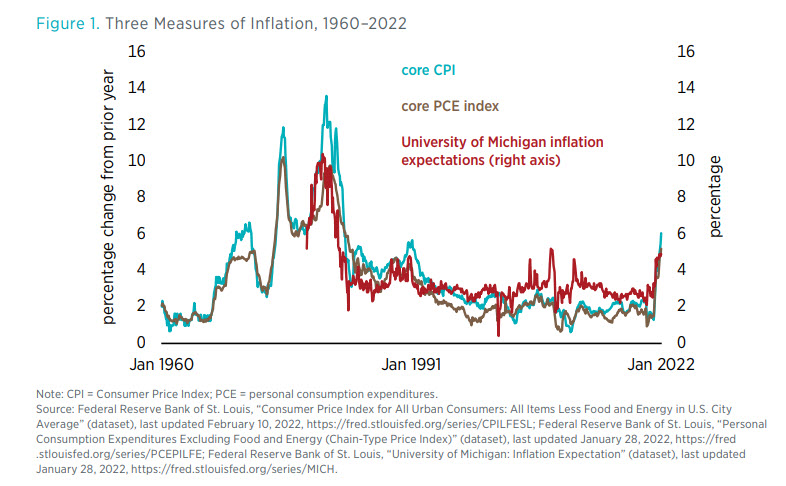

In his 1970 lecture “The Counter-Revolution in Monetary Theory,” Milton Friedman made his now-famous observation that “inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.” One cannot help but think about this observation when faced with the now 25-year puzzle of low and relatively stable levels of inflation in spite of large deficits, high debt, significant expansion of the Fed’s balance sheet, and more than a decade of accommodative monetary policy largely in the form of ultra-low interest rates. In fact, as figure 1 shows, inflation has been in such a downward trend that, for nine years beginning in 2012 (the year the Fed adopted its 2 percent inflation target), inflation rarely reached 2 percent.

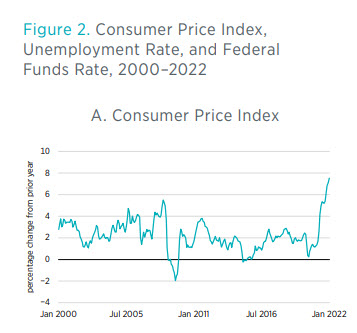

This phenomenon, not being unique to the United States, has led some to declare that inflation has been conquered, the Phillips curve is flat, and a central bank could run an economy hot without too much risk of stagflation. That is, until now. After unprecedented monetary and fiscal stimulus, the economy is overheating (as measured in terms of the nominal GDP gap), and the United States has experienced the highest levels of inflation in four decades (figure 2).

In the 12 months through January 2022, the Consumer Price Index (CPI) rose 7.5 percent, the highest inflation since 1982 and a jump from the annual CPI growth rate of 1.9 percent over the previous decade. Both the Fed and experts were caught by surprise and, thus, proven wrong about inflation. Many experts predicted that there would be no inflation. When inflation emerged, they claimed that it was transitory. When it persisted, they said that prices were just catching up to prepandemic levels. When prices began to exceed prepandemic levels, the experts blamed the problem on the supply of lumber, used cars, and other goods; on a drought in Taiwan; and on overall supply-chain tangles. And when Americans finally started really to notice the inflation, experts argued that there was nothing that the Fed could do to address supply-chain issues and that, in fact, any scaling back of the Fed’s policies needed to be delayed to eliminate shortfalls in economic activity.

Understanding the relationship between these factors and inflation is helpful, but addressing the issue ultimately requires a sound definition, such as the one posed by economist Arnold Kling: “spending [is] rising faster than production . . . primarily because the government has injected a lot of paper wealth into the economy through unprecedented levels of deficit spending.” In other words, although one cannot dismiss supply-chain issues and shifts in consumption from services to goods, monetary- and fiscal-induced demand has played a key role in this burst in inflation.

Regardless, it does not inspire confidence that no one really knows how long the inflation will last or how high prices will go. In fact, there are reasons to worry that America is bound to repeat some of the mistakes of the past because the Fed’s new policy framework (waiting to see inflation, allowing inflation to run hot to fill the output gap, promising to keep rates low to stimulate the economy, and targeting inclusive growth) and the Fed’s representatives and supporters’ talking points are transporting America back to the 1970s. Many seem to have forgotten the painful lessons of that decade.

Among these lessons is that there is no permanent tradeoff between inflation and unemployment. As Fed Chair Paul Volcker noted in early 1980 after he was appointed to tame inflation, “My basic philosophy is over time we have no choice but to deal with the inflationary situation because over time inflation and the unemployment rate go together. . . . Isn’t that the lesson of the 1970s?” Americans have also learned since then that microeconomic efficiency brought about by better incentives and well-functioning markets is better equipped than monetary policy to address issues of sustained growth and wages. And they learned that a delay in the Fed’s response to inflation could cause a severe recession.

However, an important lesson Americans learned from the 1970s is that inflation expectations matter. The general dynamics of inflation are a mix of expected inflation plus inflationary pressures that exist in the present moment, which today include pent-up demand, a tight labor market, and supply-chain constraints. These dynamics make inflation hard to predict, because inflation today depends in large part on what people expect inflation in the future will be above and beyond whatever might be produced by existing pressures. If workers expect higher prices next year, they will demand higher wages now. If businesses believe input prices and wages will go up next year, they will increase their prices today. If consumers expect prices to go up tomorrow, they will buy what they need today.

The good news is that if people believe that inflation over the long run will remain low, then when inflationary pressures disappear so will inflation. But if they believe that inflation will rise, then inflation could persist after the inflationary pressures have gone away, especially if the Fed does not tighten its monetary policy. The orthodox view among economists is that what anchors inflation expectations is the belief that the Fed has tools to control inflation, such as raising interest rates, and is willing to endure a recession to use them. The Council of Economic Advisors expounds upon this belief: "If, however, inflationary expectations become untethered from [the Fed's inflation] target, prices may rise in a lasting mannger. This sort of inflationary, or 'overheating,' spiral might then lead the central bank to raise interest rates quickly which then significantly slows the economy and increase unemployment. Another widespread belief is that the Fed’s announcement of its inflation targets and its commitment to hit those targets should by itself be enough to “coordinate expectations.”

This belief is incomplete. The next section of this brief offers an alternative anchor of inflation: sound fiscal policy. As John Cochrane explains, “Major explosions of inflation around the world have ultimately resulted from fiscal problems, and it is hard to think of a fiscally sound country that has ever experienced a major inflation. So long as the government’s fiscal house is in order, people will naturally assume that the central bank should be able to stop a small uptick in inflation.”

All that said, in spite of the inflation hike America is currently experiencing, interest rates remain low, with the nominal annual rate on five-year Treasury bonds at about 1.9 percent, whereas the real return on five-year Treasury Inflation-Protected Securities remains −1.0 percent. Another reassuring sign, Americans were told, was that survey-based measures of medium- to long-term inflation expectations did not seem to increase. As the Council of Economic Advisers reassuringly tweeted back in April 2021, “A monthly composite measure that summarizes 22 different market- and survey-based measures of long-run inflation expectations suggests higher expectations, but the levels of these expectations remain well within historical levels.”

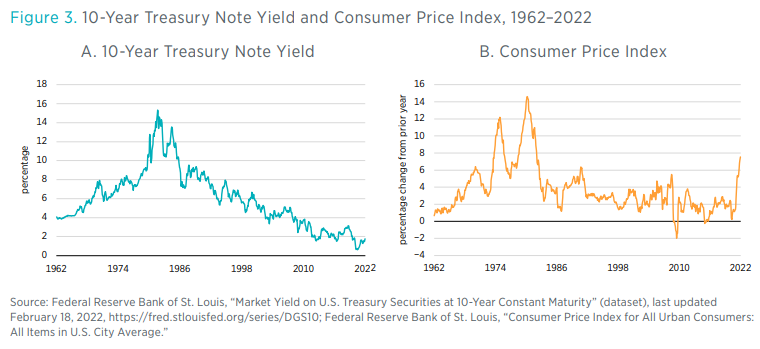

However, historically, these survey-based forecasts of long-run inflation expectations and interest rates have a terrible track record of predicting inflation. As seen in figure 3, the interest rate on 10-year Treasury notes does not rise before increases in inflation.

In other words, the market can get surprised by inflation. For instance, interest rates did not signal the inflation of the 1970s or the disinflation of the 1980s, and the Greek government could borrow at low rates until the global financial crisis, when it could not anymore. Inflation, like the typical bank run, is unpredictable precisely because it is so conditional on expectations, and expectations can change very fast.

Controlling Inflation in Times of High Debt

The risk of sustained high annual inflation on the scale of the 1970s following the government’s one-time borrowing and printing of $5 trillion is low, although everyone now admits that heightened inflation is persisting. After a slow start in 2020, the five-year break-even inflation rate, which measures the market’s expectations of inflation over the next five years, started to rise rapidly. In November 2021, it reached the highest point in the two-decade history of the measurement. This increase is worrisome and still ongoing, but most economists believe that if inflation persists, the Fed can and will, in a timely manner, raise rates to maintain its credibility as an inflation fighter.

But when and how much, specifically, should the Fed raise rates if inflation persists? On this question different people offer different answers. A lesson of the past is that it is hard to get inflation under control unless interest rates rise enough to be above the rate of inflation. Stanford economist John Taylor (after whom the Taylor rule is named) suggests that if inflation rises from 2 percent to 5 percent, for example, then interest rates should rise by 4.5 percentage points (one and one-half times the gap between the two rates). If one adds a 2.0 percent inflation target and a 1.0 percent long-run real rate of interest, then the rule recommends a federal funds rate of 7.5 percent. Others, including Fed officials, disagree and think a much lower rate increase will be necessary.

Correctly answering this question is of great importance. On one hand, contractionary monetary policy lowers aggregate demand, which can lead to lower output and employment, especially in a world of sticky wages and prices. On the other hand, indecisiveness when raising rates risks entrenching inflation and steepening the rate increases that are ultimately required to fight inflation. America saw this tradeoff operate in the 1970s and early 1980s. Fed Chair Paul Volcker had to raise interest rates from 9 percent to 19 percent and slow money growth through 1982, and the consequences of these policies were long lasting: interest rates remained high long after inflation started to fall, given that more risk-averse bondholders demanded higher returns.

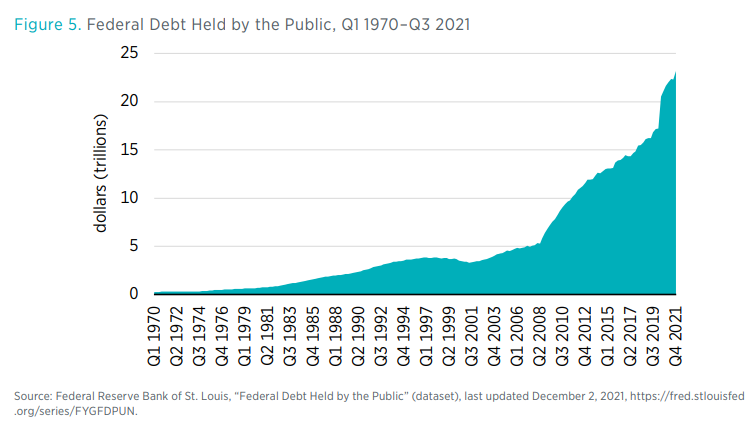

Facing this tradeoff again today, the Fed has announced three small and separate rate increases (not enough to put real interest rates in positive territory) starting in March 2022, after the termination of Fed asset purchases. But the amount of America’s debt makes fighting inflation harder today than in the past. A few fiscal facts are important to bear in mind: US debt held by the public is now $23 trillion, or 100 percent of GDP, and a large share of US debt has short-term maturity (25 percent of US debt has to be rolled over every year). Therefore, any increase in interest rates sufficient to fight inflation would quickly explode the federal budget. A rate increase to just 1 percent would add roughly $250 billion per year to the deficit, an increase to 5 percent would add $1 trillion to the deficit, and an increase to 20 percent would add $4 trillion to the deficit.

These large increases to the deficit would not be politically popular. In addition, significant increases in debt service would, theoretically, crowd out other government spending, making it harder for legislators to implement fiscal consolidation (raising tax revenues or reducing public spending). Without fiscal consolidation, raising nominal interest rates would increase real interest rates (if one assumes sticky prices). Higher real interest rates would increase household wealth through lower inflation (increasing the real value of wealth) and higher interest receipts (raising household income flows). Thus, although the central bank is aiming to lower inflation, its efforts could backfire by boosting demand for goods and services. Higher levels of debt work to amplify these (demand-driven) inflationary pressures if there are no plans for fiscal consolidation (e.g., tax increases to offset the wealth effect).

As economist Eric Leeper states, “fiscal responses are fundamental, even indispensable to monetary policy impacts on inflation.” They are “the difference between a Brazilian-style interest rate and inflation spiral and a successful reigning [sic] in of inflation,” he adds.

Empirical work confirms that fiscal contraction is a key element to reducing persistent inflation. For instance, legislators implemented fiscal consolidation (by raising revenue, decreasing spending, or both) during each of the past three latest victories over inflation: in the late 1940s, after the 1980–1982 Recession, and in the mid-1990s. In other words, stable inflation expectations are anchored not by the toughness of the Fed, but by sound fiscal policy. Unfortunately, this link between fiscal and monetary expectations is too often overlooked in conventional inflation debates, with fiscal authorities acting as though inflation outcomes are independent of fiscal policy.

Whereas the short-term danger of such debt-triggered inflation is likely small, the medium- to long-term risks are large. The following sections provide three reasons for this fact.

Debt Projections Are Not Encouraging, and the Debt Is Funded Largely by Rolling Over Short-Term Securities

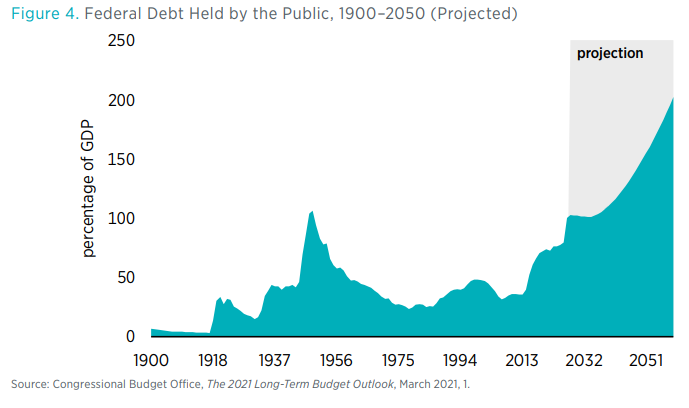

The annual long-term budget outlook of the Congressional Budget Office (CBO) is grim. The CBO expects annual deficits to run at about 4 percent of GDP for the next 10 years, and it expects about 20 percent of all federal spending to be borrowed during that time. As mentioned earlier, the federal debt held by the public is 100 percent of GDP. The CBO projects that the debt held by the public will rise to 106 percent of GDP in the coming decade. The projected debt-to-GDP ratio is 203 percent in 2050 (see figures 4 and 5).

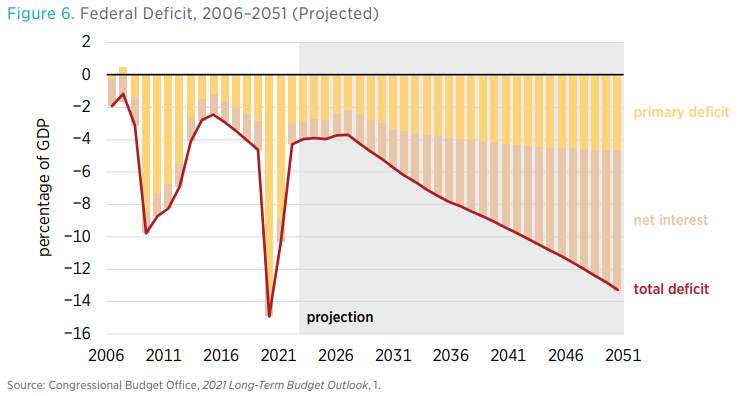

Over the next three decades, the CBO forecasts that the United States will run regular primary deficits of 5 percent while interest on the debt grows significantly (figure 6).

These projections rely on the assumption that the United States experiences no new emergencies, no new major government programs, and no future recessions. They also omit federal unfunded liabilities (benefits promised to the public—seniors, primarily—that the federal government has no coherent plan to finance). Large debt and sustained future deficits put America in unfamiliar danger and, thus, increase the likelihood that investors will believe that bonds held today will be paid off by future money printing, leading to future inflation.

However, worries about future deficits can also cause inflation today, because a large share of US debt held by the public is very short term. Currently, over $6 trillion, or 25 percent, of the debt has a maturity of one year or less. Almost 60 percent, or $14 trillion, of US debt has a maturity of four years or less. As a result, reaching a debt-to-GDP ratio that will automatically trigger higher rates or a run on the dollar followed by a debt crisis is not the primary risk America faces. Rather, the primary risk is that somewhere down the road, during another emergency that sparks massive spending and borrowing, America will face a debt rollover crisis started by short-term investors worried that the Fed will print money to accommodate fiscal policy and will let inflation get out of control.

If investors believe they might not be repaid enough to compensate them for inflation, they may decide to get rid of what they own, and new investors will require a higher rate of return to hold debt. Therefore, the longer and larger risk America faces is an inflation-driven rollover crisis that occurs when people fear they will be repaid in devalued dollars.

Domestic Actors Are Financing an Increasing Share US Debt

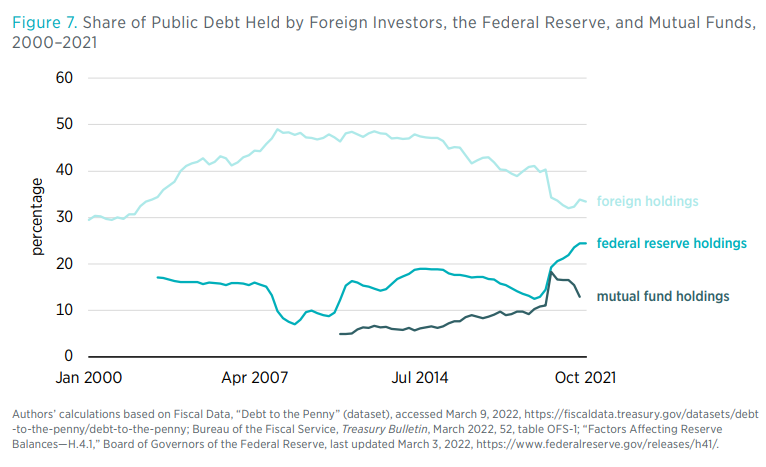

Before one even takes under consideration the current legislation going through Congress, one must acknowledge that annual budget deficits are forecast to average more than 4 percent of GDP for the next 10 years. This is high by historical standards. Although America ran large deficits during the 2007–2008 financial crisis, most of this debt was financed by foreign investors, owing to a large and growing demand for dollar-denominated assets and government liabilities. This demand was in part the product of a flight to quality and safety. Moreover, high foreign demand for safe US assets had the effect of putting downward pressure on interest rates and inflation.

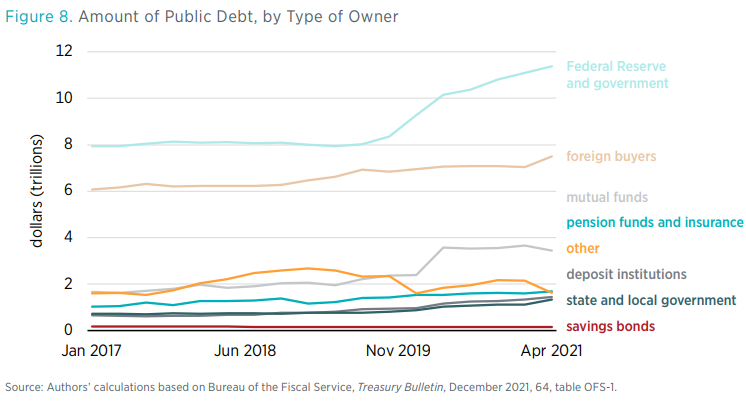

However, as figures 7 and 8 demonstrate, those conditions are changing. Domestic actors such as the Fed, banks, state and local governments, and money market mutual funds are increasingly financing the growing government debt. Unlike in economic crises of the past, many foreign nations dumped their holdings of US Treasury securities during the early months of the COVID-19 pandemic. Between February and April 2020, faced with their own need for pandemic relief funds, foreign nations reduced their holdings of US Treasury securities by over $320 billion. Although foreign demand for US Treasury securities has begun to recover in recent months, foreign investors are not the primary buyers of US debt, as they used to be. Since the middle of 2014, foreigner purchases of US Treasury securities have made up only a small share (12 percent) of the total increase in US debt. If this trend persists, the United States may not be able to count on foreign demand to absorb whatever debt it issues, which will raise the cost of rolling over debt and put greater pressure on the Fed to expand the money supply. These demand-side dynamics will undoubtedly place upward pressure on inflation.

Heightened inflationary pressures mean that the Fed now has to taper its purchases of US Treasury securities, as opposed to buying them. Depending on whether foreign demand steps in to fill the resulting gap in demand, the tapering and selling might result in higher interest rates and subsequent growth in debt service payments, but one cannot know for sure until the Fed starts selling securities that mature in coming months.

Fiscal Norms Are Shifting

The federal government seems to have adopted an open-ended attitude that its debt will not be repaid with higher taxes or spending cuts. That is a fundamental break from the previous crisis, when government rhetoric involved taking on more debt today but implementing fiscal consolidation later. The new attitude toward debt could be a serious challenge to some of the fiscal norms that have prevailed in the United States for decades, such as deficits begetting surpluses that can be used to repay debt in full or fiscal consolidation occurring when interest payments on outstanding debt become a sufficiently large fraction of federal expenditures. If investors believe that there is no broad consensus about these norms, it is likely that deficits will become more inflationary.

The Risk of Fiscal Dominance

There is little doubt that the path for the Fed to control inflation is not easy, especially given that Congress shows no sign of wanting to slow down spending. Adding to the difficulty is the question of fiscal dominance. Fiscal dominance occurs when fiscal authorities demand that the Fed set monetary policy to suit the government’s preferences. Although central banks are ostensibly independent, theory and experience put this independence to the test. The concern about Fed independence is nontrivial, given that a surge in federal debt could compel the Fed to keep interest rates low for the foreseeable future to make the government’s debt service costs manageable.

Adding to the concern of fiscal dominance is the difficulty faced by Fed officials whenever they must implement a policy that creates a risk of recession, including an increase in unemployment, which would likely be concentrated among disadvantaged workers. This difficulty looms large today given the Fed’s new desire to eliminate shortfalls in employment from its maximum level, a departure from its previous desire to prevent employment from getting too high or too low. Furthermore, in a speech earlier this year, candidate for Fed vice chair Lael Brainard explained that the long-standing “presumption that accommodation should be reduced preemptively when the unemployment rate nears its normal rate . . . may curtail progress for racial and ethnic groups that have faced systemic challenges in the labor force.” Such remarks suggest that the Fed may allow an overshoot of its average inflation target of 2 percent per annum to achieve its goals, including racial and ethnic progress. The size and duration of an overshoot that would be tolerated are unclear—such remarks leave room for a lot of discretion. However, such goals may explain why the Fed was reluctant to talk about tapering or raising interest rates despite the surge of inflation, low unemployment, and widespread worker shortages. Perhaps the Fed thought that there was still room for labor market conditions to improve.

Finally, there is an additional factor that could hinder the Fed’s inflation-fighting credibility: since the last financial crisis, the Fed has pursued policies to support asset prices and compress risk premia to boost consumption and the availability of credit. The results have been high asset prices, low interest rates even when economic growth has been relatively weak, and markets hypersensitive to upticks in policy rates.

As Luis Garicano, Jesus Saa-Requejo, and Tano Santos explained recently, this factor puts central banks, and the Fed in particular, “in a difficult position: they are holding the lion of financial stability by the jaws without being able to let go even when a second lion, inflation, may approach.”

Conclusion

It is hard to say whether inflation will continue to be high, but the probability that it will in the coming year is not negligible. At minimum, it is likely that the increase in prices produced by the most recent helicopter drops and accommodative monetary policy still has a way to go, given that trillions of dollars of extra savings remain unspent.

So far, the bond markets do not seem worried about inflation, as evidenced by the still-low interest rates. Whether they stay this way depends on what fiscal and monetary authorities do next. Will Congress continue to pass largely unfunded spending legislation? Will the Fed continue to print money to accommodate the spending? Will there be fiscal consolidation? These are important questions whose answers will decide whether people believe that (a) monetary authorities are willing to take the required steps to control inflation if needed and (b) fiscal authorities have a plan to pay down the debt. If people lose faith in both, their fear that the Fed will let inflation go to accommodate a growing debt in the future, especially in case of another emergency, could lead inflation to spiral out of control sooner than most people think. When that happens, given the growing restraints of political pressure, there will be little the Fed can do.