- | Monetary Policy Monetary Policy

- | Policy Briefs Policy Briefs

- |

Central Banks Are Inflation Creators, Not Inflation Fighters

Over the past 50 years, economists have spilled a lot of ink studying and debating periods of high inflation that began in the late 1960s, continued throughout the 1970s, and ended with the disinflation of the early 1980s. Although any particular contribution to the inflation debate of the 1970s often involved technical details about monetary policy and economic models, the debate was actually about something bigger and more fundamental. Who is responsible for inflation? Put differently, if one analogizes inflation to a fire, is the central bank the arsonist or the firefighter? The answer is that central banks are the arsonist. Central banks are inflation creators, not inflation fighters.

Unfortunately, even today, many economists do not seem to recognize that the debate was about these questions. Even many of those who now recognize that the Federal Reserve was able to bring about lower inflation in the early 1980s are prone to answer these questions incorrectly. They falsely attribute the disinflation to the Federal Reserve simply becoming a better inflation fighter. Now that the United States is experiencing the highest inflation rates of the past 40 years, it is important to revisit the lessons of these debates.

During the rising inflation of the late 1960s and the 1970s, monetarists argued that inflation is always and everywhere a monetary phenomenon. Inflation, according to the monetarists, was caused by an excess supply of money. By contrast, chair of the Board of Governors of the Federal Reserve System Arthur Burns and those of a similar mindset were convinced that inflation is caused by external, cost-push factors.

As early as 1970, Arthur Burns was arguing in speeches that “monetary and fiscal tools are inadequate for dealing with sources of price inflation such as are plaguing us now—that is, pressures on costs arising from excessive wage increases.” Allan Meltzer notes that Burns tended to blame inflation on labor unions and monopolies. As a result, Burns was convinced that monetary policy is not the most effective tool for reducing inflation. In fact, in a November 1970 entry in his diary, Burns writes:

What the boys that swarm around the White House fail to see is that the country now faces an entirely new problem—namely, a sizable inflation in the midst of recession; that classical remedies for fighting inflation or recession will simply not do; that new medicine is needed for the new illness.

That new medicine refers to wage and price controls.

If anything could summarize Arthur Burns’s tenure at the Federal Reserve, it was the mantra that “this time is different.” In 1971, Burns echoed the sentiment from his diary when he told the Joint Economic Committee that “the rules of economics are not working in quite the way they used to.”

Milton Friedman mockingly retorted that “whatever may be true about the economy, the propensity of economists to appeal to a change in our economic structure whenever they are puzzled works quite the way that it used to." He similarly noted that medicine that had been given to treat this illness worked exactly the way that an economist would expect. The problem was not that the illness was new, but rather than the patient had been given the wrong medicine.

Burns’s idea that inflation could not be reduced through monetary policy—or at least monetary policy alone—was ultimately proven wrong by the Volcker disinflation and the corresponding overhaul of Federal Reserve doctrine. Economist Robert Hetzel describes the change in monetary policy ushered in by Paul Volcker:

Under Volcker, as a result of a focus on expected inflation, the [Federal Open Market Committee] simply accepted responsibility for inflation without regard to its presumed origin as aggregate-demand or cost-push . . . . The desire to establish the credibility required to control expected inflation imposed overall consistency on monetary policy . . . . The demonstrated ability of monetary policy not only to control inflation but also to do so without periodic recourse to “high” unemployment gave credence to the idea that the central bank could control inflation through consistent application of policy thought of as a strategy.

In other words, the Federal Reserve accepted responsibility for inflation rather than viewing inflation as an external factor it needed to fight.

All of this is important because there has been a resurrection of Burns-type positions in the current debate about the cause of higher inflation rates. Senator Elizabeth Warren blames the rising inflation on greedy corporations raising their prices. Others have blamed rising prices on the greater prevalence of monopolies. Antitrust is apparently an anti-inflation tool.

Make no mistake, these ideas are wrong. A belief that greed is responsible for inflation requires a belief that firms waited 40 years to collectively and simultaneously raise prices—an amazing level of planning and discipline. In addition, no serious person believes that antitrust enforcement will bring about lower rates of inflation. More broadly, this argument is like the blaming of tariffs for higher prices. To the extent to that either of these arguments has merit, they confuse relative price changes, and possibly changes in the price level, with changes in the rate of inflation.

Regardless of these ideas’ weaknesses, the revitalization of these ideas is an indication that the important lesson from the 1970s might not have been learned. These arguments are part of a broader debate about the nature of monetary policy and inflation that spans decades. As Hetzel has repeatedly noted throughout his career studying monetary policy, the fundamental debates about inflation are really concerned with whether the central bank is an inflation creator or an inflation fighter.

The inflation-creator view entails that, if inflation is too high, it is because monetary policy is too loose. And if inflation is too low, it is because monetary policy is too tight. Some think about this in terms of the quantity theory of money: an excess supply of money causes inflation; an excess demand for money causes disinflation or even deflation. Others think about this in terms of interest rates: if inflation is high, it is because the central bank has set the bank policy rate below the natural rate (i.e., the rate that would prevail in a competitive market in a frictionless world); if inflation is low, it is because the central bank has set the bank policy rate above the natural rate.

According to the inflation-fighter view of central banking, the responsibility of monetary policymakers is to adequately respond to inflation. Those who see the central bank as an inflation fighter must therefore believe that inflation has some source other than the central bank, that it has nonmonetary factors. According to this view, economic shocks cause macroeconomic variables such as inflation to move around. The job of the central bank is to adjust its policy in response to these shocks.

These two views overlap somewhat. For example, people who see the central bank as the creator of inflation would acknowledge that many factors other than the money supply or the central bank’s policy rate affect the price level and inflation. However, they would argue that the extent to which these factors affect nominal variables is entirely determined by the central bank. In other words, those who advocate the inflation-creator view argue that any deviation of inflation from the target rate of inflation is a failure of the central bank. The failure might be active in the sense that the central bank increases or decreases the money supply too much relative to changes in money demand. Alternatively, the failure might be passive in the sense that the central bank fails to adjust its policy in response to market conditions, resulting in adverse outcomes. Either way, a central banker who pursues monetary policy that is expected to result in inflation above or below target should be fired.

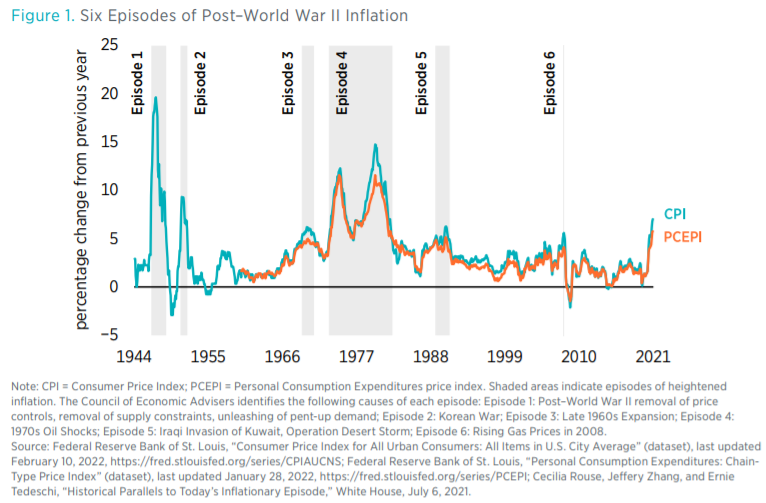

Thus, these two views differ not on the sources of the shocks that affect the macroeconomy; rather, they differ on whether deviations of inflation from the central bank’s target or from its long-term average are nonmonetary in nature and possibly beyond the control of the central bank. Those who view the central bank as an inflation fighter believe that inflation becomes high or low because something unexpected happened. This view is evident in figure 1, which is similar to a figure recently published by the president’s Council of Economic Advisers (CEA).

Figure 1 clearly articulates the inflation-fighter view of the central bank and demonstrates the CEA’s belief that external shocks explain fluctuations in the inflation rate. The COVID-19 lockdowns and reopenings are only the latest such shocks.

The problem with the CEA’s belief is that such figures are simply a plot with the time series of the inflation rate. An economist cannot assess the role of policy by simply looking at the time series evidence. Economists are interested in the counterfactual.

Counterfactuals are difficult. A counterfactual requires comparing what happened to what would have happened. Because one does not know what would have happened, one needs economic models, concepts, and analysis.

A prime example of the importance of counterfactuals is the concept of a monetary policy offset. This idea has been made popular in recent years by economist Scott Sumner. The idea is that central banks tend to respond to higher-than-expected inflation by tightening monetary policy. For example, suppose the government decides to embark on expansionary fiscal policy. All else equal, this policy would tend to increase aggregate demand. One would expect output and prices to rise. However, because the central bank would also expect output and prices to rise, it would tighten monetary policy to prevent prices from rising. The net result is that expansionary fiscal policy has little to no effect on economic activity and inflation when one looks at the time series. In other words, even if the marginal effect of fiscal policy is large, the contractionary monetary policy offsets those effects such that, upon casual inspection of the data, fiscal policy would appear not to matter.

This point is important. What one observes in the time series is what happened. One does not know what would have happened, and economists can offer guidance here. Wars are typical examples of expansionary fiscal policy. As a result, a central banker trying to maintain a particular rate of inflation would be expected to offset these expansionary effects. Two of the episodes shown in figure 1 involve wars, yet there is no evidence of monetary offset. One can blame inflation on these events only by admitting that the central bank failed to counteract these increases in demand and permitted prices to rise.

In looking at the period in figure 1 labeled “Episode 3” (late 1960s expansion), the CEA infers that inflation was caused by a booming economy. Again, this view assumes that inflation just sort of happens. There is a lot of economic activity, and so prices go up. But what is the source of this increase in economic activity? Introductory macroeconomics holds that supply-driven booms result in lower inflation whereas demand-driven booms result in higher inflation. Because monetary policy works through aggregate demand, this approach raises the question as to why this rising inflation brought about by the boom was beyond the Federal Reserve’s control.

Also, as figure 1 shows, the 1970s was a period of significant oil price shocks. However, supply shocks tend to reduce real economic output and increase prices. Thus, if the rising prices were really driven by supply shocks, such as sudden spikes in oil prices, then one would not expect to observe much of a change in the nominal value of economic activity (i.e., the product of real economic output and the price level). Yet the 1970s witnessed a higher average growth rate of nominal GDP. This growth rate indicates that monetary policy played a role in these high rates of inflation.

The CEA further points to higher gasoline prices in the period just before the Great Recession. However, it is unclear that these higher gasoline prices were driven by supply-side changes. Some evidence suggests that gasoline prices increased because of the economic growth experienced in many developing countries. It is unclear why an increase in the relative price of gasoline would be the cause of higher inflation. After all, there is a difference between accounting and economics.

Finally, figure 1 is notable for what it lacks. The dramatic reduction in inflation in the early 1980s was brought about by the Federal Reserve, led by Paul Volcker. The change in policy, as mentioned earlier, was that the Federal Reserve took responsibility for inflation and contracted monetary policy to bring about this disinflation.

Another detail missing from interpretations like that of the CEA is one of the most significant mistakes made in monetary policy in the postwar era. I am referring to the dramatic decline in the money supply that resulted in a short period of deflation in 2008.

The Volcker policy change and the deflation of 2008 bookend a long period of a low, stable inflation. Figure 1 leaves one with the impression that this period was simply a quarter-century of good luck for the central bank.

Whether it is this explicit intention or not, figures like figure 1 are meant to communicate the idea that the central bank is an inflation fighter; that inflation occurs for reasons that have little or nothing to do with the actions of the central bank; and that monetary policymakers do the best they can, but these external factors can cause significant deviations of inflation from what the central bank would prefer. In addition, this view even suggests that monetary policy might be ill-equipped to deal with particular causes of inflation. This suggestion opens the door to all sorts of alternative policy responses, many of which have been historical failures.

The lesson of the 1970s and the subsequent disinflation of the early 1980s favors the inflation-creator view of central banks. Although some might argue that the Federal Reserve simply improved at fighting inflation, this conclusion is refuted by the evidence. This argument is certainly made by some economists, such as Richard Clarida, Jordi Galí, and Mark Gertler. They estimate monetary feedback rules that measure the responsiveness of the Federal Reserve’s intermediate target—the federal funds rate—to inflation and the output gap. They find that the Federal Reserve was much more responsive to inflation in the post-Volcker era. In addition, they use a theoretical model to show that their estimates for the pre-Volcker period result in a world of multiple equilibria. However, the flaw in their analysis is that they are using the data that are available today to evaluate these periods. To properly analyze policy using this method, one needs to use the data that were available to the Federal Reserve at the time the decisions were made. Athanasios Orphanides performs this sort of analysis and shows that the responsiveness of the Federal Reserve’s intermediate target to inflation during the pre-Volcker period was not much different than that of the post-Volcker period. Thus, it cannot simply be that the Federal Reserve was a better inflation fighter after the 1970s.

By contrast, the inflation-creator view, most notably advocated by monetarists, is that the central bank is the cause of inflation and that high inflation rates can be brought down with tighter monetary policy in the form of a reduction in the growth rate of the money supply. They were frequently told they were wrong—that inflation was different this time, that the normal tools would not work, that monopolies and labor unions and oil cartels were to blame. Yet, when Paul Volcker took over as chair of the Federal Reserve’s board of governors, he explicitly placed responsibility for creating inflation on the Federal Reserve. Contractionary monetary policy, as evident in the significant declines in the growth of the money supply, brought down the rate of inflation. The dire predictions of the critics failed to materialize, and discussion of the role of unions and monopolists in the inflation process largely disappeared.

Low, stable rates of inflation continued over the next quarter-century. This stability was not due simply to luck. It also was not due to the Federal Reserve getting better at fighting inflation. Instead, the evidence suggests that the stability over this quarter-century was due to the change in Federal Reserve doctrine brought about by Volcker and the acceptance of the view that the central bank is the inflation creator.

Despite this evidence, the old inflation-fighter arguments are beginning to reemerge, which is why it is important to recall the lessons from these old debates. Central banks are not passive observers of inflation that just do their best to keep it in check. Central banks are the source of inflation. As such, the responsibility for maintaining low, stable rates of inflation is theirs.