- | Monetary Policy Monetary Policy

- | Policy Briefs Policy Briefs

- |

What Would Milton Friedman Say about the Fed’s New Framework?

This policy brief is part of a Mercatus Symposium titled “What Would Milton Friedman Say?” The symposium explores what the late Nobel laureate, economist Milton Friedman, might say about monetary policy today, as the Federal Reserve grapples with increasing inflation in the wake of the COVID-19 pandemic.

Prior to August 2020, the Federal Reserve (Fed) had a flexible 2 percent inflation target. This meant that the Fed attempted to achieve 2 percent inflation each year without consideration of previous misses to that target. The target was called flexible, as opposed to strict, because it left open the possibility that the Fed could temporarily deviate from it to stabilize unemployment. A strict inflation target would require that the Fed focus only on inflation. Arguably, flexible inflation targeting was more appropriate given the Fed’s mandate to promote price stability as well as full employment.

After years of generally undershooting the 2 percent target, in August 2020, Fed chair Jerome Powell announced the Fed’s transition to a “flexible average inflation targeting” (FAIT or AIT) framework where the Fed would aim to achieve 2 percent inflation over time. Under FAIT, the Fed factors previous undershoots or overshoots into its decisions to achieve 2 percent inflation on average. Powell also clarified that since the framework is flexible, average inflation is not defined by a mathematical formula. Rather, the Federal Open Market Committee (FOMC) retains some discretion in what it considers to be average inflation, and as in the case of the previous framework, it could deviate from its inflation target to achieve its employment target. Ironically, although this framework was developed in the context of low inflation and announced shortly after a period of brief deflation in 2020, inflation then rose unexpectedly to rates not seen in decades in 2021.

What would Milton Friedman, the great monetarist economist, say about this framework?

Before answering that question, this essay addresses what framework Friedman would most favor today. Although we cannot know for sure, Friedman would have strong reason to support a nominal GDP level target (NGDPLT) where the Fed would stabilize the volume of total dollar spending or nominal income. An NGDPLT is a velocity-adjusted money supply target, which can be thought of as a modern version of the Friedman’s constant “k-percent” money growth rule.

The essay then argues that Friedman would think of FAIT as a “mixed bag.” Even though a policy of making up for past misses is desirable, he would likely be critical of the discretion the Fed retains under FAIT. The Fed justifies the discretionary character of FAIT by arguing discretion is needed to fulfill its entire mandate.

One way for the Fed to make FAIT more rules based, while also retaining the ability to fulfill its mandate more easily, would be for the Fed to explicitly embrace former Fed vice chair Richard Clarida’s description of the new framework as a temporary price-level target (TPLT). Under a TPLT, the Fed would stabilize the price level rather than inflation, the growth of the price level, but only when interest rates are at the zero lower bound (ZLB). Outside of the ZLB, the Fed engages in flexible inflation targeting. In two important respects, a TPLT behaves similarly to an NGDPLT. First, both allow for level targeting at the ZLB. Second, both allow for the Fed to not react to negative supply shocks, which raise inflation, but also unemployment. Insofar as FAIT approaches TPLT, which itself approaches NGDPLT, Friedman would argue that FAIT could be a step in the right direction toward a more ideal policy.

FRIEDMAN AND THE K-PERCENT RULE

Friedman is closely associated with monetarism, the school of thought that emphasizes the role of money in business cycles. Although money can affect real variables, including unemployment and output in the short run, it affects only nominal variables, including inflation and nominal income in the long run. Put differently, money is nonneutral in the short run and neutral in the long run. Friedman bolstered the case for monetarism with what is perhaps his most famous work, A Monetary History of the United States: 1867–1960, coauthored with Anna J. Schwartz. In A Monetary History, Friedman and Schwartz showed empirically that changes in the US money supply led to changes in other macroeconomic variables. The most famous chapter of their book argues that a collapse in the money supply precipitated the Great Depression.

Throughout his career as an economist and public intellectual, Friedman criticized central bank discretion and preferred rules to constrain central bank behavior. Although he argued price stability should be a central bank’s ultimate goal, monetary policy affected other variables with “long and variable lags.” Fallible central bankers, faced with uncertainty about the future and operating with imperfect information, would be more likely to destabilize the economy rather than stabilize it if they attempted to target the price level, a variable beyond their control. Instead of trying to target the price level, a central bank should target money supply growth as an intermediate goal.

Friedman’s preference was to target the M2 money supply (currency, demand deposits, savings deposits, money market funds, and small-time deposits) at a growth rate of 3–5 percent. Take the famous equation of exchange

MV= PY,

where M is the nominal money stock; V is the velocity of money or the rate at which money is exchanged; P is the price level, measured by a price index such as the Consumer Price Index; and Y is real output (usually measured as real GDP). Both sides of the equation equal nominal income (usually measured as nominal GDP). We can also take the dynamic form of this equation where each variable is in growth rates:

m + v = p + y,

where m is the growth of money, v is the growth of velocity, p is the growth of the price level (inflation), and y is the growth of real output.

If m and v are stable, then the growth of nominal GDP is also stable. Friedman understood that velocity was not perfectly stable and that stable money growth was not a theoretical ideal. Despite this, he argued constant money growth was the best a central bank could do.

By the late 1960s, money growth had become quite high, and for the next decade, money growth and inflation both rose significantly. In October 1979, Fed chair Paul Volcker announced changes in policy to target the growth of the M1 money supply. This initially seemed to be a major victory for monetarists, including Friedman, who called the change “long overdue.”

This change in policy was subsequently dubbed the “monetarist experiment.” Interest rates rose dramatically, and two recessions took place during this period. By October 1982, the Volcker Fed officially ended its money supply targeting policy. The “experiment” had largely succeeded at bringing down inflation but had come at a high cost. Friedman argued that the Fed had not truly followed monetarist principles, and if it had, the economic downturn would have been less severe. Nevertheless, the experience dampened enthusiasm for money supply targeting.

Subsequent academic research showed that although the velocity had been somewhat stable prior to 1979, it became more unstable afterward. Money’s relationship with output and inflation weakened, and targeting an aggregate such as M1 or M2 made less sense. By the 1990s, many central banks relied on a short-term interest rate as the primary means of implementing policy and were either explicitly or implicitly targeting inflation.

As time went on, Friedman conceded that the case for money supply targeting had weakened. In a 1999 interview, he acknowledged that the Fed under Chair Alan Greenspan had done a good job in producing mild inflation even as M2 growth had grown at rates higher than 5 percent. Later, while not fully renouncing the case for monetary rules, he stated that discretion under Greenspan worked better than he previously thought possible. In a 2003 op-ed, he observed that inflationtargeting success was not limited to the United States as the central banks of the United Kingdom, Sweden, New Zealand, Australia, and others had all achieved mild inflation.

FRIEDMAN AND NOMINAL GDP–LEVEL TARGETING

Friedman’s main reason for supporting an instrumental rule (the k-percent rule) over an inflation target was the existence of lags in policy. By the 2000s, he conceded that many central banks had done a relatively good job in overcoming the problems posed by lags. Since Friedman had made relative peace with the idea of a central bank stabilizing a variable outside its immediate control, it is worth considering whether he would support a target other than inflation—nominal GDP.

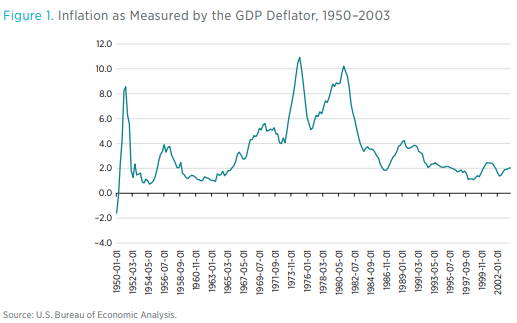

In the 2003 op-ed mentioned above, Friedman provided a graph of inflation in the United States from 1950 to 2003, similar to figure 1. Prior to the mid-1980s, inflation fluctuated like the “temperature in room without a thermostat in a location with very variable climate.” Afterward, “it is like the temperature in the same room but with a reasonably good though not perfect thermostat, and one that is set to a gradually declining temperature.”

Invoking the equation of exchange, Friedman went on to compare a good central bank to a thermostat. Just like a thermostat keeps the temperature of a room stable, the Fed “must adjust the quantity of money in order to offset changes in velocity and output” to keep prices stable.

In this example, the central bank adjusts M to keep P stable. But what about targeting PY or nominal income target? Although Friedman never publicly endorsed nominal income targeting, there are a few reasons why Friedman might support the idea today. First, as Michael Woodford has observed, a nominal GDP target is a velocity-adjusted money supply target and can thus be thought of as a modern k-percent rule.11 Unstable velocity had made the original k-percent unworkable, so it is not a stretch to imagine Friedman supporting a money growth rule aimed at overcoming this challenge.

Second, nominal GDP is a simpler variable to target than inflation. Using the equation of exchange, targeting P requires adjusting M in response to changes both in V and Y. Changes in Y are supply shocks. Although Friedman acknowledged relative central bank success in this regard, this requires a great deal of knowledge about the entire real economy.

Targeting PY only requires adjusting M in response to changes in V. The Fed’s “thermostat” would respond to only one variable rather than two. Like an inflation-targeting central bank, a nominal GDP–targeting central bank faces a difficult task in forecasting macroeconomic variables, but unlike an inflation-targeting central bank, a nominal GDP–targeting bank does not respond to supply shocks (changes in Y). Rather, it allows P to fluctuate in response to changes in Y.

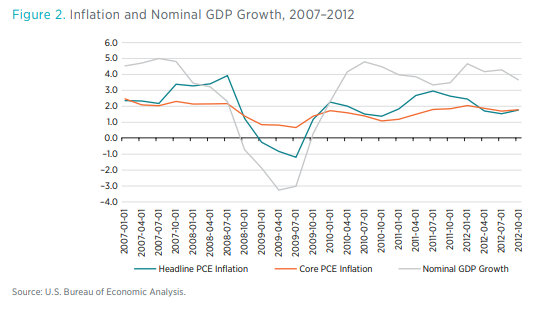

Empirical evidence shows this “knowledge problem” facing inflation-targeting central banks is very real. Figure 2 shows annual inflation as measured by both the headline personal consumption expenditures (PCE) index and the core PCE index as well as nominal GDP growth from Q1:2007 to Q4:2012. In 2008, negative supply shocks caused oil and other commodity prices to rise, which explains the rise in the headline PCE index through the third quarter of that year. The core PCE inflation rate, which does not include volatile energy prices, stayed mostly steady through this period. Given that inflation was rising by one metric and steady by the other, an inflation-targeting bank would not have a reason to loosen policy. Indeed, the Fed was very hesitant to cut the federal funds rate throughout 2008 because of inflation. By contrast, nominal GDP growth had been falling since the third quarter of 2007 and fell sharply in the third quarter of 2008. If the Fed had been targeting nominal GDP in 2008, it would have pursued a more expansionary policy, beginning earlier that year. Since households’ and firms’ economic decisions are based on their expectations of the future, a strong signal from the Fed that it was committed to keeping nominal GDP stable would have likely boosted the public’s confidence about economic recovery and mitigated the Great Recession.

Third, nominal GDP targeting offers a more rules-based approach to achieving macroeconomic stability and the Fed’s dual mandate than inflation targeting. Strict inflation targeting requires that the Fed achieve 2 percent inflation either on an annual basis (simple inflation targeting) or according to a mathematical average (average inflation targeting). This means responding to changes in the inflation rate from transitory supply shocks such as the 2008 commodity shock and the more recent 2021–2022 supply shortages. Since negative supply shocks push up prices and adversely affect the real economy, including the labor market, tightening monetary policy in response to such shock worsens the real economy further.

The Fed understands this challenge and did not immediately tighten policy in 2021 because much of the inflation could be attributed to supply shortages. The supply shock problem is a reason why the Fed prefers the more discretionary, flexible approach to inflation. Under flexible targeting, the Fed can make choices about when to deviate from the target. A nominal GDP–targeting central bank does not need to use discretion in this instance because it allows the price level to rise in response to supply shocks by construction. Nominal GDP targeting also requires no judgments about the level of full employment in the economy.

Friedman was critical of central bank discretion because he believed central bank errors would be destabilizing. Since less knowledge is required on the part of a nominal GDP–targeting central bank than an inflation-targeting one, Friedman would have strong reason to support the former over the latter.

FLEXIBLE AVERAGE INFLATION TARGETING AS A STEP TOWARD NGDPLT?

This section argues that the new FAIT framework is similar to NGDPLT in two important respects:

- Both allow for level targeting at the ZLB.

- Both allow for the Fed to “see through” or not react to negative supply shocks.

When Chair Jerome Powell announced the transition to FAIT, he explained that the FOMC would not be tied down to a particular formula defining average and that instead, its decisions would be based on “a broad array of considerations.” If there was a strict average, the recent high inflation, which is much higher than 2 percent, would mean that the Fed would have to target below 2 percent inflation for the near future. Rather, statements from Fed officials and the Fed’s inflation projections suggests that the Fed does not expect below 2 percent inflation in the future.

In a series of speeches, former Fed vice chair Richard Clarida compared FAIT to temporary pricelevel targeting (TPTL), an idea developed by Ben Bernanke and others. Under TPTL as described by Bernanke, a central bank engages in price-level targeting (PLT) only when its target interest rate is at the ZLB; when interest rates are positive, it engages in flexible inflation targeting. Moreover, Bernanke has stated:

"A temporary price-level target, unlike an ordinary price-level target, would not require the Fed to tighten policy to reverse shocks that temporarily drive up inflation when rates are away from the ZLB."

Clarida has described FAIT in similar terms:

"The new framework is asymmetric. That is . . . the goal of monetary policy after lifting off from the [ZLB] is to return inflation to its 2 percent longer-run goal, but not to push inflation below 2 percent. In other words, after liftoff from the [effective lower bound], monetary policy reverts to simple flexible inflation targeting."

PLT is similar to AIT in that the central bank makes up for past misses to its target. In the long run, the price levels under PLT and AIT should be very similar. Both struggle with the challenge of supply shocks affecting the price level. PLT is different from AIT in that under the former, the central bank targets a level path dating back to when the target began; under AIT, the central bank considers undershoots or overshoots only for a given period.

Why does Bernanke’s TPLT only kick in at the ZLB? Interest rates tend to be at the ZLB when the economy contracts and when inflation is below target. Assuming that the central bank cannot implement a negative interest rate policy, it can no longer reduce its target nominal interest rate. The Great Recession and the brief but severe 2020 COVID-19 recession are good examples of this. Since inflation is likely to be below target at the ZLB, the central bank achieves above-target inflation to get the prices back to its level path. At this point, the central bank reduces real interest rates by raising inflation expectations.

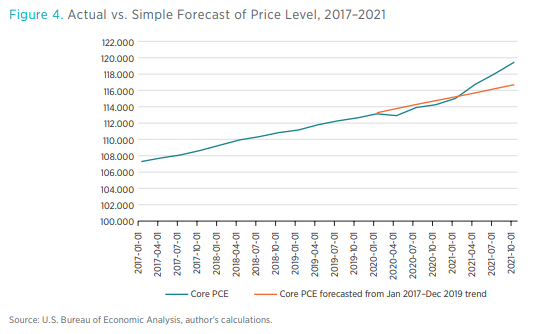

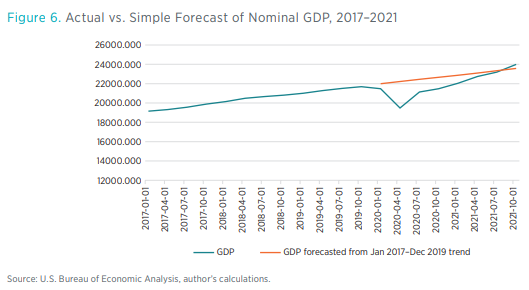

Figures 3 and 4 show the PCE index for the Great Recession and 2020 recession, respectively. They also show how the PCE performed relative to a simple forecasted trendline. Figure 3 shows that prices did not recover and get back to trend in the aftermath of the Great Recession. By contrast, figure 4 prices did recover in the aftermath of the COVID-19 recession and even went above trend. The recovery from the COVID-19 recession is an example where the Fed better approximated TPLT.

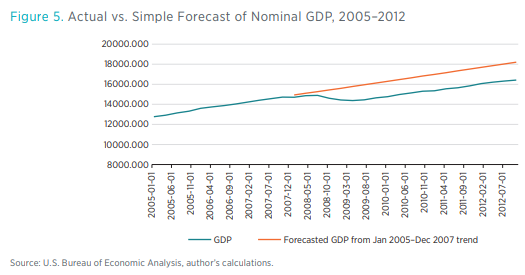

At the ZLB, a PLT and an NGDPLT behave similarly because inflation and nominal GDP growth tend to be very low. In both cases, the central bank needs to pursue a more expansionary policy to make up for the previous misses. Figures 5 and 6 show nominal GDP and the same simple forecasted trendline for the same periods in Figures 3 and 4. In the Great Recession, nominal GDP fell and did not return to trend. By contrast, nominal GDP has somewhat overshot its previous trend in the aftermath of the COVID-19 recession. Noticeably, as of Q4:2021, figure 4 shows that prices have overshot their previous trendline by approximately 2.36 percent, while figure 6 shows that nominal GDP has exceeded its previous trendline by a more modest 1.76 percent.

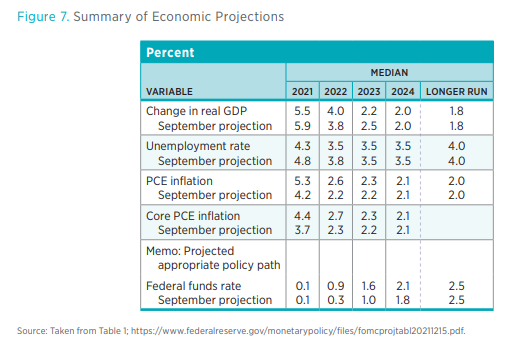

After their December 2021 meeting, the FOMC released its latest Summary of Economic Projections (SEP) for where different variables would be over the next several years. The median projections from the SEP are presented in figure 7. The FOMC estimates that PCE inflation will fall to 2.6 percent in 2022, 2.3 percent in 2023, and 2.1 percent in 2024.

Since inflation in 2021 was much higher than 2 percent, strict AIT as well as a strict PLT would require that the Fed aim for inflation lower than 2 percent over the next several years. However, it is clear from the projections that the Fed is not planning on this.

Rather, the Fed appears to be embracing Clarida’s description of FAIT, which is comparable to Bernanke’s TPLT proposal. The substantially higher than 2 percent inflation in 2021 reflects a combination of making up for sub–2 percent inflation in 2020 plus higher prices from the 2021– 2022 supply shortages. The projected inflation in 2022 onward suggests that the Fed is “seeing through” higher inflation brought on by transitory supply-side factors as it aims to ultimately bring inflation back to 2 percent but not below it.

Clarida’s description is also consistent with the “2020 Statement on Longer-Run Goals and Monetary Policy Strategy,” which the FOMC published as it transitioned to FAIT. Part of the statement reads:

"The Committee’s employment and inflation objectives are generally complementary. However, under circumstances in which the Committee judges that the objectives are not complementary, it takes into account the employment shortfalls and inflation deviations and the potentially different time horizons over which employment and inflation are projected to return to levels judged consistent with its mandate."

Although this statement leaves room for discretion, it suggests that the FOMC would not tighten policy if employment is below its full level even if inflation is above target. A negative supply shock is an important example of such a scenario.

The negative supply shocks reflect both an important advantage and disadvantage of FAIT. On the one hand, the “flexible” part of FAIT allows the Fed to not respond to adverse, negative supply shocks and thus avoiding unnecessarily harming the economy. On the other hand, FAIT makes Fed policy more discretionary and less predictable.

The Fed would not be facing this tradeoff under NGDPLT because it would simply not have to worry about changes in inflation due to supply shocks. As figures 4 and 6 indicate, the Fed’s response to the COVID-19 pandemic has been more like a nominal GDP–level-targeting central bank than an inflation-targeting or even Clarida’s TPLT central bank. Moreover, although nominal GDP has overshot its prepandemic trend, its overshoot has been less acute that the overshoot in the price level. Bringing nominal GDP back to trend requires less tightening than bringing prices or inflation back to trend does. If the Fed is concerned that a tighter policy could result in recession, then it should view NGDPLT as a more attractive option.

This begs the question, why did the Fed opt for FAIT over NGDPLT in 2020? Although the Fed has not explicitly articulated why it made this decision, there are a few possible reasons. First, central banks tend to change policies gradually. Like other central banks, the Fed had experience implementing and communicating inflation targeting. Transitioning from simple inflation targeting to average inflation targeting was a smaller step than transitioning from simple inflation targeting to NGDPLT.

Second, FAIT was developed and announced in the context of low inflation and even briefly, deflation. After the Great Recession, the Fed and most other central banks of developed countries had struggled for years to achieve 2 percent inflation. FAIT would have been a welcome development during the Great Recession. During that crisis, the Fed failed to pursue a monetary policy expansionary enough for prices and nominal spending to revert to their pre-recession trends. The result was a very sluggish recovery. Had the Fed pursued a makeup policy such as FAIT, prices would have rebounded faster, and recovery would likely have been faster. Since no major negative supply shocks occurred after the Great Recession had ended, it is unlikely that an average inflationtargeting Fed would have been confronted with the high prices that it presently faces.

Today, the Fed faces very different conditions. In 2020, the Fed responded rapidly to the pandemic and announced FAIT as a sign that it would tolerate slightly higher inflation to make up for previous sub–2 percent inflation. The economic recovery from the 2020 recession was much swifter than the recovery from the Great Recession, and the Fed’s much more robust response appeared to have played a decisive role. However, developments then took place that the Fed did not anticipate: a combination of strong aggregate demand and supply shortages causing inflation to surge to rates not seen in decades. FAIT was designed as a response to a long period of low inflation, but soon after its arrival, inflation became quite high.

This awkward timing for FAIT can be attributed to the highly unusual nature of the COVID-19 pandemic. Nevertheless, the pandemic has shown that supply shocks are a major complication for any sort of inflation-targeting central bank.

CONCLUSION

It is unclear when the COVID-19 pandemic will be fully over, and high inflation is likely to con - tinue into 2022. Therefore, we cannot give a final verdict on the Fed’s overall pandemic perfor - mance. The Fed’s challenge now is to tighten policy in the face of rising inflation without causing a recession.

Given that Milton Friedman believed that monetary policy can substantively affect real variables, including output and unemployment in the short run, one can suspect Friedman would praise the Fed in pursuing a policy expansionary enough to support economic recovery after the steep 2020 recession. At the same time, one can suspect he would fear that the Fed has “overdone it” and that he would be quite concerned about the current inflation. He would likely stress the importance of a rules-based framework getting inflation under control. One way for the Fed to set policy in a way that controls inflation without also prompting a recession is for it to adopt a nominal GDP level or velocity-adjusted money supply targeting rule.

Some economists, including former Fed vice chair Clarida, have compared the FAIT framework to a TPLT. A TPLT is a “close cousin” of a nominal GDP–level target. If the Fed is unlikely to adopt a nominal GDP target, then a TPLT is a next-best option for policy. Since a TPLT has a fairly welldefined meaning, the Fed can make FAIT more rules based by explicitly adopting TPLT.

Citations and endnotes are not included in the web version of this product. For complete citations and endnotes, please refer to the downloadable PDF at the top of the webpage.