- | Government Spending Government Spending

- | Data Visualizations Data Visualizations

- |

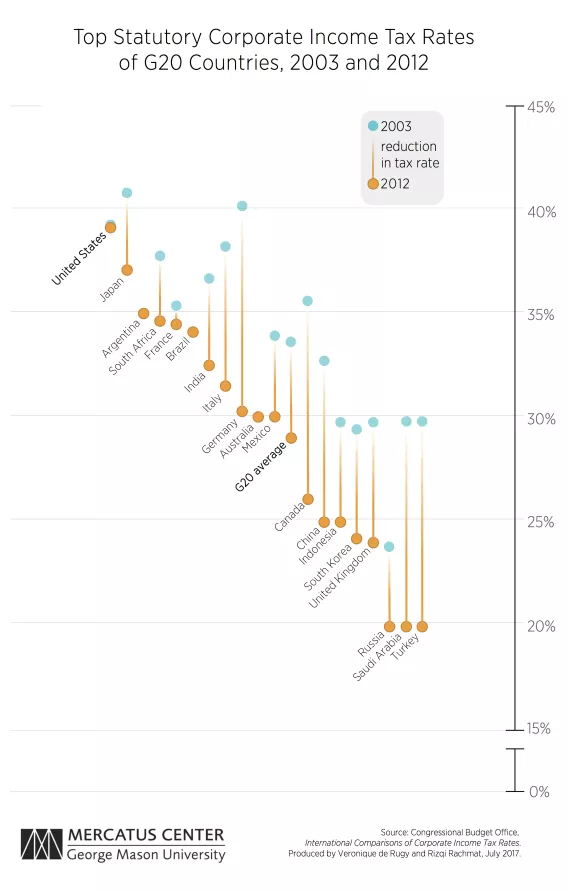

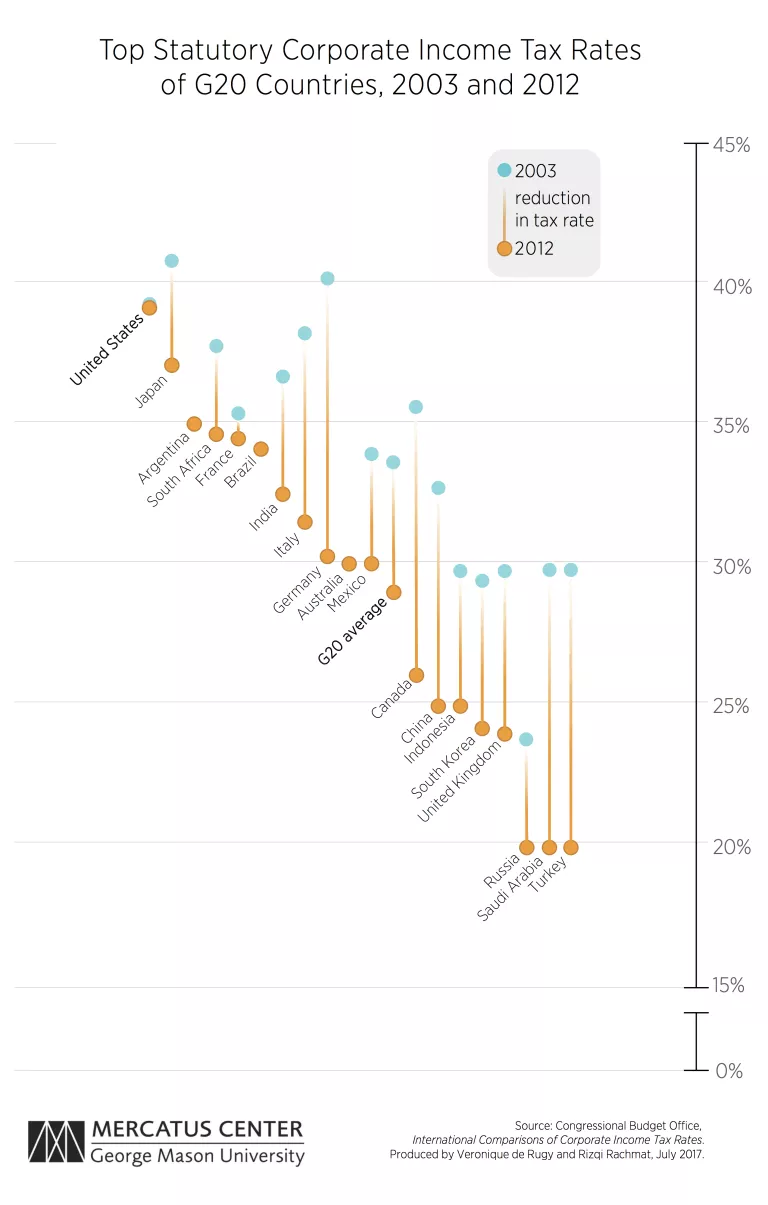

Reforming US Corporate Taxes

The United States has fallen far behind other developed countries when it comes to corporate tax reform. In contrast to other developed nations, the United States has declined to reform the way it taxes corporations. Consequently, it now has the highest statutory corporate income tax rate of the G20 countries. The federal government needs to lower the corporate income tax rate—a reform that will improve the competitiveness of American businesses and encourage economic growth.

The case of Japan is particularly interesting. In 2003, Japan held the record for the highest corporate income tax rate in the G20. During the course of several tax reforms, the country cut its corporate tax rate. As a result, in 2012 the Japanese rate stood at 37 percent. Today, it is down to 32.11 percent, and there is a plan in place to lower it further soon.

The United States should learn from the experience of Germany and Japan and many other countries that have reduced their corporate income tax rates and moved to a territorial system. They have gained in competitiveness and the reforms have promoted economic growth and increased companies’ incentives to invest in their countries.