- | Regulation Regulation

- | Policy Briefs Policy Briefs

- |

The Economic Situation: December 2025

Amid inflation, trade shifts, and rapid advances in AI, the US economy is learning to produce more with less

Getting Started: A Forecast and a Confession

With December upon us and the year about over, I begin this quarter’s report with a summary forecast for the next four quarters. Details will be provided later. Based on the GDP forecasters I follow, my assessment of inflation data, two interest rate cuts by the Fed, and other forces at play in the economy, I expect we will see 2 percent real GDP growth across the next 12 months, with inflation running 2.75 percent annually and the 10-year bond yielding between 4.0 to 4.2 percent. Productivity gains from growing AI activity will help offset slow growth in employment.

Now, for a confession. Like many economy observers, I’ve struggled this year to find a theoretical framework that explains the many swoops and turns we have experienced while riding the US 2025 policy roller coaster. Handicapped, perhaps, by habits of thought that assume government acts within traditional fences formed by seldom-tested constitutional limits and customs of political behavior conditioned by civil conduct, I’ve had difficulty analyzing this year’s “no holds barred” way of life.

I am also affected by several years of Washington experiences where federal government leaders, for the most part, seemed to see themselves as accommodating the operation of a beneficial free market rather than seeing government as the major player in a top-down state-assisted capitalist system.

There were obvious exceptions, but my experience and predispositions regarding political behavior apparently do not fit a situation where countries worldwide are reorganizing in the aftermath of a severe global pandemic that killed millions and major wars and political revolutions that split countless families and sent millions of refugees searching for safety.

Then, to top it off, global markets are reorganizing as they react to revolutionary changes in AI-inspired knowledge technologies. As Nobel Laureate Friedrich Hayek reminded us decades ago, the economic problem is fundamentally a knowledge problem: Knowledge is diffused across billions of individuals, while the need for knowledge to act is concentrated. With AI, the cost of accessing all those brains is plummeting.

As I see things now, these changes have led nations worldwide to hunker down, centralize decision-making, increase regulation, and print money to ease the pain of change. Inflation and revolution have followed. Coming out of all this are social movements marked by populism wrapped in a heavy cloak of nationalism. But Hayek also reminded us of the fatal conceit that causes people in power to think they can assemble the brightest and best minds and, armed with reports, studies, and information, proceed to outthink and outperform what decentralized, free-market forces can provide.

For example, it may be easy for presidents to predict the direct effect of actions to control prices or limit imports, but impossible to anticipate the unseen indirect effects that can be confounding.

But why did Hayek warn that the effort might be fatal? Fatal to freedom and prosperity. This was his concern.

Looking for the effects

The effects of centralized decision-making and increased regulation may be seen in the recently released Fraser Institute 2025 report on Economic Freedom of the World. Fraser’s freedom index rates up to 165 jurisdictions from 1970 through 2023 according to five data categories: size of government, legal system and property rights, sound money, freedom to trade internationally, and regulation. When COVID hit, each of the five categories was affected by national governments to soften the pandemic’s effects. For the years 2000 through 2023, data for the average value of the overall index, unweighted and weighted by population, are shown in figure 1 below. I call attention to the sharp decline that started in 2019 with a small recovery in 2023. In effect, it seems, 10 years of gains in freedom were erased by pandemic and related effects. I note that the top five free countries for 2023 are Hong Kong, Singapore, New Zealand, Switzerland, and the United States.

Debt and diminishing prosperity

The second Trump administration has taken a host of top-down actions to get the economy running the way the administration wants. While building both visible and invisible walls along our borders, the Trump team has sought to accelerate deportations of undocumented immigrants, which includes lots of working-age people; engage in on-again, off-again tariff-based conflicts with trade partners; take on major universities over personnel policies; engage large cities over crime; and take punitive actions against countries that permit drug smugglers to export to America. To make matters more challenging for those who seek to find patterns for understanding all this, examination of other industrialized countries reveals similar chaos and policy uncertainty. In other words, the world we seek to understand can’t be explained as just a matter of American Democrats and Republicans at war with each other.

Needless to say, there have been no dull moments. While never reluctant to employ lawyers to test the limits of action, President Trump has proven to be an expert at making unexpected changes in industrial policy, trade agreements, agency shutdowns, and government-employee layoffs. As though looking for a way to end the nation’s deficit habit but without saying so, he has shown himself to be a wizard in extracting payments from those who wish to export to America, migrate to America, or build factories in America. This contributes to investment-limiting economic policy uncertainty. When Trump was sworn into office in January 2025, the monthly Economic Policy Uncertainty Index stood at 64.1. For several years before that, the index bounced in a range of 100 to 140. In April, the month Trump announced his trade war plans, the index rose to 561, the highest value since the index’s 1985 inception. In October it rested at 202.

Now, for the first time in several years, the Secretary of the Treasury as reported by the Congressional Budget Office (CBO) has curtailed growth in the federal deficit and perhaps put a lid on growth in the interest cost of the debt, which now exceeds the annual cost of defense. On September 30, the end of FY 2025, the deficit stood at $1.8 trillion for the second year hand running.

The interest cost of the debt for the year stood at $1.22 trillion, up a bit from $1.13 trillion in FY 2024 and a lot from $0.56 trillion in FY 2021. (The president’s 2026 base defense budget request is for $892.6 billion.) In just four years, the interest cost more than doubled. This means the United States is violating Ferguson’s law (named after its 18th century originator, Adam Ferguson) that says a nation that spends more on debt than defense runs a high risk of being taken over by another country.

What about GDP?

The Treasury’s latest numbers indicate the average interest rate on outstanding debt to be 3.36 percent. Real GDP growth for 2025’s first two quarters was -0.6 percent and 3.8 percent, respectively, giving an average of 1.6 percent, and the prospects for the next 12 months are weak. When the growth rate of debt exceeds the growth rate of GDP, the nation becomes poorer.

On this, I note that GDP forecasters I follow have modified their outlook relative to what we saw last quarter. Near-term growth prospects have been revised upward, and minor changes have been made for 2026. There is still no indication of a recession — two consecutive quarters of negative growth — for the next 12 months. In Table 1, I report estimates provided by the Philadelphia Fed’s panel, The Wall Street Journal, and Wells Fargo Economics. I note that the International Monetary Fund also gave a positive nudge to its estimate for 2025 and 2026 US GDP growth, raising 1.9 percent to 2.0 for 2025 and 2.1 for 2026.

In the absence of data on GDP growth for the third quarter, which will be late because of the recent shutdown, I note that the October Purchasing Manager’s Index shows US manufacturing output increasing for nine months hand running. Thus, employment growth in services and manufacturing output data are promising at least a moderate, around 3 percent GDP growth for the third quarter.

Employment growth across the states

Year-over-year the US Bureau of Labor Statistics (BLS) state employment growth data for 2025’s first quarter (figure 2) show 11 states where employment is falling. This is up from three negative-growth states in the previous quarter and none before that. In short, America’s employment situation is systematically weakening. According to his calculations, Mark Zandi, chief economist at Moody’s Analytics, finds that 22 states are now in a recession.

He identifies the vulnerable ones as “any state that has an economy that centers on goods-producing activities, agriculture, light manufacturing or mining.” As seen in figure 3 below, employment growth in manufacturing shows the weaker part of the story: Just seven states showed growth in 2025’s first quarter.

Given deportations and an aging population, US employment growth is now falling. Estimates by the Pew Research Center indicate 750,000 immigrant workers have left the labor force since January 2025, and efforts by the Trump administration to ease the situation by accelerating use of a special visa for temporary agriculture workers have been snarled by the government shutdown.

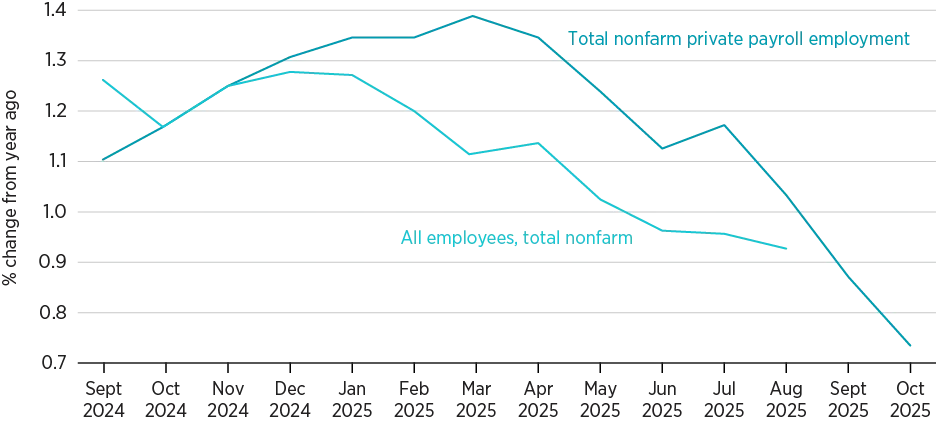

Figure 4 below shows growth in private payrolls using BLS (green) and Automatic Data Processing (ADP) (blue) data. I note that the abbreviated BLS is due to the government shutdown. The blue ADP line suggests employment growth is headed toward zero, implying that GDP growth will be determined largely by growth in productivity. Part of the weaker employment growth is explained by expanded use of AI across firms and industries. According to the Federal Reserve Bank of San Francisco, recent college graduates will likely be the hardest hit labor-market component, since they are generally entry-level hires who are more easily replaced by AI. Currently, the unemployment rate of recent graduates is rising.

FIGURE 4. US employment growth, September 2024–October 2025

Source: Automatic Data Processing, Inc.; US Bureau of Labor Statistics via FRED®.

What about inflation?

Turning to inflation, we see that September data showed the all-item Consumer Price Index (CPI) rising 3 percent on a year-over-year basis, the highest rate since January but the slowest in three months and slightly below some expectations. Gasoline at the pump and food at home were significant contributors, but upward price pressure was widespread. The report offered small comfort to consumers or to the Fed in its interest rate decision struggles. Higher inflation expectations were also confirmed in the New York Fed’s September Survey of Consumer Expectations, where 3.4 percent is the expected short-term pace and 3 percent the longer five-year horizon.

The White House press secretary’s reaction to the CPI was interesting, to say the least: “Today’s new Consumer Price Index reveals inflation smashed market expectations once again in September — with prices holding steady and wages beating inflation as President Donald J. Trump ushers America into a new Golden Age.” It is amazing to see 3 percent inflation being celebrated as “steady” and a part of the Golden Age. There was a time back in February when the White House was condemning 3 percent inflation as an unfortunate situation caused by the Biden administration. That reminds me of Garrison Keillor’s Lake Wobegon, “where all the women are strong, all the men are good looking, and all the children are above average.”

Welcome to the Golden Age!

How the report is organized

The report has three remaining sections, including two book reviews. The next section focuses on the Trump Administration’s actions that affect labor markets, actions that include accelerated deportations by Immigration and Customs Enforcement and new H-1B visa rules for hiring foreign-born scientists and mathematicians. The section that follows looks more closely at evolving and, I might add, constantly changing trade policy. The topics covered include pay-to-play capitalism, industrial policy that includes government investment in various US-bound enterprises, and bright prospects for productivity improvement, which means producing more with less. The last section is Yandle’s Reading Table.

ICE Crackdowns and Diminishing Economic Activity

Recently, a major Alabama construction project suddenly went silent. Nearly every worker, despite apparent sign-off through the “E-verify” system, failed to show up on a $20 million job site.[1] The reason? They were scared by an Immigration and Customs Enforcement (ICE) raid on a work site 230 miles away. When it’s a matter of being deported amid reports of immigrants deemed guilty until proven innocent, word travels quickly.

Granted, ICE’s stepped-up activity is a sensitive and complicated issue, but any conversation on the matter should acknowledge that ICE's sweeping nature is creating quite a bit of economic turbulence.

At another, much smaller, Alabama home construction site, a contractor reported to me that he was the only English speaker on the project, and that the other workers stayed inside at lunch for fear that, even though properly documented, they might be apprehended and forced to prove their legitimacy.

We all understand that President Trump is keeping a campaign promise to round up and deport at least one million undocumented immigrants this year. It’s easier to forget that 685,000 were deported in 2024 under the Biden administration, and more than three million were deported during the Obama administration. Some of the recently apprehended individuals have criminal records. Others with clean reports were released after crossing the border and now await judicial review of their status (a process that, given the backlog, may be years away).

Adding to the deportation turmoil, there may be as many as 1.6 million unauthorized immigrants who have voluntarily left the country since ICE efforts became more intense. The count is much disputed, but it’s not just the number that matters. The uncertainty, both for affected individuals and throughout the economy, is an inevitable result of the Trump administration’s high-profile approach.

Hard-hit industries

The round-up activity is making an already tough construction-labor problem more difficult. Construction costs are rising, and thousands of new homes that might have been are not materializing. That’s concerning in a nation where housing scarcity has been driving prices to uncomfortable levels for quite some time. A recent study by the Home Builders Institute and the National Association of Home Builders examined the effects of an earlier labor shortage on single-family home building. Labor scarcity led to a reduction of approximately 19,000 single-family homes in 2024.

The problem cuts across many industries, not just construction. According to the IPUMS Center, in 2024 noncitizens accounted for 33 percent of maid and housekeeping workers and 24 percent of landscaping workers. The Department of Agriculture reports that 42 percent of crop workers are undocumented immigrants. Growing labor scarcity adds to the difficulties farmers face from trade wars that destroy global markets for hard grains and soybeans.

Though this is speculation, America’s ICE-disturbed labor markets may have helped cause the University of Michigan’s August, September, and October consumer sentiment index to fall after two consecutive months of growth. As for the notion that native US workers might enjoy more opportunities in the labor market, consumers expressed rising concerns about declining employment prospects and inflation.

The National Federation of Independent Business’s optimism index also fell in September after being positive for three consecutive months. Get this: Some 40 percent of all “small business owners reported job openings they could not fill.” This was up two points since July and probably not a coincidence.

There’s obviously a paradox here. Ordinary people are worried about getting or keeping jobs while employers are concerned about finding enough workers to keep their businesses flourishing. In theory, native workers step in to replace immigrants. So far, ICE crackdowns that are exporting workers and causing others to be scared to go to work seem to be the more powerful economic force. Border fences are getting tighter, and we are importing fewer workers.

There’s more to the shrinking supply story, but one thing is certain: One way or another, the United States is running low on workers, and we no longer produce as many at home. We will soon be running low on the things they make — and paying higher prices for them.

H1-B visas for sale

While ICE deportations affect labor supply among skilled and unskilled workers, newly imposed restrictions on the influx of highly educated immigrants could cut the flow of another part of labor supply.[2] President Trump seldom misses an opportunity to charge a price for participating in the Great American Bread Machine. America’s capitalist economy is, after all, a world wonder. He most recently proposed charging US firms $100,000 to obtain the H-1B visas that allow foreign-born, scientifically trained, high-tech workers to join their workforce. Until now, the fee and legal charges have been $2,500, and some 85,000 visas have been issued each year. There are currently some 750,000 H-1B holders in America.

By urban location, the largest number of H1-B visa–holders live in New York City, and the second- and third-largest live in San Jose and San Francisco, CA, respectively. In response to Trump, it seems, the Chinese government announced its new K visa, which carries no fee and does not require sponsorship by hiring firms. Though the new visa is apparently not exactly welcomed by millions of underemployed recent Chinese engineering graduates, the program seems to be saying welcome to those who get the US cold-shoulder treatment.

The question here is, who stands to lose out on a great deal: immigrants, the United States, or both?

One wonders if the new higher fee will ration lots of entrepreneurial workers with a proven tendency to create jobs and economic activity, and at a time when the US labor force is shrinking. Others may wonder if all those smart immigrants really make a difference for the rest of us.

We all know that America’s immigrant population forms a large part of the labor force. In 2024, some 19.2 percent of workers were foreign born, up from 18.6 percent in 2023. Of these, Hispanics and Latinos accounted for 48.7 percent and Asian-born workers for 24.6 percent. In 2024, the median weekly earning for immigrants was $1,001, or 84.1 percent of the earnings of their native-born counterparts ($1,190).

Yet some Americans might be surprised to learn just how much this immigrant population contributes to the leadership and innovation behind high-growth companies that fuel our economy.

One recent study from the National Foundation for American Policy found that 55 percent, or 50 out of 91, of the country’s $1 billion-valued startup companies had at least one immigrant founder. Looking more broadly, a 2025 National Bureau of Economic Research (NBER) report indicates that about a quarter of all US “new employer” companies are started by immigrants.

Immigrants even account for 26 percent of US-based Nobel Prize winners from 1990 through 2000 and three of the six US Nobel science laureates named just a few weeks ago.

The large-scale NBER study mentioned earlier also examined immigrant patent activity and high-tech start-ups to determine the difference immigrants have made in the US economy. Looking at data for 300 million adults living in the United States from 1990 to 2016, researchers found that immigrants over 20 years of age made up 11 percent of the US population and produced 25.2 percent of all US patents. They also found that based on scientific citations, immigrant patents are more important than those of domestic inventors.

Still, some people will remain skeptical. Do immigrant inventors merely take a piece of the American pie for themselves? Do they get involved in commercial activity and with domestic inventors?

Drawing on data that touches 850 million individuals in over 200 countries, the NBER researchers found that between 2000 and 2017, 33 percent of US firm start-ups had an immigrant founder, and 22 percent of US start-ups had both an immigrant and domestic cofounder. Furthermore, startups by domestic and immigrant cofounders were far more successful than similar firms started by domestic founders alone.

Probing further still, the researchers found that immigrant-founded start-ups have higher quality labor as well as greater access to investor capital and broader product markets. Immigrant founders also bring greater access to patent holders in other countries. Other research indicates that unemployment rates decline in cities with more H-1B holders, and that where visa allocations are restricted, H-1B employers expand hiring in other countries.

There is also an unknown immigrant interaction effect that yields positive productivity to our economy. It may well be that venturesome souls who are eager to leave their native home and stake out a future for themselves in America are what Daniel Boorstin referred to as “go-getters.” Like the little engine that could, they say “Yes, I can.” And that precious willingness to work forms the origin of all labor supply curves.

In this way, modern immigrants share something with our bold ancestors, as well as with immigrants such as Alexander Hamilton, Andrew Carnegie, and Nikola Tesla, who made contributions we still benefit from today.

Should it cost $100,000 to bring another go-getter to our shores? Or should we leave well enough alone? There may not be a simple answer, but given the amount of economic activity high-tech immigrants bring from other parts of the world to our shores, and the myriad ways that prosperity filters into US communities, the H1-B fee should be large enough to cover all administrative expenses, but no more.

Let’s keep the door open.

Trade Deals, Pay-to-Play Capitalism, and Producing More with Less

Trying to keep abreast of President Trump’s trade deals is like watching an amateur pickleball game: You can never predict the final outcome, but it is surely interesting. Now it seems, China, India, Japan, the European Union (EU), the United Kingdom (UK), and others are ready or have signed a tariff-reducing deal, and Australia has signed a rare-earth minerals deal.[3] At this point, it’s hard to tell if trade overall will be expanded or reduced. America is raising tariffs while other countries are reducing them, and while the details are still lacking or yet to be determined, the Wells Fargo tariff tracker indicates that as of early October, annual US tariff revenues stand at $601 billion, or 64 percent of dutiable imports. While we cannot predict what the numbers will be next month, we can be certain of one thing about the pay-to-play spin on capitalism: Trump’s play will at least partly determine who, what, when, and how much capital will be invested by major US trading partners.

The president seems to see himself as the Colossus standing at the nation’s entry points, rattling the keys to the kingdom. He will take care of those who pay America’s price for entry and deny those who will not. In such a world, politics tends to trump free-market forces. He is not likely to change strategies. In some cases, the outcome looks better than what might have happened. Threatened tariffs have been reduced, and foreign markets have been widened for American goods. For example, tariffs on Japanese cars have fallen from a threatened 30 percent to 15 percent, and US auto and rice producers will have improved access to the Japanese economy.

So far, through major country trade deals, Trump is positioned to personally direct hundreds of billions of dollars of investments from US trading partners. For Japan, the number is $550 billion, for the EU $600 billion, and for South Korea $350 billion. And while the fine print is yet to be seen, Trump has indicated that in some cases, the United States will share in the profits earned on the partners’ new investment.

US Treasury Secretary Scott Bessent sees this approach as forming a model for the future. America, Inc. arises! We saw another version of this in August, when Nvidia and Advanced Micro Devices (AMD) reported that they would pay the federal government 15 percent of their joint profits from selling chips to China. The White House responded favorably to extending the idea to other firms. In yet another addendum to the new pay-to-play capitalism, Trump’s senior aides reportedly compiled a loyalty ranking of 553 major US corporations based on their support of the One Big Beautiful Bill Act.

Pay-to-play continues in yet another form with White House discussions of the federal government taking a 15 percent equity ownership in financially troubled Intel. US Commerce Secretary Howard Lutnick first indicated that the ownership would be a payment for CHIPS Act funding and would not involve any special management rights. He suggested equity participation could be required as payment for future subsidies. Then, in typical Trump administration fashion, when there was pushback to the Lutnick proposal, the administration backtracked, but only briefly. Later, Lutnick put forward the notion that the federal government should take an equity position in defense firms.

It should be noted that large forthcoming US investments and goods purchases would have occurred anyway. That’s what countries do with the dollars that accumulate from exports to America. It’s the prospective use of the green pieces of paper that gives them value. What differs here is that the expenditures and investments will be guided by a sitting president, not by the overall market forces. For example, in 2024, the EU exported around $370 billion to the United States, which means the EU would have been holding dollars of equal value once the transactions were completed. Those dollars would have been looking for a home. Now, with the EU deal in place, Trump can deliver on promises to specific US firms and industries and perhaps gain their support while doing so. We had best remember Friedrich Hayek’s fatal conceit warning that even the brightest and best can’t outsmart markets.

Trump’s efforts to control the US economy go beyond pay-to-play capitalism and extend to comparatively minor matters, from urging Coca-Cola to use cane sugar instead of corn-based sugar, to suggesting that J.P. Morgan fire its senior economist for forecasting slow economic growth and higher inflation, to advising Cracker Barrel on how best to advertise its business. He is a busy man. Of course, the list of Trump efforts to steer the US economy has to include his ongoing battle with Fed chair Jerome Powell, which now includes the threat of a lawsuit over the cost of renovating the Fed headquarters and the firing of the Bureau of Labor Statistics commissioner. In both cases, Trump argued that he was being directly harmed by the Fed’s actions.

Almost from the nation’s beginning, America has flirted with national planning and favoring one industry over another. In 1791, Alexander Hamilton famously called for protecting infant industries until they were fit and ready to deal with the hard realities of free-market competition. In the 19th-century there were constant and sometimes fierce tensions between northeastern textile manufacturers who wanted tariff protection and southern cotton producers who wanted unfettered access to world markets.

Wars and the Great Depression brought government ownership of industries and extensive regulation. Even under the relatively free-market Reagan administration, when Japan Inc. was viewed as an existential threat for the computer chip industry, the United States engaged in a version of industrial planning. But generally speaking, the heavy hand of government has relaxed somewhat (though never completely) with the passing of the emergencies that inspired it.

There is no way for us to know if President Trump’s version of pay-to-play capitalism will redefine how the American economy works in the long run. At heart, he seems to be a negotiator who doesn’t show all his cards.

But in the short run, we can be certain that, with large international investment being managed and tailored by the White House, the capability to lobby and get along with the boss will grow at the margin, at the expense of the capability to invent new products and to extend one’s own market appeal.

In short, the Trump approach centralizes economic decision-making both in the United States and with our trading partners. There have and will be wins that come with it. Cartelization and the hardening of America’s economic arteries are the results to fear.

The bottom line: Can America produce more with less?

We’ve sustained almost endless shocks including a pandemic, shutdowns, high inflation, government layoffs, immigrant infusions and deportations, federal-fund claw-backs and years of off-and-on, tariff-induced trade wars.[4] But we have also witnessed growth in robotics and the start of an AI revolution. Given all the disruptions happening across the world, and maybe because of them, could it be that we are learning to produce more with less?

Managers of major firms are indicating exactly that. With the help of AI and because of simple necessity, Amazon is laying off 30,000 people, and Airbnb, Intuit, Target, Walmart, J.P. Morgan, and Goldman Sachs have put a lid on headcount while sales are increasing.

Most hard-working Americans know that real GDP growth is a vital measure of prosperity; it is the value of new goods and services being produced in our economy. But the typical worker and consumer know little about what exactly determines real GDP growth, as well as about the details found in the US Department of Commerce’s Bureau of Economic Analysis (BEA) report each quarter. Most are, in a phrase, “rationally ignorant,” because it’s far more important to know how we are personally doing and what might lift our own families’ prosperity.

That said, the average person feels better knowing that BEA’s first estimate for 2025’s second quarter showed real GDP growth forging ahead at 3.8 percent. This is especially true if one recalls that first quarter growth wasn’t growth at all, but shrinkage at the rate of 0.60 percent. The strength of the bounce-back was something of a mystery.

If we want to get down to basics, whether we see positive or negative GDP growth (and by how much) depends on the answer to two simple questions: Are people working more or less? And when they work, are they producing more? We need to add just two numbers to get a back-of-the-envelope measure of real GDP growth: growth in total employment and growth in productivity.

Viewed through a panoramic lens, we start to see one important factor that’s made GDP growth return with a kick. The 2020 COVID shutdowns disrupted how America works. They forced some workers to find new ways to provide for themselves and their families. As a result, the share of the adult population able to participate in the nine-to-five labor market fell and remained at a lower level. Real GDP growth went negative, and we got a deep but short recession.

But we also learned something: It costs a lot less to work at home than to dress, commute, and work in a city office. Productivity went up. Then, a lot of people decided to stay out of the nine-to-five market and start home-based businesses instead. There was an explosion of new start-ups that has continued to the present. And while all this was going on, virtual meetings, then artificial intelligence, came on in spades. Productivity got more nudges.

The current picture shows rising productivity that compensates for subdued labor force participation and lower labor-force growth. In the second quarter, labor productivity was up 2.4 percent. Employment grew 1.0 percent, and over the last year hourly earnings rose 3.9 percent.

A recent National Bureau of Economic Research study gives details on just which US industries are experiencing the largest 2009–2023 productivity gains and compares those with gains for 1987–1997 and 1997–2009. As indicated in figure 4 below, “Apparel & Leather” showed the largest recent gain, “Automobiles” the second largest, and “Computers & Electronics” the third largest. It’s also worth noting that the category “Computers and Electronics” has been the productivity growth champion since 1987.

FIGURE 5. Productivity growth, 2009–2023

Source: Enghin Atalay et al., “Why Is Manufacturing Productivity Growth So Low?” (NBER Working Paper No. 34264, National Bureau of Economic Research, September 2025), 7.

The result of external shocks, technical change, and the government’s response, including inflation and trade wars, is that the nation has learned to produce more with less. That promises good things for future prosperity, especially as more workers adjust to this new normal and learn to take advantage of the new world of work.

So, what’s the bottom line? The American market economy is still resilient, and though it’s been sharply affected by White House policy actions, it works. While we must remember that every day is a new day for potentially disruptive Washington policy changes, let the good times roll.

Yandle’s Reading Table

In this report, I am reviewing two books. The first is Angus Deaton’s Economics in America, a well-written, at times humorous, account of his personal experience as a Scottish economist spending an extraordinarily successful professional life as a Princeton faculty member, researcher, and Nobel Prize recipient. The book is subtitled An Immigrant Economist Explores the Land of Inequality. The focus on inequality, in a sense, defines the book. I learned a great deal from the book and hope it will be widely read and discussed. Deaton is an excellent writer and teacher.

But while the book is well worth reading and studying, I found Deaton’s account of economics in America deeply frustrating. The book’s subtitle partly explains why. Deaton’s fixation on inequality led him to make a plea to economists to return to their roots and focus on poverty, address the dramatic changes in income distribution that have widened the gap between rich and poor, and reengage with the profession’s calling to promote human flourishing and justice.

As I questioned the assertion regarding an economist’s normative calling, I found myself asking Google, “What do economists do?” I also made a plea to AI by way of Google and asked, “What is economics”? Neither Google nor AI seemed to agree with Deaton’s plea. Instead, both platforms described economists as being engaged in the positive but perhaps more humble effort to understand and explain human community engagement with scarcity in the effort to satisfy insatiable wants. I hasten to note that Deaton’s deeply discussed belief that economists can make a difference in how the world actually works is an apparently powerful motivating force in his life. The belief may be more common among British academics than their American counterparts. Deaton’s personal commitment to trying to affect political outcomes may also explain why leading Chicago School scholars such as George Stigler and Milton Friedman were keenly admired by Deaton for their excellent scholarship but were not a source of inspiration for his work. The same philosophical orientation may explain why in his informal commentary on economics in America Deaton made little or no mention of the Virginia School, the rise of Public Choice Economics, or the efforts of James M. Buchanan, Gordon Tullock, and Robert Tollison to explain why political efforts to make the world better can be steered in ways that also increase inequality.

Of course, Deaton’s book is about his American experience, about how someone from another place and culture can be equipped to see things that the rest of us might not focus on when in our original habitat. It is in this light that I found several of his chapters to be excellent sources of new information and thought. Deaton’s Chapter Three is titled “Poverty at Home and Poverty Abroad.” The chapter highlights his creative data analyses of US and global income data to draw comparisons of the share of national populations that may be living under some specified poverty line. He explains how he worked the data for multiple nations to establish a poverty line and make comparisons of well-being for US states and nations around the world. Though facing an impossible task at the outset, Deaton explains how his effort worked out and, based on the results, he found that using $5.00 a day as a poverty-defining income, the share of population in poverty was the same for China as the United States. Surely controversial, of course, the findings are offered as an example of efforts that might be made to better compare inequality across time and place, which, of course, is one of Deaton’s chief interests.

Chapter Four, “The Politics of Numbers: Fixing the Price?,” addresses politicians’ past efforts to influence, if not totally denigrate, the government-produced measures of inflation and employment. Sounds familiar, doesn’t it? Deaton takes the reader into the back room, so to speak, where the CPI is produced by the Bureau of Labor Statistics, and reminds us of the index’s political importance in adjusting the retirement income of tens of millions of people, as well as the cost of essentials specified in contracts that adjust for inflation.

As Deaton tells the story, we learn that the CPI has a well-identified positive bias, at least on theoretical grounds, that if adjusted for could lead to sharp reductions in federal deficits and future debt. The bias comes from matters having to do with adjusting for quality changes on goods in the consumer basket and for substitution effects that occur when the price of one item rises but consumer substitute a cheaper commodity. The results of a 1995 “blue ribbon” committee’s study of the problem and recommended changes led to an effort by Speaker of the House Newt Gingrich to force a BLS correction or face closing. (Again, this has a familiar ring to it, doesn’t it?) Instead of making changes, another study committee was named, and less draconian changes were recommended. The budget crisis passed, and the CPI survived in its present form. Deaton makes what might be a boring discussion of statistical issues highly entertaining and informative.

On August 12, 2022, world-renowned novelist Salman Rushdie, author of the controversial 1989 The Satanic Verses, which prompted Ayatollah Khomeini of Iran to issue a global fatwa calling for his death, stood to speak at the Chautauqua Institution. Rushdie had planned to talk about providing safe spaces in America for authors from elsewhere, and Chautauqua is world famous for providing an open forum for the discussion of ideas.

The global fatwa against Rushdie reflected Muslim outrage regarding his depiction of the prophet, an action seen as undermining the religious glue that holds together people who worship Muhammed. Because of the fatwa, Rushdie was provided police protection, and his life was threatened numerous times. But that was a long time ago in England. In 2022, he was living in America, and he felt secure that August morning.

As Rushdie tells the story in his 2024 book Knife, just as he stood to speak, a young man dressed in black, carrying a knife, rushed toward him, and in a flash stabbed Rushdie some 15 times in the eye, face, neck and stomach. The assailant was subdued by Rushdie’s copresenter and members of the audience, and Rushdie, assisted by two physicians who happened to be in the audience, was airlifted to a hospital in Erie, Pennsylvania. After hours of surgery followed by rehab and treatment, he recovered, though he lost the sight of one eye and much of the use of one hand and arm. Somehow, after all this, Rushdie feels no deep hatred towards his assailant but definitely feels that his life took on a new meaning that morning.

In one of the book’s more fascinating chapters, Rushie engages in an imaginary conversation with his assailant, now serving a 25-year sentence for attempted murder. Rushie asks the questions one might expect and offers responses that tell us how he was affected by the experience. The chapter helps the reader understand some of the deeper issues that make it seemingly impossible to find lasting peace. In another way, the chapter seems to be a form of self-developed therapy for Rushdie.

Knife provides detailed descriptions of his treatment and long recovery. His near-death experience reshaped his life and led him to gain a new and deeper appreciation for his wife, family members, and neighbors who brought him comfort and love. Near the book’s end, as he ponders all this, he speaks of his wife, Eliza, and indicates that they ask: “How are we today? Where do things stand right now? What would be good to do today, okay to do again, and if so, how would we go about doing it and with whom”? He reminds us that joy is of the moment, and we should find it here and now.

The book is an interesting and troublesome read, and its key lesson is simple and powerful.

Notes

[1] This discussion is based on Tim Reid, “This Construction Was On Time and On Budget. Then Came ICE,” Reuters, July 28, 2025, https://www.reuters.com/world/us/this-construction-project-was-time-bud….

[2]This section is based on Bruce Yandle, “Trump’s $100K Fee on Foreign Skill Is a Net Loss for America,” St. Louis Post Dispatch, November 6, 2025, https://www.stltoday.com/opinion/column/article_b16cca6e-84b1-4d8a-89cc….

[3] This section is based on Bruce Yandle, “Trump’s Trade Deals Are Pay-to-Play Capitalism,” Washington Examiner, August 9, 2025, https://www.washingtonexaminer.com/restoring-america/faith-freedom-self…

[4] This discussion is based on Bruce Yandle, “Is America Producing More with Less?,” DC Journal, August 20, 2025, https://dcjournal.com/is-america-producing-more-with-less/.