- | Regulation Regulation

- | Policy Briefs Policy Briefs

- |

The Economic Situation: June 2026

Amid uncertainty, America’s economic resilience endures

Getting Started

In just a few days, we will celebrate America’s 250th birthday. The nation’s longevity is probably more than the founders expected. After all, no people before had deliberately and successfully broken away from a mother country to form a democratic republic, announcing to the world that “all men are created equal and endowed by their Creator with certain inalienable rights, among which are life, liberty, and the pursuit of happiness.” What historian Walter Isaacson calls the most beautiful sentence ever written (his book is reviewed later in this report), this announcement was broadly embraced as more than elegant prose; it was a noble aspiration and an audacious challenge for a population of 2.5 million people, 500,000 of whom were enslaved.

Indeed, led by slave-owner Thomas Jefferson, who was charged with writing the first draft of the Declaration of Independence and desperately wanted to find a coordinated way to end slavery, the founders struggled to include a requirement that slavery be eliminated. They recognized that eliminating slavery would have to be handled with care by a government that embraced freedom. What a dream! But much to Jefferson’s distress, abolition was a bridge too far. That bridge was finally—and barely—crossed following the Civil War, though equality remained a dream, and still is.

From the founders’ aspiration, the role of the new democratic republic’s government has expanded dramatically. We now have a government that protects the nation from foreign aggression, maintains domestic peace, and provides a system of justice, highways, bridges, and infrastructure—activities that Scottish philosopher and economist Adam Smith, whose 1776 magnum opus, An Inquiry into the Nature and Causes of the Wealth of Nations, introduced ideas about free markets, called the duties of the sovereign. But government does far more. Our national government’s actions embrace practically everything, from the provision of basic healthcare and retirement benefits to regulating the prices of imports, eyeglasses, pharmaceuticals, and petroleum products, to bailing out favored bankrupt firms, guaranteeing loans, and promoting the development of electric vehicles and outer-space travel. And this just begins to describe how government has evolved in the “pursuit of happiness.”

Indeed, government leaders seldom refer to our economy as being based primarily on free-market capitalism or private action, let alone mention Adam Smith’s ideas. And for good reason: Those notions are no longer seen as part of the nation’s foundation stones. It seems few people have read Adam Smith, or much else about the foundations of government. We are a nation of pragmatists, dealmakers, not ideologues “endowed with certain unalienable rights.” But we still have memory.

That memory is evident in current debates over the nation’s economic direction. In a recent exploration of America’s growing “state capitalism,” as some people term our economic order, a columnist pointed out in The Economist that, with thunderous public statements, President Donald Trump has pushed taxpayer-funded investments into a rare-earth mine in California, a zinc operation in Tennessee, major initiatives at Intel, nuclear reactors at Westinghouse, and, of course, talked about taking over Spirit airlines and perhaps helping others now in line. Yet while the pace of state investment has quickened, the level is still small relative to that of other leading industrialized countries. But this may be faint praise for a nation that once trumpeted the importance of market-based incentives and Adam Smith’s invisible hand.

We’ve come a long way since 1776

As American economic historian Robert Higgs described persuasively in his now-classic 1987 book Crisis and Leviathan, over the centuries there has been a systematic tendency for the federal government to expand its activities in response to shocks and crises—often funded by deficits—and to maintain those expanded activities long after the motivating crises have passed. Most recently, government activity, though not employment, has grown in response to 9/11, COVID, the Afghanistan War, and a perceived nuclear threat from Iran. Deficit financing is projected for the next 10 years, and paying interest on the debt while maintaining other government-funded commitments is the large, yawning challenge.

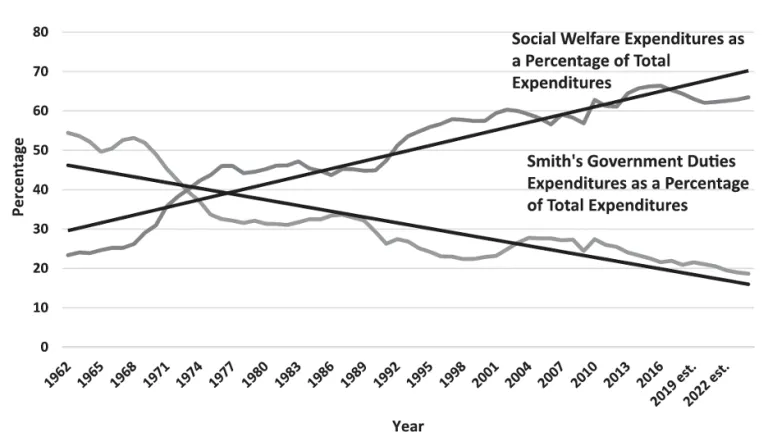

This pattern of expansion is reflected in federal spending trends. In 2020, economists Jody Lipford and Sydney Patten examined federal government expenditure trends from 1962 through 2022 (est.), including spending on the duties of the sovereign and other parts of the federal budget. Figure 1, drawn from their report, suggests what to expect.

FIGURE 1. Federal government expenditure trends

Source: Jody W. Lipford and Syndney Patten, "Is the Welfare State Crowding Out Government’s Basic Functions?: An Update," The Independent Review 25, no. 1 (2020).

Considering the massive scope of US government activities, one might reasonably wonder whether the nation is, in some measurable sense, large enough, to carry out all the promised commitments. When we compare the United States to other leading nations, we sometimes forget just how massive the US economy really is and how long it has been the world’s dominant economic force.

How large is the United States' economy?

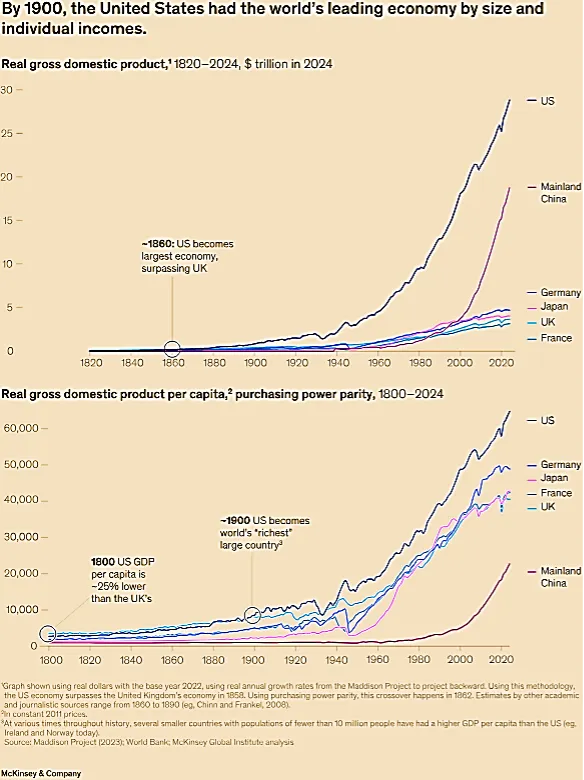

Drawing on a recent report from the Conversable Economist, I provide in figure 2 charts comparing total real GDP by year and real GDP per capita for the years 1920 to 2024. As the charts show, the United States became the world’s dominant economy by 1860, and since 2020 its lead has widened relative to China, the world’s second-largest economic power. The per capita GDP chart, where US productivity is a key driver, is even more impressive.

FIGURE 2. Comparison of GDP and GDP per capita

Looking at GDP growth

Fast-forward to the present. The Department of Commerce’s second estimate of real GDP growth for the first quarter of 2026 came in at an improved 1.6 percent. Led by growth in investment and exports, this increase followed the fourth quarter’s lower 0.5 percent growth, which reflected an extended government shutdown and sharp reductions in government employment under the Trump administration, as well as low levels of private investment. Growth in the third quarter of 2025 was a strong 4.4 percent. These numbers tell us we are observing the effects of large policy changes on the macroeconomy, along with a quieter, AI-driven industrial revolution. At the same time, we also face the added uncertainty that comes from the Iran war and sharply rising energy prices. Economic forecasters are challenged to revise their estimates.

Table 1 shows quarterly real GDP growth estimates for the next four quarters from three forecast groups I regularly follow. It’s important to note that The Wall Street Journal and Wells Fargo estimates were produced in April and reflect the run-up in energy prices associated with the invasion of Iran, while the Philadelphia Fed’s forecast was produced in March. The contrast between earlier and later forecasts is striking. Notably, none of the forecasters expects a recession, but the pace of output growth is much slower than what we saw in 2025. The reason? The forecasts now incorporate the effects of Trump’s trade wars and, for two of the projections, the Iran war.

The geographic imprint

As indicated in figure 3, which shows 2025 year-over-year state GDP growth, economic activity is unevenly distributed across the 50 states. The Southeast stands out as the stronger growth region. Traveling west, one must reach Arkansas and then Utah before encountering states with similarly high growth rates.

Figure 4, however, which shows February leading growth indicators for the 50 states, looks more promising: Just eight states report negative numbers.

How this report is organized

The report has three remaining sections. The next section focuses on Trump’s on-again, off-again tariff policies and their effect on the nation’s economic heartbeat. The issue is not so much about the pros and cons of tariffs; uncertainty about when and if specific tariffs will apply is a key element of the discussion. The section also includes a discussion of the effects of global auto industry investment. The third section turns to the Iran war, the newly proposed federal budget, and the prospects for more inflation. Here we find more uncertainty but for one thing: Inflation will continue as we, as nation, seek to consume more each year than we produce. Finally, the last section takes us to Yandle’s reading table including a report on three books.

Tariffs and Prosperity’s Prospects

On February 20, the US Supreme Court struck down the extensive tariffs Trump imposed under the International Emergency Economic Powers Act of 1977 (IEEPA).1The ruling was not a fatal blow to the administration’s defining economic policy agenda, but it was a reminder that the nation was formed by a group of people trying to free themselves from tariffs imposed on goods they wished to import tax free. What goes around, comes around.

Those Tea Party patriots opposed taxation without representation and ultimately adopted a Constitution that gave Congress, not the president, the exclusive power to tax, whether by tariffs or otherwise. Of course, through legislation, Congress can grant that authority to the executive branch under certain circumstances. Unfortunately for Trump, as interpreted by the Court, the IEEPA—which never uses the word “tariff” but instead refers to regulation in addressing emergencies—was not a suitable vehicle for his wide-ranging tariff program.

Though clearly not welcomed by President Trump and his advisors, the Court’s action was not unexpected. The US Court of Appeals for the Federal Circuit had issued a similar ruling in August 2025, and the US International Court of Trade had ruled unanimously the same way in May. Trump now turns to other, less attractive but still viable legislation, such as Sections 122 and 301 of the Trade Act of 1974 and Section 338 of the Tariff Act of 1930, to support continued tariffs. All of these alternatives require regulatory procedures; they cannot be implemented instantly by simply signing an executive order.

Trump leadership was left with no choice but to refund some $130 billion in import duties paid by US importers. By the fourth quarter of 2025, some $364 billion had been collected. Yet, in a “never say die” or “naughty and nice” response, Trump indicated that the administration would remember those who chose to forgo a deserved refund. It is as if major economic entities now operate in a kind of Trumpian purgatory, where regular penance and loyalty must be demonstrated to avoid being cast into outer darkness where Trump favors and licenses are reversed, and punishment can be costly. The level of anxiety may be highest for firms that produce sophisticated chips and related technologies sought by Chinese producers. Just recently, US chip producers received Department of Commerce orders limiting exports to China.

Tariff-based uncertainty

With the Iran war, an unsettled Middle East, rising energy prices, and reports of jet-fuel shortages in parts of Asia and other nations, the Court-unleashed tidal wave rolled over a sea of tariff uncertainty that was already at play. Time will determine how all the previous tariff-based trade agreements signed by a host of US trading partners will survive. One can’t help but recall the Humpty Dumpty nursery rhyme and wonder if all the king’s men can put things back together again. But one thing is certain: They will be trying.

In an effort to put things together again, Trump immediately imposed a 10 percent tariff on all US imports. Then, a day later, in the spirit of keeping uncertainty alive, he raised the rate to 15 percent, the maximum allowed under Section 122 of the 1974 Trade Act, which permits such measures for up to 150 days. Though President Trump would likely disagree, there’s little doubt that tariff-induced uncertainty is restraining key sectors of this economy. It is not so much the level or scope of tariffs, but rather the unpredictability of what Trump will do next month or next year that forms the real challenge.

Of course, it is uncertainty, the arbitrary use of tariffs when attempting to strike a deal, that makes the instrument so attractive to Trump. Proudly citing growth data, Trump recently pointed to his tariffs and claimed they “have created an American economic miracle, and we are quickly building the greatest economy in the history of the world.” Others point to America’s K-shaped economy, where one leg is rising rapidly and the other is sinking, and argue that all is not well and tariffs are the reason.

For example, Washington consultant Bruce Mehlman points out that consumer confidence among people without a college degree fell to an all-time low in January 2026, according to the University of Michigan’s Index of Consumer Sentiment, which began in 1976. Mehlman indicates that the warehouse workforce, which is heavily affected by reduced imports, has declined by more than 50 thousand in the last 12 months. As to the other leg, those lifted by a buoyant stock market—and there are a lot of them—are happily spending like there is no tomorrow. The top 10 percent of US earners now account for a record 49 percent of all consumer spending. The May index is even lower.

What about manufacturing, the protected industry? Have tariffs helped? In January 2026 total manufacturing employment stood at 12.59 million workers, a bit shy of where it stood a year earlier. In its 2025 manufacturing survey, the consulting firm Deloitte noted that more than three-quarters of manufacturers “consistently cited trade uncertainty as their top concern.” For global auto producers and other industries, living with known tariffs is one thing; not knowing what Trump will do next month or next year is the real wrecking bar.

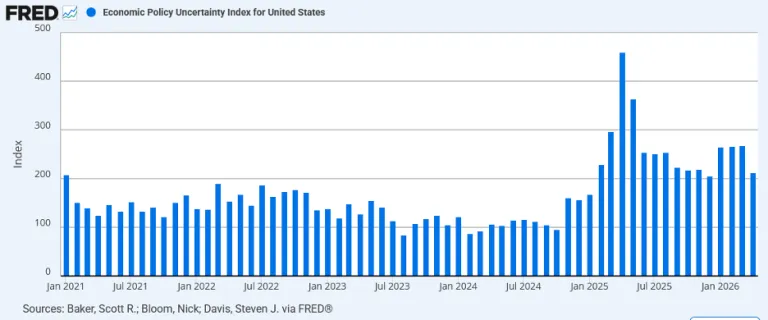

A look at the daily Economic Policy Uncertainty Index provides context. Based on the frequency of certain words in 10 major US newspapers, the index is used in statistical analysis to explain US capital investment and GDP growth. Periods of high uncertainty correspond with pauses and lower investment in core capital goods (those that go into expanded manufacturing facilities). Before cranking bulldozers to construct a plant that will take years to complete, CEOs need to know that the rules of the game won’t change. They need certainty.

Figure 5 shows the monthly average value for the uncertainty index maintained by the Federal Reserve Bank of St. Louis from January 2021 through April 2026. Prior to the start of the Trump administration in January 2025, the index bounced along with a mean value of about 250. In January 2025, the monthly average hit 495 and bounced to even higher levels in response to Trump’s tariffs and other policy changes. In March, following the Court’s striking down Trump’s tariffs, the monthly index rose to 395. We are close to where we started.

FIGURE 5. The monthly average value for the uncertainty index

Source: Scott R. Baker, Nick Bloom, and Steven J. Davis, "Economic Policy Uncertainty Index for United States [USEPUINDXD]," retrieved from FRED, Federal Reserve Bank of St. Louis, https://fred.stlouisfed.org/series/USEPUINDXD, May 28, 2026.

Business leaders know by now that Mr. Trump will reach for his tariff gun whenever a country’s agents fail to go along with his policies, whether it is Mexico and drug enforcement, Canada and trade with China, or India’s trade with Russia. But the timing and steadfastness of position cannot be predicted accurately.

That’s why, even after the United States and European Union (EU) completed a long and arduous post-April tariff negotiation in the summer of 2025—reducing average tariffs to 15 percent from the earlier announced 25 percent level—EU leadership and corporate CEOs could breathe only a temporary sigh of relief. The higher 25 percent tariffs would come again.

Autos: A case study

European auto producers have wrestled with tariff uncertainty since Trump’s first administration, when his ire focused on German brands such as Mercedes, Volkswagen (VW), and BMW. Based on Trump’s zero-sum interpretation of trade, where exporters win and importers lose, the EU was “ripping us off,” shipping thousands of vehicles here monthly while buying few from us. Trump never highlighted that Mercedes, BMW, and VW have massive US investments and employ tens of thousands of American workers who, in addition to serving the domestic market, export to the rest of the world.

Without warning, on January 16 of this year, Trump announced an arbitrary and sudden return to the pre-summer-negotiation EU tariff levels—his way of punishing Europe for its opposition to his plan to take Greenland “one way or the other.” On January 21, the uncertainty index registered 543.

In response, EU President Ursula von der Leyen said: "The European Union and the United States have agreed to a trade deal last July. And in politics as in business—a deal is a deal.” Any European automaker, affected by tariffs, that had felt secure and able to plan following the summer agreement was shaken. Then, on January 26, Trump reversed the reversal. The index fell back to 285, but in today’s world this must be considered a snapshot of a wave that’s receded for the moment. And it was for a brief period. On May 1, after being criticized for his Iran war policies by the German chancellor, Trump announced 25 percent tariffs on European imports to the United States. Again, EU leadership registered disbelief, but recognized this is the situation we must learn to deal with.

Earlier, VW Group’s Audi division was on the verge of announcing a final decision on the construction of a $4 billion US manufacturing plant, its first, which would employ 4,000 workers. South Carolina or Tennessee had been suggested as sites. It was not to be. Also on January 26, VW President Oliver Blume said: "With the tariff burden remaining unchanged, a large additional investment isn't financially viable.”

Leading the world’s second-largest auto producer, after Toyota—one that operates in 30 countries and is therefore very familiar with the risks of tariff uncertainty—Blume explained that “stable, reliable framework conditions are crucial for industry. That’s why we continue to focus on dialogue and international cooperation—on both sides of the Atlantic.” VW left open the possibility that Audi production might someday happen at the firm’s large Chattanooga plant or its new Scout Motors plant under construction in Blythewood, South Carolina. But for now, uncertainty had killed the deal.

We observed another example of tariff uncertainty in late January, when Trump threatened to reverse the negotiated tariff plan for autos from South Korea. Hyundai Motors CEO José Muñoz, who manages massive US investment, including a new plant ready to be opened in Georgia, and whose company sold more than one million vehicles in the United States in 2025, indicated he “wanted his people to be ready for anything.” Unlike Audi’s situation, Hyundai already has multiple US factories in operation. As Muñoz put it, “Once you make a comment to have a factory, and then you have the factory up and running, there is no way back.”

Finally, concern about Chinese auto competition has risen to such a level that 70 US Democrat members of Congress recently sent the White House a petition asking that China not be allowed to own or operate a vehicle manufacturing plant on US soil—or export vehicles to the United States—even if inputs come from North America, noting that such activity would present a security threat. The Chinese embassy responded with a request that national security not be used as justification.

Final thoughts

Following the Supreme Court’s ruling that reduced “Tariff Man” Trump’s ability to arbitrarily impose tariffs on trading partners, the US economy is swimming in a sea of Trump-inspired uncertainty. Thankfully, there is far more to the US economy than the trade sector, and there are other offsetting strengths. But until things change, American prospects as an industrial power will not be as bright as they might otherwise be.

The Iran War, US Economy, and More Federal Debt

When the Trump administration launched the war in Iran two months ago, higher oil and energy prices were surely expected.2Yet there was a sense that the US economy was strong and vibrant enough to keep running smoothly. Fed by statements from Trump, there was also a feeling that the sudden US/Israeli attack would end quickly, that once bombed, Iran would yield to US demands to end its nuclear bomb effort. The US economic engine was viewed as capable of handling a Middle East war without serious difficulty. Now, two months later, with the war still continuing and weapon inventories being depleted, second thoughts are emerging.

Just a week before engaging Iran in war, the president painted a bright picture in his February 24 State of the Union address: “Inflation is plummeting, incomes are rising fast. The roaring economy is roaring like never before, and our enemies are scared, our military and police are stacked, and America is respected again.”

Now, the economy’s heartbeat is strong but not exactly soaring. Inflation is heading skyward, and signs of stress are beginning to appear across traditional allies. Did Trump receive bad advice prior to his State of the Union address about the economic outlook? Or was the speech intended to be mainly rhetorical?

There have been some meaningful data reversals and disappointments reflecting the prewar period. The domestic economy may not have been as strong as believed when the conflict began on February 28, when the latest estimate for 2025 fourth-quarter GDP growth stood at a weak-but-positive 1.4 percent. This was revised down to 0.5 percent on April 9. Now, of course, the first estimate for first quarter, 2.0 percent, indicates things are looking better.

As the war progressed, we saw significant revisions in labor market data. The April 3 US Bureau of Labor Statistics employment report showed a gain of 178,000 jobs for March and 115,000 in April, but February’s loss was revised to a larger decline of 133,000 jobs. Overall, nonfarm payroll growth showed little gain over the last 12 months. Most of the employment gains have come in healthcare and construction. Only three states saw manufacturing employment growth in the first nine months of 2026; the rest lost factory jobs.

Turning to inflation, on May 12 the Bureau of Labor Statistics reported that the April all-items Consumer Price Index had risen 3.8 percent over the prior 12 months. Rapidly rising energy costs, especially gasoline at the pump, had entered the picture. Excluding food and energy, the increase was 2.8 percent, still well above the prewar 2.4 percent level and likely to rise further. The important Fed-watched quarterly Personal Consumption Expenditures Index, produced by the Department of Commerce, was up 4.5 percent in April, well above fourth quarter’s 2.7 percent. Rising energy prices are now baked into the economy.

Then there’s the skyrocketing price of oil and energy inputs into gasoline, fertilizer, and practically everything else. In late March, the cost of petroleum-based fertilizer inputs, urea and ammonia, rose 50 percent and 20 percent, respectively. The warning light on the farm economy turned red. If crop yields fall, consumers will voice strong displeasure over food prices.

Is there a Fatal Conceit?

Economics offers no obvious prescription for peace once a multi-country war is underway, but a key lesson from economist and Nobel laureate F.A. Hayek may make the path to better times easier. When conflicts or emergencies arise, national leaders tend to subscribe too readily to the idea that they can treat the world’s economy like a complicated, but ultimately understandable, vehicle and chart the optimal path forward. A bunker mentality takes hold. Hayek referred to this as a “fatal conceit.”

The real world is simply too large, and the necessary information too dispersed and ever-changing for command-and-control decision makers to engineer the outcomes they want. Wartime decision makers must be ready to relax their grip on the economy, give other decision makers latitude to move freely, and allow the market process operate.

Let us hope that, whatever assumptions were made at the outlet of this war, our leaders remember that we’ll all have a smoother ride when cooperating in a free and open society.

The new budget and Liberation Day’s demise

In late April, the White House released its 2027 budget request to Congress, calling for massive increases in defense and border-related spending, serious cuts elsewhere, and the same old deficit-and-debt song and dance.3In so doing, President Trump dashed prospects for his own dream of ending the supposed “rip-offs” being perpetrated on America by our international trading partners.

If the anniversary celebration for Trump’s “Liberation Day” tariffs didn’t already ring hollow, it should now.

Trump has long been vocal in his displeasure with other nations that sell a lot to Americans but buy less from us. But if the US trade deficit is the enemy, then deficit spending must be as well.

Even with the presidential budget’s highly optimistic assumptions about GDP growth boosting government balance sheets—e.g., 3.5 percent real GDP growth in 2026 and 3.1% for 2027, 2028 and 2029—an analysis by the Committee for a Responsible Federal Budget links the proposal with continual deficit spending through 2036. (It’s interesting that the White House document itself provided no direct deficit calculations.) In dollar terms, the annual deficit would move from “$2.1 trillion in FY 2026 to $2.2 trillion in 2027 then fall to $2.0 trillion in 2029 and $1.3 trillion by 2036.”

At the same time, due to considerations such as weak levels of private savings and a public sector that soaks up every dollar, the American people are destined to continue consuming more each year than is produced in the 50 states.

We are a high-consumption, low-saving society. With the exception of 2015, US consumers—both privately and through government—have annually consumed more than the nation has produced every year since 2002.

All of that deficit spending and the goods and services that Americans consume must come from somewhere. People elsewhere—in China, for example—save more than we do. They have bought US government bonds to fund our deficits and have sold us goods and services that American consumers are generally glad to have.

Trump’s long-term answer to the resulting trade imbalance is his love affair with tariffs, which culminated on Liberation Day, April 2, 2025. The justifications for many of his tariffs have since been weakened by the Supreme Court, but they largely remain in place.

Interestingly, on Liberation Day’s anniversary, just one day before the budget was released, the White House announced that “President Trump threw away the illusions of ‘free trade’ to finally put Americans and America First.” Yes, Trump replaced consumer sovereignty with tariff-based command and control. Now his budget calls for ongoing deficit spending and new debt to support it, making his dream of trade-balance an impossible one to achieve. Indeed, the trade deficit surged in March as imports of motor vehicles and consumer goods peaked.

America’s fiscal history, not its history of free trade, is the real nightmare. We have had a litany of past deficit-cutting efforts, of which some actually made a difference. But now the deficit weeds in the lawn are suffocating the shrubs. US debt has been downgraded by all three major credit rating agencies.

The costs of paying the interest are rising rapidly and now rival spending on national defense. As Cato Institute analyst Romina Boccia points out, “Looking ahead, the federal government’s largest obligations—Social Security, Medicare, Medicaid, and interest on the debt—are projected to consume all federal revenues within little more than a decade.” Put another way, something has to give.

We’d best hope that, rather than filling our harbors with tariff-shaped rocks, President Trump will keep the free-trade doors open and focus instead on controlling our government spending habit.

Yandle’s Reading Table

With July 4 and the celebration of America’s 250th birthday upon us, what could be a more appropriate read than historian and noted biographer Walter Isaacson’s amazing 67-page book, The Greatest Sentence Ever Written? An obvious lover of words and careful written communication, Isaacson explores the interaction among Thomas Jefferson, Benjamin Franklin, John Adams, and other founders as the Declaration of Independence was being drafted in Philadelphia in June 1776. Recognizing fully that its action would lead to violence that would put their lives and fortunes at risk, the writing committee, led primarily by Jefferson, wrote, edited, argued, and wrote again until it was satisfied with the result ratified by the Continental Congress.

As has been noted by others, Jefferson was a Euclidean thinker and a Deist; he was not a Christian, and that helps explain the way he first wrote the Isaacson-designated “Greatest Sentence.” As we all know, the final draft read, “We hold these truths to be self-evident, that all men are created equal, that they are endowed by their Creator with certain unalienable rights, that among these are life, liberty, and the pursuit of happiness.” But Jefferson’s first draft was more Euclidean. It read, “We hold these truths to be sacred, that all men are created equal, and from that equal creation they derive rights.” We learn that Jefferson fully appreciated the blatantly hypocritical inconsistency in his “all men are created equal” appeal, and in his first draft he called on government to end slavery. As a slave owner, and given that each of the colonies at the time allowed slavery, Jefferson believed they had a tiger by the tail. As he saw things, the impoverished, uneducated slave population could not simply be set free; it had to be worked out. Jefferson was distraught when Franklin edited out his call for ending slavery.

An evident lover of words, Isaacson takes the reader through the Greatest Sentence one word at a time. He then provides a full and, for me, fresh discussion of Franklin’s strong intellectual leadership and, with that, offers a vivid portrayal of Franklin himself. We learn, for example, that Franklin was an extraordinarily generous philanthropist, contributing to every Philadelphia church, the largest financial supporter of the Jewish synagogue, and a backer of a venue that welcomed Muslim speakers. Going beyond this, we also learn more about Franklin’s interaction with leading Scottish Enlightenment thinkers, with whom he held his own. It turns out that for Isaacson, Franklin is far and away the hero of the story. I note that the author also explores the before and after that accompanied the founding event. We learn more about the thoughts of Thomas Hobbes, Jean-Jacques Rousseau, John Locke, and George Mason as they shaped thinking on the rise of order and freedom. As to the afterword, Isaacson examines briefly the growth of the US economy and probes the purpose of economic growth and how ordinary people may become winners or losers in a globalized economy.

As we celebrate America’s founding and contemplate the Greatest Sentence, we do so knowing full well that the sentence was made great not by its words alone but by the fact that it represented the will of the people, as articulated by a small group of powerful thinkers who understood that freedom is about the pursuit of happiness. I leave a final and much-appreciated feature of Isaacson’s book: It was printed using the same typeface that produced the 1776 Declaration of Independence. Franklin picked Caslon, a typeface first produced in London. It makes the piece all the more authentic.

Washington Post columnist Shadi Hamid’s 2025 The Case for American Power is exceptional for several reasons. First, the book is a well-written and well-reasoned scholarly effort to shed meaningful light on the current global power struggle and where things may be headed. Second, the author is a noted Muslim writer, and he recognizes that this, as he suggests, may be a turnoff for some readers. He is also sensitive to government attempts to limit migration for people who share his religious beliefs. I find his discussions strengthened by his cultural distinctiveness. Third, and perhaps most important, the book reflects a revolution in the author’s thinking. Prior to this effort and deeply influenced by 9/11, Hamid opposed endorsing the use of hard power by the United States to influence world outcomes; he was a soft-power advocate. Though disillusioned by recent wars, he once saw America as being capable of promoting world peace. That changed, perhaps while writing this book. Instead, calling for the United States to assert itself as a world power, Hamid demonstrates an even greater commitment to America’s traditional values and democratic principles.

The Case is timely. The US is currently entangled in a bombing war against Iran, has threatened Cuba with violence, has removed Venezuela’s president and his wife by force and taken control of that country’s petroleum industry. Under Trump’s leadership, the nation has threatened to take Greenland “one way or another” and, even before all this, suggested that Canada should become a 51st state. And, to top it off, Trump has embraced command-and-control tariffs to manage the US economy and punish those who fail to embrace the use of power. If these acts do not reflect a raw show of power, it is hard to know what would.

All of this is relevant to Hamid’s discussion, but he seeks to make an even more troubling point. Supported by polling data, which he provides, Americans are no longer deeply in love with their country. As he puts it, we don’t like ourselves as much as we once did. Coincidentally, this point is also reflected in annual happiness surveys, where the most recent one America ranks 23rd out of 147 countries, after years of placing in the top 20. Hamid discusses his personal turning point, citing 9/11 and the associated attacks on key U.S. targets. But unlike earlier periods, when people abroad were turned off by “ugly American” behavior, Hamid argues that now it is Americans themselves who, contrary to the words in Lee Greenwood’s song, are not “proud to be an American where at least I know I am free.”

Hamid discusses love of country and points to a problem. He notes that the “problem with love is that it can easily devolve into something darker … when one feels betrayed by the beloved” (59). Still, it is love of country that causes him to call for patience, suggesting that “this, too, will pass.”

So, given these troubled times and lost love, how does Hamid make his case for American power? Even with his concerns about the dominance of hypocrisy in things political, Hamid brings to the fore American exceptionalism as stated in the Declaration of Independence and still embraced in our deeper actions. As he sees it, no other nation called out to the world a revolutionary dream that “all men are created equal and endowed with their creator with certain unalienable rights.” He invokes Alexis de Tocqueville’s observation that for Americans, democracy is akin to a religion (91).

Hamid concludes that there are times when power will be required to demonstrate that America’s free people are still willing to sacrifice and die for the sake of freedom. He points out: American power is…the product of American choices. And those choices can change. That’s why we have elections, and that’s why any single election, however dispiriting the result, is never the end of the story” (185). In a profound way, Hamid is grappling with Martin Luther King Jr.’s phrase, “The arc of the moral universe is long, but it bends toward justice.” Hamid joins Walter Isaacson in noting that the arc doesn’t bend itself; someone has to bend it.

I am not much of a fiction reader, so it is rare that a novel comes in my hands that I literally can’t put down. Allen Levi’s 2023 Theo of Golden fills the bill, and based on my own reading experience, and that of others to whom I have given the book, I believe that Levi has written a classic that, by definition, will live on and grow in stature over time. As with most beautifully written and inspiring literature, it is difficult to explain the book’s power.

Levi’s first, the novel was initially self-published. As the book circulated, it caught the eye of Simon & Schuster, which published it, and it quickly became a New York Times best seller. The book’s lead character is Gamez Theophilus Zilavez, who understandably prefers to call himself Theo. He is a man in his eighties, most recently from New York City, but originally from Portugal. By his actions, Theo is obviously wealthy, widely traveled and highly educated in art and music.

Theo proves to be a lover of mankind, a gifted conversationalist, and a genius at diverting conversations away from himself, which means the reason for his visit to Golden is slow to surface. Focusing on people’s faces, and especially eye-to-eye contact, Theo teaches how respect and kindness can bring rich friendship and joy. Through conversation and action, he shows that it is possible for the last to be first, and the first last. Fundamentally, but without putting the idea in bold-faced type, the book is about love of one’s fellow man.

Theo arrives in a small southern town, Golden, with small restaurants, book and bike shops, and a well-known coffee house that features the talents of local musicians and one special artist whose 92 charcoal portraits of local residents hang on the wall. Each of the drawings becomes a vehicle for meaningful conversation. Most of the book’s action takes place along a river with ample space for walking and finding a park bench for leisurely conversation with an interesting mix of ordinary people. For those who know the town, Theo’s Golden looks a lot like Columbus, Georgia, where Levi was born.

As the book unfolds, the reader becomes engaged with a number of those whose portraits hang on the coffeehouse wall. There is a homeless street person, an African American janitor with a seriously ill daughter, a hungry cellist, and a street-based guitar player, and the artist himself. Each of these—and more—become the subject of bench-based street conversations that reveal a lot about what may be fundamentally important in life’s struggle. Theo teaches a lot as the story unfolds. You will not want to put it down.

Notes

[1] This section is based on Bruce Yandle, “Will Another Wave of Tariff Uncertainty Hold Economy Back?,” Real Clear Markets, March 3, 2026.

[2] This section is based on Bruce Yandle, “The Iran War Triggers the US Economy’s Engine Light,” TwinCities.com, May 12, 2026.

[3] Based on Bruce Yandle, “Trump’s New Budget Signals the Demise of ‘Liberation Day,’” The Hill, April 18, 2026.