- | Regulation Regulation

- | Policy Briefs Policy Briefs

- |

The Economic Situation: March 2026

Economic uncertainty, a widening K-shaped economy, tax refund inflation risks—and Trump's conscience through an Adam Smithian lens

Getting Started

Just as we were completing this report, the Supreme Court ruled that the broad-based tariffs imposed by the Trump administration in April are illegal. The ruling raises uncertainty as to if and how Trump will replace the tariffs, if the $140 billion of collected tariff revenues will be returned to the importers who paid the tariffs, and how major trading relationships will change. To put it mildly, the Court decision’s impact is large and difficult to sort out. That sorting out must come later. For now, we address only what is unaffected by the Court ruling.

We begin with the national economy and GDP growth. When the Bureau of Economic Affairs raised its final third-quarter GDP growth estimate to 4.4 percent and noted that inflation was holding steady, many economy watchers exhaled and leaned back—at least momentarily. Then, falling exports, a government shutdown, and terrible weather took a temporary (we hope) but serious toll. The fourth quarter’s first estimate came in at a very weak 1.4 percent. Still, one had to ask: “What was driving the third quarter’s exceptional growth?” How can one square 4 percent real growth with an economy that shows hardly any employment growth? After all, the 2025 economy hardly produced any jobs, and GDP is produced by people! Just 181,000 jobs were added in 2025, and manufacturing lost 108,000 jobs. Is this really the beginning of Trump’s promised golden age?

Recalling that real GDP growth is determined by gains in total hours worked plus growth in labor productivity yields an answer. Productivity improvements generated by AI, record-setting new business formations, and investments in related power generation must be a major part of the explanation. Productivity growth for the third quarter came in at 4.9 percent; by comparison, a year ago the value was 1.9 percent. Reductions in taxes and regulation may be another part of the answer. If this is the case, we should expect GDP forecasters to be raising their estimates for 2026. And that is exactly what we are seeing.

Table 1 shows quarterly real GDP growth estimates for 2026 for three forecast groups I regularly follow. It’s important to note that The Wall Street Journal and Wells Fargo estimates surfaced in January. The Philadelphia Fed’s forecast was produced in November 2025. The contrast between early and late forecasts is striking but commonly seen. We should also note that there is no recession expected by the forecasters, but the pace of output is much slower than the growth we saw in 2025’s third quarter. The reason? The forecasters indicate that they expect Trump’s tariffs to begin to bite.

The geographic imprint

We observe a slowing economy when we look at the change in state coincident indicators for the 50 states. Figure 1 shows charts for July 2025 and December 2025. I note that December has fewer higher-growth states than July.

I now present second-quarter, year-over-year growth in state employment for 2025 and 2024. Figure 2 shows a dramatic difference across the states. Every state posted growth in 2024 (shown in blue), but 2025 is markedly weaker. The picture is even darker for state manufacturing employment.

How this report is organized

This report has four remaining sections. The next focuses first on economic uncertainty and then on disruptions that have occurred in labor markets and the larger macro economy. This is followed by a discussion of the resulting K-shaped economy, which is to say, a macro economy with sharply different sectors with respect to full or just partial participation in the nation’s prosperity. The third section puts the spotlight on the pending income tax refund or forgiveness included in recent legislation and promised by Trump. The section asks if the tax refund will generate self-defeating inflation, as it occurred when the Biden administration sent government checks to soften COVID’s pain. Then, section four asks about President Trump’s conscience and if Adam Smith’s notion of the impartial spectator will help us understand Trump’s behavior. A short book review is found in the final section.

Assessing the Situation

The Trump administration has held office for a year now, and there has been far more rattling of the global timbers than anyone could have anticipated. Trump never seems to rest and also seems to believe that a better world will be born out of chaos, not from peaceful, reasoned, behind-the-scenes discourse. Indeed, commentators have noted that cabinet meetings look like reality TV shows, an activity in which Trump has considerable experience and expertise from his years producing The Apprentice.

Trump’s actions have generated dramatic changes in the daily Economic Policy Uncertainty Index shown in figure 3. The Index is produced by researchers who monitor the occurrence of certain keywords in newspapers worldwide.

Policy uncertainty shot skyward in April 2025 when Trump announced the start of what turned out to be an on-again, off-again trade war. Although ruled unconstitutional on February 20 by the Supreme Court, Trump’s April tariff plan is being revised. Tariffs are still Trump’s principal foreign policy tool to use in going after nations that fail to say yes to his proposals or that buddy up with his avowed enemies. As a result, uncertainty has bounced along a higher 2025 path, hitting a recent high point following Trump’s late-January speech at the Davos World Economic Forum. Generally speaking, high uncertainty introduces precautionary delays that take a toll on long-term capital investments, especially those that are not readily reversed. Pale by comparison to earlier years, most recently, the US Census Bureau reported November 2025 year-over-year growth in non-defense capital goods orders at 5.6 percent; it was just 0.8 percent in April. But as new policy boulders hit the economy, here at home we’ve witnessed a full-scale churning of labor markets that might be compared to a brutal version of children’s musical chairs. Let’s see where the analogy takes us.

Musical chairs, anyone?

Do you remember the game?[1] Chairs were set in a row, one for each seated child, and there was someone playing an old upright piano. With the start of the piano music, the children would rise and rush around the chairs until the music stopped. While the children rushed around, a friendly adult quickly removed some of the chairs. When the music stopped and the children had to find a chair to sit on, some screaming children learned they were out of the game. They lost their jobs. Others got seated, smiled, and waited for the music to start again.

In January a year ago, a high share of the US labor force was employed—164 million were at work, sitting in their chairs. The unemployment rate stood at 4.0 percent, and there were 0.9 job openings for every unemployed person. Then, the music started, chairs began to be shuffled, and the players moved around, hoping that when the music stopped, they again would be seated (employed). But alas, jobs were disappearing faster than they were being added. The November 2025 employment head count showed 160 million were still in the game, the unemployment rate rested at 4.4 percent, yet there were 1.1 job openings for each unemployed worker.

But the music was still playing!

Taking a closer look at 2025, in the early part of the year, Elon Musk’s DOGE activities, directed toward reducing federal employment and spending, drew lots of attention. The Trump administration initially promised to find savings of more than a trillion dollars by November; then it was just one trillion. But when the effort was in the throes of actually being made, the goal fell to $150 billion. What actually was pocketed in savings may be counted in the billions, or even nothing.

But what happened to the federal workforce? In January there were approximately 3.0 million employed. When November rolled around the count stood at 2.7 million. Ten percent of the employment chairs had disappeared. On another front, there were lots of deportations and raids by ICE during 2025. What about foreign-born workers on private payrolls? In January, the most recent data point, the count was 31.7 million, almost exactly the same as in January 2025. No growth.

Putting the spotlight on manufacturing, with great fanfare, the Trump administration trumpeted a commitment to making American manufacturing great again. The high-ranging tariffs announced in April were justified partly by the need to protect essential US industries. Then, to the tune of $10 billion, major investments of taxpayer dollars in steel-making, minerals, and semiconductor industries were also announced during the year. There was lots of musical chair action.

But if the goal was employment gains, the result was disappointing. In January 2026 total manufacturing employment stood at 12.593 million workers, a bit shy of where it stood in January 2025. Stagnant manufacturing employment was accompanied by job losses for port and warehouse workers affected by falling import-export activity. Obviously, boosting industrial employment in a world with record-setting AI investment and growth in labor productivity is like trying to swim upstream just below Niagara Falls. That leaves the economy’s services sector, for those looking for employment growth. In January 2025, that sector had 136.7 million workers on board. The January 2026 count stood at 137.1 million. But job growth in services was far more pronounced than this overall number suggests. According to Federal Reserve Bank of Philadelphia president Anna Paulson, almost 90 percent of all private payroll growth through November of last year occurred in a single sector: healthcare and social assistance.

What about the effect of all this churning on the prospects for US worker earnings classified by their educational attainment? Has additional education systematically led to higher wages at all levels of attainment? High school? College and beyond? Looking at growth in median wages across recent years, including the current period, for workers 25 and older by education category, Timothy Taylor finds that workers with less than a high school diploma have seen the highest gains, outpacing every other education category. The next highest is for high school graduates. Lower growth in median wages has accrued to those with some college or associate degree holders, where growth in median wages has weakened. But the more troublesome trend is seen recently for bachelor’s degree holders, where growth in median earnings, which has a strong prior record, has flattened.

For almost a year now, labor markets have been beset by what looks like a game of government-managed musical chairs. As in any game, there have been winners and losers. But in this game, outcries and political pressure can affect how the game is played, when the music stops, and how the chairs get reshuffled. But no matter how loud the music or how fervent the shuffling of chairs, when it comes to employment, America’s economy is still, and will be, a services economy, and one that seems hungry for workers equipped for the new AI-driven world.

Chugging Along in a ‘K-shaped’ Economy

People are talking about America’s “K-shaped economy,” so named because a visual rendering of GDP, or income growth, shows different sectors’ fortunes diverging like the arms of the letter.[2] The K’s rising leg accounts for fact that more than half of American households who have a retirement account invested in the market. Those households comprise a segment of the population that has experienced unusual gains in stocks, bonds, and housing values and has benefited from post-COVID employment changes.

Perhaps lifted by the performance of the shares of the “magnificent seven”—Apple, NVIDIA, Microsoft, Amazon, Tesla, Alphabet, and Meta—investors who stayed in the market had a good year. Driven largely by Alphabet and NVIDIA, the “seven” rose an average of 27.5 percent in 2025, compared with the S&P 500’s rise of 17.9 percent. As to effects of the continued bull market, 2024 data analyzed by the Swiss bank UBS show that the United States had almost 24 million millionaires, with 1,000 joining those ranks every day.

As recently noted in The Wall Street Journal, “the share of US household financial wealth derived from stocks has never been so high,” and that has helped keep retail sales soaring. Indeed, about half of consumer spending comes from the top 10 percent of households by income. And that group holds more wealth than all those below them taken together. These Gatsby-like households are often employed in a handful of sectors that have done unusually well: health care, education, information, and commercial investment (which should be read as “data center construction,” a key topic to be discussed later).

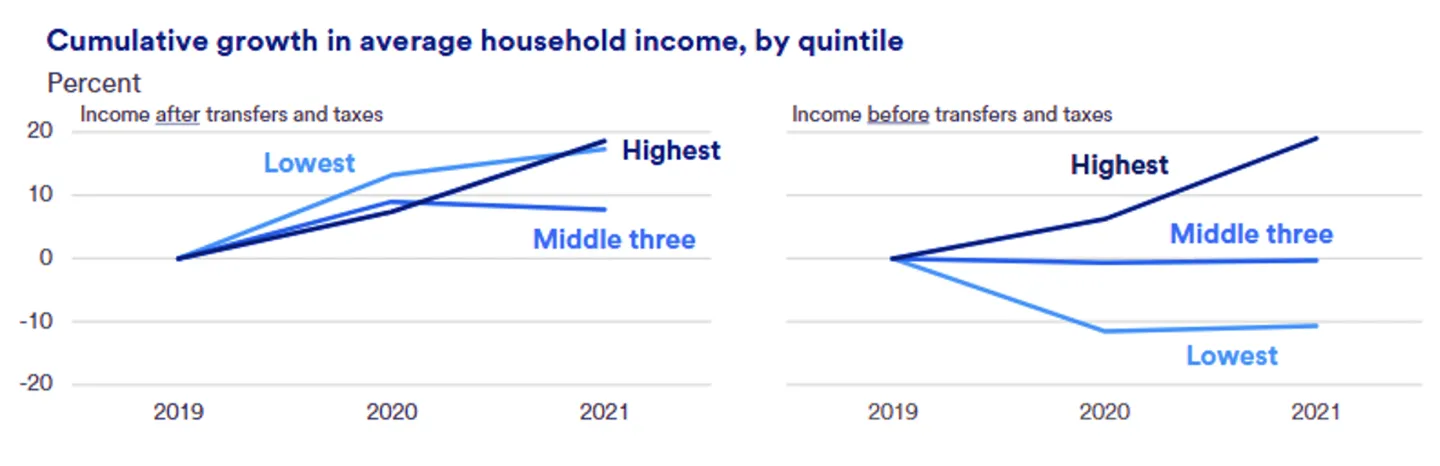

We see a graphic rendering of household income from 2019 through 2021, before and after welfare transfers, in figure 4. Note the acceleration of the highest quintile and the lost ground of the lowest quintile in the right-hand panel. Then compare this with the left panel, and note how the lowest quintile gains ground when welfare adjustments are included. But it is the unmoved middle quintile that captures our attention. This 20 percent of all households is frozen in time. They have experienced no meaningful gains. In a sense, they are the “forgotten man,” the person who goes to work every day, pays taxes, votes, seldom complains, and hopes to keep their job.

FIGURE 4. Changing relative income positions

Source: Beth Ann Bovino and Matt Schoeppner, “The K-economy in 2026: Same story, New Amplifiers,” US Bank, Economic Commentary, January 7, 2026, https://www.usbank.com/content/dam/usbank/en/documents/pdfs/corporate-a…;

The K’s falling leg accounts for those in the workforce who have seen little to no gain in real income, are managing rising credit card debt, and unlike their wealthier fellow citizens, have suffered employment and income losses from the COVID shutdowns. We see the results of the weak leg in some recent data. For example, the data services firm ADP reported 32,000 lost US jobs in November—a sharp reversal from October’s 47,000 gain, but not unexpected. But within that data, smaller firms employing from 1 to 49 workers laid off 120,000, while larger employers added workers. The weak leg raises added concerns about the prospects for improving US social mobility—the likelihood that a child will have an income equal to or greater than their parents, a likelihood that has been declining for years in low-income communities.

Even with record-level tariffs in place to give room for more hiring, there has been hardly any growth overall in manufacturing and very little in construction. We have seen job gains in the manufacturing of auto batteries and engineered wood products, and in parts of the auto industry. Still, Americans who work in industries such as these are concerned about keeping jobs, lost purchasing power, and affordability at the supermarket. They are pessimistic about the prosperity’s prospects. Indeed, January’s Consumer Confidence reading, though up a bit from December, was 25 percent lower than a year ago. Much of the concern expressed by those surveyed centered on kitchen-table issues—high prices for groceries, energy, and insurance, and uncertainty in employment.

Age and experience play a role, too. New college grads are struggling to find jobs as AI and automation change the labor market. There are 42 million young adults wrestling with over $1.8 trillion in student debt that, under pending Trump administration rule changes, must be paid or offset by work and service.

All this and more helps explain the limping lower leg, but when the two legs are averaged together, we get better than 4.0 percent growth in real GDP for the third quarter.

How can a K-shaped economy perform so well when hiring is practically dead in the water, industrial production gains are practically zero, and health and educational services are two of America’s hottest sectors? We can hardly achieve lasting growth and prosperity on the backs of taxpayer-subsidized services.

The big drivers

The good news is that we may not have to try. That’s because of the K-economy’s big GDP producer: massive data center growth and investment in power plants to keep the centers running.

Indeed, the impact is so large that it has pushed consumption spending out of first place in explaining GDP growth. A recent study by Harvard economist Jason Furman found that excluding spending on technology-related infrastructure, real GDP growth in 2025’s first half would have been just 0.1 percent instead of the 2.6 percent ultimately reported by the Commerce Department.

Tax Refunds: Will They Be Vaporized by Inflation?

According to Treasury Secretary Scott Bessent, a late Santa Claus will continue delivering bundles of joy to US taxpayers, who will receive whopping tax refunds during 2026’s first half.[3] Some $100 billion will flow from a retroactive tax cut contained in the One Big Beautiful Bill Act passed in July. And there are some special gifts for corporate America still waiting in Santa’s sled as well. Along with cash for consumers, the legislation brings large reductions in corporate taxes.

Some think the fiscal effects of all this will be large enough to add half a point to America’s GDP growth in the first quarter of 2026. But then there’s another, more ominous, possibility: a new surge of inflation. The price of gold, long understood to be the investor’s refuge against a deteriorating dollar, is sounding an alarm. It has soared from $2,600 an ounce in January 2025 to $4,400 in December.

Will it be different this time? There’s a lot to consider.

If the story sounds familiar, it’s because not long ago—when President Joe Biden was doling out generous piles of emergency funds to taxpayers—the price of gold reacted mildly, and inflation shot through the roof a couple of years later. This time, it seems, investors are on higher alert.

Of course, there’s more to consider. First and perhaps foremost, the Biden administration was dealing with an economy suffering from a pandemic shutdown. The US Treasury and Federal Reserve Board were in cahoots. Unheard-of quantitative easing had been introduced in an effort to curtail financial panics and protect the US banking system. The Fed was directly purchasing new Treasury debt to the tune of $3.5 trillion; together, they were printing money to cover costs.

Obviously, things are different this time.

In December, the United States had $37.6 trillion in public debt on the books and holding. Because of President Trump’s efforts to gain tariff-fueled revenues and reduce the scope and pace of public-sector spending, the nation has just reached an operating point where we are spending less than we take in. According to the Bipartisan Policy Center, the federal government’s cumulative deficit for fiscal year 2026 through November was $439 billion—19 percent lower than the same time last year. Revenues increased by 18 percent and outlays increased by 1 percent from fiscal year 2025.

This may not last, but it at least offers the prospect of less debt and therefore less need to print money and fuel more inflation.

If so, why the runaway price of gold? We must remember that gold is ultimately money, a store of value universally accepted to extinguish debt. It’s also the ultimate disaster hedge. When economies and life itself become disrupted, as in the Middle East, Ukraine, Nigeria, and Venezuela, people convert assets to gold as they reorganize life. There is also a sizable and growing industrial demand for gold to be used in the production of computers and other electronic devices. Taken together, these rising demand forces are pushing the price of gold higher.

So, will the soon-to-be received fresh bundles of cash be vaporized by inflation? Or will inflation’s forces be cowed by America’s reduced need for printed money? For the next couple of years, at least, I am betting against surging inflation.

But looking farther out and considering that America has yet to definitively get its fiscal house in order, I fear that the printing press will again become a policy tool, and inflation will continue to be a constant threat against prosperity.

Will Trump’s “Impartial Spectator” Soften His Hard Foreign-Policy Edges?

The list of Trump’s extraordinary administration moves in recent days is long. He conducted an attack on Venezuela, brought President Nicolas Maduro and his wife Cilia Flores to stand trial in New York for illegal drug smuggling, and secured sway over massive petroleum reserves. Along with this far-reaching action, Trump indicated that the United States will gain control of Greenland “one way or another,” Cubans should prepare for collapse, Colombia and Mexico should tread lightly, and Iran should expect “very strong action” if protestors there continue to be executed.

Asked in an interview if there were any constraints limiting what he might do on the world stage, Trump replied: “Yeah, there is one thing, My own morality. My own mind. It’s the only thing that can stop me.” He added, “I don’t need international law. I’m not looking to hurt people.”

Some Trump critics—no matter how shocked or opposed to his actions they are—may be welcoming the thought that he, like most of the rest of us, is thinking about conscience and how it affects behavior. By no means does this assure peaceful outcomes, but it’s not unreasonable to think that it makes those outcomes more likely.

Conscience is a virtue; acting on it is also a tool of self-interest. As moral philosopher and economist Adam Smith proposed in his 1759 Theory of Moral Sentiments, we are each equipped with an “impartial spectator”—a “man within the breast”—who observes and affects our actions.[4] Smith made an implicit argument that this helps form an invisible hand, similar to that of the free market, which enables self-interested people to become more moral creatures.

The mental process Smith described, similar to what Sigmund Freud termed the “superego,” chastens what might otherwise be driven by greed, jealousy, an insatiable desire for power, and other less divine appetites. As economist Vernon Smith explains, Adam Smith’s spectator[5] develops from social interactions that result from the human tendency to desire respect, welcome the larger community’s praise and, for politicians, keep their base aligned. These form habits of the heart that lead us toward long-term gains in social settings.

But Adam Smith reminds us that each society’s or nation’s impartial spectator is endogenous to that setting, which implies that Trump’s effort to be seen as just or great is directed toward his own people. This may yield a “partial spectator.” Others must fend for themselves.

It's worth considering Smith’s more pointed comments about political leaders who seek to curry favor.

Smith says: “The propriety of our moral sentiments is never so apt to be corrupted, as when the indulgent and partial spectator is at hand, while the indifferent and impartial one is at a great distance. … When two nations are at variance, the citizen of each pays little regard to the sentiments which foreign nations may entertain concerning his conduct. His whole ambition is to obtain the approbation of his own fellow citizens; and as they are all animated by the same hostile passions which animate himself, he can never please them so much as by enraging and offending their enemies. The partial spectator is at hand.”[6]

Smith more famously explained how self-interest enables the most efficient allocation of society’s resources. Describing human action in a world where force and coercion are not an option, he remarked that it was not from “the benevolence of the butcher, the brewer, or the baker, that we expect our dinner, but from their regard to their own interest” as they earn customers through superior products and pricing.

When there is competition (or even the threat of competition) in our commercial dealings, each person’s self-interest balanced against that of others can have a positive effect on overall human well-being; indeed, it’s a necessary part of freedom’s machinery that delivers a happy outcome.

But what about the world of international politics, where force and coercion are part of the equation? Can the competing self-interests of surging and receding world leaders still lead to a balance that serves the whole? Can such a process be chastened by the “man within the breast”?

Trump’s deputy chief of staff, Stephen Miller, suggests that this is no time to rely on “niceties” to do the right thing: “We live in a world … that is governed by strength, that is governed by force, that is governed by power. These are the iron laws of the world since the beginning of time.”

As bleak as those words sound, there is another reality to acknowledge: Competition still matters. While the United States may be able through force to have its way with Venezuela, Mexico, Colombia, and Greenland, we are not the only game in town for prosperity partnering. There are other world powers—small and large—that have something to offer to these nations, or to America for that matter.

Though there are many things at play, the incentive still exists to heed the impartial spectator, sharpen our preference for peace, and lead to a more harmonious world.

Yandle’s Reading Stand

Thoughts of America’s high-paced growth in millionaires and the surging upper leg of the K-shaped economy bring to mind a classic that we may want to revisit. Fitzgerald’s 1925 The Great Gatsby colors our vision of America’s Jazz Age when, fueled partly by fortunes made from the United States’s strong global position following a devastating World War One and a Prohibition-induced underground economy, those at the top of another K-shaped economy a century ago seemed to have unlimited wealth. Fitzgerald captures the dramatic difference in lifestyles of a blue-collar couple, auto mechanic George and wife Myrtle Wilson, and that of old- and new-wealth millionaires, Tom and Daisy Buchanan and Jay Gatsby. All were pursuing their dreams.

Just a bit more than 100 pages long, the book focuses on Jay Gatsby, a mysteriously wealthy new occupant of a freshly built and richly maintained Long Island mansion. As those familiar with the story readily recall, Gatsby was single-minded in his pursuit of another man’s wife, Daisy Buchanan, whom he had known and loved earlier in his life. Fitting 1930s American self-help author Napoleon Hill’s description of a successful person, Gatsby displayed a “definiteness of purpose” and seemed to hold to the principle that what the mind can “conceive and believe, it can achieve.”

Fitzgerald is at his best describing Gatsby’s glittering lawn parties, attended by hundreds who danced the night away while enjoying a constant flow of food and champagne. All part of a tender trap to recover his lost love, who lived across the lake from his home, Gatsby’s parties ended the day he and Daisy were reunited briefly at the home of Gatsby’s neighbor, Nick Carraway, who narrates the story. Because of a tragic ending that led to Gatsby’s misguided murder, Gatsby and Daisy were not reunited. As the story ends, old wealth survived and perhaps flourished.

But Fitzgerald does more than tell a story about a K-shaped economy. His story contains an impartial spectator, a conscience of sorts, that saw all that was happening and perhaps affected outcomes. It was a billboard on the main highway from the homes of the wealthy to downtown New York City and going past the home of George and Myrtle Wilson. The billboard advertised an optician that showed a huge face wearing glasses. In the billboard “the eyes of Doctor T. J. Eckleburg are blue and gigantic—their retinas are one yard high. They look out of no face, but, instead, from a pair of enormous yellow spectacles which pass over a non-existent nose.” Dr. Eckleburg’s eyes reappear later in the novel.

As we know perhaps too well, the high-stepping Jazz Age came to an end in 1929 when the Great Crash suddenly erased billions of newly formed wealth. Should we expect the same? 2029? Let’s hope we have learned how better to manage our excesses.

Notes

[1] This section draws on Bruce Yandle, “Commentary: Workers must navigate a musical chairs labor market,” Charleston Post & Courier, https://www.postandcourier.com/opinion/commentary/us-sc-employment-land…

[2] This section is based on Bruce Yandle, “Commentary: America Chugs Along in a ‘K-shaped’ Economy,” Tribune News Service, https://www.msn.com/en-us/money/markets/commentary-america-chugs-along-….

[3] This section is based on Bruce Yandle, “Tax Refunds Are Coming. Will They Be Vaporized by Inflation?,” Tribune News Service, https://www.msn.com/en-us/money/markets/commentary-tax-refunds-are-comi….

[4] This section draws on Bruce Yandle, “Will Adam Smith’s ‘Impartial Spectator’ Soften Trump’s Hardest Foreign-Policy Edges”? The Daily Economy, https://thedailyeconomy.org/article/will-adam-smiths-impartial-spectator-soften-trumps-hardest/

[5] Background for this discussion and the Public Choice reference were provided by Professor Jody Lipford at Francis Marion University.

[6] Adam Smith, The Theory of Moral Sentiments, 1759: III.3.42–43 and III.3.44.