- | Monetary Policy Monetary Policy

- | Policy Briefs Policy Briefs

- |

The Economic Situation, September 2019

The arrival of fall brings a break in 2019’s summer heat wave; continued economic uncertainty with respect to US trade policy, deficits, and immigration policy; and a slowing US and world economy. Economic policy uncertainty seems now to have become a Trump policy instrument to be used along with regulatory, fiscal, and monetary policy to achieve political goals. Along with the uncertainty, fall also brings acceleration in election politics, with more than a score of Democrats hoping to become their party’s nominee for the White House.

Election politics generates debates and speeches in what is often called America’s crazy season. This year’s politics is generating some rather extreme proposals for “what I will do if I become president.” While political rhetoric is about what might happen, the slowing world economy is about what is actually happening.

This Economic Situation report begins with a discussion of the world economy and then focuses on the United States. Examination of data in both cases leaves little doubt that the days of better-than-three-percent sustained real GDP growth are in America’s past, at least for the next few years. The discussion of the US economy also pays attention to what is happening across the 50 states. President Trump’s use of tariffs and trade wars as instruments for achieving political goals is the focus of the report’s second section.

Turning to crazy season policy proposals, the report then addresses two proposals that, though rather extreme, may survive, depending, of course, on the 2020 election outcome. First, an increase in the minimum wage from $7.25 to $15.00 per hour over several years; second, student debt forgiveness. Once again, the report contains a section that focuses on a particular state. This quarter’s report puts New Mexico in the state spotlight. Finally, the report’s last section provides a couple of book reviews for interested readers.

Economic Outlook for the World and the United States

My description of the economic outlook for the world economy would be “slowing after a season of strength.” Using a few more words, the International Monetary Fund (IMF) put the matter this way in its April 2019 report:

"One year ago, economic activity was accelerating in almost every region of the world and the global economy was projected to grow at 3.9 percent in 2018 and 2019. One year later, much has changed: the escalation of US–China trade tensions, macroeconomic stress in Argentina and Turkey, disruptions to the auto sector in Germany, tighter credit policies in China, and financial tightening alongside the normalization of monetary policy in the larger advanced economic have all contributed to a significantly weakened global expansion, especially in the second half of 2018."

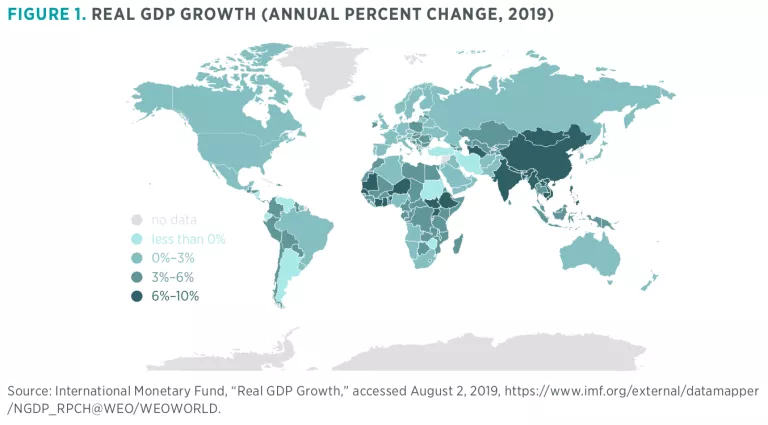

The International Monetary Fund (IMF) in April reduced its 2019 estimate for world real GDP growth from 3.5 percent to 3.3 percent—following 2018’s 3.6 percent—and, in doing so, noted that slower growth was prevalent in 70 percent of the world’s economies. Then, in July, with still more trade war weakness evident, the IMF cut its 2019 growth estimate to 3.2 percent. I note that the IMF predicts 2020 will see world GDP growth recovering to 3.5 percent.

Looking at countries and regions that together form more than half of the world’s economy, the IMF expects 2019 real GDP growth of 2.3 percent for the United States—slowing to 1.9 percent in 2020—1.3 percent for the European Union, 1.3 percent for the United Kingdom, and less than 0.9 percent for Japan. Figure 1 gives a visual rendering of how economic growth is expected to occur across the world. I call attention to the location of the high-growth economies. These are largely found in Africa and Asia.

Examination of more recent data confirms the IMF analysis. For example, recent reports on manufacturing and export data from China, the European Union, and the United Kingdom show continued weakness with trade war uncertainties, Brexit, and Europe’s generally slower economy, underlined by Germany’s negative GDP growth for this year’s second quarter. Activity in world petroleum markets also points toward weaker future prospects. Even in the face of high Middle East uncertainty, especially with regard to Iran, crude oil prices continue to fall. Indeed, the director of the International Energy Agency in July 2019 reduced the agency forecast for 2019 from 1.2 million barrels of oil per day to 1.1 million, an almost 10 percent reduction in demand.

The US Picture

As indicated in the world economic outlook discussion, the US economy, much like that of the rest of the developed world, began to slow significantly in late 2018 and at the start of 2019. While consumer spending continued to show remarkable strength, employment growth, US industrial production, and exports weakened. The Trump administration’s escalating trade war with China, threats of tariffs on Mexican imports, and additional tariff threats on European autos and even French wine raised uncertainty across the manufacturing sector. The negative effects generated by trade war uncertainties were reinforced by debates regarding reversals of Federal Reserve (Fed) interest rate policies along with the possibility of another government shutdown in association with congressional debate regarding raising the nation’s debt limit. By late July, the Fed and debt limit uncertainties were resolved when the Fed reduced interest rates by a mild 25 basis points at its July meeting and Congress passed a two-year budget bill that eliminated the risk of government shutdown. Meanwhile, trade war uncertainties and a slowing industrial economy remained in place.

The effects of these uncertainties are seen in the slowing growth in industrial production, where the year-over-year growth rate peaked in September 2018 and has diminished almost every month since then. We see a similar pattern for total employment, where year-over-year growth peaked in January 2019 and has followed a declining trend in the months since. The same pattern is observed for commercial and industrial loans made by all US banks: year-over-year growth has been falling since February 2019. Similar weakness is now showing up in transportation action. Year-over-year growth in the Cass Freight Index, which captures activity for all forms of transportation, began to decline in May 2018, entered negative growth territory in December 2018, and remains in negative growth territory today. I emphasize that I am speaking of growth rates in this discussion, not levels of activity.

These weaknesses were captured in the US Department of Commerce’s 2.1 percent second quarter real GDP growth estimate issued in July. Combining the 2.1 percent second quarter growth with the 3.1 percent first quarter growth yields a 2.6 percent simple average for the first six months, which is greater than the IMF’s predicted US economic growth rate for the year (2.3 percent) and is exactly Wells Fargo’s estimate. I should add that I am still clinging to my 2.8 percent estimate for 2019’s real GDP growth. This decline in GDP growth to pre-Goldilocks levels—less than 3.0 percent—is triggered at least partly by the trade war stance and protectionist actions taken deliberately by the Trump administration. Shrinking exports and imports (of which many are used as manufacturing inputs), declining capital investment, and delayed foreign direct investment are some of the drivers of the slower pace. Put another way, weaker prospects for future prosperity are a matter of policy choice.

Recession?

With so many key economic indicators showing weakness, the possibility of recession—two consecutive quarters of negative real GDP growth—naturally comes to fore. And there is one additional reason to pose this question. For example, the yield curve, the difference between the yield on the 10-year Treasury note and the yield on the 91-day Treasury bill, entered negative territory on May 23, a condition that often precedes a recession. Indeed, the Federal Reserve Bank of New York’s recession forecast, based on yield-curve inversion or a negative gap between the short- and long-term interest rates, has been flashing a warning signal, indicating a better-than-30-percent chance of a recession in 12 months, the largest probability since 2009.

Yet while the New York Fed model has been accurate, we must remember that yield-curve inversions are not like meteors suddenly appearing out of nowhere. They are the result of actions taken by the Fed itself. When the Fed raises rates out of concern for what it sees as smoldering inflation, the economy responds by slowing down a bit. More rate increases result in a further slowing of the economy, which reduces investment demand, which in turn leads to reductions in the 10-year note’s yield. So now the Fed, having raised rates four times in 2018 and gotten a yield-curve inversion, has reversed its position. After the Federal Open Market Committee cut rates at its July 31 meeting, the yield-curve inversion practically disappeared. The more normal yield-curve shape prevailed for a few weeks until President Trump announced suddenly an expansion of tariffs on Chinese goods. Then, after China responded with a weaker currency value, the trade war “fruit basket turnover” continued. Once again, with world GDP growth shaken, long-term interest rates fell, and the yield curve inverted. Will we see a recession—two consecutive months of negative real GDP growth—in the next 12 months? Based on what we know now, I think not. The normal election year incentives create a push to more deficit spending, less confrontational trade talk, and continued regulation relaxation, which should be enough to generate greater than two percent real GDP growth in the year ahead.

The Geographic Imprint

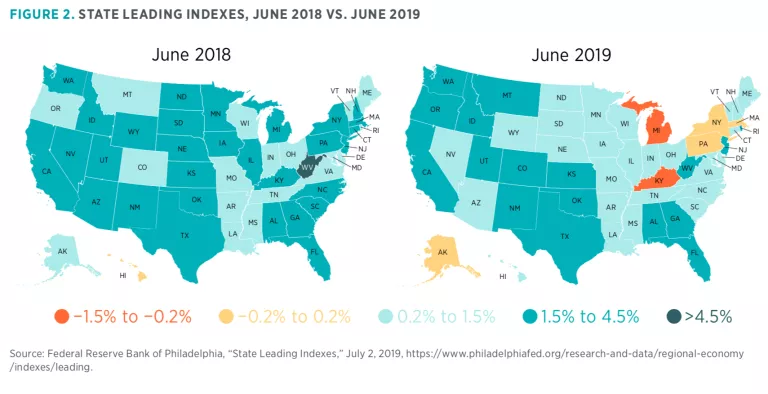

When I am asked about the future prospects for the economy in sessions on the economic situation, I often ask for a bit more guidance on the question: “For which region or state?” There is obviously a wide variation in the performance of the economy across the 50 states and, of course, within states and even counties. Indeed, I wish we had readily available data on economic growth for zip codes!

Putting that wish to one side, I can be thankful for the work of economists at the Federal Reserve Bank of Philadelphia, who produce monthly data that give a reading on leading economic indicators in every state. These data reflect expectations for growth in personal income six months into the future. I provide two maps in figure 2 based on recent data—one map for June 2019 and the other, for comparison purposes, for June 2018. Counting the darker teal states in each map tells us what has happened to future prospects in just the past year. Things are definitely not as bright now as they were then.

Examining the June 2019 map shows that Michigan and Kentucky, two leading auto states, are not doing so well. Relative weakness is also seen in the western grain-producing states.

Thoughts on Tariffs and Trade

President Trump’s enthusiastic embrace of tariffs as an instrument to be used in bringing desired changes in the behavior of US trading partners has generated a huge amount of commentary. Writing about free and fair trade recently in the Wall Street Journal, President Trump’s director of trade and manufacturing policy, Peter Navarro, took issue with some World Trade Organization (WTO) rules. He especially dislikes the rules that require member nations to avoid applying discriminatory tariff policies when trading with other WTO members. Navarro, like his boss, favors the use of tariffs as a big stick for battering other countries when their policies are unacceptable to him. Recall that the president refers to himself as “Tariff Man.”

But while Navarro’s analysis of the relative merits of WTO rules opens what could be a useful policy debate, a related statement that higher imports always lead to lower GDP and therefore less employment leaves a lot to be desired. Navarro put it this way: “But because imports don’t contribute to gross domestic product, unfair trade reduces growth, and narrowing the trade deficit through higher exports and lower imports boosts growth.”

This is, at the very least, a gross misunderstanding of what is nothing more than an accounting identity—and it explains nothing about the benefits of imports to American businesses and households. At the simplest level, the equation says GDP = Consumption + Investment + Government Spending + Exports − Imports. All this is intended to do is ensure that the data reflect where goods are produced accurately. It doesn’t mean that a country becomes poorer if it trades.

The issue of intermediate goods is a wonderful illustration of this point. An intermediate good is a component that will be made a part of a final domestic product. It turns out that in lots of cases, imports are used as a component in products that later become exports.

The International Trade Commission describes the situation this way: “Globalization of supply chains, better known as ‘offshoring,’ tends to rely on the production of manufactured goods (most of which are intermediate inputs) abroad. The intermediate inputs are commonly manufactured by either a foreign affiliate or an independent supplier and are then imported back to the United States for final assembly.”

Consider BMW, the largest exporter of US-made automobiles. In 2017, BMW exported more than 270,000 automobiles produced at its South Carolina plant. Each one of the vehicles contained an engine and transmission produced abroad that had been imported to the United States. The value of BMW’s 2017 exports was $8.6 billion, more than 15 percent of the value of all US auto exports that year. If we wish to build and export more BMWs, we must import more BMW engines and transmissions. If by presidential command we reduce the importation of engines and transmissions, we will immediately reduce our exports by a greater value. A completed BMW is worth more than a BMW engine and transmission.

This is not small potatoes. In 2016, the United States imported about $90 billion in consumer goods, $77.6 billion in capital goods, and $34.7 billion in intermediate goods. For example, Alcoa imports aluminum made by one of its own Canadian plants and uses the newly produced metal when fabricating final goods to be sold in the United States. An increase in imports for Alcoa enables US production to increase. Higher imports, higher GDP.

Mr. Navarro and perhaps other Trump administration advisers need to rethink the administration’s anti–free trade position.

Interference with Trade Is Interference with Freedom

In a recent radio interview, the talk show host I was speaking with focused on US trade policy and what might be expected from the ongoing tariff wars with China. I made the point that the Trump administration’s affection for tariffs involves more than China—that as early as April 2017, the United States had imposed tariffs on Canadian timber products, followed shortly thereafter by tariffs on Korean-produced home appliances, and then globally on broad categories of aluminum and steel.

I noted the recent on-again, off-again brush with tariffs on all imports from Mexico and recalled that very early in the Trump years, serious attention had been devoted to implementing a border tax on Mexican imports as a way to fund construction of a wall along the US southern border. I also mentioned that Trump had ordered a US Department of Commerce investigation of automobile imports and the extent to which the strong US market presence of foreign-produced vehicles might have a negative effect on the country’s ability to defend itself in event of war. And after all this, there was a threat to impose tariffs on exports from Guatemala in an attempt to get that country to cooperate in limiting immigration to the United States and a late July suggestion by the president that he might impose tariffs on French wines, or something, in retaliation for the tax France recently imposed on US technology companies.

In short, the Trump administration’s extensive trade actions cannot be explained solely as an effort to induce China and other countries to open their doors more widely to American goods. Nor are they simply about avoiding foreign trade practices that disadvantage US producers. Now, as I reconsider that conversation, I come to a broader conclusion: Trump administration tariff policies seem simply to reflect pragmatic attempts to have it the president’s way. Brandishing tariff threats and imposing them recklessly undoubtedly gives the president a sense of power. The ability to act as gatekeeper to the world’s largest economic playing field gets exercised with the offer of differing justifications for different tariffs. Meanwhile the world and US economies slow, and the once burgeoning Goldilocks economy resumes its pre-Trump sleepwalk.

Near the end of the radio interview, I was asked an excellent but tough question: What should so-called average Americans, who hear constant chatter about tariffs and trade wars and are looking for a way to determine what really hurts them or helps them, focus on?

Before getting to what might be called practical considerations, I suggested that all Americans should question the role of their government in limiting their ability to write contracts with sellers of legitimate goods and services, irrespective of the address or location of sellers. We Americans, operating in an ostensibly open, free-market economy, look to government to protect our property rights, to help adjudicate disputed contracts, and to provide security for our families, homes, and shipping lanes. We should view with skepticism any government action that limits our freedom to engage voluntarily in trade with other people. Under our system of government, any limitation on trade is a limitation on our own pursuit of happiness.

After taking a deep breath—which the host probably appreciated—I turned to the practical part of the question: First, look closely at what happens to the cost of housing and the prices of automobiles and appliances, at employment growth for exporting and importing employers, and at the prices Americans pay for small-ticket items, which more often than not come here from China.

Plenty of consumers may do that, see slightly higher prices, and find little to be all that alarmed about, but that doesn’t mean that limitations on free trade impose a trivial cost on ordinary people. Price increases of a few nickels and dimes on a host of consumer goods for a few hundred million consumers can generate a huge total loss, but one that is still almost hidden to the eyes of one consumer or even one family. Moreover, a family of limited means may pay hundreds or thousands more for everyday items over the course of a year without realizing where its money went.

Now assume for the sake of argument that a search for the costs of tariffs on goods that US consumers buy from Canada, China, Germany, Mexico, or elsewhere turned up nothing. Even if there is yet another cost, any people denied the ability to buy the items they prefer have borne it.

The American dream is about freedom. Americans should be sensitive to any loss of freedom at the hands of government and wary of justification for such curtailment.

Crazy Season Promises

It’s crazy season in Washington, which is another way of saying it is a time when presidential hopefuls are making extravagant promises in their efforts to secure nomination. Almost inevitably, proposals to raise the federal minimum wage from its current $7.25 per hour enter the ongoing debate among potential candidates for office. Joining minimum wage this year are promises regarding relief of student debt, which, of course, represents a real bonanza for millions of college students and graduates who still owe some if not all of the money they borrowed.

The Raise the Wage Act

The Raise the Wage Act, which was introduced in the Democrat-controlled House of Representatives in January and passed by the House of Representatives, 231 to 199, on July 18—largely along party lines—would raise the federal minimum wage from the current $7.25 per hour, where it has been stuck since 2009, to $15.00 in 2024. Senate Majority Leader Mitch McConnell (R-Kentucky) immediately indicated that the Senate would not be taking up the matter. Anyone fresh to these shores, with no knowledge on the topic, reading about the low minimum wage would likely be shocked: “Do you mean to say the US minimum wage is $7.25 and has not been changed in 10 years? How do entry-level workers make it?”

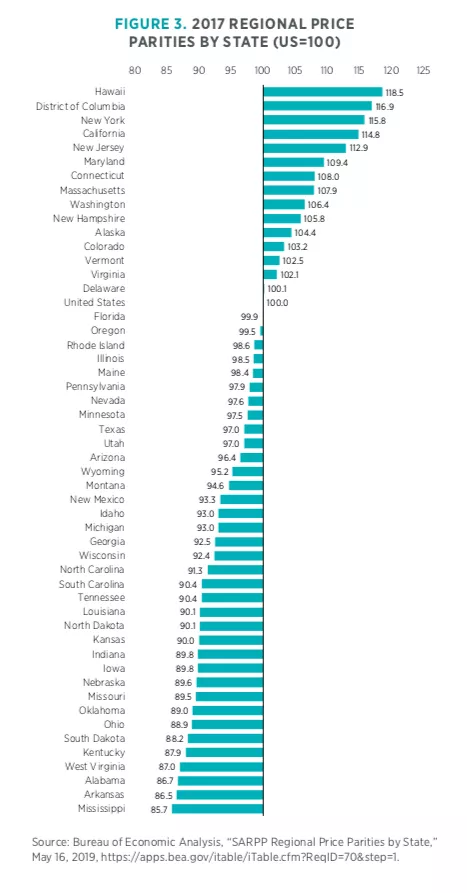

There is obviously far more to the story. First off, in 2017, according to the Bureau of Labor Statistics, just 542,000 out of 84 million US wage earners were paid $7.25 per hour. Of course, any one of these would be happy to see a paycheck based on a $15 hourly wage. Then, any state or municipal government can independently establish its own unique minimum wage laws. For example, in January 2019, some 30 states and the District of Columbia had minimum wage mandates that exceeded the federal level. These range from a high of $13.25 in DC to $12.00 for California and Massachusetts to $11.10 for Colorado and New York, to $10.10 in Connecticut and Hawaii. As might be expected, differences in the mandated state wage levels closely reflect differences in state cost of living.

Consider the comparative cost-of-living data in the accompanying US Department of Commerce chart (see figure 3). Data points for each state show how a state’s cost of living compares with the US average. As can be seen, Hawaii, the District of Columbia, New York, and California are positioned at the top of chart. Their living costs are more than 14 percent higher than the US average. As just noted, their minimum wages are also substantially higher than the $7.25 US minimum. At the lower end of the data one finds states that have living costs that are substantially lower than the US average. West Virginia, Arkansas, and Mississippi rest at the bottom of chart. The minimum wage rates in those states are $8.75, $9.25, and $7.25, respectively. I note that the federal $7.25 minimum applies in another large group of lower-cost states: Alabama, Georgia, Idaho, Indiana, Iowa, Kansas, Louisiana, North Carolina, North Dakota, Pennsylvania, South Carolina, and Wisconsin.

Of course, there is more going on here than just cost-of-living differences. But generally speaking, market-determined wages that influence state minimum wage laws reflect differences in the cost of living. Wise politicians know this.

So what’s going on with Congress? Why not leave it to the states to set the floor for wages? After all, those at the state level would seem better situated to assess local living costs and other relevant costs. Is it all “sound and fury, signifying nothing”?

Probably not. A second glance at figure 3 will identify which states will be punished most in the struggle for economic development if their minimum wage laws are required to be set at $15.00. Obviously, if that came to pass, lower-cost states would lose their competitive advantage, and high-cost states could be less concerned about the outmigration of people, industrial plants, and corporate headquarters.

In a July 2019 study, the nonpartisan Congressional Budget Office (CBO) estimated the employment and income effects of the proposed Raise the Wage Act. According to CBO, the 2025 increase to $15.00 an hour would lift the incomes of 1.3 million workers above the national poverty level but would have a two-thirds chance of eliminating employment for as many as 3.7 million US workers. Senator McConnell referred to the study when he indicated there would be no Senate vote on the matter. How much would the below-poverty family gain? By 2025, the average below-poverty family assisted by the law would see a $600 increase in annual income. CBO points out that this income increase comes at the cost of lost income for the newly unemployed, higher consumer prices induced by the higher wages, and lower earnings from businesses affected by the higher wage mandate.

Undoubtedly, elected officials who support the Raise the Wage Act know all this. Yet they have chosen a seemingly high-cost way to, as they see it, improve the well-being of US low-wage workers. Why might that be the case?

First off, a Raise the Wage Act is easy to understand and sends a popular signal to supporters. Those running for office can say, “Elect me, and I will do my best to raise the minimum wage, and will do so by passing a law.” Enough said. And then there may be an unstated bootleggers-and-Baptists goal that Raise the Wage Act supporters hope to achieve. Remember, in the analogy, both bootleggers and Baptists support laws that close liquor stores on Sunday, but for different reasons. In this case, it could be that higher minimum wage laws assist organized labor in districts and states that have to compete with low-wage workers. A higher minimum wage enforced by federal law will make life a bit easier for union officials to collect more union dues. But what about the surveys and polls that show strong support for higher minimum wage laws. What are we to make of them? Most decent people prefer higher to lower wages for themselves and their neighbors, and when asked they will tend to take the opportunity to express their ethical preferences. But it seems that most decent people also don’t like laws that cause people to lose their jobs. With more information of the sort found in the recent CBO study, the Raise the Wage Act should be in for some rough sledding.

This may be the time for the states to continue to show minimum wage leadership, and that could be “the right kind of nothing” for raising the federal minimum wage.

Is There a Student Debt Crisis?

Senator Elizabeth Warren (D-Massachusetts) and Representative James Clyburn (D-South Carolina) recently signaled their plan to introduce legislation that would forgive up to $50,000 of student loan debt for 42,000 former students, or about 95 percent of debt holders. They claim that recent graduates, on average, leave college owing $30,000 or more. This debt bonanza would be funded by a wealth tax on America’s super rich. Now another candidate—Senator Bernie Sanders (I-Vermont)—has jumped in with a bonanza of his own.

Are Americans drowning in student loans? Should we should prioritize debt relief above any number of other spending priorities? The numbers say no, whether or not it turns out to be a winning political issue.

Echoing a statement she’s made many times while campaigning for president, Senator Warren said, “The student debt crisis is real and it’s crushing millions of people—especially people of color. It’s time to decide: Are we going to be a country that only helps the rich and powerful get richer and more powerful, or are we going to be a country that invests in its future?”

Not to be outdone, Senator Sanders upped the ante and promised that, if elected president, he would cancel all $1.6 trillion in student debt and get the funds for doing so by imposing a fee on all stock and bond transactions.

Well, either way, all those who hold student debt should be overjoyed. Who wouldn’t be?

They, on average, are educated and employed in one of the world’s strongest economies. According to the Social Security Administration, the median bachelor’s degree holder can expect to earn $650,000 to $900,000 more in a lifetime than those with just a high school diploma. And to get to this enviable position, he—voluntarily—borrowed money as a student and is now in the payback period.

But let’s push away the emotion and campaign rhetoric for a moment. The fact that a lot of Americans found it in their best interest to borrow money to pay for college tuition doesn’t mean there is a “crisis” that is “crushing millions of people” any more than does the fact that lots of young American adults feel compelled to borrow money for SUVs or condos. We should probe deeper.

What about student loan delinquencies? Are they going through the roof?

According to data maintained by the Federal Reserve Bank of New York, the 90+ day delinquency rate on student loans has been relatively constant at 12 to 13 percent since 2012. There is no sudden increase. Indeed, if some former students have slowed in paying back loans, it may be because they expect some of their debt to be forgiven.

What about the loans themselves? Has the lending pace quickened in recent years? And is it true that US students, facing unusually high tuition charges, have had to engage in more borrowing in pursuit of that $900,000 lifetime earning premium?

According to data from the College Board, a nonprofit seeking to expand access to higher education, 58 percent of bachelor’s graduates from public universities in the academic year 2016/17 had a student loan, and the average amount of their debt was $15,500. Ten years earlier, the share with a loan stood at 55 percent, a bit lower, and the average amount owed, adjusted for inflation, was also a bit lower, at $12,400. For graduates from private universities, 61 percent held debt in 2016/17, and the average loan was $20,000. A decade earlier, the share with debt was higher, not lower, at 66 percent, and the average loan was nearly identical at $19,900.

Sen. Warren’s $30,000 figure emerges when graduate degree recipients are included. Debt is much higher for those graduating from medical colleges, law schools, and other graduate programs, but so are their expected earnings.

And so, what are we to make of this student debt crisis? Is it about students or politics? And if officials impose a wealth tax for the purpose of erasing student debt, why not housing debt? Or car debt? Or hardships that hit people out the blue, such as hospital debt?

Maybe we should leave well enough alone and let those good folks who signed the dotted line on a loan application bear up and pay up.

New Mexico in the State Spotlight

Senior Research Fellow and Director, Policy Analytics Project, Mercatus Center at George Mason University

Data Engineer, Policy Analytics Project, Mercatus Center at George Mason University

Each quarter, we select one state and assess that state’s economic outlook and health. Last quarter, we put Missouri in the spotlight. In previous quarters, we have examined Colorado, Hawaii, Illinois, Kentucky, Michigan, Nebraska, North Carolina, Oregon, and Utah. We focus on New Mexico this quarter.

When one examines New Mexico’s economy, it is helpful to recognize that one-third of the state’s land is owned by the federal government. This obviously affects overall economic activity. Historically, New Mexico’s economy has performed well below the state average owing to a pedestrian industry growth, poor income per capita indicators, and a workforce that has a propensity to migrate to neighboring states. An example of one of these trends is New Mexico’s manufacturing industry, a sector that is extremely important for economic growth. Since January 2009, New Mexico has seen a 14 percent decrease in employment in its manufacturing industry. This has not been the case for the neighboring states of Arizona and Wyoming, who saw an 8.7 percent and 9.8 percent increase in employment, respectively.

Personal income per capita is another metric that highlights these trends. New Mexico saw low growth in income per capita from 2009 to 2017, at 21.61 percent. While this may seem high, neighboring states Colorado and Arizona experienced 37.13 and 27.86 percent growth, respectively, and the United States as a whole experienced a 32.15 percent increase over the same span. Economists in New Mexico are well aware of the state’s economic struggles. Think New Mexico, a respected think tank in the state of New Mexico, states,

"Between 2007-2011, over 3,000 businesses and 43,000 jobs vanished from New Mexico. In 2012, the state’s economy grew by only 0.2%, the 47th slowest rate in the nation, while the economies of all of our neighboring states grew at least 10 times as fast. As a result, over 137,000 New Mexicans (14.7% of the workforce) were unemployed or underemployed in 2012, and an increasing number were leaving the state to seek work elsewhere."

However, the past few years have shown some promising signs of growth for the state, driven mainly by growth in the oil and gas extraction industry. Some have even gone as far as saying that the state’s economy has shown more strength than any other state’s economy since Trump’s election. Many of the positive and negative components of New Mexico’s economy will be discussed in this report, including an analysis of major industries, major economic factors, regulatory burden, and future economic indicators.

The industry that seems to be driving the recent success of New Mexico’s economy is classified by the Bureau of Economic Analysis as “Mining, Quarrying, and Oil and Gas Extraction.” This industry has grown from $5.96 billion to more than $9.65 billion from 2016 to 2018, in terms of GDP contribution. Specifically, the oil and gas subcomponent is what is driving the majority of the larger industry’s growth. The 62 percent increase in the oil and gas industry by far dwarfs any other industry’s growth in the state over that same span.

But there are other industries showing remarkable growth. For example, from 2016 to 2018, the finance, insurance, real estate, rental, and leasing industry is the largest industry in the state and has experienced GDP growth from $15.50 billion to $16.58 billion. The second-largest industry in the state, professional and business services, grew about 10 percent, from $9.71 billion to $10.72 billion in GDP terms during the same time period. While neither of these industries recorded large growth, they both contributed to the state’s 10 percent overall GDP growth since 2016.

Other components of New Mexico’s economy do give some mixed signals. As of 2018, residents of New Mexico had the lowest per capita personal income in the United States, resting at $36,814. However, this may be partially balanced out by New Mexico having the lowest annual cost of living per person among all states, at $41,338.

Education may also be an area of weakness for New Mexico, as the state is tied with Arizona for having the lowest high school graduation rate in the United States, sitting at 72 percent. Only 26.7 percent of the state’s 25-year-old-or-older population has bachelor’s degrees, giving New Mexico a rank of 36 among the United States.

While New Mexico’s economy has grown over the past few years, the state’s unemployment and fiscal statistics paint a weak picture. The Mercatus Center’s 2018 fiscal rankings mark New Mexico as the 45th healthiest state (fiscally), citing the state’s service-level solvency as its largest problem. New Mexico also has a high ratio of debt to state personal income. The state’s 4.9 percent June 2019 unemployment rate places it 48th out of the 50 states and the District of Columbia.

As might be expected from the earlier discussion, New Mexico metro areas do not rank among the nation’s leading cities. Policom Corporation, an economic research organization, ranks the economic strength of metropolitan areas based on a large number of economic indicators. New Mexico contains 4 of the 383 metropolitan areas ranked by Policom. For 2019, Albuquerque ranked at number 288, Farmington at 355, Las Cruces at 290, and Santa Fe at 289.

New Mexico’s Regulatory Outlook

New Mexico’s regulatory code is published by the Commission of Public Records and is housed on the State Records Center and Archives webpage. New Mexico’s administrative code spans across 22 titles that are organized based on subject rather than by department, as is typically done. Organizing by regulatory topic avoids duplicative regulations and enables businesses and other interested parties to find relevant regulations more quickly.

While New Mexico’s regulatory code may be better organized than most other state regulatory codes, its code is larger than the average code. New Mexico’s code contains 9,245,344 words and would take almost 515 hours to read. This makes New Mexico’s code the 17th-largest out of the 41 state codes examined by the Mercatus Center’s State RegData project.

Out of the 35 state codes that have been analyzed by State RegData, New Mexico has the 18th-largest count of restrictions. These are words that are legal and binding in nature and include terms such as shall, must, may not, prohibited, and required. New Mexico has 125,395 regulatory restrictions as of 2018. The average count for the 41 Mercatus-analyzed states rests at 136,721.

New Mexico’s largest title is Title 20, “Environmental Protection,” with 19,948 restrictions. However, New Mexico’s most regulated industry, as classified at the three-digit North American Industry Classification System (NAICS) level, is not related to the environment. This industry is ambulatory healthcare services (NAICS 621), which has 4,928 relevant restrictions in New Mexico’s code.

Every state is also affected by federal regulations. This effect can vary from state to state based on the mixture of industries in each states’ economy. The Mercatus Center’s FRASE Index, which measures the effect of federal regulation on state economies, ranks New Mexico close to the middle of the pack, experiencing the 27th-lowest impact of federal regulations out of all 50 states and the District of Columbia.

Conclusion

Even though New Mexico’s economy is showing recent strength, other indicators, including future economic indices, paint a different picture. For example, the Federal Reserve Bank of Philadelphia’s state leading indicator, which is based on expected personal income growth six months ahead, puts New Mexico slightly above the average state. However, the New Economy Index for 2017 ranks New Mexico as 34th out of all 50 states with respect to knowledge jobs, economic dynamism, globalization, digital economy, and innovation capacity.

Yandle’s Reading Table

I am taking a different tack in my discussion of books this time. Instead of reviewing newly published (or read) books that find their way to my reading table, I am reviewing three books that I recently reread in an effort to better understand and hopefully explain what seems to be going on in our economy. It may be said that the choice to reread a book indicates the book’s importance to the reader. The three books I recently reread are Thomas L. Friedman’s 2000 best seller The Lexus and the Olive Tree: Understanding Globalization (New York: Picador), James M. Buchanan and Richard E. Wagner’s, Democracy in Deficit: The Political Legacy of Lord Keynes (Indianapolis: Liberty Fund), and Albert O. Hirschman’s, Exit, Voice, and Loyalty: Responses to Declines in Firms, Organizations, and States (Cambridge: Harvard University Press).

Friedman’s exquisitely documented book addresses the rapid rise of a technology-driven global economy that has produced and spread wealth worldwide, along with delivery of severe transitional pressures that have obsoleted entire work specialties, laid waste to highly specialized but now no-longer-competitive industrial communities, and placed enormous pressure on culture-defining customs and traditions that define who and what people are. Yes, globalization brings widespread demand for the finest products capitalism can produce, symbolized by the Lexus automobile, along with a realization that making a transition from ox carts and bicycles to automobiles changes more than just the time it takes to get to work each day. In short, there are large social tradeoffs that occur when a nation decides to participate fully in the global economy and wear what Friedman calls the “golden straitjacket” that limits independent action regarding what and how to produce but can yield at the same time large increases in income and wealth.

Along with the golden straitjacket, Friedman emphasizes another change that eroded the ability of globalized national economies to determine their own destiny. Globalization and the end of the Cold War reduced the role played by superpowers and nation-states themselves in funding large projects across clients and lifted the importance of what he names the electronic herd, the world financial community, which became the major source of cash and capital for government projects and private investment.

Friedman develops and richly documents the emerging Lexus/olive tree tradeoff and then devotes considerable ink and space to discussions of reactions—both positive and negative—to globalization forces. It is in this discussion that I hoped to find meaningful commentary that might explain the recent rise of nationalism and populist-driven politics. Friedman does have something to offer, but still not much. In his discussion of globalization winners and losers, he talks about the “turtles,” workers displaced by higher technology–based manufacturing who are not equipped to jump to the next occupational rocket ship. Large numbers of primarily male workers are pushed to one side and left to fill low-level jobs in a world economy that needs fewer of them. These people lose their income and self-respect. But instead of seeing this group as forming “the forgotten man” who can be catered to by canny politicians, Friedman looks to displaced bureaucrats and no-longer-celebrated former local leaders to form an antiglobalization bandwagon. He clearly sees organized labor as a force that will oppose the opening of borders for people, goods, and services. Upon rereading the book, I concluded that Friedman’s turtles and Lexus/olive tree pressures contributed to the rise of nationalism but were not the primary movers. I am left thinking that reactions to the large waves of refugees who sought refuge in Europe and elsewhere were a major driver along with the financial collapse and Great Recession that followed. Now almost 20 years later, Friedman’s 2000 book still makes for delightful reading.

I reread Buchanan’s and Wagner’s 1977 book, Democracy in Deficit, in an effort to refresh my memory for their explanation of the deficit/debt habit that seems to affect all democracies. No matter the level of long-term prosperity or the current conditions of labor markets and incomes, democracies seemingly cannot prevent themselves from borrowing and spending. Even in times like today, there just never seems to be enough revenue to fund a democracy’s critical needs.

I found the reread to be refreshing but not encouraging. Drawing on public choice logic, of which the authors are themselves major contributors, they put forward a simple argument. A nation’s citizens love the benefits that can be provided by vote-hungry politicians, but they hate taxes. Canny and wise politicians learn quickly that to keep their jobs, they should send pork to the special interest groups that keep them employed and fund the pork with debt, not taxes. Even though pure theory might say that funding with debt to be paid for with future taxes can be shown to be equivalent to funding with taxes now, it still turns out that ordinary voters believe they can escape the future tax burden, in some cases by refunding old debt with new borrowing. So the beat goes on, even for so-called conservative administrations.

And so why did debt become so popular in the post–World War II period, but not so before? Buchanan and Wagner argue that the former Victorian attitudes about the virtues of paying one’s bills on time, balancing the books, and staying out of debt were eroded away by Great Depression functional finance promoted by Keynesian protagonists. In today’s world, politicians even argue that more debt is always the way to go, that there really is no limit to what the country may do with a debt-driven perpetual motion economy. Others who recall stories of European hyperinflation and are today focused on Venezuela’s catastrophic situation with printing press money cling to the notion that before the government spends more, it should know how to pay the bill with real money, not with debt.

Finally, I reread Exit, Voice, and Loyalty, Hirschman’s marvelous 1970 book, out of concern for President Trump’s harsh verbal condemnation of four newly elected congresswomen because of their sharp criticism of him and actions taken by his administration. The four women, who were exercising voice in criticizing the president, happen to be members of minority groups; one was born in Somalia. Upon condemning them, Trump suggested they should go back to the countries from which they came and indicated that they are not welcome here. Only one of the four was born in another country. Instead of voice, Trump preferred that they exit.

Hirschman’s book, subtitled Responses to Decline in Firms, Organizations, and States, seeks to explain how businesses, organizations, institutions, communities of people, families, and even nations gain access to what it is that pleases—or displeases—customers, members, and citizens, and apply that knowledge to survive, improve, and perhaps flourish. Shoppers at particular grocery stores, for example, who find the fresh produce no longer to their liking, can voice a complaint to the manager and hope for better days, or they can simply exit the store and shop somewhere else. In either case, their displeasure is communicated. In the grocery case, exit is easy and cheap. One finds few protests in front of grocery stores calling for improved produce. When exit costs are extremely high, as in changing citizenship, it is critically important for societies and nations to tolerate, if not encourage, criticism. Hirschman explains how every group, organization, and nation will, at times, have dysfunctional leadership. That being the case, it is critically important that options for exit and voice be made available. In politics, people rely on these forces and the “loyal opposition” to help check excessive and sometimes harmful behavior on the part of elected officials. Hirschman reminds readers that competition matters in all aspects of life.