- | Policy Briefs Policy Briefs

- |

Explaining the Debate Surrounding President Trump’s Payroll Tax Deferral

President Trump signed an executive order in August 2020 allowing American workers’ payroll tax contributions to be deferred until the end of the year. This action has been aggressively criticized by President Trump’s political opponents. The purpose of this policy brief is to explain the substantive issues and factors surrounding the debate over President Trump’s actions.

Background on the Social Security Payroll Tax: Its Purpose and Effects

Factor 1: The Purpose of the Payroll Tax Is to Fund Social Security

Workers’ earnings (up to an annual cap that is automatically adjusted each year) are subject to a 12.4 percent payroll tax that funds the Social Security program. Ostensibly, 6.2 percentage points of that amount are paid by the worker, and 6.2 are paid by the worker’s employer, but economists agree that all 12.4 points of the tax are taken out of the worker’s compensation and thereby reduce his or her take-home wages. Workers also pay a similar payroll tax (2.9 percent in most cases) to support Medicare Hospital Insurance.

The amount of the payroll tax is not arbitrary. The Social Security trust funds depend on payroll taxes for most of their income, along with interest that is earned on any revenue that remains unspent (the program also has a much smaller revenue stream from the income taxation of Social Security benefits). The purpose of the payroll tax is straightforward: to fund Social Security so that any benefits it pays are deemed to have been earned by workers via their contributions, in contrast to other federal benefit programs that are financed from the government’s general fund. The current payroll tax rate reflects what government officials thought would provide sufficient funding to Social Security when it was last adjusted several decades ago.

Factor 2: President Trump Lacks the Authority to Cut the Payroll Tax and Is Merely Allowing Its Collection to Be Deferred

The payroll tax rate is set in law, which the president lacks the authority to change. Instead, the president’s executive order simply defers the mandatory collection of certain payroll taxes, which American workers still owe. Unless the law changes, workers will have to make up in 2021 any payroll taxes they don’t pay this year. For this reason, many employers are continuing to forward these payroll taxes to the federal government, despite the president’s executive order.

At the same time, President Trump’s executive order directs the secretary of the Treasury to “explore avenues, including legislation, to eliminate the obligation to pay the taxes deferred.” President Trump has also expressed the hope that the tax forgiveness would be permanent, though White House officials subsequently clarified that this meant that workers would not have to repay the foregone taxes next year, rather than that the payroll tax would be totally eliminated going forward.

Factor 3: The Payroll Tax Imposes a Substantial Cost on Employment

The Social Security payroll tax subtracts 12.4 percent from the wage compensation an employer can provide to an employee for doing a job and, thus, is a substantial cost imposed on employment. It is for this reason that reducing the payroll tax is occasionally suggested whenever elected officials consider how to boost job creation during a recession. Economists disagree about how much the payroll tax affects employment, but the Congressional Budget Office and many other experts find that lowering the payroll tax would reduce labor costs and generally increase employment.

An important caveat should be applied to these conclusions. The payroll tax is not simply a randomly generated toll on worker wages. Instead, it funds Social Security benefits. As Joe Antos has pointed out, ending the payroll tax and funding Social Security with general revenues, while leaving its current benefit formula in place, would actually discourage work. With current payroll tax funding, Social Security is designed so that workers are entitled to more benefits as they earn more wages. Without it, the federal government would have to raise income taxes to fund Social Security, reducing individuals’ work incentives by eliminating the requirement that they have wage earnings in order to accrue Social Security benefits.

How Payroll Tax Collections Affect Social Security’s Financing Shortfall

Factor 4: Social Security Faces Projected Insolvency Because Its Scheduled Benefits Far Exceed the Amount Payroll Tax Collections Can Fund under Current Law

This is important context for the president’s move. Federal lawmakers have scheduled Social Security benefit payments far exceeding what the current payroll tax rate can fund. They did not intend to do this; the current benefit and tax schedules reflect decisions made in 1983, when it was projected that these schedules would keep Social Security solvent for the next 75 years. In the decades since then, an enormous financing deficit has opened, and lawmakers have not met their responsibility to fix it. This inaction lingers because repairs require politically treacherous decisions such as slowing the growth of benefits, raising eligibility ages, increasing the payroll tax, or some combination thereof—even though the longer action is delayed, the more severe these adjustments will need to be.

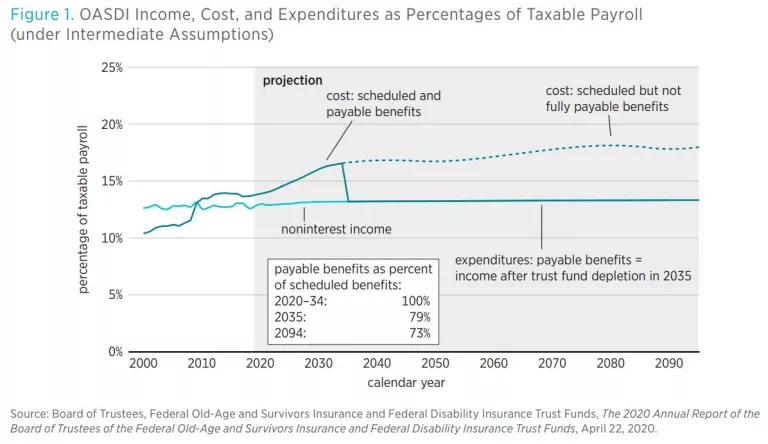

The Social Security portion of the payroll tax would need to rise immediately from 12.40 percent to 15.54 percent to finance current benefit schedules over the long term. There is little chance that the public will have an appetite for such a huge tax increase, so it is almost certain that current benefit growth rates will need to be slowed down. Regardless, even the current payroll tax rate is not nearly enough to fund Social Security’s current benefit schedule, as shown in figure 1 from the annual trustees’ report, illustrating the excess of scheduled benefits over projected tax income.

Factor 5: If the Payroll Tax Is Cut (Rather Than Simply Deferred), Then All Other Things Being Equal, the Social Security Financing Shortfall Will Get Even Worse

Social Security’s current financing shortfall makes this fact obvious. Lawmakers want to avoid worsening this shortfall, which would bring the date of Social Security’s insolvency closer, at which point benefits would be suddenly and sharply cut (by 24 percent under current law) because the system would lack sufficient funds to pay full benefits. Worsening the shortfall makes the changes required to preserve solvency—raising taxes or reducing scheduled benefits—even more severe than they already are.

Because lawmakers don’t want to accelerate insolvency and thereby trigger larger, sooner benefit cuts, proposals for payroll tax relief sometimes include provisions to replace any income that the Social Security trust funds lose with revenues redirected from the government’s general fund. This maneuver, however, violates the foundational principle underlying Social Security: that it is a benefit earned through workers’ payroll tax contributions. If Social Security instead becomes funded by income taxes, and many beneficiaries thus receive benefits without paying for them, then it becomes like any other welfare program, and its payments lose the politically privileged status they have always enjoyed. In sum, cutting the payroll tax creates a Hobson’s choice between abandoning the program’s historical earned-benefit construct and accelerating its insolvency.

The Policy and Political Contexts Surrounding Proposals for Payroll Tax Relief

Factor 6: Election-Year Politics Are Distorting the Discussion of the Issue

America actually went through a similar process during the Obama administration, eliciting different political reactions than those happening now. In 2011–2012, also to mitigate an economic downturn, President Obama proposed, and lawmakers enacted, a temporary payroll tax cut of 2.0 percentage points (from 12.4 percent to 10.4 percent). I criticized that action at the time on many of the same grounds discussed in this brief: namely, that Social Security was already underfunded, that the payroll tax’s job was to fund Social Security rather than to serve as an economic tuning mechanism, and that replacing payroll taxes with general revenues undermined the earned-benefit foundation that has kept Social Security benefits a reliable income source through the decades.

Now that President Trump has similarly proposed to fight an economic downturn with a payroll tax cut, a different set of political actors has emerged to critique the idea. Glenn Kessler of the Washington Post Fact Checker reviewed one recent episode of political opportunism involving the attribution of a hypothetical plan to President Trump to permanently eliminate the payroll tax and crash the Social Security system within three years.

My concerns about the real Trump policy largely parallel those I expressed about the previous Obama policy, with a few tweaks. In some respects, President Trump’s idea is not as damaging to Social Security as President Obama’s: Trump’s is of shorter duration and does not involve general revenue financing (at least not yet). In one important respect, however, the Trump policy is worse for Social Security: it holds back the entirety of individuals’ payroll tax obligations rather than just 2 percentage points. The Trump policy also seems of trivial benefit to the job market because, as the Treasury Department has recently clarified, “all deferred taxes must be fully repaid by April 30, 2021.”

Payroll Tax Relief Is Bad for Social Security

Factor 7: The Trump Policy Is Aimed at Making It Easier for Businesses Struggling through 2020 to Hire and Retain Workers

There is good reason to be concerned about President Trump’s order, specifically its effect on Social Security. One popular criticism, however, is off base: that cutting the payroll tax is “poor stimulus” amid the recession because it does “nothing” for “unemployed workers who need the most help.” It’s true that cutting the payroll tax doesn’t help the unemployed, who indeed need federal government support. However, this is not a typical recession; it cannot be cured by the common recession-fighting approach of simply giving people more money to spend.

The current economic downturn is a direct result of government policies aimed at fighting the spread of COVID-19. Bizarrely, US personal savings hit an all-time high this year as government sent relief checks to individuals but constrained them from many of their usual ways of spending the money. The key to getting through this downturn is not writing more checks to individuals that they aren’t allowed to spend, but rather enabling businesses to stay afloat and to retain their workers until spending patterns can return more closely to normal. President Trump’s policy is bad for Social Security, but he’s right that the federal government needs to support job retention during the pandemic.

Factor 8: The Payroll Tax Cut Proposal Is Exposing Gradual, Bipartisan Abandonment of Social Security’s Historical Financing Structure

Andrew Biggs recently published a provocative column in which he argues that President Trump’s move on the payroll tax might counterintuitively point the way to a new bipartisan consensus on how to reform Social Security. Specifically, it could nudge toward a future in which lawmakers simply give up on the idea of collecting enough payroll taxes to fund Social Security and start financing it from the general fund (basically, with income taxes).

As a former Social Security trustee, I harbor many concerns about such a change. The stability and reliability of Social Security benefits derive in large part from the perception that they have been earned by workers’ payroll tax contributions. If the link between what workers contribute and what they receive becomes severed, Social Security benefits and eligibility rules would likely become subject to incessant renegotiation, as benefits typically are in every welfare program where there is an overt collision of interests between taxpayers and beneficiaries. Moreover, policymakers should be careful about discarding a funding system that has, at least in the past, occasionally forced financing corrections (most notably the 1983 Social Security amendments), a mechanism that is completely absent from the general federal budget. Finally, the public has exhibited no desire to do away with Social Security’s historical design.

That said, Biggs is certainly correct in his analysis of the political dynamics gathering around Social Security. Many influential thinkers on the Right regard Social Security’s trust funds and its earned-benefit construct as fictions that inhibit necessary reforms to contain system cost growth. On the Left as well, proposals to abandon the constraints of self-financing have proliferated in recent years: these include proposed legislation to fund an across-the-board benefit increase with general revenues, proposals to use general revenues to eliminate Social Security’s shortfall, and the aforementioned payroll tax cut and general revenue infusion enacted during the Obama administration. Continuing the Social Security system under its current financing structure requires balancing the program’s books, and more officials on both the Left and Right express a disinclination to even try.

Conclusion

President Trump’s executive order to defer the collection of the payroll tax is bad for Social Security, as was President Obama’s payroll tax cut before it. However, the Trump payroll tax policy did not cause, but simply reflects, the disintegration of a longstanding political norm holding that Social Security should be fully self-financing.

I agree with those who express concerns about the payroll tax deferral’s effects on Social Security. The concerns ring somewhat hollow, however, in the context of lawmakers’ ongoing, increasing unwillingness to correct the growing imbalance between Social Security’s benefit and tax schedules. Failing to collect payroll taxes certainly undermines Social Security’s future solvency, but so too does lawmakers’ continuing refusal to balance Social Security’s accounts.