- | Monetary Policy Monetary Policy

- | Policy Briefs Policy Briefs

- |

Gas Prices, Inflation Expectations, and Consumer Sentiment

Gas prices have risen rapidly in recent months. At the end of May 2022, regular gasoline averaged $4.44 per gallon nationwide, compared with $2.99 a year earlier. Much of the increase came after the Russian invasion of Ukraine in late February 2022. High gas prices are especially hard on low- and middle-income households, and policymakers are scrambling to address them. For example, President Joe Biden recently called on Congress to impose a gas tax holiday, and Federal Reserve (Fed) Chair Jerome Powell referred to high gas prices several times during his June 2022 press conference.

In particular, Powell noted that high gas prices are “not something we can do something about,” then immediately added that, “by the way, headline inflation, headline inflation is important for expectations. People, the public’s expectations, why would they be distinguishing between core inflation and headline inflation. Core inflation is something we think about because it is a better predictor of future inflation. But headline inflation is what people experience, they don’t know what core is.”

Here, Powell was distinguishing between headline inflation, which includes volatile prices such as food and energy, and core inflation, which excludes these more volatile prices. The Fed’s 2 percent inflation target is defined in terms of the headline personal consumption expenditures (PCE) price index, but the Fed typically relies on the core PCE price index as a clearer signal of underlying inflation trends. Powell’s remarks about gas prices and headline inflation indicate that the Fed recognizes the potentially outsized effect of gas prices on consumer expectations—that is, with gas prices rising, simply stabilizing core inflation might not be enough to restore public confidence in the Fed’s commitment to price stability.

In this policy brief, I discuss the effects of gas prices on consumer expectations and sentiment on the basis of two of my research papers: “Inflation Expectations and the Price at the Pump” (published in 2018 in the Journal of Macroeconomics) studies the impact of gas prices on consumers’ expectations of inflation, and “Stuck in the Seventies?: Gas Prices and Consumer Sentiment” (coauthored with Christos Makridis and published in 2020 in the Review of Economics and Statistics) focuses on how gas prices affect sentiment about overall economic conditions.

Inflation Expectations and the Price at the Pump

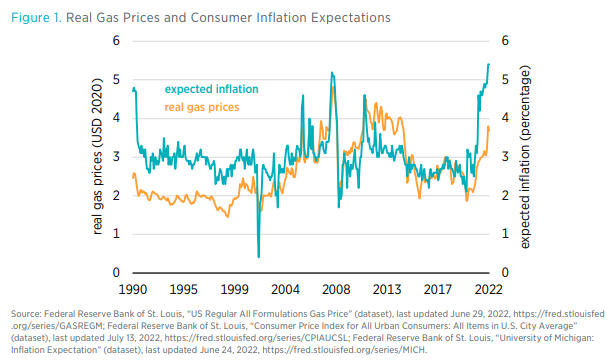

Gas prices and household inflation expectations are closely correlated. Figure 1 shows time series of real gas prices along with inflation expectations from the University of Michigan Survey of Consumers. Clearly, large spikes and declines in gas prices are associated with similar movements in inflation expectations. For example, as gas prices rose from $2.64 per gallon in February 2010 to a peak of $3.91 per gallon in May 2011, inflation expectations simultaneously increased from 2.7 percent to 3.8 percent. Both series declined together for the latter part of 2011. More recently, gas prices and inflation expectations have both spiked even more notably.

This same pattern holds over a longer period. Though the gas price data are not available until 1990, gas prices are highly correlated with oil prices, which are available since the beginning of the University of Michigan survey data, in 1978. From 1978 to the present, the correlation between consumer inflation expectations and real oil prices is 0.44. That is, consumer inflation expectations rise when gas prices rise and fall when gas prices fall.

This time series evidence has led researchers to suggest that gas prices have an outsized effect on consumer inflation expectations. This might be the case if the high frequency of gas purchases makes gas prices especially salient or if people have a psychological tendency to notice and remember extreme price changes more than mild price changes In my 2018 paper, I made use of additional questions from the University of Michigan Survey to address whether consumer inflation expectations are excessively sensitive to gas prices. In other words, given that gas prices account for roughly 5 percent of consumer expenditures, do consumers weight the gas prices they observe more heavily than that expenditure share when forming their perceptions of current inflation and their expectations about future inflation?

To answer this question, I used individual consumers’ survey responses about their expectations of inflation over the next 12 months and over the next 5 to 10 years, as well as consumers’ expectations of gas price changes over the same time horizons. Doing so allowed me to estimate the parameters of a simple model of expectation formation. In the model, a consumer’s perception of headline inflation is a weighted average of his or her perceptions of gas and nongas inflation, where the weight ω on gas price inflation need not necessarily correspond to the expenditure share on gasoline. The consumer uses these perceptions and his or her beliefs about the persistence of inflation to form expectations of future gas and nongas inflation.

I find that the weight ω for gas price inflation is very similar to the expenditure share for gas, meaning that consumers do not weight gas prices excessively in their inflation expectations. I also find that consumers do not expect shocks to gas price inflation to persist—if gas prices are rising quickly, they expect gas prices to rise more slowly in the future. My estimates combined imply that if gas price inflation increases by 1.000 percentage point, then 12-month inflation expectations increase by about 0.010 percentage points, and 5- to 10-year inflation expectations increase by less than 0.003 percentage points.

Because gas price fluctuations can be large, even these small estimates still imply that gas price fluctuations can be a major driver of inflation expectations. However, I show that the magnitude of the response is consistent with consumers using a fairly reasonable model of inflation dynamics in which the weight for gas price inflation in headline inflation is similar to the expenditure share on gas.

Gas Prices and Consumer Sentiment

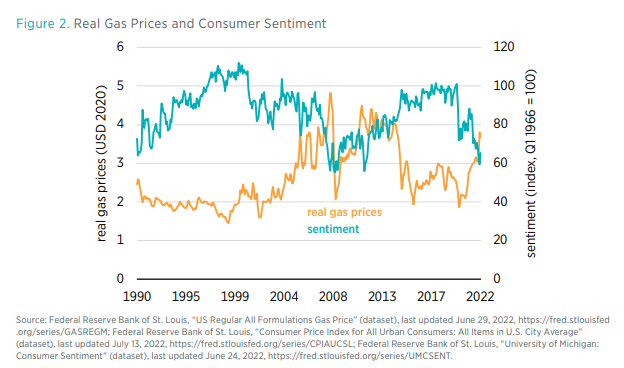

Figure 2 is similar to figure 1, but it shows the correlation of real gas prices with consumer sentiment rather than consumer inflation expectations. Consumer sentiment is a measure of consumers’ beliefs about how well the overall economy is doing now and how it will do in the future. In this case, the two series are negatively correlated, with a correlation coefficient of −0.54. Since 1978, the correlation between real oil prices and consumer sentiment has been −0.58.

The correlation between sentiment and gas prices is not perfect, and there are clear examples of drops in sentiment without a rise in gas prices. In the first few months of the COVID-19 pandemic, for example, consumer sentiment plunged at the same time that gas prices were falling. But the recovery in sentiment that began in late 2020 has since been wiped away as gas prices have climbed, and sentiment is now well below its 2020 low point.

In my 2020 paper, my coauthor Christos Makridis and I used higher-frequency data to study the causal impact of gas price fluctuations on consumer sentiment. The Gallup U.S. Poll surveys a sample of around 1,000 respondents daily about their economic sentiment. We used daily, state-level gas price data to match each survey response with the gas price in the state the response was collected and on the day that the response was collected. Doing so allowed us to test how a change in local gas prices affects consumer sentiment, even controlling for respondent characteristics and nationwide trends. We found that consumers interpret rising local gas prices as a negative signal about national macroeconomic conditions.

Because the Gallup poll also collects information about respondents’ demographics, we were able to study whether respondents with different characteristics respond differently to gas prices. Most notably, we found that consumers who were born before 1962, and hence were old enough to remember the oil price shocks of the 1970s and early 1980s, have a stronger decline in sentiment in response to higher gas prices. This result is consistent with “learning from experience” effects that have been documented in other contexts in previous research.

The decline in consumer sentiment that accompanies rising gas prices can amplify the effects of high gas prices on consumption. High gas prices reduce the amount of discretionary income that households can spend after purchasing the gas they need. On top of that, high gas prices also make consumers fear that a recession could be coming, leading them to reduce consumption as a precaution and putting a damper on economic activity.

Implications for Monetary Policy

It is clear to see why high gas prices are commanding so much attention from policymakers and the media. Rising gas prices likely go a long way in explaining the recent rise in consumer inflation expectations and decline in consumer sentiment. For the Fed, rising inflation expectations pose a risk that expectations could become unanchored from the 2 percent inflation target. For politicians, poor consumer sentiment hurts approval ratings.

At a Senate Banking Committee hearing in June, Senator Elizabeth Warren asked Chair Powell whether gas prices would go down as a result of the Fed’s recent interest rate hike. Chair Powell answered, “I wouldn’t say so, no.” In response, Senator Warren remarked that “rate hikes won’t make Vladimir Putin turn his tanks around and leave Ukraine. Rate hikes won’t break up monopolies. Rate hikes won’t straighten out the supply chain . . . .”

This is largely correct. The Fed has neither the mandate nor the tools to target specific prices, such as the price of gas. The Fed’s mandate is for aggregate price stability, not relative price stability. As Chair Powell explained to Senator Warren, “the idea is to moderate demand so it can be in better balance with supply.”

The entire exchange between the chair and the senator reveals one of the major troubles that can arise with inflation targeting: Inflation can exceed the central bank’s target because of demand shocks or supply shocks. Monetary policy, which works through aggregate demand, can best stabilize the economy if it responds only to demand shocks, and looks through supply shocks. But it is hard to tell, in real time, what kind of shock is causing inflation. Even high oil prices can reflect low supply or high demand. It is also hard to communicate to the public and to politicians why rising gas prices sometimes prompt a rate hike and sometimes do not, while for consumers, rising gas prices always prompt a decline in sentiment.

With a nominal gross domestic product (NGDP) level target, by contrast, which would stabilize the path of nominal spending, the Fed would automatically respond to demand-driven inflation and look through supply-driven inflation. The Fed would have a much easier time explaining its decisions to the public, without the need for confusing discussions of oil and gas prices. The Fed hiked interest rates in June because NGDP was well above its trend path. Even if gas prices decline substantially in the next few weeks, the Fed should continue to raise interest rates if NGDP appears to be growing above its trend path, it and should stop raising rates when NGDP is normalized.