- | Regulation Regulation

- | Policy Briefs Policy Briefs

- |

Helping Small Businesses Comply with Federal Regulations

All people who have ever dreamed of being their own bosses, opening their own businesses, or creating new kinds of businesses but who haven’t yet acted on those dreams are potential small business owners. But because these businesses do not yet exist, their owners don’t belong to any recognizable group. There is no guardian ad litem who protects their opportunities to be their own bosses.

Although the Regulatory Flexibility Act and the Small Business Regulatory Enforcement and Fairness Act (SBREFA) protect small businesses that “bear a disproportionate share of regulatory costs and burdens,” there is no law, and, in fact, no constituency, to protect potential entrants. After all, they don’t even know they are potential entrants until they try, like Senator McGovern, to open their own businesses.

The Regulatory Flexibility Act, the SBREFA, and the earnest efforts of the Small Business Administration (SBA) have no doubt been helpful for small businesses. Nonetheless, federal regulations still pose significant problems for existing small businesses and potential entrants. A recent survey posed the following question to small business owners: “If you were to start your exact business today, approximately how much money do you think you would spend on regulatory compliance efforts in the first year?” The average response was approximately $83,000. While regulatory compliance costs may be viewed as a necessary cost of doing business in the United States, the complexity of the rules and the difficulty of interpreting and understanding them appear to be the larger obstacles for existing or potential small businesses. Whereas 23 percent of survey respondents indicated that the biggest cause of regulatory difficulty is “the cost of compliance,” 44 percent responded that either “the complexity of rules” or “the difficulty of interpreting and understanding rules” was the primary difficulty.

Such difficulties have consequences. The same survey found that 39 percent of respondents had delayed or halted business investments other than new hires because of “uncertainty related to a pending regulation,” while 42 percent had delayed or halted business investments because of “uncertainty on the meaning or interpretation of existing regulations.” Recent research has highlighted the importance of the relationship between regulation and business investments. A 2016 study found that the accumulation of regulations—by distorting or deterring business investments—slowed annual economic growth by an average of 0.8 percentage points from 1980 to 2012. As a result of that forgone growth, the economy is 25 percent smaller than it would have been otherwise. That means every person in the country is about $13,000 poorer than they might have been.

Such tangible costs, coupled with the survey evidence of actual deterrence of business investments by small businesses, indicate a continued need for regulatory reform addressing small businesses. Three modest measures would help:

- Require agencies to exempt small businesses from regulation if they are not a significant cause of the problem that motivated the regulation.

- Spread out the compliance times for multiple rules.

- Require agencies to publish preliminary analyses before proposing major regulations.

The Problem

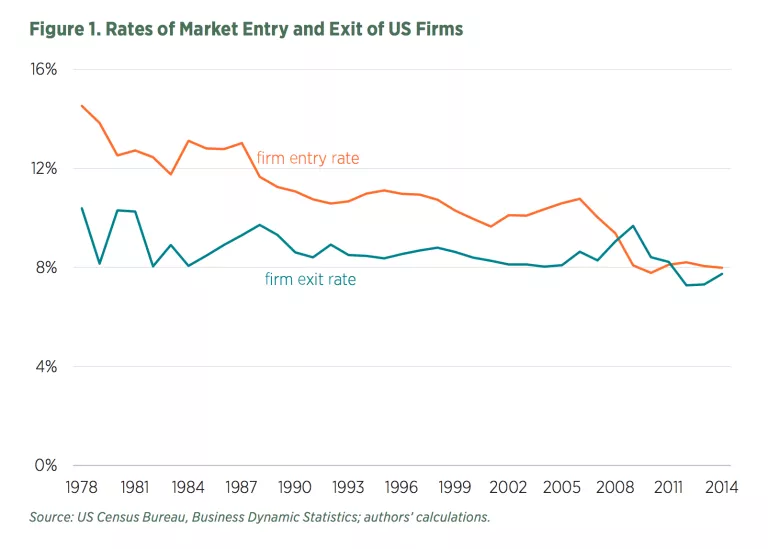

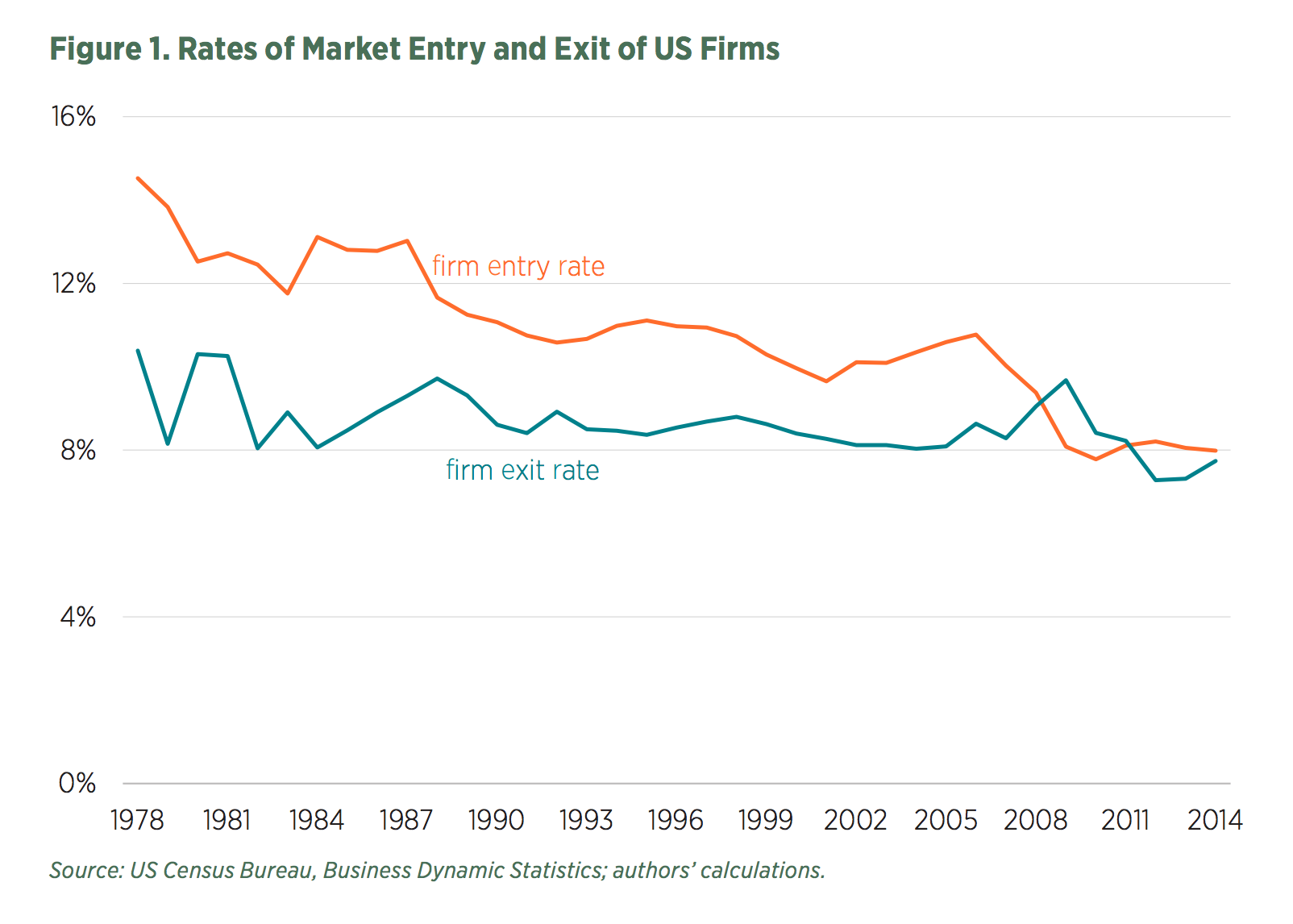

The United States now ranks 12th among developed nations in terms of business startup activity. For the first time ever, more businesses closed in America in the past several years than new ones opened (although that trend has recently reversed).

The SBA’s Office of Advocacy (Advocacy) marked its 40th anniversary in 2016. Advocacy is the independent voice within the federal government for small businesses. Advocacy estimates that its work on behalf of small businesses has resulted in cumulative cost savings of $128.7 billion between 1998 and 2015, with $1.6 billion saved in 2015 alone. Despite some notable success, a recent poll reported that 61 percent of small businesses owners said that “they feel the burden of federal rules weighing on their business.” This concern about overregulation was the second most common among respondents, behind overtaxation.

The government requires analyses and includes organizations to oversee those analyses for environmental impacts (EPA), economic efficiency (Office of Information and Regulatory Affairs in the Office of Management and Budget), and effects on (incumbent) small businesses and small governments (Advocacy). For potential entrants, Executive Order 12866 mentions “adverse effects” on competition as a reason for analysis, and some agencies must specifically consider effects on competition (e.g., the Department of Energy in its energy efficiency regulations). In some cases, as mentioned in EO 12866, the Department of Justice and the Federal Trade Commission are charged with identifying anticompetitive conduct. In addition, Executive Order 13725 requires that agencies “eliminate regulations that restrict competition without corresponding benefits.” However, there does not appear to be a single agency charged with analyzing and representing the interests of potential entrants.

Taking a few steps could help both potential and current small business owners deal with the complexities and costs of regulations.

Solutions

1. Exempt small businesses if they are not a significant source of the problem that motivated the regulation

Incumbent small businesses are responsible for following the 2,500–4,500 federal regulations produced each year. They must take time to read proposed regulations, determine whether their businesses are affected, and, if so, understand the regulations’ likely effects and comment on them to have any say in the future of the proposed regulation. Many business owners do not have expertise on the federal regulatory process and, even if they have the time to make informed comments on the regulation, may not be sure whether their comments will make any difference. Furthermore, business owners sometimes fear that commenting negatively on a regulation will prompt regulators to single them out.

Because the SBA will never be able to comment on all the rules that affect small businesses, one way to ensure that agencies take small businesses’ concerns into account is to require agencies to determine at the outset whether small businesses are a significant source of the problem the regulation seeks to solve. If small businesses do not contribute significantly to the problem, there is no need to regulate them. If they are a noticeable but still modest source of the problem, the agency should explicitly compare the social benefits of regulating small businesses with the associated costs.

Regulatory agencies occasionally grant these kinds of exemptions. For example, in its rule regulating the safe production of shell eggs, the FDA exempted farms with fewer than 3,000 laying hens from some of the requirements because enforcing the rule on small farms would cost more than $175 million while the benefits would total only $10 million. The FDA noted there was no evidence of “elevated risk of sporadic illness or outbreaks” associated with small farms. It is doubtful that any small chicken farmer would have had the resources to comment on this rule. Further, there was no one to represent those who might want to start small-scale chicken farms in the future.

For new entrants, the task is even more daunting. The Code of Federal Regulations has increased from 22,877 pages in 1960 to more than 175,000 pages now. One way to help potential small businesses is to develop an additional publication dividing the CFR by industry, including only the rules that affect small businesses.

2. Disperse compliance dates

A second issue for small businesses is the timing of effective dates for multiple new regulations. For example, consider the production of beer—an industry where craft brewers and other small businesses are intrinsic to the explosion in variety and quality over the past decade. Between 2009 and 2010, the new rulemakings from the federal government created an additional 3,850 regulatory restrictions that are relevant to breweries (Census Bureau NAICS code 31212).

Likewise, the federal government imposed 4,600 regulatory restrictions on the waste treatment disposal industry (Census Bureau NAICS code 5622) in 2014. However, the date a rule is finalized is not the same date as the date the rule goes into effect. There were 17 different new rules for the waste disposal treatment industry that had enforcement dates in 2014. These regulations’ effective dates were not uniformly distributed over time. In fact, four of these rules had effective dates occurring in a single month, and three other rules went into effect in a different month.

A small business generally cannot get a loan to cover costs of complying with a given regulation—regulatory compliance is typically not viewed as a business investment that is likely to generate profitable returns. This means that small business owners must pay for compliance out of retained earnings. If regulatory costs are not too high and, in particular, too concentrated in one month or quarter, more small businesses can afford to comply. As the above example shows, 7 of the 17 new regulations affecting one industry in 2014 went into effect in just 2 months. Such a concentration of effective dates in a short period of time can overwhelm small businesses’ ability to fund measures for compliance from their retained earnings and adopt them.

The roughly 3,500 new rules finalized in 2014 came from approximately 96 independent and 220 executive branch agencies, producing an average of nearly 300 regulations each month. Each agency independently determines the dates by which firms must comply. Unfortunately, there is no central coordinating body in the federal government that ensures these regulations are spread out evenly throughout the year for each industry.

When, for example, there are surges in new rules, such as observed during the “midnight regulations” period at the end of a presidency, new rules’ effective dates may disproportionately bunch up, straining small businesses’ ability to comply using only retained earnings.

This seems like a natural job for the small agency whose job it is to coordinate the actions of federal agencies, the Office of Information and Regulatory Affairs (OIRA) in OMB. Currently, OIRA is assigned the “responsibility of coordinating interagency Executive Branch review of significant regulations.” With a small addition to its staff, it could also coordinate compliance dates with executive branch and independent agencies. OIRA could keep a regulatory calendar for each industry and, when agencies want to regulate a particular industry, work with the agency to ensure that rules’ compliance dates are as evenly distributed as possible. The same principle applies to commenting on proposed rules, because it is difficult to follow and comment on multiple proposed rules in a short span of time.

3. Require analysis before decisions

A 70- to 80-page notice of proposed rulemaking (NPRM) in the Federal Register is only part of what a stakeholder must read to be able to understand what the agency is doing. A complex regulation can require thousands of pages of supporting documents and several years to develop, including gathering information, proposing a rule, collecting comments on the rule, and finalizing it. The individual rule will often cite other rules in the Code of Federal Regulations that are affected by the proposed rule, analysis such as risk assessments that are referenced, and other scientific and legal documents that are offered in support of the rule.

After the agency spends years gathering the supporting documents, performing analyses, and reporting them in proposals that can run thousands of pages long, how much time do commenters typically have to respond? The answer from the federal government: “In general, agencies will specify a comment period ranging from 30 to 60 days.” In some cases, agencies may extend the comment period to 180 days or more.

That amount of time may be inadequate for many stakeholders—especially small business owners—to thoughtfully consider the regulation and prepare a substantive response. If a stakeholder wishes to challenge an analysis, such as a risk assessment, paperwork reduction analysis, regulatory flexibility analysis (RFA), or regulatory impact analysis (RIA), assembling the required evidence may take as long as the agency took to prepare the original analysis, often a year or more. Agencies also sometimes include surveys in their proposed rules and, if one wished to validate the results of a survey, a new survey would have to be conducted.

To make matters worse, agencies frequently make decisions about regulations before conducting the analysis that is supposed to inform the decision. That is, “by the time the NPRM is issued, the agency has made a very substantial commitment to the draft rule it is proposing, and will be understandably reluctant to modify it very substantially afterwards.”

To curb such “ready, fire, aim” rulemaking, agencies could make much more extensive use of an advance notice of proposed rulemaking (ANPRM) that includes a preliminary analysis of the problem the regulation seeks to solve, alternative solutions, and the benefits and costs of the alternatives. ANPRMs with preliminary RIAs and RFAs would also give stakeholders more time to understand the basis for the regulation, prepare thoughtful responses, and provide the agency with data or studies that may be helpful—before the agency has publicly committed to a favored approach.

This preliminary analysis should also include a preliminary assessment of effects on small businesses. First, the agency should determine whether small businesses are even a substantial source of the problem. If they are, the agency should assess whether the expected benefits from regulating small businesses outweigh the expected costs. Finally, if small businesses are to be regulated, the agency should identify alternatives that grant regulatory flexibility in those options and provide its preliminary estimates of the benefits and costs of those options. This would at least give small businesses a better chance of becoming meaningfully involved in the regulatory process.

Conclusion

Just as Senator McGovern was unable to understand how deeply small businesses were restricted by regulation before he actually owned one, regulators may also be similarly blinded. While the Regulatory Flexibility Act and the Small Business Enforcement and Fairness Act have helped, small businesses still usually play David to the federal Goliath. The three suggestions here would give small businesses and potential small businesses a fairer shot in the federal regulatory process.

{kind=link}