- | Government Spending Government Spending

- | Policy Briefs Policy Briefs

- |

If Congress Only Does One Thing, It Must Reform the Corporate Income Tax System

It would be hard to overstate how badly the US tax system needs an overhaul. It’s complicated, burdensome, unfair, and expensive. Worse, it hinders economic growth. Unfortunately, as we learned in 1986, comprehensive tax reform is extremely difficult to deliver, even in the best of circumstances. The current political environment allows little or no flexibility for bipartisan solutions, making the challenge even greater today.

For this reason, it is vital to not lose sight of the tax reforms that will have the biggest return for the American people if Congress can’t get enough support for a comprehensive do-over. Congress’s and the administration’s number one priority should be to reform the corporate income tax system. The combined burden of the highest corporate income tax rate of all industrialized countries and a punishing worldwide tax system falls mostly on American workers in the form of lower wages.

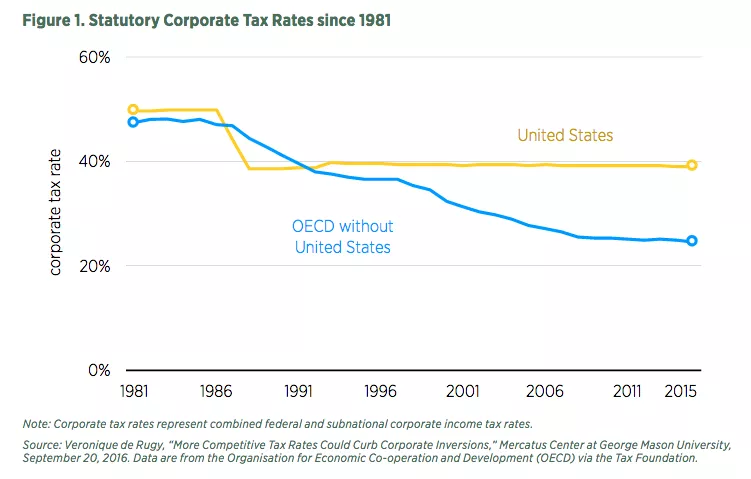

The Highest Tax Rate

At the time of the 1986 tax reform, the top corporate tax rate was 46 percent, but it was cut to 34 percent in 1988. Despite an increase to 35 percent in 1993, the United States was reasonably competitive with other major economies during this period. This happy condition didn’t last. Figure 1 shows how, as other industrialized countries cut their tax rates in the 1990s, US lawmakers chose not to—and as a result the combined (federal plus state) rate stayed at the extremely high level of 38.7 percent.

Today, the combined US rate is 39.1 percent, the highest among all developed nations. This means that US companies operating abroad are competing against foreign companies that face a much lower cost of doing business than the US companies do. US companies operating abroad can, of course, avoid US tax rates by keeping their overseas income outside the United States, as we will see below. Domestic companies, however, aren’t so lucky: they face the high corporate income tax rate without much hope of a reprieve. This high rate puts US companies at a competitive disadvantage in the global marketplace.

A Punishing Worldwide System

The United States taxes corporations under a worldwide tax system. This means that companies are subject to taxation on all income regardless of where it is earned. For example, the profits of US-owned plants based overseas are subject to US taxes—even though these profits might already have been taxed in the countries where they were earned. Companies with foreign earnings do receive a credit for foreign income taxes paid. That said, these foreign tax credits are not enough to offset the companies’ additional tax bill in the United States, and this puts them at a competitive disadvantage.

Most other industrialized countries do not tax “foreign-source” business income as aggressively as the United States does. In fact, more than three-quarters of the members of the 26-member Organisation for Economic Co-operation and Development have “territorial” tax systems that exempt foreign earned income. The combination of high tax rates and a worldwide tax system makes the US corporate income tax system extremely punishing and anticompetitive.

Taxation of most profits of US multinational companies’ foreign subsidiaries is imposed only when the profits are repatriated through a dividend payment to the US parent company. In other words, as long as a company keeps its foreign earnings abroad, it doesn’t have to pay the additional US tax. This ability to delay tax payments—known as deferral—is an important feature that alleviates the double taxation of income built into a worldwide tax system. Deferral explains much of the $2.5 trillion in foreign earned income stored abroad by American companies.

Thanks to the deferral provision, the difference in the fiscal burden between worldwide and territorial tax systems is reduced. However, companies in territorial tax regimes enjoy the freedom to bring their money back home or reinvest it in domestic capital and labor if it is in their interest. American companies, on the other hand, are forced to keep their foreign earned income abroad if they want to benefit from a lower corporate tax burden.

This feature of the US corporate tax system—on top of a high tax rate—has important implications for US competitiveness in foreign markets. Because of higher tax costs, US-based firms may lose foreign market share, generate lower returns for American shareholders, sell fewer products to foreign subsidiaries, and hire fewer skilled workers domestically. The US worldwide tax system also helps to explain why in the last two decades a growing number of companies have decided to engage in corporate inversion, the practice of acquiring a foreign company and then relocating one’s legal headquarters outside the United States for tax purposes.

Punishing to Domestic Workers

While it seems counterintuitive, those who stand to benefit the most from cuts in the corporate income tax rate are not the rich but American workers. That’s because corporations do not really pay taxes. What they do is collect taxes from individuals (i.e., workers, consumers, and shareholders).

Economists have come a long way in their understanding of who really shoulders the burden of the corporate income tax. The last time the United States was in a position to engage in tax reform, most economists believed that the burden of the tax was falling exclusively on the owners of capital in the form of lower returns. However, globalization, the increased openness of the US economy, the mobility of capital, and capital’s sensitivity to tax factors challenged the accuracy of this finding. In a 2006 study, economist William C. Randolph of the Congressional Budget Office estimated who were the winners and losers under the corporate tax. He concluded that “domestic labor bears slightly more than 70 percent of the burden.”

Many other studies have followed since, and on the basis of empirical estimates we know that today American workers shoulder anywhere between 75 percent and 100 percent of the cost of the corporate income tax in the form of lower wages.

In a recent review of the literature, the Heritage Foundation’s Adam Michel concludes that “a 20-point reduction of the corporate income tax to 15 percent could boost the relative market incomes of the poorest Americans by more than twice the increase for the richest. A tax cut for corporations is therefore a tax cut for the average American.”

Conclusion

Ideally, the entire tax system should be reformed. The entire system is dysfunctional and compliance with the federal tax code is horribly expensive and time consuming. The system has an oversized and sometimes counterproductive influence on the choices that people and companies make. It encourages tax avoidance and evasion, and it is costly to taxpayers not only in terms of taxes paid but also in terms of the money and time spent complying with the tax code. It should be fundamentally revamped.

Unfortunately, politics can get in the way of good economics and good policy. If Congress fails to engage in fundamental reform, lawmakers must at least reform the corporate income tax system.

Related Content

- | Government Spending Government Spending

- | Mercatus Podcasts Mercatus Podcasts

Three Tax Reform Priorities that Should Top Congress’s List

- | Government Spending Government Spending

- | Policy Spotlights Policy Spotlights

Enacting True Tax Reform, Not Just Tax Cuts

- | Government Spending Government Spending

- | Data Visualizations Data Visualizations

Reforming US Corporate Taxes