- | Labor Markets Labor Markets

- | Policy Briefs Policy Briefs

- |

A Proactive Response to AI-Driven Job Displacement

How reforming the tax code can build a resilient workforce

Artificial intelligence is transforming the US economy at breakneck speed, and fears of mass job displacement are fueling calls for heavy-handed government intervention. A straightforward but overlooked low-hanging-fruit solution lies hidden in the tax code: correcting the fundamental bias that makes it easier for businesses to invest in machines than in the workers who must learn to use them.

The current tax framework creates a profound asymmetry between physical and human capital investment. Through bonus depreciation under section 168(k)—a tax provision that allows immediate write-offs of equipment costs—businesses can expense a robot or an AI server in the year it is purchased, yet they must navigate a maze of restrictions to deduct the cost of retraining the people expected to use that technology. This asymmetric treatment skews business investment decisions away from economic merit and toward tax advantages, leading to systematic underinvestment in human capital development, which is the very training that enables workers to collaborate effectively with new technologies and capture the productivity gains that AI makes possible.[1] The imbalance discourages firms—particularly small, owner-operated ones—from investing in upskilling.

Six major restrictions in the Internal Revenue Code (IRC) create bottlenecks that effectively penalize businesses for investing in human capital. These restrictions were designed for a different era and have long undermined the flexibility firms need to adapt to today’s AI-driven economy, where rigidity carries an even greater cost. The restrictions are particularly punitive for small businesses, whose owners often cannot access educational assistance programs because of ownership caps, and for lower-wage workers, who face barriers to skill development.

The legal foundation for the treatment of physical and human capital investment dates to the Supreme Court’s 1933 decision in Welch v. Helvering, where Justice Benjamin Cardozo held that “learning [is] akin to capital assets... The money spent in acquiring them is well and wisely spent. It is not an ordinary expense of the operation of a business.”[2] Under this framework, human and physical capital were treated alike: Neither was deductible. Congress has since reversed course on physical capital, enacting sections 168(k) and 179 to permit immediate expensing. Human capital, however, remains governed by the 1933 framework—creating an asymmetry that Cardozo’s own reasoning suggests should not exist.[3]

This paper argues that Congress can remove the obsolete IRC restrictions and unleash market-driven solutions to AI displacement without resorting to dirigiste labor-market programs. The following sections (1) identify the six key restrictions in the Internal Revenue Code that discourage investment in human capital, (2) propose targeted reforms to restore neutrality between human and physical capital, (3) discuss the significance of human-capital parity, and (4) review the distributional and fiscal considerations of sound tax reform, before concluding with a discussion of the broader economic implications of these reforms.

1. The Tax Bottleneck in an AI Economy

Artificial intelligence is exposing how outdated provisions in the US tax code constrain workforce adaptation. The tax rules that govern education and training expenses were written for a mid-20th-century economy in which skills changed slowly and automation was limited. In today’s fast-evolving environment, these same rules now penalize the investments most essential to resilience—employee retraining and upskilling. Section 1 examines how six key restrictions in the Internal Revenue Code, particularly in sections 162, 127, and 168, create structural barriers to human-capital investment, distorting business decisions and locking firms out of the training their workers need. Each subsection below shows how these outdated rules operate in an AI-driven economy and why reform is essential to restoring neutrality between physical and human capital.

1.1 No deduction for training to meet minimum job requirements

IRC section 162 and associated guidance in IRS Publication 970, Chapter 11, disallow deductions for employee education when the coursework “is needed to meet the minimum educational requirements of your present trade or business.”[4] Originally intended as a safeguard against tax abuse, this provision now undermines the competitive flexibility essential in an economy reshaped by AI. Rather than protecting the market, this provision distorts it, trapping workers in outdated roles and stifling the entrepreneurial dynamism that drives genuine economic resilience.

1.2 Job‑relatedness freezes workers in yesterday’s roles

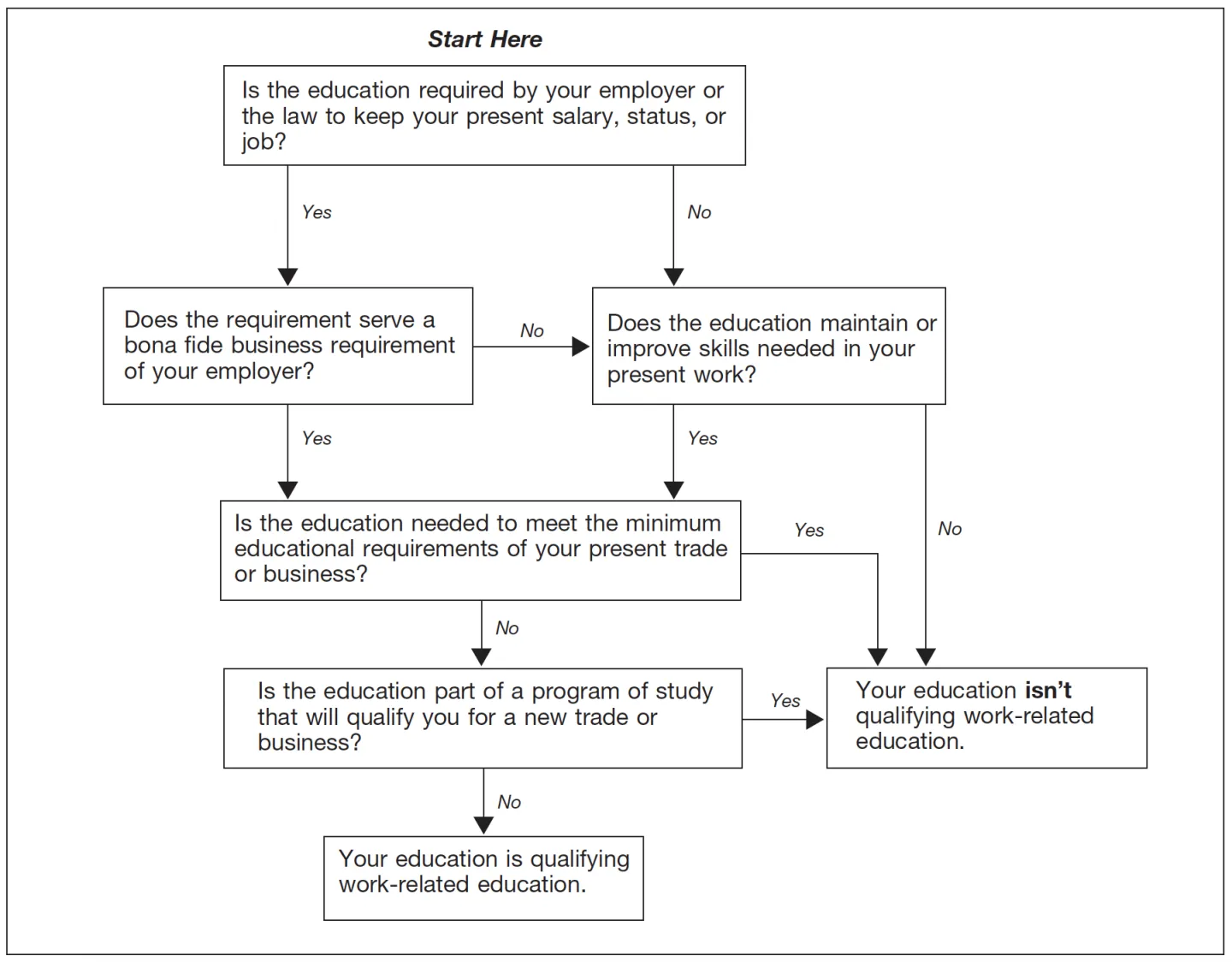

IRC section 162 permits a business deduction for employee education only when the coursework “is required by [the] employer... or maintains or improves skills needed in [the employee’s] present work,” and it expressly denies a deduction when the training “qualif[ies] you for a new trade or business”[5] (emphases added). In the pre‑AI era, this distinction was benign; today, it penalizes firms that teach frontline staff how to collaborate with large language models, to analyze sensor data, or to transition from manual to supervisory tasks.

As illustrated in the IRS flowchart from Publication 970 (figure 1), in order to determine whether work-related education qualifies for tax deductibility, employers must navigate a convoluted two-prong test with multiple disqualifying conditions. Such rigid guidance imposes unnecessary compliance burdens—especially on family-run small businesses with limited administrative capacity. Instead of encouraging skill development, the complexity of these rules often deters employers from offering training at all.

FIGURE 1. IRS decision tree for qualified work-related education deductions under § 162

Source: Internal Revenue Service, Publication 970: Tax Benefits for Education, 2024, 60.

1.3 The 5 percent owner cap in section 127

A qualified educational assistance program (QEAP) may exclude up to $5,250 per employee from income, but no more than 5 percent of total QEAP benefits may flow to individuals who own more than 5 percent of the firm.[6]

For a sole proprietorship or family LLC—forms that dominate America’s enterprise landscape—any owner-student automatically exceeds the 5 percent cap, making compliance impossible. In practical terms, this means small businesses where owners are typically the only employees cannot offer a compliant QEAP under section 127, because 100 percent of benefits would inevitably flow to owners, exceeding the cap. As a result, small-business owners are effectively locked out of using the tax code’s educational expensing provisions, right when they need them most.

By contrast, small businesses can immediately expense up to $2.5 million in physical capital under section 179.[7] This is especially counterproductive in a moment when small businesses are rapidly adopting AI tools and innovations. According to recent findings, open-source AI is acting as a powerful equalizer, allowing smaller firms to compete with larger incumbents.[8] Yet to seize these gains fully, small business owners must train themselves and their employees—a goal the current tax framework actively frustrates. Tax policy should reward, not punish, entrepreneurial initiative in upskilling.

1.4 The nondiscrimination requirement in section 127

Beyond the owner cap, QEAPs are also required to meet nondiscrimination rules, meaning they cannot primarily benefit highly compensated employees.[9] This requirement compounds the access problem for human capital investment. Lower-wage employees, who stand to benefit most from upskilling, often encounter barriers such as lack of awareness, inflexible work schedules, and minimal enrollment support. If highly compensated employees disproportionately utilize the QEAP—even if the program is technically available to all—the business risks failing the nondiscrimination test.

Facing penalties and compliance burdens, employers frequently opt to discontinue these educational programs altogether, inadvertently leaving behind the workers who need training most. If an employer believes that investing in the education of a high-performing employee offers the best ROI, the tax code should not stand in the way. In a dynamic labor market, employers—not rigid tax rules—should decide where training dollars go.

1.5 The $5,250 benefit cap in section 127

Even if a business clears both the owner cap and the nondiscrimination hurdles, QEAP benefits are capped at $5,250 per employee annually. This limit was set in 1986 and has never been adjusted for inflation. That cap would equal approximately $15,500 in today’s dollars, meaning that over four decades it has lost nearly two-thirds of its real value.[10]

1.6 Expensing investment in physical capital without human capital

Until July 2025, the tax code actually tilted against physical capital: Most equipment had to be depreciated over time, while wages and many other labor costs were immediately deductible under section 162.[11] The One Big Beautiful Bill Act (OBBBA) of July 2025 removed that asymmetry on the capital side by permanently restoring 100 percent bonus depreciation under section 168(k) for qualified property with class lives of 20 years or less—a major shift in capital cost recovery.[12]

In contrast, while Congress modernized the treatment of physical capital, it left the modernization of human capital investment behind. Ordinary compensation is deductible, but the tax code continues to ration training through section 162’s job-related and minimum-requirements tests and section 127’s plan-design limits. As shown in table 1, that means a firm can now write off a robot or edge server in year one but must still jump through hoops—or be disallowed entirely—to deduct the training that enables its employees to use that technology. This is the neutrality gap the recommendations below aim to close.

Section 168(k) currently allows 100 percent bonus depreciation for qualified machinery and technology, permitting an immediate write‑off for an AI system regardless of future use.[13] The tax code thus rewards labor‑saving hardware while rationing labor‑augmenting training.

TABLE 1: Consequences of the current restrictions

Source: Author’s representation.

The combined effect of these six restrictions is systematic underinvestment in human capital precisely when rapid technological change demands continual reskilling. Tax code simplicity and neutrality would favor treating education reimbursements like any other form of compensation—taxable unless excluded on broad, simple grounds. All six restrictions identified above should be eliminated to restore parity with physical capital expensing.

2. The Solution: Six Policy Recommendations

Congress can restore neutrality between human and physical capital investment by removing six discrete restrictions. This would involve targeted reforms that require no new programs or spending—only the elimination of outdated restrictions that penalize workforce training. Each recommendation below addresses one of the restrictions identified in section 1 above.

- Repeal the “new trade or business” bar.

Amend section 162 to allow deductions for education that equips an employee (or owner) for any anticipated role within the enterprise. - Eliminate the “minimum education requirement” test.

Amend section 162 to permit deductions for education that equips an employee (or owner) with baseline qualifications needed to perform or transition into roles within the business. - Abolish the 5 percent owner limitation.

Strike section 127(b)(3). Owners who do the work should not be penalized for investing in their own productivity. - Remove nondiscrimination testing for QEAPs.

Rely on general anti‑abuse standards rather than rigid head‑count ratios; let markets, not tax lawyers, decide who most needs training. - Lift the $5,250 cap for QEAPs.

Eliminate the section 127(a)(2) limit entirely, so tax-free educational assistance keeps pace with modern training costs. - Extend full and immediate expensing to all bona fide job‑related training.

Parity with 100 percent bonus depreciation under IRC section 168(k) would eliminate the tax bias that favors machines over human capital.

3. Why Human‑Capital Parity Matters

Restoring parity between investments in human and physical capital is more than a matter of fairness—it is essential for long-run economic growth. Training is a core driver of productivity and wage gains, yet current tax rules discourage firms from making those investments. When the tax code penalizes upskilling, it not only constrains business flexibility but also slows innovation and income growth across the economy. This section explains why human-capital investment yields broad social and economic benefits, how market frictions can cause firms to underinvest in training, and why modernizing the tax treatment of training is critical to sustaining an adaptable, AI-ready workforce.

- Training drives long-run growth. Endogenous-growth theory establishes that skill accumulation is a core engine of long-run GDP growth.[14] Subsequent empirical work confirms that firm-specific, on-the-job training explains a large share of wage and productivity gains as economies mature—making employer-led human-capital investment vital both to national prosperity and to rising worker incomes.[15]

- Market failure and imperfect contracts limit firm-led upskilling. Even though on-the-job training is the most effective way to build workforce skills, classic theory warns that firms will underinvest in general, portable skills—since workers can leave and capture the returns.[16] Yet a rich set of literature shows companies still shoulder significant training costs.[17] While some of this underinvestment could, in theory, be mitigated through complete contracts—such as back-loaded wage schedules (deferred compensation) or training bonds—these workarounds are imperfect and legally constrained.[18] Allowing full and immediate expensing of bona fide training would close the gap, letting firms invest at the socially efficient level.

- Most businesses are nonemployer firms. Of the nation’s 35.7 million businesses in 2022, 29.8 million—roughly 84 percent—were nonemployers run by self‑employed owners.[19] Any rule that locks owners out of QEAPs therefore blocks the predominant US business form from formal skill investment.

Firm-led training reduces automation risk and raises wages. Firm-provided upskilling enables workers to transition into less automatable roles, supporting both employment and income growth. Research shows that training embedded within production settings is more responsive to evolving job demands than generalized retraining.[20] Removing tax barriers to such training would empower firms to build adaptive, future-ready workforces.

4. Distributional and Fiscal Considerations

Sound tax reform requires attention not only to efficiency but also to distributional and fiscal effects. Expanding expensing for job-related training would strengthen economic mobility by extending training opportunities to lower-wage workers and small-business employees who are often excluded under current rules. At the same time, the fiscal impact of these changes would be modest and largely a matter of timing rather than permanent revenue loss. The points below show how modernizing the tax treatment of training advances four key principles.

- Progressivity. Lower‑wage workers benefit when firms scale education programs formerly reserved for managers. Eliminating complex tests frees resources to expand eligibility and outreach.

- Revenue impact. Treasury scores will show timing, not permanent revenue loss—just as with hardware expensing. Experience with bonus depreciation suggests front‑loaded deductions spur investment and broaden the base for future taxable income.[21]

- Simplicity. Reforms collapse multiple pages of regulations into a single principle: If the expense is ordinary, necessary, and job‑relevant, it is deductible.

- Neutrality. The tax code should treat human and physical capital alike. A dollar spent on worker training should receive the same timing and exclusion benefits as a dollar spent on equipment—without the government picking winners and losers between machines and people.

5. Conclusion

America stands at a pivotal moment: Artificial intelligence promises unprecedented gains in productivity and innovation. Yet without swift policy action, its benefits run the risk of bypassing the very workers who power our economy. By dismantling outdated provisions in the Internal Revenue Code, Congress can finally level the playing field between machines and people. Extending full and immediate expensing to all bona fide job-related training will empower businesses of every size to invest confidently in human capital, fueling resilient, adaptable workforces.

Such reforms would yield a trifecta of policy wins: simplicity, by collapsing sprawling regulations into a single, clear standard; neutrality, by treating training dollars as equal to equipment expenditures; and progressivity, by unlocking access for lower-wage and small-business employees who have been shut out of current programs. Experience with bonus depreciation demonstrates that front-loaded deductions spur investment and broaden the future tax base—an effect we can replicate for workforce development.

Rather than taxing AI or erecting complex new entitlement programs, Congress can seize this moment to harness market forces for widespread upskilling.[22] Removing needless compliance hurdles will not only reduce transition pain for displaced workers but also ensure that America’s next wave of technological leadership is matched by a workforce equipped to thrive alongside it. It is both fiscally responsible and economically strategic to make immediate, full expensing of worker training permanent—because when businesses invest in people, everyone wins.

About the Author

Revana Sharfuddin is a research fellow at the Labor Policy Project at the Mercatus Center at George Mason University. Her research centers on labor economics, the evolving nature of work, and the ways labor markets can adapt to foster growth and mobility for workers with diverse backgrounds and needs. She also studies labor market dynamics across different institutional contexts, particularly in developing countries, with a focus on the role of women in the workforce and the interplay between work and family life.

Notes

[1] There is substantial evidence supporting claims for both the investment tilt and training underinvestment in the current tax code. For evidence on how tax preferences shift firms toward eligible equipment investment, see Eric Zwick and James Mahon, “Tax Policy and Heterogeneous Investment Behavior,” American Economic Review 107, no. 1 (2017): 217–48 (bonus depreciation raises investment in eligible capital); and Kevin A. Hassett and R. Glenn Hubbard, “Tax Policy and Business Investment,” Journal of Economic Perspectives 16, no. 4 (2002): 51–72 (survey: investment responds to user-cost/tax changes). For evidence on how employer training responds to tax price via deductions, see Edwin Leuven and Hessel Oosterbeek, “Evaluating the Effect of Tax Deductions on Training,” Journal of Labor Economics 22, no. 2 (2004): 461–88 (an age-40 extra deduction increased training incidence by approximately 15–20 percent at the threshold—largely timing/substitution, but clear evidence that deductions change firms’ training choices). For evidence on how training is a key complement to realizing productivity gains from new tech, including AI, see Lorraine Dearden, Howard Reed, and John Van Reenen, “The Impact of Training on Productivity and Wages,” Oxford Bulletin of Economics and Statistics 68, no. 4 (2006): 397–421 (productivity effects exceed wage effects); Timothy F. Bresnahan, Erik Brynjolfsson, and Lorin M. Hitt, “Information Technology, Workplace Organization, and the Demand for Skilled Labor: Firm-Level Evidence,” Quarterly Journal of Economics 117, no. 1 (2002): 339–76 (IT gains arrive with complementary org/skill investments); and Erik Brynjolfsson, Danielle Li, and Lindsey Raymond, “Generative AI at Work,” Quarterly Journal of Economics 140, no. 2 (2025): 889–943 (measured productivity gains are largest when workers learn/absorb AI tools).

[2] Welch v. Helvering, 290 U.S. 111 (1933).

[3] 26 U.S.C. § 179 (election to expense certain depreciable business assets), Legal Information Institute, Cornell Law School, accessed July 7, 2025, https://www.law.cornell.edu/uscode/text/26/179.

[4] Internal Revenue Service, Publication 970: Tax Benefits for Education, 2024.

[5] Internal Revenue Service, Publication 970: Tax Benefits for Education, 2024.

[6] US Department of the Treasury, “26 CFR § 1.127-2 - Qualified Educational Assistance Programs,” Legal Information Institute, Cornell Law School, accessed July 7, 2025, https://www.law.cornell.edu/cfr/text/26/1.127-2.

[7] 26 U.S.C. § 179.

[8] “New Study Shows Open-Source AI Is a Catalyst for Economic Growth,” Meta Newsroom, May 2025, https://about.fb.com/news/2025/05/new-study-shows-open-source-ai-catalyst-economic-growth/.

[9] “New Study Shows Open-Source AI Is a Catalyst for Economic Growth,” Meta Newsroom.

[10] Aspen Institute, Future of Work Initiative, Modernizing Tax Incentives for Employer-Provided Educational Assistance (Aspen Institute, 2020).

[11] Jeremy Sompels and Jonathan Winterkorn, “100% Bonus Depreciation Returns with the One, Big, Beautiful Bill,” Plante Moran, July 21, 2025, https://www.plantemoran.com/explore-our-thinking/insight/2022/08/the-tcja-100-percent-bonus-depreciation-starts-to-phase-out-after-2022.

[12] Congress.gov, “H.R.1 - 119th Congress (2025-2026): One Big Beautiful Bill Act,” July 4, 2025, https://www.congress.gov/bill/119th-congress/house-bill/1. Buildings still face long cost-recovery periods (typically 27.5 or 39 years). Extending immediate expensing to structures would complete the move toward tax neutrality between different forms of physical capital investment. See Erica York, “Depreciation of Structures,” Tax Foundation, January 7, 2020, https://taxfoundation.org/research/all/federal/depreciation-of-structures/.

[13] Garrett Watson et al., “‘One Big Beautiful Bill Act’ Tax Policies: Details and Analysis,” Tax Foundation, July 4, 2025, https://taxfoundation.org/research/all/federal/big-beautiful-bill-senate-gop-tax-plan/.

[14] Internal Revenue Service, Publication 946: How to Depreciate Property, 2024.

[15] Eric A. Hanushek and Ludger Woessmann, The Knowledge Capital of Nations: Education and the Economics of Growth (MIT Press, 2015); Xiao Ma, Alejandro Nakab, and Daniela Vidart, “Human Capital Investment and Development: The Role of On-the-Job Training,” Journal of Political Economy Macroeconomics 2, no. 1 (November 2020).

[16] Gary S. Becker, “Investment in Human Capital: A Theoretical Analysis,” in Investment in Human Beings, ed. Universities-National Bureau Committee for Economic Research, Journal of Political Economy 70, no. 5, part 2. (October 1962), 9–49.

[17] Daron Acemoglu and Jörn-Steffen Pischke, “Why Do Firms Train? Theory and Evidence,” The Quarterly Journal of Economics 113, no. 1 (February 1998): 79–119; Lisa M. Lynch and Sandra E. Black, “Beyond the Incidence of Employer-Provided Training,” Industrial and Labor Relations Review 52, no. 1 (October 1998): 64–81.

[18] Edward P. Lazear, “Why Is There Mandatory Retirement?,” Journal of Political Economy 87, no. 6 (December 1979): 1261–84; Acemoglu and Pischke, “Why Do Firms Train?”

[19] US Census Bureau, “Census Bureau Releases Demographic Characteristics of Nonemployer Business Owners,” press release no. CB25-TPS.32, May 8, 2025.

[20] Oliver Falck et al., “Training, Automation, and Wages: International Worker-Level Evidence” (IZA Discussion Paper No. 17503,Institute of Labor Economics (IZA), December 2024).

[21] Yale Budget Lab, “Depreciation 101,” accessed July 7, 2025, https://budgetlab.yale.edu/research/depreciation-101; Jason Fichtner and Adam Michel, “Options for Corporate Capital Cost Recovery: Tax Rates and Depreciation” (Mercatus Policy Research, Mercatus Center at George Mason University, January 29, 2015).

[22] Bernard Marr, “Will AI Make Universal Basic Income Inevitable?,” Forbes, December 12, 2024; Daron Acemoglu, David Autor, and Simon Johnson, “Can We Have Pro-Worker AI? Choosing a Path of Machines in Service of Minds” (Policy Memo, MIT Shaping the Future of Work Initiative, September 19, 2023).