- | Financial Markets Financial Markets

- | Policy Briefs Policy Briefs

- |

Risks to Innovative Credit Posed by Emerging Regulatory and Litigation Trends

Fintech lenders present an opportunity to expand credit access and quality. Although such lenders should be subject to appropriate regulation, the regulation must work with the fundamental economic reality of the market.

Nonbank online “fintech” lenders (sometimes known as marketplace or peer-to-peer lenders) have emerged as an important source of credit for individuals and small businesses. In 2015, these fintech lenders issued approximately $36.5 billion in loans in the United States. Although fintech lenders were initially discussed as a possible existential threat to banks, many such lenders rely on banks to facilitate credit. These innovative firms could expand access to credit for millions of American consumers and small businesses that are credit constrained. Unfortunately, recent regulatory and litigation developments that call into question the right of banks to issue and sell loans threaten to impede access to this new credit source. This policy brief outlines the threats to the bank-partnership model used by some fintech lenders, explains why the survival of the model matters, and offers suggestions for action.

THE ROLE OF BANKS IN FINTECH LENDING

Banks play an important role for many fintech lenders, including Lending Club, Prosper, PayPal Working Capital, Square, and Intuit. Those lenders work with a bank to originate a loan that the bank sells to the lender after a short period of time. The lender—which may sell, securitize, or retain the loan on its balance sheet—services the loan and collects payment.

Lenders partner with banks in part because of regulation. Fintech lenders, being creatures of the Internet, are capable of extending credit from coast to coast, but they are subject to onerous state-by-state regulation. Under federal law, banks are able to “export” the interest rate requirements of their home state for loans they make nationwide. This exportation includes not only the maximum allowable interest rate, but also the law governing what constitutes interest. By partnering with a bank, nonbank lenders can provide a consistent product, which is governed by the law of the bank’s home state, and they can avoid having to be licensed by every state in which they extend credit.

Lenders and borrowers benefit. The US Department of the Treasury found that these arrangements have helped fintech lenders improve the credit market. For some borrowers, fintech lenders provide cheaper credit. For others, fintech lenders provide greater access. For example, PayPal Working Capital, which partners with a bank to issue loans to small businesses, has been able to extend credit disproportionately to underserved populations and to areas that have seen a significant decline in the number of banks serving them.

EMERGING THREATS TO THE BANK-PARTNERSHIP MODEL

Despite its benefits, this model might not survive. Recent litigation has undercut the assumption that a nonbank entity can buy a loan from a bank and benefit from the bank’s ability to export rates and terms. This ability is key to the bank-partnership model. Although the recent cases generally do not involve fintech lenders, those cases implicate such lenders and have already had a negative effect on consumers’ access to credit.

The Threat to “Valid when Made”

The ruling of the US Court of Appeals for the Second Circuit in Madden v. Midland Funding LLC calls into question the venerable common-law principle that a loan that is valid and nonusurious at its inception cannot subsequently become usurious (the “valid-when-made” doctrine). In the Madden case, a New York borrower opened a credit card account with a national bank that charged an interest rate that was permitted by the bank’s home state laws but that exceeded New York’s usury cap. When the borrower defaulted, the bank sold the debt, which eventually was purchased by Midland Funding, a nonbank debt purchaser. Midland Funding sought to collect the outstanding debt, including interest that accrued after the debt had been sold. The borrower sued, and the Second Circuit held that the National Bank Act’s interest rate export did not cover the nonbank debt buyer. The court reasoned that its decision did not significantly infringe on the powers of the national bank because the bank could still sell the debt, albeit either to a more limited pool of buyers or at a discount.

Midland Funding appealed the decision to the Supreme Court. The Supreme Court requested the solicitor general’s view, and the solicitor general, along with the Office of the Comptroller of the Currency (OCC), opined that the Second Circuit got the law wrong and that the power to make loans included the power to sell loans to nonbank entities and have the loans retain their validity. Notwithstanding their disagreement with the appellate court on the law, the solicitor general and the OCC argued on procedural grounds that the Supreme Court should not take the case, and the Supreme Court declined to do so.

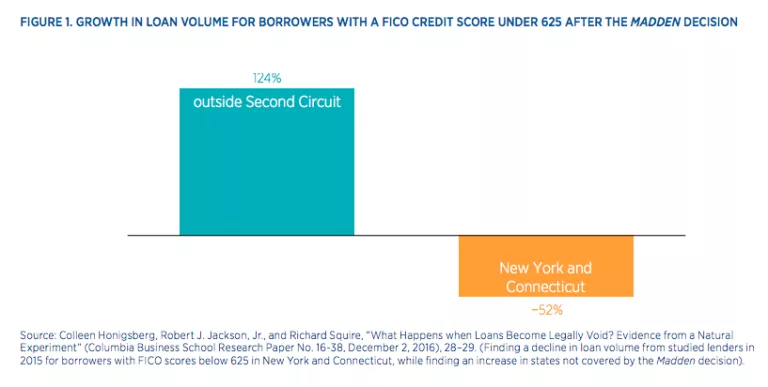

Although the Madden case did not involve fintech lenders, the risk that a bank loan purchased by a nonbank could become invalid has direct implications for the bank-partnership model. The case has produced considerable fallout in the Second Circuit, including a significant reduction in credit for borrowers with lower credit scores (who would be charged a higher rate). Professors Colleen Honigsberg, Robert J. Jackson, and Richard Squire have documented this decline. As shown in figure 1, they find that in 2015 in New York and Connecticut (states in the Second Circuit) the number of loans made by leading marketplace lending platforms to borrowers with FICO credit scores below 625 decreased by 52 percent relative to 2014, while in other circuits the number of loans for comparable borrowers increased by 124 percent. Conversely, loan growth for borrowers with FICO scores above 700 (who would be less likely to be charged interest in excess of New York’s or Connecticut’s usury limits) were comparable between New York and Connecticut and other circuits.

In Madden, there was no dispute about who the lender was. The bank issued the borrower a credit card with the expectation that the borrower would remain a bank customer and sold the debt only when it became nonperforming. Conversely, in the bank-partnership model, the expectation has been that the bank would promptly sell the loan to the fintech lender, which would then own and maintain the customer relationship. This situation raises the specter of the “true lender” doctrine, which has significant implications for what law applies to a loan. If the nonbank entity is deemed to be the true lender, then it does not enjoy broad federal preemption but is instead bound by state usury laws.

Courts take different approaches to the true lender question. Some courts have looked only to the loan contract. For those courts, looking beyond the contract to factors such as the parties’ subjective intent or the risk borne by the bank would add uncertainty and be inconsistent with the exemption from state usury laws that banks enjoy under federal law. However, other courts have looked beyond the contract to the underlying economic reality of the loan at its inception. Those courts consider the role the bank (or tribe) and nonbank perform in the loan process, including advertising, setting underwriting criteria, making loan decisions, and underwriting specific borrowers. The courts also look at the amount of risk borne by each party. If a bank sells a loan quickly or has a standing agreement or prepaid account with the nonbank entity, courts may consider this evidence that the nonbank entity is the actual lender.

Consumer Financial Protection Bureau (CFPB) v. CashCall provides a recent example of the difficulties posed by looking beyond the contract. The CFPB sued a nonbank lender (CashCall) that partnered with Western Sky Financial (WSF), a corporation operating under the law of the Cheyenne River Sioux Tribe (CRST) to issue loans. The contract listed WSF as the lender, and a choice-of-law provision stipulated that the contract was governed by CRST law. Moreover, WSF employees performed underwriting and made lending decisions. Nevertheless, the court found CashCall to be the true lender. The court based its decision on the conclusion that CashCall bore the entire economic risk of the transaction because WSF was contractually insulated from default risk and CashCall funded a reserve to pay for two days’ worth of loans in advance. The court also invalidated the contract’s choice-of-law provision because it found that the CRST did not have sufficient ties to the transaction (even though lending decisions were made in the CRST’s jurisdiction). The court then found that the law of the borrowers’ home state, instead of CashCall’s home state, should apply because the borrowers applied for, paid for, and received funds in their home state.

The court’s analysis in that case highlights the danger of looking beyond the contract. Although it is plausible to view the transaction as occurring in the borrowers’ state, it is equally or even more plausible to view the borrowers as coming to the lender’s state to avail themselves of the lender’s state’s law. The Supreme Court in Marquette National Bank of Minneapolis v. First of Omaha Service Corp. noted that a borrower was always able to go to the lender’s state to avail herself of the lender’s state laws and that applying for a credit card via the mail was similar. Applying for a loan online is a natural continuation that does not justify a departure from this reasoning. The CashCall court’s analysis is also inconsistent with the Supreme Court’s determination in Marquette that the lender’s home state bore the closest nexus to the loan transaction and that defining “location” by where the credit was received would introduce significant confusion.

Fintech lenders are experiencing the fallout from Madden and the true lender cases. A New York borrower sued Lending Club for allegedly making a usurious and invalid loan with WebBank’s “sham” participation. Regulators are also starting to consider whether loans made by fintech lenders with bank partnerships are governed by state law. For example, Colorado has notified fintech lenders that the state considers the loans to be governed by its law. Lenders, for their part, have changed their contracts with their bank partners to tie the bank’s compensation more closely to the long-term performance of the loan.

When lenders change their relationships with banks solely to mitigate regulatory risk, the process is likely to introduce more complexity and cost to the borrower. Why should it matter who the true lender is from a regulatory perspective? If a loan is acceptable for a bank to make, why should a nonbank entity be prohibited from making the same loan? Raising questions about the validity of marketplace loans blocks innovative fintech lenders’ efforts to improve access to credit for marginal borrowers.

WHAT CAN BE DONE

To encourage innovation and access in lending, a clear, consistent regulatory approach is needed. Several potential and nonexclusive paths can be pursued to establish such an approach.

State Coordination

States could change their lending regulations to make it easy for lenders licensed in one state to lend in other states without having to comply with the laws of both states. Although state regulators have discussed such an approach, those discussions may not result in any meaningful change. First, states could have changed their laws to permit greater uniformity for banks in the past, but federal law intervention was necessary to provide reliable exportation. There is little reason to think that this time will be different. Second, even if states were able to establish a uniform standard, state laws could change, so nonbank lenders—unlike their bank competitors—would have to engage in costly, constant monitoring.

Federal Regulatory Relief

The Federal Deposit Insurance Corporation (FDIC) and OCC could issue a regulation clarifying that a bank can sell a loan without compromising exportation. Such a regulation could be modeled on a similar clarifying regulation by the FDIC and OCC about what constitutes interest. Such a federal regulation would preempt state law, and it would provide certainty to lenders and their bank partners.

Expanded Bank Chartering

Fintech lenders could become banks themselves, an approach that would obviate the need for a bank partnership and reduce the complexity and uncertainty of loan transactions. The OCC has proposed creating a bank charter for fintech firms, including lenders. Such a charter would give fintech firms the powers granted to national banks by the National Bank Act. Although this change could be an important step in equalizing the regulatory landscape, fintech firms would not avail themselves of such a charter if obtaining and maintaining the charter were unduly difficult or expensive. Additionally, while a charter might benefit fintech firms, banks seeking to sell loans to nonbank lenders would still run into problems because of the legal uncertainty. The result would be higher costs for borrowers.

Legislation

Congress also could act to create a clear and effective regulatory environment for banks and fintech lenders. For example, codifying the principle of “valid-when-made” would address the concerns raised by the Madden decision. Likewise, legislation could clarify whether a loan should be considered a bank loan if it was sold by a bank soon after it was made and without the bank’s retaining ongoing default risk.

CONCLUSION

Fintech lenders present an opportunity to expand credit access and quality. Although such lenders should be subject to appropriate regulation, the regulation must work with the fundamental economic reality of the market. Ensuring that regulations do not burden fintech lenders more heavily than their bank competitors are burdened and that the validity of their loans is not in doubt are important steps toward helping realize the promises of innovation.

{kind=link}