- | Monetary Policy Monetary Policy

- | Policy Briefs Policy Briefs

- |

Should the Fed Pay Interest on Bank Reserves?

For the first 95 years of its existence, the Federal Reserve (Fed) did not pay any interest on money that commercial banks deposited at the Fed. These deposits at the Fed, which are considered bank reserves, were treated no differently from reserves held as vault cash, which also earned no interest. Then, on October 8, 2008, the Fed suddenly began paying interest on reserves (IOR) deposited at the Fed.

While the decision to pay IOR was not particularly controversial at the time (other central banks had been doing this for years), it radically changed the nature of US monetary policy. The lack of controversy may have partially reflected confusion over the nature of monetary policy before 2008. Hasn’t the Fed always been controlling interest rates? So what makes the adoption of IOR so revolutionary? And should the Fed be paying interest on bank reserves? In my view, there is a danger that IOR will further entrench the Fed’s interest-rate-targeting approach to policy, which proved woefully inadequate during the Great Recession.

What Does It Mean to “Target Interest Rates”?

Before 2008, US monetary policy was implemented primarily through changes in the supply of money. This was even true during the period when the Fed targeted the federal funds rate, the rate that banks pay on overnight loans to each other. Interest rate targeting was mostly implemented through increases and decreases in the supply of money aimed at moving the market interest rate close to the Fed’s target.

With the adoption of IOR, however, policy now focuses on changing the demand for money by adjusting the interest rate that the Fed pays on bank reserves. The Fed can now ease or tighten monetary policy without injecting or removing any money from the economy.

Unfortunately, it is not possible to understand the implications of IOR without first clearing up two big misconceptions about the relationship between monetary policy and interest rates. Many people assume that the fed funds interest rate is directly controlled by the Fed. It’s also widely assumed that a lower interest rate means a more expansionary monetary policy. Neither view is correct.

Before IOR was adopted in 2008, the Fed influenced market interest rates by adjusting the supply of money. When they wanted to decrease interest rates, they injected more money into the economy, and vice versa. However, these short-term interest rates continued to represent market-clearing prices, even when targeted by the Fed. There was no shortage or surplus of loanable funds in the fed funds market.

As an analogy, think about two ways to “control” oil prices. One method would be artificial price controls, such as the ones the United States adopted during the 1970s. Under this system, a maximum price artificially set below equilibrium results in a shortage of oil. Another approach would be to adjust the total supply of oil in order to influence the global price. This method was used by OPEC and does not result in a shortage of oil. Quantity supplied continues to equal quantity demanded.

Monetary policy prior to 2008 was more like the OPEC example; the Fed used its control of the supply of money to nudge market interest rates toward the Fed’s target. Later we’ll see that the Fed adopted IOR in 2008 precisely because it was unhappy with the limitations of this system (namely, that the Fed was able only to target the money supply or interest rates, but not both). Going back to the OPEC example, the oil cartel is able to set a price or an output quota, but not both. IOR allows the Fed to simultaneously control both the interest rate and the money supply.

Low Interest Rates Do Not Represent Easy Money

The second misconception concerns the relationship between interest rates and monetary policy. When reporting on the Fed, the media tends to equate lower interest rates with a more expansionary monetary policy. In fact, as Milton Friedman pointed out in 1997, it’s more often the case that the exact opposite is true:

"Low interest rates are generally a sign that money has been tight, as in Japan; high interest rates, that money has been easy. . . . After the U.S. experience during the Great Depression, and after inflation and rising interest rates in the 1970s and disinflation and falling interest rates in the 1980s, I thought the fallacy of identifying tight money with high interest rates and easy money with low interest rates was dead. Apparently, old fallacies never die."

Why is there so much confusion on this point? Probably because on any given day, a decision by the Fed to lower its fed funds target makes policy more expansionary (or “easy”) than if they had not cut interest rates. But over longer periods of time, just the opposite is true.

A decision by the Fed to increase the money supply will initially decrease short-term interest rates, owing to the liquidity effect. This refers to the fact that to get the public to hold larger cash balances (i.e., more liquidity), interest rates must decrease when new money is injected. In the longer-term, however, an increase in the money supply will raise interest rates to higher levels. The expansionary monetary policy will lead to higher inflation and perhaps higher economic growth. Both of these factors tend to push nominal interest rates higher.

The Fisher effect refers to the fact that when inflation rises, lenders demand higher nominal interest rates to compensate for the loss of purchasing power owing to inflation. The “income effect” refers to the fact that there is more demand for credit in a booming economy, which puts upward pressure on interest rates (see figure 1 for a depiction of these effects).

To summarize, an expansionary monetary policy will decrease interest rates for a brief period of time but will eventually lead to faster growth and higher inflation, which push interest rates higher in the medium to long term. Importantly, at any given time, America is more likely to be experiencing the medium- to long-run effects of earlier monetary policy changes, rather than the short-run effect of a current change in policy. This is why Friedman said that low interest rates are often a sign that money has been tight. Don’t confuse “right now” with short run and “later” with long run. What is happening to interest rates today often reflects the long-run effect of policy decisions made a year or two ago. Falling interest rates usually mean that money has previously been tight.

Why Was IOR Adopted in October 2008?

Before the payment of interest on reserves, banks faced an opportunity cost of holding reserves that was equal to the nominal interest rate. This was a sort of implicit tax on bank reserves, and the Fed was concerned that it led banks to hold too little liquidity.

In 2006, Congress gave the Fed permission to begin paying IOR starting in 2011. Soon after Lehman Brothers failed in September 2008, Congress acceded to a Fed request to immediately begin paying interest on bank reserves. The decision was relatively uncontroversial at the time the policy was adopted in early October, but that’s only because most people had no idea why the Fed wished to adopt the policy.

During September 2008, the Fed had injected enormous amounts of liquidity into the banking system. That sort of monetary injection would normally drive interest rates to very low levels. As noted earlier, under the traditional policy of targeting the fed funds rate, the Fed can control the money supply or interest rates, but not both. The Fed was determined to inject new money into the economy to help the banks, but it did not wish to see interest rates fall below its target of 2 percent (later cut to 1.5 percent on October 8, 2008). Without the ability to pay interest on reserves, interest rates would have immediately fallen to zero after the large quantity of money was injected.

Astute readers might wonder what would have been so bad about interest rates falling to zero during the financial crisis. In retrospect, this would indeed have been an appropriate move by the Fed. In his memoir, Ben Bernanke admitted that the Fed erred in not cutting rates more quickly after Lehman failed in September 2008.

At the time, however, the Fed was more worried about inflation than recession. Although America was already nine months into the worst recession since the 1930s, during September and October of 2008 the Fed was concerned that the economy was in danger of overheating. The policy of IOR was a way of sterilizing all the new money that was being injected into the economy for the purpose of rescuing the banking system.

The term “sterilization” refers to policies that cause newly injected money to be set aside as a store of value, rather than circulate as a medium of exchange. One can think of IOR as a policy where the Fed pays banks to hold the new money being injected into the economy, rather than have it move out into circulation. Cynics complained that the Fed was trying to rescue Wall Street without giving a boost to Main Street. More likely the Fed simply misjudged the economic situation.

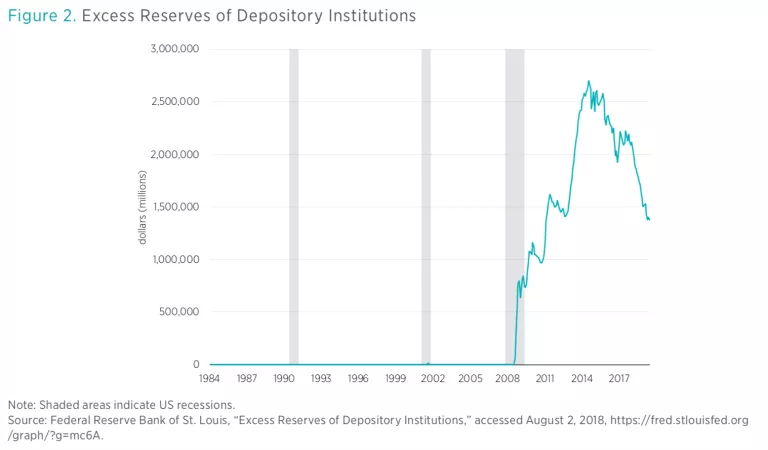

Prior to 2008, new injections of money quickly found their way into circulation. That’s because banks could earn a positive interest rate on safe assets such as T-bills, but the Fed paid no interest at all on bank reserves. Thus, banks got rid of excess reserves (beyond their legally required reserves) as quickly as possible, like a hot potato. Once the Fed began paying IOR at a rate slightly higher than T-bill yields, however, it became much more attractive for banks to hold excess reserves. Figure 2 shows the dramatic impact of IOR, which caused excess reserves to quickly soar from a few billion dollars to a peak of nearly 2.8 trillion dollars:

Unlike the fed funds rate, the interest rate on reserves is not a market price; it’s an administered price set by the Fed. It’s useful to think of IOR as a government subsidy—or a tax if the rate is set at a negative level, as in Europe and Japan. A higher IOR is a subsidy that encourages banks to hold onto reserves and makes policy tighter. A lower IOR encourages banks to move more money out into the economy and makes money looser.

When dealing with an equilibrium market price such as the fed funds rate, one does not want to “reason from a price change.” As explained earlier, it’s dangerous to assume that a lower fed funds rate represents easier money. For instance, money got tighter during 2007 and 2008, even as the fed funds rate fell, because the economy’s equilibrium or “natural” interest rate was falling even faster. Money was getting effectively tighter, despite the lower interest rate.

In contrast, a lower IOR really does make money easier. As an analogy, when the market price of oil rises, one may see more consumption if the increase is the result of more oil demand, and less consumption if the price increase is the result of less oil supply. In contrast, a higher tax on oil always tends to reduce consumption, and an oil subsidy always tends to boost consumption. A policy of IOR is more like a tax or subsidy, not a market price. Ironically, the misconception that many people had about the fed funds rate—that a lower rate meant easier money—is actually true for interest on reserves. Ceteris paribus, a lower IOR does in fact represent a more expansionary monetary policy, as it encourages banks to move money out into the economy, where it will boost total spending.

Why Do Some Central Banks Pay Negative Interest on Reserves?

The European Central Bank, the Bank of Japan, and a number of other central banks pay a negative interest rate on reserves. In other words, they impose a tax on bank reserves. Many people are confused by this policy, and in fairness even many economists were caught off guard when the policies were first implemented. The average person was confused because the whole idea of negative interest rates seems somehow unnatural.

Economists typically don’t have any objection to the general concept of negative rates, but assumed the concept would never work because investors always had an alternative option: zero-interest-rate currency. Indeed, until recently, it was assumed that the zero interest rate on cash created a sort of “zero lower bound” on nominal interest rates. Why would anyone hold money in a bank deposit at negative rates, when they could hold cash earning a zero rate of return?

It turns out that many large institutions are willing to hold large sums of money at slightly negative interest rates. Whether because of the risk of fire or theft, or because of heightened government scrutiny over unusually large cash holdings, large institutions do not seem willing to hold billions of dollars of currency. As a result, a number of central banks have been able to successfully drive the nominal interest rate into slightly negative territory. To be sure, there are limits as to how far negative that interest rates can go. At some point the demand for cash would increase sharply. So far, no central bank has been able to push market rates down to negative 1 percent.

After the Fed adopted a policy of IOR in late 2008, I argued that the interest rate should be set at a negative level. At the time, many scoffed at this suggestion, doubting whether the effect would be expansionary. After all, negative IOR is a tax on reserves, and we normally think of taxes having a negative impact on the economy.

But money is very different from other goods. Less demand for goods is contractionary for the economy and often leads to higher unemployment. Money is just the opposite. Less demand for money is expansionary for the economy, boosting employment. That’s because money is the other side of any transaction. People can reduce their holding of money only by purchasing goods, services, or financial assets. Thus, a tax on bank reserves (negative IOR) will tend to boost spending on other goods, services, and assets. Indeed, asset markets reacted to announcements of negative IOR in Europe and Japan as if negative IOR were an expansionary monetary policy shift.

On the other hand, people should not expect too much from negative IOR. Central banks have been reluctant to push IOR too far negative, and thus far the program has only had a modest expansionary impact, where it has been tried. In that respect it is sort of like quantitative easing (QE)—a useful tool, but often employed as a defense mechanism where the overall policy regime has failed and pushed the economy deep into recession. A better policy would be to adopt a monetary regime that did not require emergency measures such as QE and negative IOR. One such alternative policy is nominal GDP (NGDP) level targeting, at a trend rate of NGDP growth high enough to keep nominal interest rates above zero.

Why Is the Fed Continuing to Use IOR, even after the Emergency Is Over?

The injections of excess reserves during late 2008 were aimed at providing emergency liquidity to an interbank loan market that was freezing up. There was a general fear of more bank failures, and there was a reluctance to lend money. Now that the emergency is long past, why do these excess reserves remain in the system?

Recall that the Fed originally asked for permission for IOR back in 2006, long before the recession. In addition, many foreign central banks had been paying interest on bank reserves for many years. The Fed argues that monetary policy operates more efficiently when the banking system has plenty of liquidity, and a policy of IOR insures a high level of excess reserves without triggering high inflation.

Critics such as George Selgin and David Beckworth argue that IOR led banks to substitute reserves for loans on their balance sheet, making it harder for small firms to gain credit. Selgin also points out that IOR allows central banks to accumulate extremely large balance sheets and engage too heavily in credit allocation in the economy. For instance, the Fed purchased large quantities of mortgage-backed securities after 2008 with the aim of propping up the housing market. He also argued that the policy undercut the interbank loan market for fed funds, as banks had little incentive to lend out reserves.

In addition to all of these problems, there is another potential drawback to a policy of IOR. This policy moves central banking ever further away from a “quantity of money” approach to policy, and toward a “rental cost of money” (i.e., interest rate) approach to policy. The downside of targeting interest rates became very clear in late 2008, when the nominal interest rate fell close to zero in the United States. Because the Fed chose not to implement negative IOR, its primary policy tool became stuck at zero, and thus the policy tool became ineffective.

To a much greater extent than most people realize, monetary policy is mostly about communication. Thus, the direct effect of a one-quarter percent cut in the target interest rate might be small, but the impact of what this action communicates about the future path of policy can be quite large. When nominal interest rates fall to zero, central banks that rely on interest rate targeting become “mute,” unable to communicate with the public unless they shift to a radically different policy regime.

Compare this to policy tools that do not have a zero lower bound, such as the money supply or the exchange rate. With those policy instruments, central banks can continue to communicate their policy intentions even after interest rates fall to zero. The central bank of Singapore uses the exchange rate as its policy instrument, not interest rates, and thus never faces the problem of being unable to signal to the public by adjusting its policy instrument.

One might think of interest rate targeting as like a car with a steering mechanism that works 90 percent of the time but locks up when driving on twisty mountain roads. Interest rate targeting works fine most of the time but locks up just when it’s most needed—in a deep recession. Admittedly, interest rate targeting is not identical to a policy of paying IOR, but in practice IOR is a way for central banks to double down on the use of interest rates as a policy instrument. At the same time, changes in the money supply become less effective in impacting the economy under a system of IOR.

The monetarist critique of Keynesian policy during the 1970s focused on how central banks relied too much on interest rates and paid too little attention to changes in the quantity of money. These monetarist insights may be lost if policymakers continue to make the short-term interest rate increasingly central to the operation of monetary policy.