- | Labor Markets Labor Markets

- | Public Interest Comments Public Interest Comments

- |

The Labor Market Effects of Codifying the New Jersey ABC Test

The proposed rule would likely cut jobs, hurt freelancers, and reduce work opportunities—especially for women

Codification of ABC Test for Independent Contractor Status (Proposed Rule N.J.A.C. 12:11)

Agency: New Jersey Department of Labor and Workforce Development

Comment Period Opens: May 5, 2025

Comment Period Closes: August 6, 2025

Comment Submitted: August 4, 2025

The New Jersey Department of Labor and Workforce Development (NJDOL) has proposed to codify its interpretation of New Jersey’s ABC test (N.J.A.C. 12:11). The proposed regulation presents a narrow interpretation of the case law and creates a significantly more restrictive version of the state’s current ABC test.

We are grateful for the opportunity to submit a comment to the NJDOL in response to its proposed rule. Our comment presents rigorous and causal empirical research about the effects of the proposed rule and is designed to aid the NJDOL as it considers the merits of the rule.

Executive Summary

Comprehensive empirical research analyzing the economic impacts of similar ABC test implementations across multiple states, including specific findings for New Jersey, indicates that the NJDOL’s proposed rule is highly likely to negatively impact W-2 employment, self-employment, and overall employment in the state, with a pronounced adverse effect on working women. Findings from our research team demonstrate that restrictive ABC tests lead to significant unintended consequences that harm both workers and the broader economy, ultimately contradicting the stated policy objectives of protecting workers and ensuring fair competition.

In particular, our results show that in New Jersey the current ABC test has already caused decreases in employment across the board:

- a 3.81% decrease in W-2 employment (contrary to the goals of New Jersey policymakers)

- a 10.08% decrease in self-employment

- a 3.95% decrease in overall employment

More troubling, the New Jersey data reveal stark gender disparities: Women’s traditional W-2 employment declined by 7.40%, while men's showed no significant change—raising concerns about disproportionate impacts on women following the policy change. This pattern suggests that the NJDOL’s proposed rule—which creates a more restrictive version of the state’s current ABC test—may inadvertently create gender-specific barriers in the labor market while failing to deliver its promised worker protections.

ABC tests appear to produce an overkill effect, in which legitimate independent contractors cannot maintain working relationships with hiring entities. While the policy may succeed in reclassifying some genuinely misclassified workers, any benefit is outweighed by the harm to properly classified independent contractors who lose their independent work opportunities without obtaining W-2 employment under the stricter criteria. The result is net job destruction not job protection.

Indeed, state audits that use random sampling methods consistently find that only 1–4% of workers across all industries are actually misclassified, with most cases concentrated in construction services as well as personal and care services. This means 95–99% of independent contractor relationships are legitimate and properly classified. Implementing sweeping ABC test regulations to address such a narrow problem concentrated in a handful of industries risks causing significant collateral damage to the overwhelming majority of properly classified work arrangements.

Worker-classification laws should strike a balance: strong enough to address bad-faith misclassification, but not so restrictive that they deny legitimate freelancers and entrepreneurs the opportunity to work independently. Unfortunately, ABC tests fall on the extremely restrictive end of the spectrum and therefore fail that balancing act. The NJDOL’s proposal tips the balance further to the extreme.

Rather than codifying a more restrictive intrepretation of the ABC test across the board—which would harm legitimate workers in order to catch a small minority of violators—New Jersey could instead pursue targeted enforcement in industries with documented misclassification problems. This more precise approach would maximize enforcement effectiveness while protecting the 95–99% of independent contractors who are properly classified and choose this work arrangement. Such targeted policy would achieve the stated goals of combating misclassification without the devastating unintended consequences documented both in our research and by anecdotal evidence from workers in California.

Research Background and Methodology

As economists specializing in labor market policy, our research team has conducted the first causal empirical analysis of ABC tests across the United States from 1990–2024.[1] This research, currently under review for publication, analyzes employment outcomes in nine states that have implemented ABC tests: California, Hawaii, Illinois, Maine, Massachusetts, New Hampshire, New Jersey, New Mexico, and Nevada.

The study uses the Callaway and Sant’Anna Difference-in-Differences (DiD) approach along with an event-study framework tailored to settings with staggered policy adoption. This methodology isolates the causal effects of ABC test implementation on overall employment, traditional (W-2) employment, and self-employment.

We use monthly employment data from the Bureau of Labor Statistics and the Census Bureau’s Current Population Survey (CPS). States that adopted the ABC test are treated as the treatment group, and states that retained right-to-control or common law classification standards serve as the control group. Our team also consulted with a law firm to confirm the identity and implementation timing of ABC test states.

Key Findings: ABC Tests Reduce Employment Across All Categories

Our comprehensive analysis reveals that restrictive ABC tests fail to achieve their intended policy objectives and instead produce significant unintended negative consequences for workers. The findings presented represent causal effects—not correlations—established through rigorous econometric analysis using a DiD methodology with multiple robustness checks. All key results are statistically significant at conventional levels, indicating that these outcomes are highly unlikely to have occurred by chance and instead represent systematic policy-induced labor market disruptions. [2]

The implementation of an ABC test led to the following statistically significant declines:

- a 4.73% decrease in W-2 employment (contrary to the goals of policymakers)

- a 6.43% decrease in self-employment

- a 4.79% decrease in overall employment

These numbers represent changes in employment in ABC test states relative to control states (those that retained the common law or right-to-control test). Occupations with high concentrations of independent contractors experienced the largest reductions in employment.

The findings demonstrate that ABC tests do not simply reallocate workers from independent contractor status to traditional employment, as intended. Instead, they reduce employment across all categories, exacerbating job insecurity and restricting access to meaningful work.

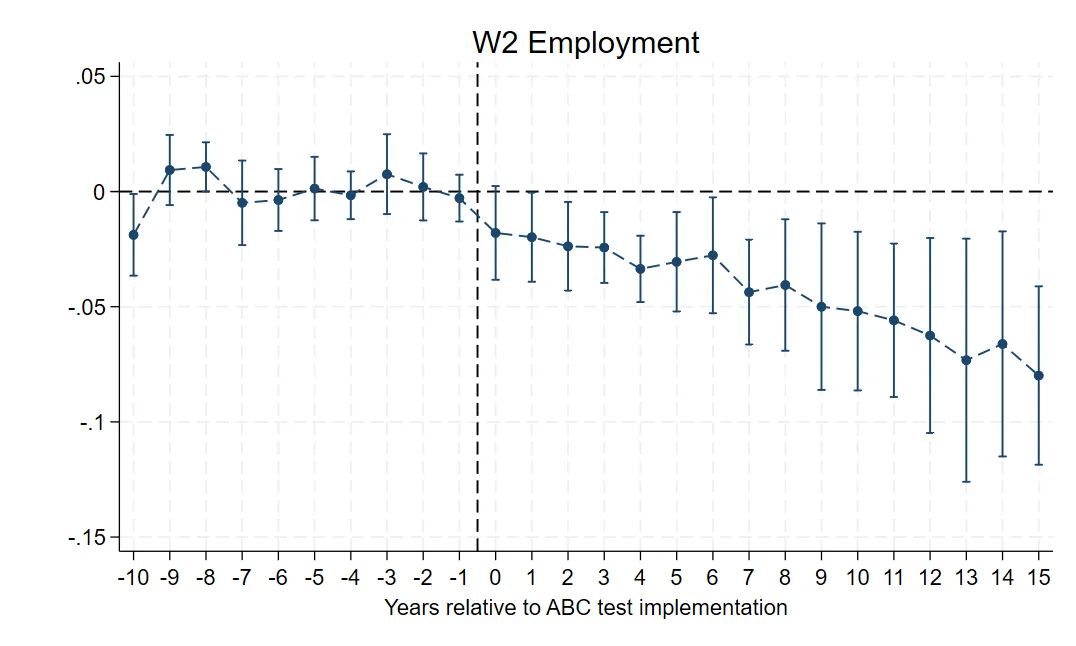

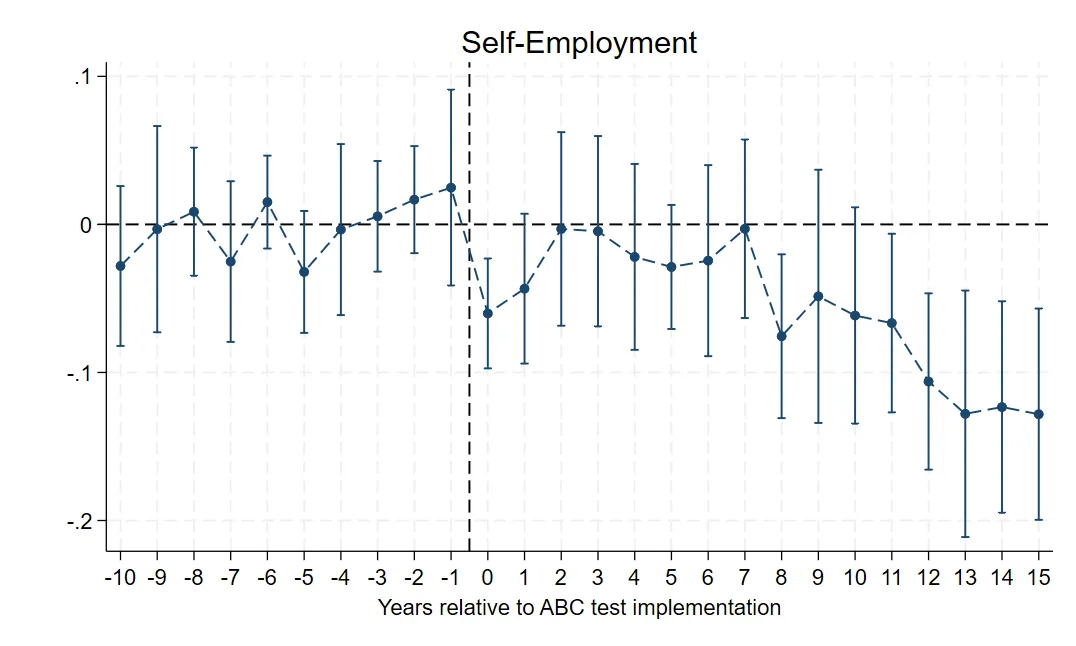

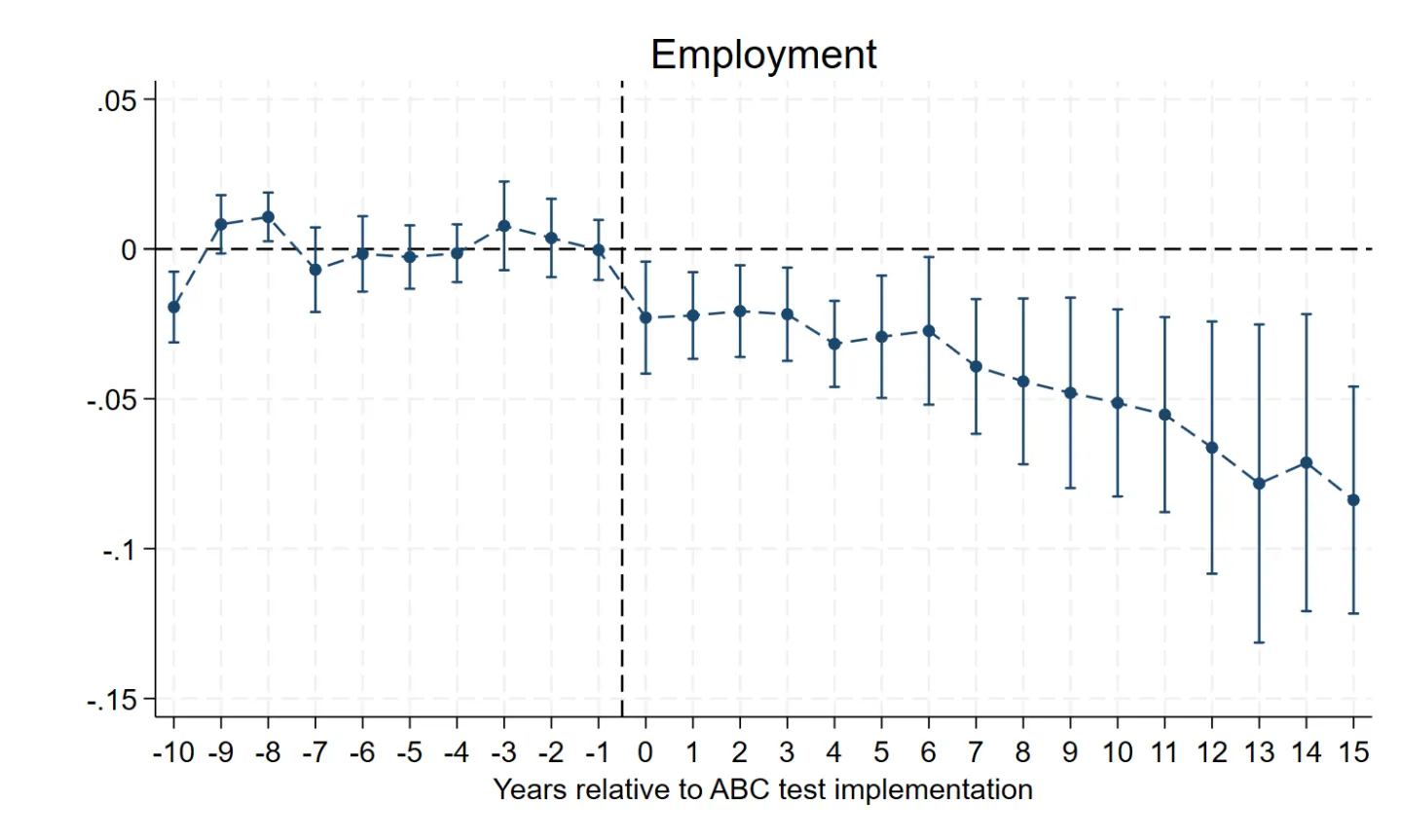

Below we present event study graphs that further illustrate the negative effects of the ABC test on traditional (W-2) employment, self-employment, and overall employment over time (see figures 1–3). These visualizations from our event study methodology support the main DiD results. In the graphs, the vertical dashed lines indicate the point at which the ABC test was implemented, and the y-axis coefficients represent the estimated change in employment relative to the pre-implementation period.

As illustrated, both overall employment and traditional (W-2) employment exhibit a significant and sustained decline following ABC test adoption, with effects worsening notably over the subsequent 5–15 years. In contrast, self-employment shows an immediate sharp drop, followed by a slight brief rebound and then a prolonged, pronounced decline.

While our data do not allow us to pinpoint the specific mechanisms at play, the empirical patterns suggest an overkill effect in which legitimate independent contractor relationships are systematically disrupted. Although the policy may succeed in reclassifying some genuinely misclassified workers as intended, any limited benefit is outweighed by a much larger negative impact on properly classified independent contractors who no longer meet the stricter legal criteria. This mechanism explains the declines—rather than the expected reallocation from independent contracting to payroll jobs—we observe in both traditional W-2 employment and self-employment,. The result is net job destruction not job protection.

FIGURE 1. ABC test impact on traditional (W-2) employment

FIGURE 2. ABC test impact on self-employment

FIGURE 3. ABC test impact on overall employment

New Jersey–Specific Analysis: Significant Negative Impact on Workers

To generate the New Jersey–specific results, our research team conducted a targeted analysis isolating New Jersey as the sole treatment state, while maintaining the same control group of common law and right-to-control states to ensure methodological consistency with our broader multi-state study.

This approach leverages New Jersey’s ABC test implementation period from 1995 to 2024, providing nearly three decades of data.[3] The findings represent true causal effects—not spurious correlations—all statistically significant at conventional levels.

Our analysis finds that New Jersey’s current ABC test has caused the following employment declines:

- a 3.81% decrease in W-2 employment (contrary to the goals of New Jersey policymakers)

- including a 7.40% reduction in female W-2 employment (indicating disproportionate harm to women’s W-2 employment opportunities)

- a 10.08% decrease in self-employment

- a 3.95% decrease in overall employment

These numbers reflect changes in New Jersey employment outcomes under the ABC test relative to control states (those that maintained common law or right-to-control tests during this period), allowing for a clean comparison of policy effects. Consistent with our national findings, New Jersey’s ABC test produced significant negative impacts on both W-2 employment and self-employment— contradicting the policy’s stated objective of increasing traditional employment. Even more troubling is that the New Jersey data reveals stark gender disparities: Women’s traditional W-2 employment declined by 7.40%, while men’s showed no statistically significant change. This pattern suggests that the NJDOL’s proposed rule—which creates a more restrictive version of the state’s current ABC test— may inadvertently create gender-specific barriers in the labor market while failing to deliver its promised worker protections.

California's Experience: A Cautionary Tale

A separate study by our research team analyzing California’s Assembly Bill 5 (AB5)—the most stringent implementation of the ABC test in the nation—provides compelling additional evidence of the harmful effects of such policies. After California codified the ABC test into law through AB5, [4]

- self-employment fell by 10.5% for non-exempt occupations,

- overall employment decined by 4.4% for non-exempt occupations, and

- no robust evidence emerged of increased traditional employment in those same non-exempt occupations.

Additionally, news outlets reported business closures and relocations following AB5’s enactment. The real-world consequences proved severe enough that California faced significant political backlash, ultimately requiring the state to carve out exemptions for more than 100 occupations—a tacit acknowledgement that the policy was causing more harm than benefit. Even with these numerous carve-outs, the remaining non-exempt occupations continued to experience substantial economic disruption, without achieving the law’s stated objectives of increased worker protections and traditional employment.

The California experience serves as a cautionary tale: Even the most aggressive ABC test implementation, initially backed by extensive political support and later modified with industry specific exemptions, failed to deliver its promised benefits, while it created documented harm to workers. NJDOL’s proposed regulation will likely have a more widespread and severe impact on workers because, unlike California’s AB5—which included exemptions for over 100 industries—there are no indications of any exemptions under the proposed rule.

Policy Implications

According to state reports using a random audit approach, less than 5% of workers across all industries are misclassified, with most cases concentrated in construction services and personal and care services. Critically, state audit reports using random sampling methods—which provide the most statistically representative estimates—consistently find that only 1–4% of workers across all industries are misclassified.[5] This means 95–99% of independent contractor relationships are legitimate and properly classified. Implementing sweeping ABC test regulations to address such a narrow problem concentrated in only a handful of industries risks causing massive collateral damage to the overwhelming majority of properly functioning independent contractor arrangements.

Rather than adopting broad ABC test codification that harms legitimate workers while attempting to catch a small minority of violators, New Jersey could instead pursue targeted enforcement in industries with documented misclassification problems. This more precise approach would maximize enforcement effectiveness against actual violations while protecting the livelihoods of 95–99% of independent contractors who are properly classified and choose this work arrangement. Such targeted policy would achieve the stated goals of combating misclassification without the severe negative consequences documented in our research.

Conclusion

The empirical evidence strongly suggests that codifying NJDOL’s interpretation of New Jersey’s ABC test would have the following effects:

- Reduce overall employment, self-employment, and W-2 employment in the state

- Disproportionately harm women’s W-2 employment prospects

- Fail to increase traditional employment as intended

These outcomes directly contradict the policy’s stated objectives of protecting workers. Rather than helping workers, the proposed rules risk harming the very people they intend to protect, while imposing significant costs on New Jersey’s economy. The weight of empirical evidence demonstrates that broad ABC test implementation creates more problems than it solves.

Worker-classification laws should strike a balance: strong enough to address bad-faith misclassification, but not so restrictive that they deny legitimate freelancers and entrepreneurs the opportunity to work independently. Unfortunately, ABC tests fall at the most restrictive end of the regulatory spectrum, and therefore fail to achieve that balance. The NJDOL’s proposal tips the balance further to the extreme.

Notes

[1] This research was conducted with Markus Bjoerkheim. A summary of the results can be found here.

[2] “Conventional levels” typically refer to p-values less than 0.05, with stronger significance indicated by lower thresholds. In this analysis, significance levels range from p < 0.01 to p < 0.001.

[3] The New Jersey ABC test has applied to wage and hour law since at least 1995, as documented in the New Jersey Supreme Court Case Hargrove v. Sleepy's (2015).

[4] Liya Palagashvili et al., “Assessing the Impact of Worker Reclassification: Employment Outcomes Post-California AB5” (Mercatus Working Paper, Mercatus Center at George Mason University, Arlington, VA, January 31, 2024).

[5] We reviewed all accessible state audit reports on worker misclassification listed in the appendix of the National Employment Law Project’s (NELP) 2020 study, “Independent Contractor Misclassification Imposes Huge Costs on Workers and Federal and State Treasuries.” We also included newer reports not in the NELP study, such as Minnesota’s 2024 and Maryland’s 2025 audits. From these, we selected only those that used random audits, as they offer the most representative data on misclassification across industries. In contrast, targeted audits—based on referrals or complaints—are biased, since they disproportionately include employers or industries more likely to misclassify workers, thereby inflating misclassification rates. Random audits give every employer an equal chance of selection, ensuring far more accurate estimates.