- | Low Interest Rates and the Economy: A Mercatus Colloquium Low Interest Rates and the Economy: A Mercatus Colloquium

- | Monetary Policy Monetary Policy

- | Research Papers Research Papers

- |

The Effects of Interest Rates on Treasury Revenue Policy

This series about the economic and fiscal effects of an interest rate change has left as largely unaddressed how a policy of maintaining historically low interest rates and how an abrupt departure from that policy would affect the Treasury Department’s fiscal and economic initiatives. Those effects, however, should not be diminished or overlooked. Indeed, one of the policy portfolios that has been whipped most by the current zero-bound interest policy has been that of the Treasury.

The question posed by this colloquium has two branches, both of which are pertinent to understanding the problems that zero-bound interest rates have caused the Treasury. On the one hand, historically low interest rates have significantly reduced the cost of borrowing operating and program funds, thus avoiding the politically sensitive territory of raising taxes or cutting spending in order to meet cash flow needs.

On the other hand, a significant increase in interest rates would likely (a) undermine this policy of deficit financing, (b) raise the prospects of lower income from the Federal Reserve, and (c) expose the US dollar to possible devaluation. This short essay will address both the effects of low interest rates and the effects of rising rates.

The First Branch: The Effects of Low Interest Rates

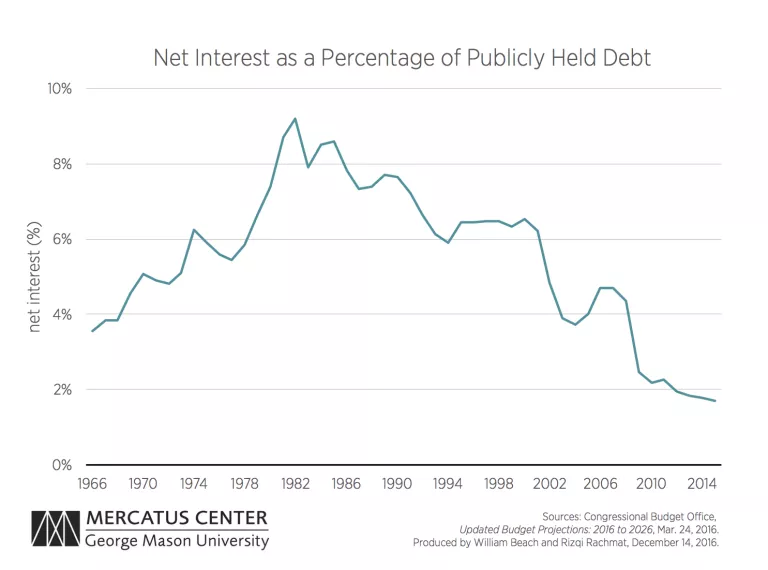

A widespread assumption among economists is that the Federal Reserve’s zero-bound interest rate policy has supported deficit financing as opposed to other fiscal moves to reduce a reliance on borrowing. Although interest rates generally have been falling for the past 35 years, borrowing costs for new debt issues were—in some cases—five to eight times lower than they were 10 to 20 years ago. The 10-year Treasury rate reached 5.14 percent in June 2007, only to fall to 1.56 percent in July 2012. It had been as high as 7.6 percent at the beginning of 1995. Such dramatic declines in borrowing costs put the Treasury in the driver’s seat when it came to funding deficits. Figure 1, which uses data from the Congressional Budget Office’s (CBO’s) historical data series for outlays, revenues, and debt, shows the path of net interest as a percentage of publicly held debt.

The average interest rate on publicly held debt fell below 2.5 percent in 2009 and declined rapidly thereafter. Although the overriding consideration of the Treasury during the recession and recovery was simply funding the trillions in new debt, the low and declining average and marginal costs of doing so no doubt encouraged borrowing.

Would new borrowing rates that were twice or three times as high have been a higher hurdle for massive federal borrowing? Most likely such rates would have slowed the growth of deficit financing. This intuition is supported by the sharp congressional debt-limit debate of 2011 that resulted in the Budget Control Act of that year. Had interest costs been rising as a percentage of borrowing, Congress would have had added impetus to contain outlays and likely would have complained less about having to do so.

One salutary fiscal benefit of low rates (at least since 2008) was the strong remittances that the Federal Reserve paid to the Treasury during those heavy borrowing years. When interest expenses for the Federal Reserve are low and income from its portfolio of financial assets is growing, stronger Federal Reserve profits emerge. Those profits, minus the system’s operating costs, are remitted to the Treasury.

In 2008, the CBO projected remittances from the Federal Reserve to be about $47 billion, or about 1.8 percent of total revenues. By 2015, remittances had grown to $117.1 billion, or 3.5 percent of total revenues. (The Federal Reserve reported that the year’s remittances included a one-time transfer of $19.3 billion to reduce Reserve Bank capital surpluses. Interest income on securities totaled $113.6 billion. Interest expenses amounted to $6.4 billion.) Thus, the Treasury has booked a revenue stream of nearly 4 percent of all revenues that could easily be diminished if rising interest rates significantly boost interest expenses on bank reserves.

Not only did low rates encourage an unbalanced approach to funding operations and programs and promote reliance on interest-sensitive sources of revenue, but also they may have masked danger in the Treasury’s own portfolio of interest-earning investments. I refer, of course, to the student loan portfolio.

In the unified budget accounting system used by the White House and the CBO, account code 900 is where interest earnings and outlays are accumulated. Many observers of the federal government’s fiscal problems fail to note that “net interest” is, indeed, net. What does that mean? Net interest is the result of subtracting interest earnings from payments to bondholders.

For example, interest outlays to bondholders in 2015 equaled about $402 billion. From that figure was subtracted about $179 billion in interest earnings to obtain a net interest number of $223 billion. According to the White House Office of Management and Budget, about 25 percent of the income in this account comes from interest earnings on student loans. A careful reader will immediately see that the Treasury’s fiscal plan is based in no small part on the payment performance of student loans. (Total earnings on student loans involve other factors beyond the interest components, many of which are expenses for administration and operation of the loan programs. USA Today reported that “profits” from the federal student loan programs equaled $41.3 billion in 2013, or about $6 billion more than interest earnings.)

To sum up the first branch, the low-interest-rate policy may have had a major effect on creating problematic fiscal imbalances by (a) easing the cost of deficit financing; (b) building reliance on revenue sources that are sensitive to interest rate movements, such as Federal Reserve remittances; and (c) creating an explosive element in the net interest account, should rising rates degrade the performance of new student loan issues and slow the economic ability of current loan holders to repay their debt.

The Second Branch: The Effects of Rising Rates

Although the academic jury is still out concerning the positive economic effects of especially low interest rates (many of my colleagues in this colloquium have written about this topic), the fiscal effects mentioned earlier should raise alarms. When the prospect of rising rates is added to those imbalances, prospects for serious fiscal and economic harm could appear.

Of course, the fiscal effects of rising rates depend fundamentally on what the Congress does to move toward balancing revenues and outlays. If the 115th Congress that commences on January 4, 2017, shows no more capacity for hard fiscal choices than did its predecessors, then the primary problem that the Treasury and the Federal Reserve will face is a condition called “fiscal dominance.”

CBO currently forecasts rapidly rising deficits between now and 2026. Thus, by the middle of this upcoming 10-year period, or by 2022, the deficit will once again be more than $1 trillion. Over the entire 10-year period, deficits will sum to $9.4 trillion. The Treasury will no doubt fund that amount by borrowing, and its partner in that endeavor will once again be the Federal Reserve. However, deficits will only get worse beyond 2026 before they peak in the mid-2030s and begin annual declines (assuming that inflation and the value of the dollar remain stable).

The prospect of ever-worsening deficits after 2016 prompted internal debate at the Federal Reserve over whether the only function it would perform would be purchasing Treasury debt. That purchase would mean, among other things, that monetary policy could have the dual responsibility of keeping the Treasury’s borrowing costs low and protecting the dollar from devaluation pressure.

A Federal Reserve conference (largely off the record) was held in New York in February 2013 to discuss the likelihood of fiscal dominance. The principal paper for the conference was prepared by David Greenlaw, James Hamilton, Peter Hooper, and Frederick Mishkin (all seasoned Federal Reserve and monetary economists) and was titled “Crunch Time: Fiscal Crises and the Role of Monetary Policy.” The Board of Governors did not endorse the paper’s findings, and the board officially responded through remarks by Jerome Powell, a governor of the Federal Reserve. Powell did not disagree that the fiscal dominance could occur but instead argued that it is not likely to happen in the near term or, given recent 2011 spending controls, even in the medium term.

Several months later, I asked Janet Yellen at a briefing for Senate and House staff members whether she was concerned about fiscal dominance. She replied that this issue was one of many things that kept her up at night, but she was confident that Congress would find a way to prevent that day from coming. (The meeting with Hill staff members occurred in May 2013, during which time I was serving as the chief economist of the Senate’s Committee on the Budget.)

Powell and Yellen basically said the same thing: the Fed’s interest rate and monetary policy decisions are now in the hands of Congress. If the Treasury has no other option than to fund an unsustainable fiscal future, then the options for monetary and economic policy are limited, to say the least. As Greenlaw and his colleagues noted, however, one option still available in an era of fiscal dominance is inflation, which would lower the value of existing debt if pursued with sufficient vigor. Yet that option raises the prospect of dollar devaluation, which would only increase the pace of deficit financing by augmenting inflationary pressures and possibly inducing investors to require an inflationary discount when buying Treasury debt.

In a world of little and slowly growing federal debt, rising rates would simply be a welcome development. Such rising rates would help to correct the economic and fiscal distortions produced by especially low rates and would lead to better pricing of assets and investment opportunities.

However, we live far from that world. Instead, the United States is in a moment of economic history where doing the right thing could produce harmful results without the correct predicate in place. Indisputably, that predicate is dramatic efforts by the Congress to fix the current drivers of our rising and historically high deficits and to restore the federal government’s finances to fiscal stability. Nothing less will avert the increasingly sleepless nights of the Federal Reserve Chair.

Series Information

This essay is the twelfth in a twelve-essay colloquium on the effect of low interest rates on the economy. To read other essays in the series, click here.

{kind=link}