- | Housing Housing

- | State Testimonies State Testimonies

- |

Considerations for Improved Pension Solvency and Retirement Options in Maryland

Testimony before the Maryland House Appropriations Committee

Chairwoman McIntosh, Ranking Member Beitzel, and members of the committee:

Thank you for allowing me to testify today on the subject of defined contribution plans (DC) and their role in state retirement systems. As part of my research in the State and Local Policy Project at the Mercatus Center at George Mason University, I study the finances and fiscal impact of public sector pensions. My research includes several analyses of state and local pension systems, including Alabama, Delaware, Illinois, Rhode Island, and Scranton, Pennsylvania. In addition, I have frequently testified on state pension systems and recently served on the Virginia Commission on Employee Retirement Security and Pension Reform.

There are two major facets to consider with respect to DC plans: their effectiveness as a retirement vehicle and their fiscal impact. Offering an optional DC plan to Maryland’s public employees will be beneficial for Maryland’s workforce and for individual retirees. It not only gives workers a choice in how they plan for their retirements, but it is also an option that permits for personal mobility and flexibility. The success of the DC option as a suitable retirement vehicle depends on its design. As a fiscal remedy the DC option must be put into the context of the funding shortfalls facing the current defined benefit (DB) system. There is one clear benefit to the DC option. As new workers opt for the DC plan, the fiscal risk to the state is reduced. However, merely adopting this option alone will not improve the funding status of the open DB plan, nor will it necessarily reduce costs. The design elements of the DC plan—including sufficient contributions, good investment options, and sensible options for withdrawals—are all essential to ensuring its success as a retirement vehicle for employees.

Elements of Well-Designed DC Plans

Currently three states (Michigan, Alaska, and Oklahoma) offer mandatory DC plans to their workers. A further six states (Florida, Montana, North Dakota, South Carolina, Ohio, and Colorado) offer workers the option to enroll in a traditional DB plan or a DC plan. A further 10 states offer a hybrid pension plan with elements of both a DB and a DC plan. Virginia is now considering legislation to extend the DC option currently offered to universities to Virginia’s teachers and public employees. Forty-five states, including Maryland, offer either optional or mandatory DC plans to state university employees. Given the growing importance of this retirement option to public-sector workers, it is important to consider the DC plan’s design features and fiscal impact.

The design of a DC plan determines its success as a reliable source of retirement income.

The elements of a DC plan design include the following:

- Sufficient contributions from employees and employers. Data from the Pew Center on the States indicates typical optional DC plans have between 7 and 9 percent employer contributions and 13 to 16 percent combined contributions.

- Well-crafted, approved investment options that do not expose investors to excessive risk, such as index and life-cycle funds.

- The option of annuitization of savings upon retirement and the option for systematic withdrawals.

The Case in Maryland

University employees in Maryland receive an employer contribution of 7.5 percent of annual base salary, with no employee contribution. The employer may select between Fidelity Investments and TIAA-CREF, and then designate the investment allocation. The DC plan under consideration improves the savings rate for Maryland employees. Under the State Retirement Choice for the 21st Century Workforce Act, employers and employees each contribute 5 percent of annual salary for a total contribution of 10 percent.

Employee Gains from an Optional DC Plan

Offering an optional DC plan for Maryland workers expands retirement options and produces several additional benefits for employees. It produces immediate vesting of retirement income for employee contributions and a three-year vesting period for employer contributions. This is particularly beneficial for short- and medium-term workers who do not accrue long tenure at one job. Thus, it allows for personal mobility and career growth without negatively affecting retirement savings. This feature may help to attract and retain younger workers and also those who enter government service at mid-career. Removing the job lock presented by the nature of the DB plan is likely to improve productivity for certain job types. In addition, some workers may simply prefer the DC as their retirement option because it permits investment flexibility.

Fiscal Consequences of an Optional DC Plan

The fiscal impact of offering an optional DC plan, and the extent to which a new optional DC plan lowers costs to the state, is complex and should be considered in the context of the fiscal health of Maryland’s DB pension plan.

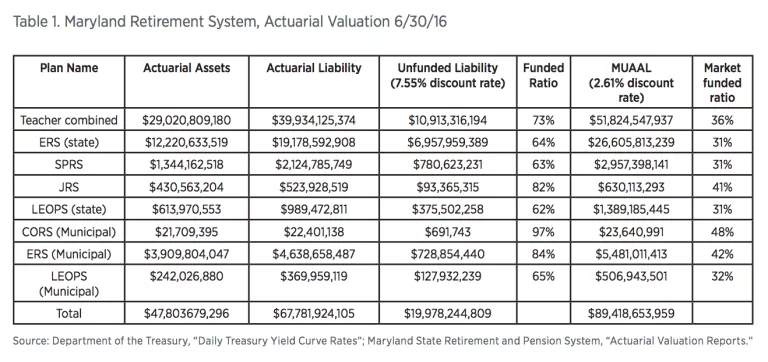

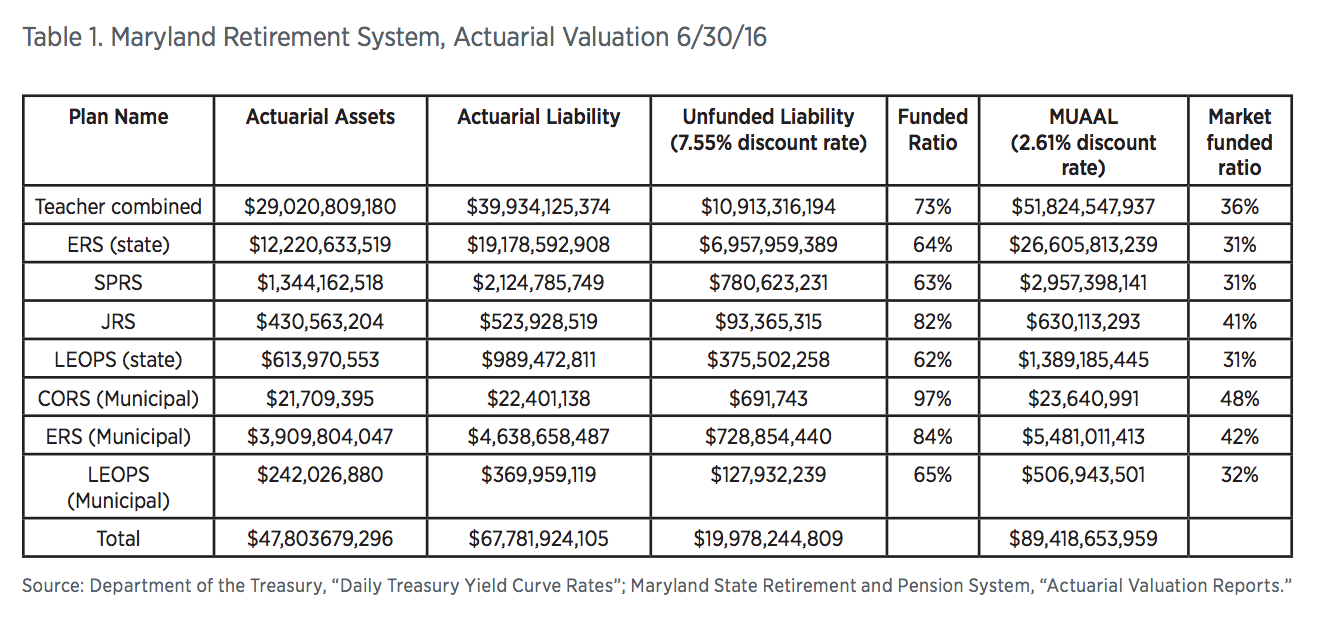

According to the actuarial reports, Maryland’s Retirement System faces an unfunded liability of $19.9 billion in FY 2016. These estimates are based on the state earning an assumed 7.55 percent on plan assets each year. When valuing these liabilities on a guaranteed-to-be-paid basis, based on the return on Treasury bonds, the unfunded liability is more than four times larger, or $89.4 billion. Recent investment returns have been poor for the retirement system, putting more pressure on the state to make up contributions.

Maryland is likely to continue facing fiscal pressure owing to past unfunded liabilities. The optional DC plan will shift risk away from the state. After the state makes the employer contribution to the DC plan, it does not have any further obligation. However, opening a DC plan for new employees does not reduce costs to the current DB plan, at least in the near term. An optional DC plan will lower future accruals to the DB plan. The ultimate fiscal impact will depend on the number of new employees who elect the DC option.

It is also important to note that while employees bear the investment risk of the DC plan, investment risk is also present to those participating in the DB plan. It is often wrongly stated that the DB plan poses no risk to retirees because the state is able to absorb investment risk by amassing sufficient assets or because of the long-lived nature of government.

Arguments that suggest DB plans are better able to absorb investment risk are based on an inaccurate understanding of risk and how the DB plan operates. Poor investment performance in a DB plan, such as negative returns that reduce the assets available, adversely affect the funding status of the DB plan. The timing of negative returns could affect the ability of the plan to meet expected payouts without requiring greater employee and employer contributions or public funds.

The only difference between the DC plan and DB plan in this regard is that in the DB plan the state has the option to shift investment risk to the taxpayer—and make up for pension funding gaps—through higher taxes, or it can shift risk to the employee through reduced benefits.

The impetus for the State Retirement Choice for the 21st Century Workforce Act, therefore, is twofold: to increase choice for workers in their retirement options and to help preserve the current DB system. Offering workers a choice is important to attracting a high-quality workforce. The DC plan is a good vehicle for many workers—especially those with a high degree of personal or career mobility. The DC plan, when structured well, can provide a decent level of savings in retirement. The proposed match is on par with what many states offer to their workers. By offering a well-considered list of investment options, the state may ensure employees do not take on excessive investment risk.

The second question of whether offering a DC option will enhance Maryland’s fiscal position is more nuanced. By opening an optional DC, and depending on the take-up rate, future workers may elect to move to a plan in which investment risk is shifted away from the state. This is likely to be of some help to the state. At the same time, early vesting may cost the state money due to adverse selection. Employees who intend to cash out early have a higher likelihood of selecting the DC plan. With the current DB plan remaining open, the state must also recognize that the DB system, which is facing a funding gap, will continue to accrue obligations. Growing unfunded liabilities will necessitate even greater structural pension reform in the future.

Introducing the DC plan—while beneficial for the workforce and employees—will not, by itself, necessarily improve the funding status of the open plan or reduce costs to the government. An optional DC plan will allow new employees greater choice in structuring their retirement savings. It likely to be an attractive option for many workers, helping to ensure a high-quality workforce for Maryland. However, offering an optional DC plan for new employees must be part of a multifaceted approach to confront the mounting obligations in Maryland’s DB pension plans, if the problem is to be successfully resolved.

Thank you for the opportunity to comment on this important issue. I am happy to answer any questions.

{kind=link}