- | Expert Commentary Expert Commentary

- |

The American Rescue Plan’s Disastrous Pension Bailout

The federal bailout of multiemployer pension plans will encourage more of the irresponsible behavior that got pensions into trouble in the first place

On March 12, President Biden signed the American Rescue Plan (ARP), a $1.9 trillion spending package moved through Congress on a party-line vote. The legislation is controversial for several reasons, one being that many of its provisions are wholly unrelated to the COVID pandemic from which it’s supposed to provide relief, another being that its enormous deficit-spending price tag dwarfs economists’ consensus view of how much support the economy needs. It is unsurprising, if unfortunate, that the new majority would use Congress’ special budget reconciliation rules to enact a host of provisions aimed at pleasing various political constituencies. But even considering the political context of the new law, the package’s pension bailout stands out among its provisions for the long-term damage it is likely to cause.

To refer to the ARP’s pension provisions as merely irresponsible is to understate matters. Even if not corrupt in intent, they cannot help but ultimately be corrupting. They will provide an estimated $86 billion of taxpayer money to bail out pension promises made jointly by corporate management and union representatives, actors who spent years understating their pension obligations so as to avoid meeting their associated funding requirements. The message the ARP relays to pension sponsors everywhere—from private corporations to states and localities—is clear: Don’t bother funding your pension promises. Make the right political connections and they’ll have taxpayers bail you out. The costs of this legislation will be immense, both in dollars and in its effects on future behavior.

Background: The Multiemployer Pension Solvency Crisis

Understanding the implications of the bailout requires some understanding of multiemployer pensions and their impending solvency crisis. Multiemployer pensions are private sector pensions that, as the name implies, have multiple employer sponsors, typically covering workers in a common industry or geographic area. They are collectively bargained plans, so it’s common to think of them as union plans. A basic goal of this type of plan is to give workers additional protection if they change jobs to work for another employer in the same industry.

For example, if the worker’s new employer is a sponsor of the same plan as his or her previous employer, that worker can continue to accrue pension benefits without interruption. The sharing of funding obligations among employers within a plan is also intended to provide greater protection against risk. For example, if one employer goes out of business, the surviving employers inherit responsibility for funding the pensions of the exiting employer’s workers.

Pension law is incredibly complex, and the preceding description glosses over several key elements of multiemployer plans, such as the withdrawal liability rules that determine the payments that exiting employer sponsors must make on their way out the door. However, the essential things to know are as follows:

- Multiemployer plans are collectively bargained plans, typically covering union workers in a common industry;

- Collective bargaining determines the contributions that participating employers must make (federal law may require additional contributions if plans become underfunded);

- The plan is managed by a board of trustees, split equally between representatives of management and labor;

- This board of trustees bears responsibility for determining the benefits the plan can pay, based on the employers’ contributions, and for ensuring that the plan is fully funded.

Multiemployer plans are insured by a government-chartered corporation, the Pension Benefit Guaranty Corp. (PBGC). The PBGC manages a couple of pension insurance programs, one of which is its multiemployer program. The PBGC provides financial assistance if a multiemployer plan becomes unable to pay PBGC-guaranteed benefits. Technically, the financial assistance takes the form of “loans,” but in practice the PBGC basically subsidizes insolvent plans because the loans are hardly ever paid back.

The PBGC only insures a base amount of workers’ multiemployer pension benefits (for example, up to $17,160 annually for 40 years of work), so if a plan ever goes belly up, workers stand to lose substantial retirement income despite their pensions being nominally insured. Data published by the PBGC indicate that in a plan insolvency situation, about half of the workers will lose 15% or more of their promised benefits, and 1 in 5 will lose the majority of their pension benefits.

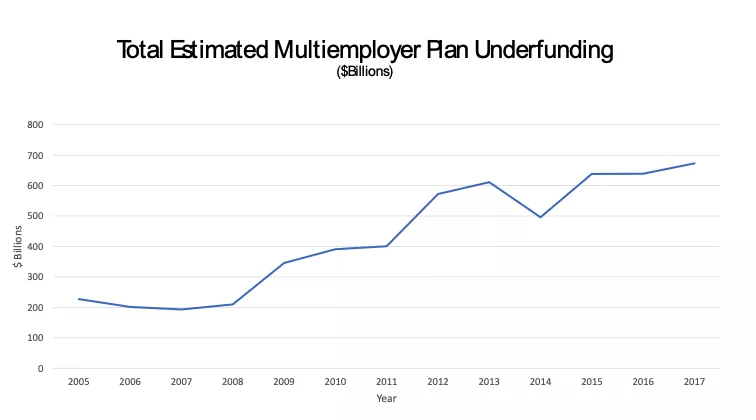

So, what is the problem that triggered this federal intervention in multiemployer pensions? It is that multiemployer plan trustees have badly underfunded their pension promises. The most recent estimate for the amount of underfunding in multiemployer pensions is $673 billion.

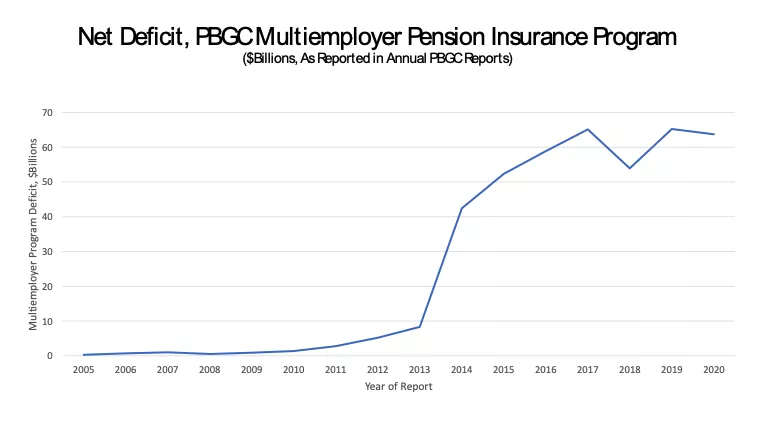

Not only are multiemployer pensions badly underfunded, but the projected insolvency of some large multiemployer plans would swamp the PBGC’s insurance program. The last PBGC annual report projected that the multiemployer pension insurance program faced a deficit of $63.7 billion, and that it would be completely insolvent by 2026. If the PBGC’s insurance funds were to become depleted, it would be unable to protect even the base level of pension benefits that are theoretically guaranteed. Some experts have estimated that certain workers in multiemployer plans could lose 90% of their pension benefits upon PBGC insolvency.

How the Multiemployer Crisis Happened

Again, the multiemployer pension solvency problem is incredibly complex and cannot be fully detailed here. For additional background, see my Mercatus working paper on the problem. However, two primary drivers of the crisis warrant especial mention.

The first and biggest problem is that multiemployer plan trustees have long exploited gaps in federal law that permit them to misstate their liabilities, assets and funding needs. A number of methods have been employed to do this, but one of the most egregious is the use of inflated discount rates to mismeasure the present value of plans’ liabilities. This behavior is not a secret; it has long been widely known that multiemployer plan trustees were doing this, using techniques that federal law forbade single-employer plans to use. There is a consensus among economists that these multiemployer plan trustees’ discounting techniques are unambiguously wrong and have resulted in liability understatement and enormous pension underfunding. Lawmakers, however, have failed to crack down on these practices in multiemployer plans, with disastrous results.

A second major problem involves another specific weakness in the federal statutory system for multiemployer plans. That statutory system is rife with loopholes and gaps, including inadequate premium assessments and lax funding rules. But one particular problem stands out. In theory, whenever employers withdraw from sponsoring a multiemployer pension plan, whether because they are going out of business or for any other reason, they are supposed to make a withdrawal payment that funds their workers’ share of the plan’s unfunded vested benefits. However, various loopholes often cause such withdrawal payments to be inadequate to fund these obligations. This leaves the remaining employer sponsors in the plan holding the bag for funding benefits owed to those workers. Such workers are often referred to as “orphan workers,” and their benefit obligations inherited by other plan sponsors are referred to as “orphan liabilities.” Academic research shows that plans with higher percentages of orphan workers are more likely to be badly underfunded.

The multiemployer pension funding problem and the pension insurance crisis can’t be fixed unless and until the problems described above are fixed. For obvious reasons, the problems can’t be repaired as long as plan sponsors continue the practice of understating their plans’ liabilities; a liability won’t be funded if it’s not even recognized. It’s also highly unlikely that multiemployer pension plan funding can ever be adequate as long as exiting employer sponsors dump unfunded benefit obligations onto other sponsors in the same plan. Lasting pension reform therefore requires fixing both the valuation problem and the orphan worker problem.

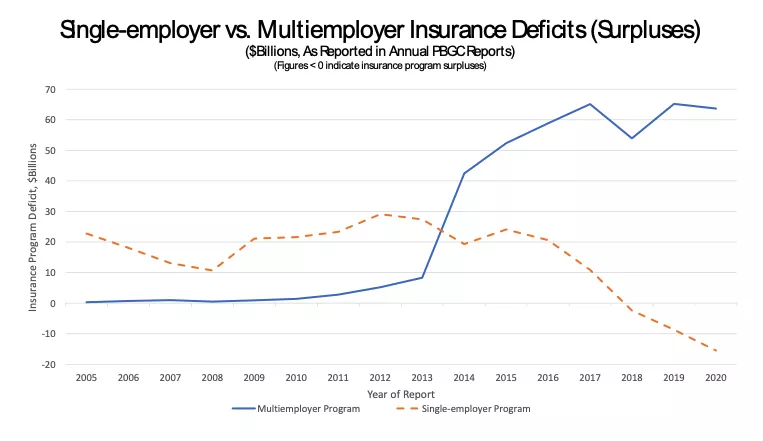

When crafting policy, it’s also important to understand what did not cause the multiemployer pension funding crisis. Bailout advocates sometimes assert, wrongly, that these plans got into trouble through no fault of their own, simply due to market conditions beyond their control or because of unfavorable demographic trends in these industries. This is readily seen as incorrect by comparing the financial situations of the single-employer and the multiemployer pension insurance systems.

Coming into this year, the single-employer pension insurance system was looking at a healthy surplus, while the multiemployer system was facing insolvency. Both systems operate in exactly the same financial market conditions, and the demographic forces facing the single-employer pension system are every bit as difficult as they are in the multiemployer system. Despite this, the PBGC’s single-employer insurance program showed a net positive position of $15.5 billion in the latest annual report.

The different situations in the two insurance programs are a direct result of different approaches in federal policy. Federal lawmakers, in the 2006 Pension Protection Act (PPA) championed and signed by President George W. Bush, cleaned up the single-employer system’s funding rules. No similar reforms were enacted for the multiemployer pension system, where bad practices were allowed to continue. Had federal lawmakers reformed the multiemployer pension system’s funding rules as they did with single-employer plans, there would have been no expensive taxpayer-financed bailout this year.

The ARP bailout will not prevent problems in the multiemployer pension system from recurring and mounting because it permits multiemployer pensions to continue accruing additional pension liabilities without accurately measuring them or adequately funding them.

Why the ARP’s Pension Provisions Are So Damaging

The ARP contains a number of costly and irresponsible provisions affecting multiemployer pensions. For starters, the legislation would provide funds, estimated at $86 billion, to be used for grants to underfunded multiemployer pension plans—in other words, a taxpayer-funded pension bailout. This is a dramatic departure from the foundational principle of private sector pensions, which is that they are benefits provided by employers to their workers, with insurance that is funded by sponsor-paid premiums.

Essentially, the ARP would require taxpayers, most of whom are ineligible to receive such pensions themselves, to shoulder a substantial cost of the benefits certain corporations and unions promise their workers. The legislation has been criticized as being a “union pension” bailout, which it certainly is. However, it is equally a bailout of corporations and, implicitly, of their shareholders. The ARP pension bailout is at bottom a triumph of the politically connected—of corporations and unions—working in tandem to transfer the costs of their own promises to the U.S. taxpayer.

The ARP’s provisions would penalize responsible management of pension plans and incent further underfunding. Eligibility for government assistance is predicated on how underfunded plans are, which creates incentives for sponsors to more severely underfund their plans. Other provisions of the ARP reverse previous legislation that had been enacted to contain unfunded benefit increases—with the ARP instead actually requiring that bailed-out plans reinstate benefits that were previously suspended because they were unfunded. This, too, is a dramatic departure from longstanding pension protections, namely the principle that underfunded plans should not be allowed to promise additional benefits unless they pay for them up front. The ARP, by contrast, requires that sponsors offer benefits that they cannot fund.

In other words, not only does the ARP provide for a taxpayer bailout of corporate and union pension promises, it exacerbates the cost of that bailout by increasing benefit obligations and undercutting funding incentives. The bailout itself sets a damaging precedent that will spur future underfunding, essentially communicating to irresponsible actors that they will be rewarded and telling responsible pension sponsors that they are suckers. But the ARP goes even further, packaging the bailout with additional inducements for more underfunding and larger benefit promises.

Perhaps the most bizarre aspect of the ARP is that it contains no provisions to reform the irresponsible practices that led to calls for a bailout in the first place. Not only will plan sponsors who papered over their funding responsibilities be bailed out, but they will be allowed to continue employing inflated discount rates that understate their pension liabilities and future funding needs. This virtually guarantees that additional bailouts will be required in the future.

While the ARP’s worst provisions pertain to multiemployer pensions, it will also do damage on the single-employer pension front. It’s fair to say that to date, the single-employer pension funding regime established by the 2006 PPA has worked well, even as the multiemployer system has careened toward disaster. Yet the ARP dismantles the prudent funding system established for single-employer pensions under the PPA, setting the single-employer pension system as well on a course where it may ultimately develop problems similar to those in multiemployer pensions.

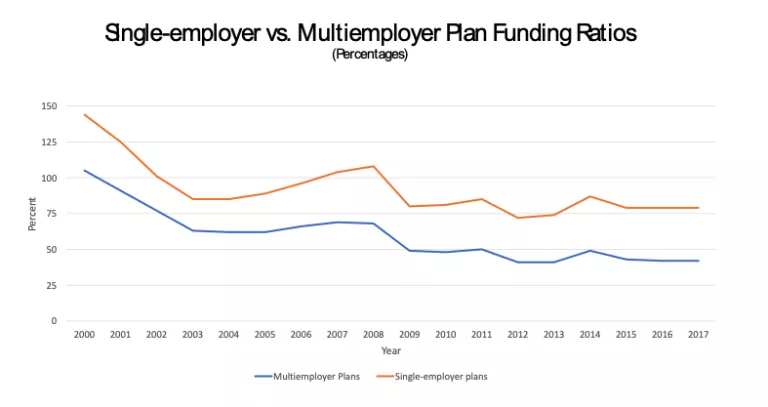

For example, the ARP would wipe out recognition of single-employer pensions’ funding shortfalls that materialized prior to this year. This ignores the reality that single-employer pensions, though better funded than multiemployer plans, are and have been underfunded: Single-employer pensions are but 79% funded, on average. Yet the ARP would allow single-employer pensions to start from scratch in addressing their funding shortfalls, discarding the PPA’s seven-year schedule that had worked so successfully in favor of a longer, 15-year schedule that would extend pension sponsors much more time to dig themselves into trouble from which they cannot escape on their own.

Worse yet, the ARP will also allow single-employer plans to use inflated discount rates when calculating their liabilities. This means that the single-employer plans’ liabilities will be underreported and that underfunding will worsen in them as well. The single-employer rules still wouldn’t be quite as bad as they are in multiemployer plans, where trustees are basically allowed to invent a discount rate untethered to economic realities. Nevertheless, the change will still result in mismeasurement of single-employer plans’ liabilities and more underfunding.

While one can certainly make a reasonable case for providing single-employer plan sponsors with funding relief, given current economic conditions and the currently strong position of PBGC’s single-employer insurance system, this should never be done by doctoring the interest rates that plan sponsors employ to measure their liabilities. No good can come from deliberately misreporting pension liabilities, no matter what one’s preferred policy is with respect to funding requirements.

Unpersuasive Defenses of the Bailout

A number of defenses have been offered for the pension provisions in the ARP. They are all unpersuasive.

One defense is that these workers are innocent victims, and they both need and deserve to receive their pension benefits. That is certainly true, but it is not at issue here. Workers do deserve their promised pension benefits, which is why pension plan sponsors and trustees should be required to fund them. It does not mean that corporations and unions should be allowed to shift the bill for these pension benefits to taxpayers. To the contrary, the federal government’s providing a bailout will only encourage corporations and unions to make more empty promises to their workers, banking on the likelihood of future government bailouts.

A second defense is that the situation in multiemployer pensions has become so bad that it’s too late to keep the multiemployer pension insurance system solvent without an infusion of taxpayer dollars. This is a plausible argument, but it does not argue for the approach taken in the ARP. If the bailout was indeed inevitable, it makes it all the more important to reform the system so that the same situation does not recur. Lawmakers should require that pension assets and liabilities be accurately measured going forward and clamp down on sponsors making additional unfunded benefit promises, before offering any taxpayer-financed assistance. What has happened instead is that the bailout has been coupled with incentives that virtually guarantee that taxpayers will be required to pay more in the future—perhaps hundreds of billions of dollars more.

A third defense has been that there should be no objection to bailing out worker pensions because, after all, Washington bailed out rich fat cats on Wall Street in 2008. This reply only highlights the faults and failures of the ARP relative to 2008’s far more responsibly designed Troubled Asset Relief Program (TARP). In 2008, federal lawmakers made a point of attaching tight strings to any Wall Street bailout, limiting executive compensation, clamping down on bonus payments and making sure that taxpayers recouped their investment first. Taxpayers actually came out ahead on the 2008 bailout, which they will not do with respect to the pension bailout.

Today’s Congress surely should have embraced a TARP-style approach to any multiemployer pension bailouts this year: It’s indefensible that multiemployer plans are pocketing $86 billion in taxpayer-funded assistance without any restrictions on compensation within the recipient corporations or unions whose bad practices caused the problem, without any requirements that taxpayers be repaid first before the corporations and unions involved are allowed to benefit, and without any reforms of pension plan mismanagement. If TARP is a precedent, let it be a true precedent. No corporate or union bailouts should ever be provided with taxpayer money without enormous strings attached.

The ARP’s pension bailout is a policy disaster and will lead to future disasters. Americans will be paying for it for years to come. Lawmakers should be urged to revisit this issue and to correct these dire mistakes at the earliest opportunity.