- | Monetary Policy Monetary Policy

- | Expert Commentary Expert Commentary

- |

A Better Way to Gauge Economic Performance

New research on NGDP Gap measurement can inform better macroeconomic policy

The key objective for macroeconomic policy in advanced economies is to avoid or mitigate boom-and-bust cycles while maintaining price stability. Many policymakers approach this task by looking to the output gap, meaning the difference between where the economy is and where it could be at its full potential. Getting this right has never been easy, but there are ways to make it easier.

When policymakers see the economy running below its potential — a negative output gap — then economic activity is too “cold,” and monetary and fiscal policy need to be loosened to stimulate economic growth. Conversely, if the economy is running above its potential — a positive output gap — then economic activity is too “hot,” and macroeconomic policy needs to be tightened to keep inflation and financial instability concerns at bay.

The use of the output gap, however, comes with significant challenges. It can only be estimated with uncertainty and, as a result, can give misleading signals about the economy. Here’s a new way to tackle these challenges.

As background, the output gap is calculated by taking the percent difference between actual real gross domestic product (GDP) and potential real GDP. Two big measurement problems emerge in this exercise:

- First, potential real GDP is not directly observable and must be estimated. The true potential of an economy is never fully known, so this exercise is as much art as science.

- Second, the value of real GDP is often revised over time. Consequently, the final output gap value can be very different from the initial estimate used by policymakers. Research by Athanasios Orphanides finds that this confusion may have contributed to the high inflation of the 1970s. More recent research suggests it is still a concern today.

To address these challenges, the Mercatus Center launched the Nominal Gross Domestic Product (NGDP) Gap measure in 2020 as a better means of assessing the health of the economy. The NGDP Gap instead measures the percent difference between the actual dollar size of the economy and what it was expected to be by the public for a given period. It is calculated using the actual level of NGDP, the total dollars of spending in the economy, and a neutral-level estimate of NGDP.

This latter, neutral-level measure is constructed by taking an average of past, overlapping consensus forecasts of NGDP for a given period. These consensus forecasts can be viewed as reflecting the public’s expectation of NGDP. The expected dollar size of the economy revealed in this estimate is important because people make decisions based on their expected dollar incomes. For example, households make decisions to take out mortgages and car loans, and firms commit to large multiyear contracts, based on how much money they expect to take in.

Differences between actual and expected dollar incomes can be disruptive because households and firms are not always able to adjust plans quickly. The NGDP Gap is a way to assess this difference and can be used by policymakers to adjust the stance of macroeconomic policy. Unlike the output gap, it relies completely on observable variables - which both actual NGDP and publicly avialable forecasts of NGDP are - and tends to have fewer data revision issues. Two versions of the NGDP Gap can be seen in the figure below.

In Septemeber of 2021, the Mercatus Center published a working paper by economists Andrew Martinez and Alexander Schibuola on “The Expectations Gap,” which builds upon and expands the NGDP Gap concept in important ways.

First, Martinez and Schibuola show that the NGDP Gap is robust to the use of different consensus forecasts. The original NGDP gap relied on forecasts from the Survey of Professional Forecasters provided by the Philadelphia Fed, shown in the blue line above. The results are almost identical to those found using another professional forecast from the Blue Chip Economic Indicators, shown in red.

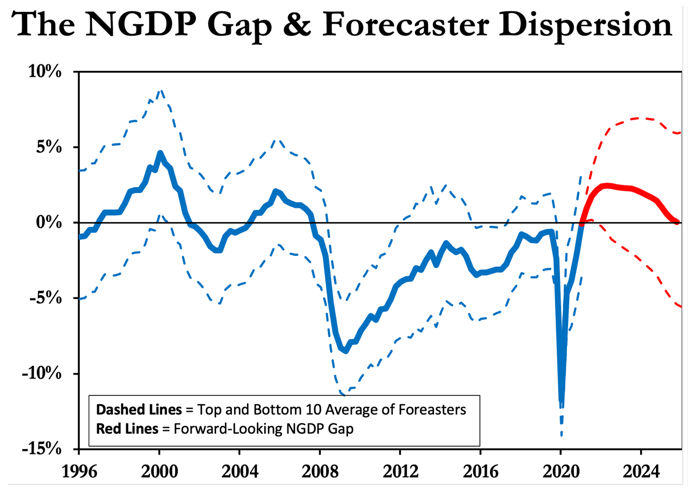

Second, Martinez and Schibuola look at the dispersion of the underlying individual forecasts that make up the NGDP Gap. This feature, seen in the figure below, allows us to see the NGDP gap for all forecasters, not just the median. This information is useful because it allows us to see whether non-zero values of the NGDP Gap are truly meaningful and are therefore suggestive of big misses in nominal income expectations. For example, this data reveals that the 2001 recession did not experience a meaningful NGDP Gap while the “invisible recession” of 2015-2016 actually saw a significant NGDP Gap emerge.

Third, Martinez and Schibuola find that in a “horse race” or comparison between the NGDP Gap and various measures of the output gap, the former measure provides information not found in the latter. Finally, the authors build a forward-looking NGDP Gap and find that it outperforms simple forecasting benchmarks and acts as a useful leading indicator of business cycle turning points.

It would behoove policymakers to look to the NGDP Gap as a substitute for the output gap. As Martinez and Schibuola note, doing so would shift “the emphasis from ‘navigating by the stars’ to navigating by what [economic] agents expect.” Here’s hoping they do.

Photo by Pixabay