Word from the Bureau of Labor Statistics that October’s unfilled job openings jumped to around 11 million — the second highest level on record and up from some 6.8 million in October 2020 — provided powerful evidence that employment markets have a long way to go before things begin to feel normal again. But for those inclined to look on the bright side, we can find some silver lining.

Recalling that in November there were 6.9 million counted as unemployed and at least theoretically available to help fill the 11 million openings, we now have a situation where newly entering workers can readily find work, and where those employed can easily switch jobs should they have any reason for doing so.

This is why my conversations about the economic situation with local South Carolina employers have a common theme. For some, the business outlook is the brightest in recent memory, and in some cases, capacity is sold out for the year ahead. However, the availability of labor, lumber, steel buildings, and even doorknobs for completing large apartment projects is as bad as it has been in recent memory.

My discussions with construction employers bring back personal memories of post-World War II, when new 1946 automobiles were arriving without bumpers or taillights because of yet-to-be healed supply chain problems. But no one then referred to “supply chains;” they just said, “We can’t get the parts!” One local executive told me recently that his firm is completing large construction projects with substitute floor tile, doors, and hardware that will have to be replaced later when the right stuff becomes available again. Little wonder that construction costs are rising.

However, while COVID-19 is still generating economic pain and anxiety for many, related gales of change are making the economy more productive and may even generate what we could look back on as a golden age for entrepreneurship. Let me explain.

In their search for ways to satisfy surging consumer demand, many nimble employers are reassessing worker skills and what some term “adjacent capabilities,” which is another way of saying underutilized or yet-to-be recognized skills and abilities. The result: more effective deployment of workers … and better pay.

Expanding businesses often look for ways to improve profits by moving specialized production capabilities into new product categories—say, from producing steel sheeting for automobiles into corrugated galvanized steel for industrial buildings. There is now a push to reposition workers and the workplace itself, so that newly emerging crucial needs can be satisfied in-house.

Much of this effort can lead to the discovery of lower costs and even happier employees. In this way, pandemic-induced scarcities and disrupted supply chains may be seen later as the prelude to plenty. We should recognize that the noted adjustments are occurring globally, and big changes are assisted by emerging cloud computing, which makes IT economies of scale available to all who will pay the price. This further enables a “work wherever you wish” type of employee deployment.

With a sort of COVID-generated global industrial revolution occurring, we should not be surprised to know that a veritable explosion of new business starts is occurring in the United States. Indeed, out of necessity, hard times generally cause people to find ways to put bread on the table — sometimes literally when a family decides to turn their kitchen into a bakery and their front living room into a small café. As the old saying puts it, “When the going gets tough, the tough get going.”

For those who like to keep score on such matters, the U.S. Census Bureau has since 2004 provided a monthly count of new business openings by state and for various categories of activity and scope. Just to convey an idea of relative magnitudes, in November 2021 there were 432,000 new business formations in the United States. That, of course, suggests there are at least that many people who would like to work for themselves, part-time if not full-time.

This helps to explain why labor markets are so tight. Anyone thinking about starting a new business must come to grips with the financial realities they will encounter. This suggests that some level of savings is needed to help get a new business on its feet. The influx of COVID stimulus money to individuals and families — much of which has remained in Americans’ bank accounts, perhaps in spite of lawmakers’ intent — could have helped stimulate the new business revolution. Of course, we would expect a lag between putting the money in the bank and starting a business.

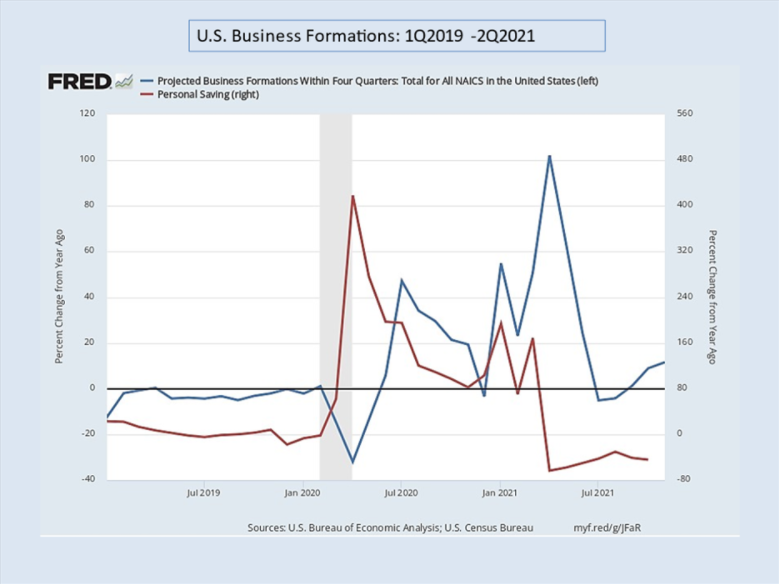

In the nearby chart, I provide data on new U.S. business formations from the first quarter of 2019 though 2021’s second quarter, along with data for personal savings. The data show year-over-year growth rates.

A quick look at the chart tells us that the federal stimulus programs associated with the 2019-2020 pandemic disruption brought three surges in the personal savings rate. About 60 days after the first surge, we see a large increase in business formations. The business formation surge continues as the growth rate of savings rises, falls and becomes negative.

Could we be in the midst of an entrepreneurship golden age? Maybe. Why maybe? Because these are troubled times, and it is a bit too early to tell how many of the new flowers will bloom next spring. Even so, one thing is sure: COVID economic forces are changing the way the world works, and sometimes for the better.

Photo by Andrew Lichtenstein/Corbis via Getty Image