- | Housing Housing

- | Expert Commentary Expert Commentary

- |

Income Tax Benefits to Homeowners Are Regressive

Part Thirteen of Kevin Erdmann's Housing Affordability Series

Two of the most important changes to the tax code made by the Tax Cuts and Jobs Act of 2017 (TCJA) relate to housing: a reduction in the deductibility of state and local taxes and a reduction in the mortgage interest deduction.

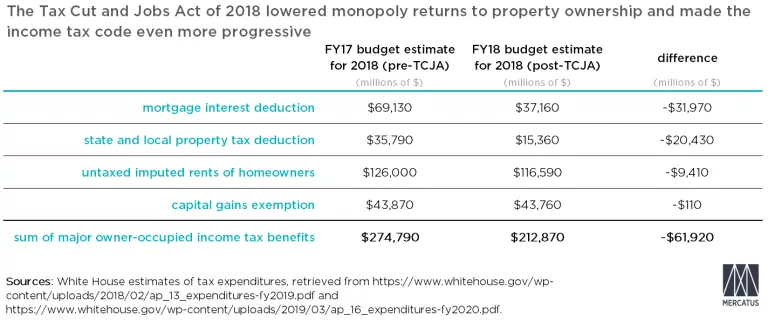

Figure 1 is a summary of the major tax effects on housing, and the estimated scale of those effects before and after TCJA. The table reflects White House estimates of the scale of each of these tax deductions from before and after the passage of the bill. The TCJA was not the only factor at work here, but we can presume that the large changes in the mortgage interest deduction and state and local property tax deduction are largely related to TCJA.

The reduction in tax benefits to homeowners of over $50 billion dollars from the mortgage interest deduction and the state and local tax deduction represents a major shift toward an even more progressive income tax code.

The deductibility of state and local property taxes is an especially interesting facet of these changes. The TCJA limits the deductibility of state and local taxes to $10,000. As I argued in part nine of this series, property taxes can be considered a sort of public claim of ownership on real estate assets. Effectively, a property tax is a mechanism by which real estate owners must pay rent to the state.

Consider, for instance, a 100 percent property tax. If property taxes are basically a form of public partial ownership in properties, then a 100 percent tax would effectively be the total socialization of residential property. Since the private owner of a property would have no right to any of the rental income on the property, property would have little private market value. In that case, property taxes would basically be equal to the rental value of a property, and the state would collect those taxes as rents as if it was the sole owner. To a first approximation, the price of homes would be the annual rental value after expenses. The price of the home would effectively be like a refundable deposit and the property tax payments would be the rent. (For this exercise, please set aside the practical effect this extreme tax would have on supply.)

The point of that extreme hypothetical is to show that property taxes reduce the market value of a home relative to its rental value. In our extreme hypothetical, the homeowner would have a high property tax bill, but since the home would be practically free, they would have no cost of capital. They wouldn’t have to sell other assets to buy the house or pay interest on a mortgage. So, property taxes aren’t really an added expense for homeowners. All things considered, they simply shift those expenses so that, for instance, they are paid to the state instead of a bank.

Or, think of it in this way. It is normal for owners of capital to deduct expenses before they pay tax on capital income, but since homeowners don’t pay tax on the rental value of their homes, there is no need for this deduction. In the hypothetical example above, the homeowner is paying rent to the state, just as any tenant pays rent to a landlord. Tenants don’t get to deduct their rental payments from their taxable income. Since property taxes are basically a rental payment to the state, a neutral tax code would not allow those taxes to be deducted either.

Landlords do get to deduct these various costs from their gross rental income, but that is because landlords pay taxes on their rental income. Homeowners don’t pay taxes on the rental value of the homes they live in. If they did, these deductions would be justified. But, they do not. Since the subsidy only applies to homeowners, it is regressive in practice: a tax subsidy mostly for higher income households.

There are two facets to this tax change. In terms of carrots and sticks to local jurisdictions, removing this deduction will incentivize them to lower property taxes. If relatively higher property taxes might help to stabilize housing markets and collect public capital to encourage local infrastructure development and housing expansion, then maybe a federal tax subsidy to encourage those taxes isn’t all bad.

On the other hand, since local taxes above $10,000 will largely be limited to high-tier properties in expensive cities, this is a way for the federal government to increase the ability of the state at all levels to claim monopoly profits from the urban housing cartel. The effect of this tax change will be to reduce the value of very expensive homes, because governments will be claiming more of the excess rental value for themselves. And frequently, the value of very expensive homes comes from monopoly power expressed through local zoning laws and other obstructions to new housing.

A similar argument can be made regarding the mortgage interest deduction. The deduction encourages debt-funded real estate investments, which can be destabilizing. Also, in absolute dollars, it tends to be mostly claimed by households with very high incomes purchasing very expensive homes.

Eliminating these deductions can increase the progressivity of the income tax code and also claim the profits of monopoly real estate ownership for the state purse. In all, estimated benefits to homeowners have been reduced by more than $60 billion. Much of that can be attributed to the TCJA. The TCJA can be supported on these grounds.

Photo credit: Chip Somodevilla/Getty Images