- | Academic & Student Programs Academic & Student Programs

- | Labor Markets Labor Markets

- | Expert Commentary Expert Commentary

- |

The Real Unemployment Rate Is Probably Higher Than Anyone Realizes

But the sky isn’t falling (yet)

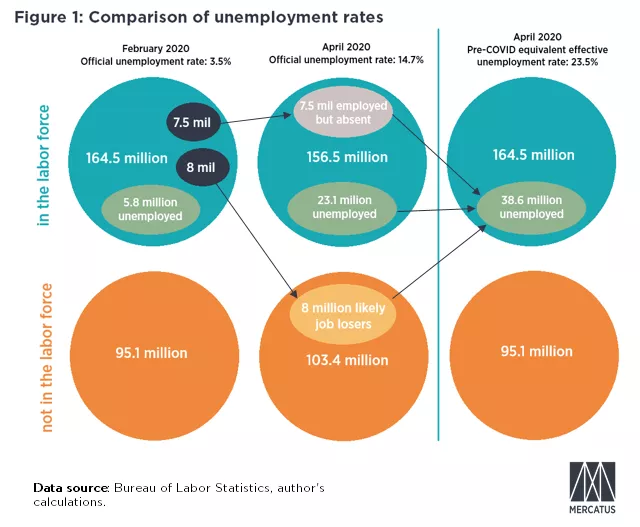

The official unemployment rate announced on May 8, 14.7 percent, was the highest level since the Great Depression. The truth, however, may be even worse: the Bureau of Labor Statistics (BLS) missed counting 15.5 million people who probably should be regarded as unemployed. This would mean that, in effect, the pre-coronavirus comparable unemployment rate might actually be around 23.5 percent.

And yet, despite the deeper-than-expected economic hole we find ourselves in, there’s reason to be hopeful. It’s not far-fetched to believe that the recovery from this recession will be swifter than expected. Most of those who are unemployed are temporarily furloughed rather than permanently laid off. Combining that with effective policies, public health solutions, and entrepreneurial problem-solving, life might adjust to a new normal faster than we think.

Reassessing estimates of the unemployment rate

In a recent article, I suggested a new labor market metric, the pandemic furlough rate, to help understand the labor market impact of the coronavirus. Developing new metrics is important because the headline unemployment rate doesn’t contain everything that we need to know, and may even lead us astray. A deeper dive into the unemployment data will help illustrate what’s really going on in the labor market.

Perhaps the biggest news from the latest jobs report is that the BLS itself has suggested that the estimated unemployment rate is incorrect. This is because as many as 7.5 million workers who likely should have been counted as “unemployed-on temporary layoff” were instead classified by BLS surveyors as “absent from work.” If these workers were instead counted as unemployed, it would raise the headline unemployment rate from 14.7 percent to about 19.5 percent.

In addition, to ensure a proper comparison between the pre-coronavirus economy and the current economy, most employment statistics should be compared against the same statistic from February. This is because data surveys were taken February 9-15, the week before the coronavirus started affecting the US economy. In contrast, the surveys for the March jobs report were taken during the week of March 8-14, after officials starting closing schools and just before governors began issuing shutdown orders.

In the case of the unemployment rate, there’s a problem with comparing February and April. The size of the labor force substantially decreased (by 8 million workers, nearly 5 percent) between those two months. Because the unemployment rate calculation uses the contemporaneous size of the labor force, the unemployment rates from the two months aren’t comparable. Large monthly changes in labor market metrics are nearly unprecedented, so this generally isn’t a problem.

To make the current unemployment rate comparable with the pre-coronavirus unemployment rate, I use the size of the February labor force rather than that from April. This produces an estimated unemployment rate of 18.6 percent. You could call this the “pre-coronavirus comparable unemployment rate.”

However, there’s another problem with this estimate of unemployment. It’s reasonable to believe that the uncounted 8 million workers should be considered unemployed. After all, 8 million baby boomers didn’t simultaneously decide to retire! It’s likely these people simply didn’t satisfy the specific characteristics needed to be counted. For example, the headline unemployment rate (which the BLS calls U-3) only counts people as unemployed if they are jobless, have actively sought out employment within the past four weeks, and are currently available to take a job.

In fact, most of these 8 million workers didn’t even satisfy a more permissible definition of joblessness, the “marginally attached to the labor force” unemployment rate (U-5). This rate counts people as unemployed if they want a job, have actively sought out employment within the last year, and are currently available to take a job. But the swiftness of COVID-19’s onset and the nature of state and city economic shutdown orders probably means that these 8 million people either haven’t sought employment within the necessary time period or don’t believe they are currently available to start a job.

Adding these 8 million people who were counted as having left the labor force increases the group of those considered “effectively unemployed” to 38.6 million. This produces a pre-coronavirus comparable effective unemployment rate of 23.5 percent. See Figure 1 for a graphical representation of this unemployment rate.

This is even higher than what many economists have argued the current unemployment rate really is, but it agrees with the “north of 20 percent” estimate of the future unemployment rate suggested by White House economic adviser Kevin Hassett and the 25 percent peak unemployment rate projected by Goldman Sachs analysts David Mericle and Ronnie Walker. We seem to have already arrived at those projections; we just didn’t know it because the standard BLS data is not equipped to properly convey our current economic situation.

But we shouldn’t blame the BLS that some unemployed workers fell through the measurement cracks. The agency’s data gathering and processing efforts are rightly regarded as the gold standard for generating worthwhile and comparable statistics. In fact, it’s because of their rigor in data handling and adherence to previously determined methods that their standard unemployment metrics aren’t able to fully capture the current unusual economic situation.

Looking forward, the May jobs report data is being collected this week, meaning that next month we’ll be able to see how much closer the unemployment rate will be to the estimated 25.6 percent peak unemployment rate from the Great Depression. Given that many governors and mayors are already lifting mandatory business closure orders and that the Paycheck Protection Program loan requirements are pushing some businesses to reopen, it’s possible that we’ll avoid hitting that historic peak.

So, what’s the good news?

Considering the dire headlines from this jobs report, as well as the much-higher revised unemployment rate, the news was actually better than expected. Nearly all of the rise in the U3 unemployment rate since February is due to the increase in furloughed workers—those who are on temporary layoff. This should lead us to reevaluate our expectations of the economic future. The current economic downturn will likely prove different than our experiences with previous recessions, where much of the joblessness was the result of economic (not public health) disruptions, leading to permanent layoffs.

Permanent layoffs lead to increased economic costs in the subsequent recovery. These include the time that employers and workers spend searching, sorting, and selecting to reestablish new employment relationships. Repairing this unraveling is part of the reason that improvement in the labor market tends to lag behind the broader economic recovery.

So, despite the depth of this recession, we might expect it to be shorter-lived than we would typically experience (assuming the coronavirus cooperates). Most of the jobs workers have left haven’t “vanished” and the economy isn’t “shattered,” as reported by the Associated Press. Rebuilding the economy will indeed be difficult but should be less problematic than a typical recession where bankruptcies and business failures require the web of economic connections to be substantially reknit.

That said, if policymakers keep all-out economic shutdowns in place, or if businesses and public health authorities aren’t able to develop effective strategies to minimize exposure to infection, then we may see temporary shutdowns become permanent closures and layoffs. The speed of the economic recovery will be directly dependent on maintaining the economic connections that existed before the pandemic.

Additionally, there is reason to be concerned that the 8 million workers who left the labor force between February and April are more likely to have been permanently laid off from their jobs, as opposed to being furloughed like most current separated workers. If the entire BLS-reported decrease in the labor force was due to layoffs, then the total number of workers laid off from February to March, 8.7 million, is nearly equivalent to the 8.8 million decline in employment during the Great Recession. If this is true, it would certainly suggest a more difficult economic recovery is ahead of us.

A swift recovery will require (at a minimum):

- Investing in public health projects that minimize or mitigate a potential resurgence of the coronavirus (such as accurate and rapid testing, contact tracing, vaccines, etc.).

- Developing methods to minimize the spread of the virus while enabling a return to some semblance of normal life.

- Maintaining (as much as practicable) the employment relationships between workers and businesses that existed before coronavirus fears shut down the economy.

- Providing confidence for business owners that the act of reopening won’t expose them to undue liability.

- Reassuring workers that their financial security won’t be compromised if they contract COVID-19 and have to miss work while also facing high healthcare costs.

Most of these requirements have been at least partially met or are in the process of being addressed, suggesting that hope for a swifter-than-normal recovery isn’t unreasonable.

Even though the unemployment rate is likely much higher than reported, the sky hasn’t fallen… yet. But the fact that it could reinforces the need to quickly develop the tools and systems to hold it up. We need to prevent the intentional economic shutdowns from creating circumstances that lead to an uncontrolled plunge. The hole that we have to dig out of might be deeper than that of the Great Recession, but we still have the opportunity to snap back quicker than expected if the public and policymakers avoid partisanship and focus on solutions.

Image: Rene Magritte, "Decalcomania," 1966.