- | Housing Housing

- | Expert Commentary Expert Commentary

- |

Rising Prices, Lower Rents; Rising Rents, Rising Prices

Part Five of Kevin Erdmann's Housing Affordability Series

To understand the importance of supply for housing affordability, and to understand why home prices and rents became so disconnected before the crisis, one must view the US housing market as the combination of two very different markets.

There is the Closed Access market, where political obstructions prevent supply from responding to price. And there is the rest of the country, where price increases can generally trigger new supply. Where supply is blocked, rising demand just keeps pushing prices higher. Where supply can come on line, it presents options for buyers, and keeps prices near the cost of new building.

During the pre-crisis housing boom, focusing on home prices in a national market, Americans concluded that healthy rates of building led to rising housing costs. But, focusing on rents in local markets, it is clear that healthy rates of building led to declining housing costs.

To think about the difference between the flat rental costs of the boom period and rising prices, think in terms of households and units. The Closed Access problem means that instead of building new units where housing is valuable, households move to less expensive places to build new units. So rent is moderated by changing the geographic composition of the population.

Rental costs were relatively stable during the boom because families were moving to less expensive cities and building homes there. Renters were moving away to more affordable cities because they were squeezed by rising rents. Homeowners were moving away to more affordable cities because they were being offered very high prices for their homes.

Or, to put this another way, since the mid-1990s, the Closed Access cities have become increasingly prosperous. The 21st century post-industrial economic transition has made certain urban centers very valuable, which drives demand for living and working there.

These cities were already relatively prosperous, but since the mid-1990s, this trend has strengthened. In 1995, the average income in New York, LA, San Francisco, Boston, and San Diego was about 26 percent higher than in the rest of the US. By 2017, it was 42 percent higher.

Since those metro areas also have very tight controls on homebuilding—tighter than any other major cities in the US—that convergence can’t happen. Instead, demand for living in those metro areas butts up against the limited supply of shelter.

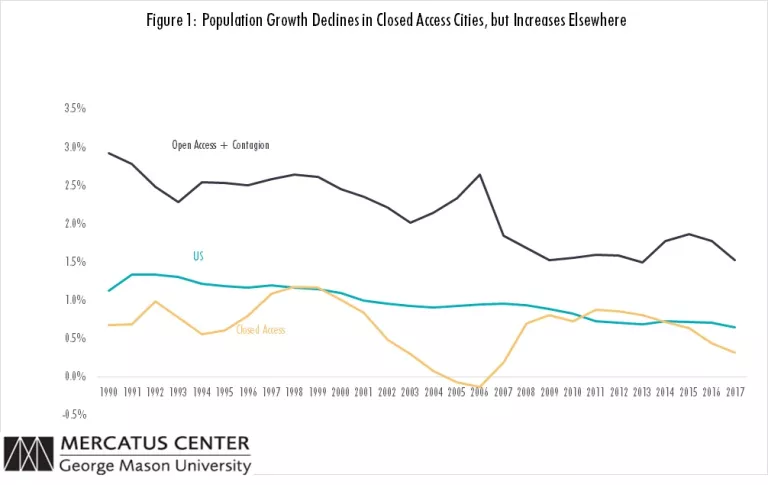

Figure 1 compares population growth in the Closed Access cities to population growth in major metropolitan areas that attract new workers and allow ample homebuilding. Here I have included the Open Access cities of Dallas, Atlanta, and Houston, and also Miami, Phoenix, Riverside, and Tampa, which I refer to as the Contagion cities, because their local home prices briefly spiked as they were over-run by migration out of Closed Access cities in 2004-2005.

After the turn of the century, population growth ground to a halt in the Closed Access cities, mostly because households with lower incomes increasingly were moving away from them. Many of them were moving into places like Phoenix, so there was a brief spike in population growth in the Contagion cities.

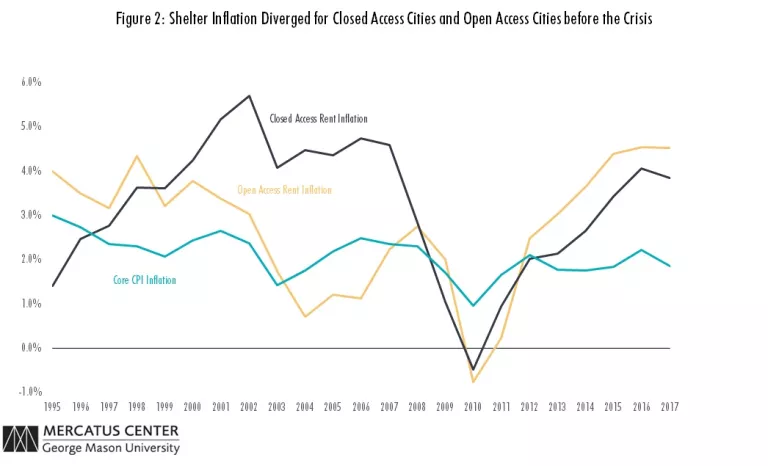

Figure 2 compares shelter inflation in the Closed Access cities with shelter inflation in the Open Access cities (large cities that still allow ample building and that weren’t overrun with migration from the Closed Access cities). Throughout the building boom, rent inflation remained high in the Closed Access cities. That is because those cities did not have a housing boom. But, in the Open Access cities, as building rates rose, rent inflation declined. (In contrast to the “overexpansion” theory of the housing crisis, taking into account all types of housing units, the expansion of the housing stock during the boom was moderate. Total units per capita did not rise excessively.)

In total, one might wonder how rental expenses remained fairly stable as a portion of American incomes if rents were rising so much in the Closed Access cities. The American public engages in the inevitable process of geographical sorting by income to maintain that level of spending. This is where the difference between households and housing units influences these measures.

Households move into the Closed Access cities to attain high incomes. In order to do that, they significantly reduce the housing they consume. The small Closed Access unit that might have rented for $1,000/month in earlier times now rents for $3,000. High income households are greatly reducing the space and quality of the units they live in so they can move to the Closed Access cities. In the process of making that move, they can manage to maintain rental expenses that are somewhat close to normal, as a portion of their budget. So, as a household, rent doesn’t climb substantially outside the norm. But the rent inflation on the Closed Access unit they moved into is perpetually high. And the price of that unit reflects those high and rising rents.

There are households in Closed Access cities for whom rent is increasing to uncomfortably high levels as a portion of their incomes. Those are the households that move away in order to make room for the new Closed Access residents. They move to places where new units are built to accommodate them, and when they make that move, there is no effect on rent inflation. The prices of homes where they move remains moderate (except for briefly in the Contagion cities) and rent declines as a portion of their income.

The only reason prices and rents in the Closed Access cities could continue to climb was because the composition of the households living in them was changing. But the active housing and lending markets facilitated those migration shifts were keeping rents and prices low in other places. In fact, in an economy dealing with Closed Access, an active housing market is necessary to mitigate the rising costs of Closed Access.

The High Cost of the Housing Bust

Looking back at Figure 1, notice how the housing bust and the financial crisis put an end to that cost-mitigating migration. Since the crisis, migration out of the Closed Access cities has slowed, so that their population growth has been nearly the same as for the country as a whole. Cities like Phoenix and Dallas have still grown somewhat faster than the national average, but their annual rates of growth declined by nearly one percentage point because of the housing bust.

Moving to Figure 2, see how this has translated into rent inflation that now is high throughout the country. Now, in all parts of the country, rents are rising for the same reason they were rising in the Closed Access cities before the crisis—a lack of new building.

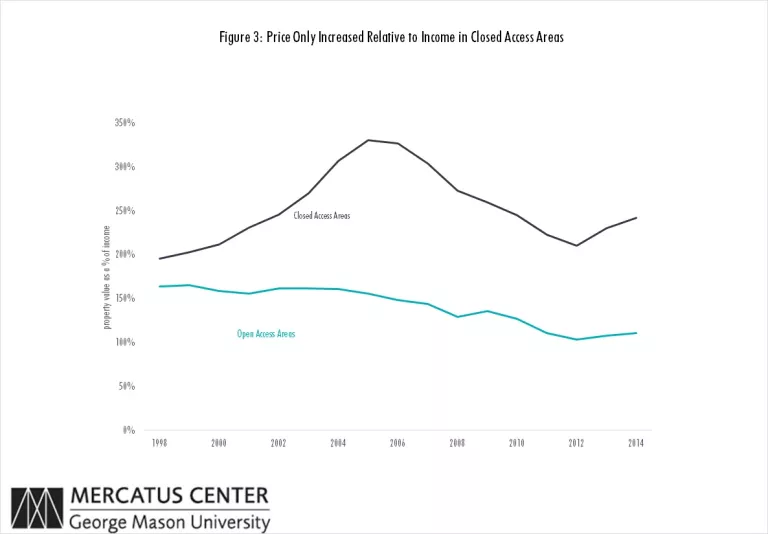

High prices can only be reduced relative to rents by encouraging new building or by locking buyers out of the market. Many potential buyers have been locked out of the market since 2008, and that did succeed in bring prices down. Again, looking at a national market, in terms of price, this appears to be a return to normalcy. It appears that the attempt to limit access through lending markets has solved the housing cost problem.

But, as Figure 3 makes clear, this is false. The suppression of credit has lowered Closed Access prices, but they are still high because rents are high. Open access housing has been pushed to a level well below previous norms. But attempting to solve the price problem in Open Access cities has created a rent problem.

Ironically, in order to truly solve the housing cost problem, prices in cities like the Open Access cities need to rise back to levels that induce the new building that can bring down rents. Dreaded “financialization” is what will bring down housing costs. When rising prices were associated with rising mortgages outstanding, rising prices were associated with falling rents, where new lending could fund new building. Prices have begun to rise again, but now they are associated with rising rents.

Where building new homes is permitted, rising prices lead to declining rents. But, rising rents lead to rising prices. In the long run, even the solution to rising prices begins with a focus on lowering rents.

Photo credit: Getty Images/Busà Photography