- | Monetary Policy Monetary Policy

- | Expert Commentary Expert Commentary

- |

Two Important Things We Learned from the Fed Chair Yesterday

Interest Rates to Keep Rising, Higher Inflation May Be Okay

As expected, the Federal Reserve raised its target interest rate a quarter of a percentage point on Wednesday. Its target range for short-term interest rates now sits at 1.75 to 2 percent. The Fed also signaled that it will probably raise interest rates twice more in 2018 given what it saw as good health in the economy. That would put short-term interest rates at 2.25 to 2.50 percent by the end of the year.

Fed Chair Jay Powell reiterated the optimistic take on the economy during his post-Federal Open Market Committee (FOMC) press conference. He noted that the FOMC’s decision to raise rates is a “sign that the US economy is in great shape” and that “most people who want to find jobs are finding them.”

This optimism was also apparent in the FOMC’s projection that it would raise interest rates three times next year. So if all goes according to plan, short-term interest rates should be between 3and 3.25 percent by the end of 2019.

Of course, all may not go according to plan. Some observers worry the Fed rate hikes could get ahead of the recovery and ahead of a neutral monetary policy stance. Some point to a flattening treasury yield curve as a potentially worrying sign. Historically, if treasury curves have inverted a recession has followed.

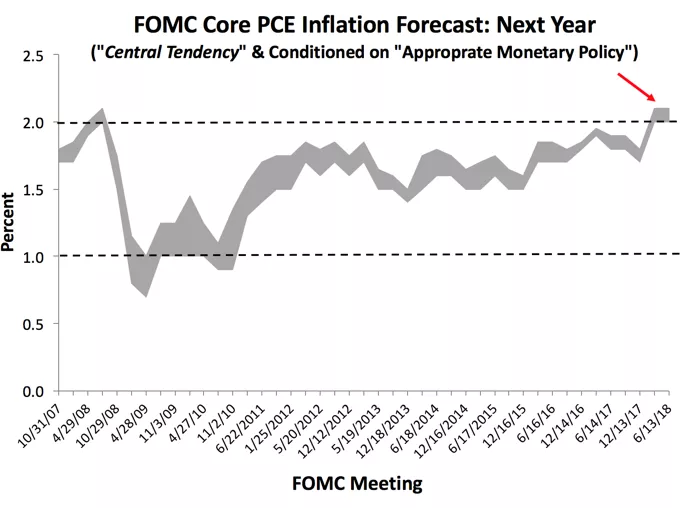

The Fed also signaled it will tolerate some inflation overshoot beyond its two percent target. In its Summary of Economic Projections (SEP), FOMC officials indicated that inflation may rise as high as 2.2 percent. While this may not seem like a big deal, it is a striking departure from the past decade when FOMC officials treated two percent as an inflation ceiling rather than a symmetric target.

The figure below illustrates this development. It shows the SEP’s central tendency for one measure of inflation over the next year. To be clear, the SEP instructs the FOMC members to submit paths for the core inflation “based on his or her assessment of appropriate monetary policy." The figure below, in other words, shows what FOMC members think inflation should be over the next year given “appropriate monetary policy.”

What is striking is about this figure is that it reveals FOMC officials thought appropriate monetary policy should generate inflation well below two percent for many years after the Great Recession. Even if one looks at two year-ahead horizons, where the Fed should have a lot of control over inflation, FOMC officials still view two percent as a ceiling. This is not how a true flexible inflation target (FIT) works. A FIT allows some overshoots and undershoots so that on average a particular target is hit. The FOMC, even at two years out, was instead treating two percent as a ceiling. Consequently, actual core inflation (based on the Personal Consumption Expenditures index) has been averaging below two percent over the past decade.

{kind=link}

This undershooting was a problem because typically after recessions there is a ‘bounce-back’ in spending and inflation that helps offset the collapse. It seems the Fed was afraid to let this robust recovery happen. As I argue in this recent paper, the FOMC was a slave to its inflation fears and this may have contributed to the slow recovery.

The irony is now the Fed seems okay with inflation overshoots. But the US economy is well past the bounce-back stage. There is less benefit to running the economy hot now, when it is near full employment, than right after the recession when the economy had much more slack. Again, 2.2 percent is not much above the two percent target rate and does not imply much overheating. But relative to the Fed’s past intolerance of inflation overshooting, it is hard to understand this shift in their preferences.

Fed chair Jay Powell also said at the press conference that the FOMC had not been discussing price level targeting but probably would in the future. It is great to see them open to change. As Tate Lacey notes, however, a price level is a step in the right direction but only a step. As Scott Sumner and myself have been arguing in our work at Mercatus, the final goal of US monetary policy should be a nominal GDP level target. So here is hoping Jay Powell and other FOMC officials also take time to consider it.