- | Expert Commentary Expert Commentary

- |

We Need to Use the Business Cycle to Pay Down Debt | Mercatus Policy Digest

The level of public debt is $24 trillion, and that is too high. It is so high now that it will likely lower our future standard of living. This could happen whether we choose to start paying it down soon or continue to ignore the problem. If we choose the latter, the impact might be quite large, especially if interest rates continue to rise and remain high for years into the future.

We will, of course, have no choice about another surge in borrowing if we head into another recession. If we get lucky and avoid recession, we do have a choice — we can slow our borrowing and eventually work towards paying some of this debt surge back. Incredibly, we are planning to do just the opposite. The president’s 2023 budget would have us borrow another $13 trillion over the next decade even if we have the solid economic growth that they project.

Since the end of World War II, federal debt has surged during recessions. For most of this time, we’ve relied upon the help of strong GDP growth during economic expansions to slow borrowing and moderate debt levels. After the Great Recession, things changed. First, we had what was at the time the biggest surge in non-war related federal borrowing in history. Debt as a percent of GDP literally doubled in just five years.

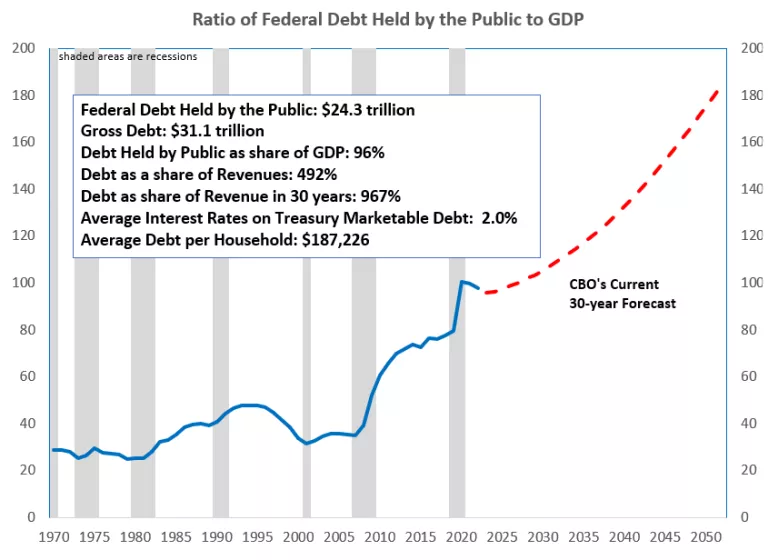

Second, when we eventually recovered to a period of solid GDP growth, we simply failed to take advantage enough to moderate the debt level. This is unlike previous economic expansions, and we even let debt begin to surge again when we headed into another non-war surge in public borrowing, this time from the global health crisis. This clearly compounded the severe fiscal impact of the pandemic recession. See figure 1 for our debt-to-GDP ratio since 1970, the most recent long-term forecast of debt under current law, and some basic facts about our debt.

The Level of Debt

So how much did debt surge in the Great Recession? In 2007, annual federal outlays outpaced tax revenues by “just” $160 billion or 6 percent. In the 15 years since, we added $20 trillion more in borrowing, and accumulated debt now totals 500 percent of annual tax revenue.

And just to be clear, this debt is not some abstract thing that the government alone must deal with. Current debt is a future tax increase. It is five full years full of tax revenue. And, according to the Congressional Budget Office, it will be 10 full years of total tax revenue unless we act. This will take decades and decades to pay off, requiring us to significantly raise taxes and/or lower federal spending (which diverts tax dollars to debt repayment rather spending on current programs). It is hard to see how this can be done without a decline in our standard of living.

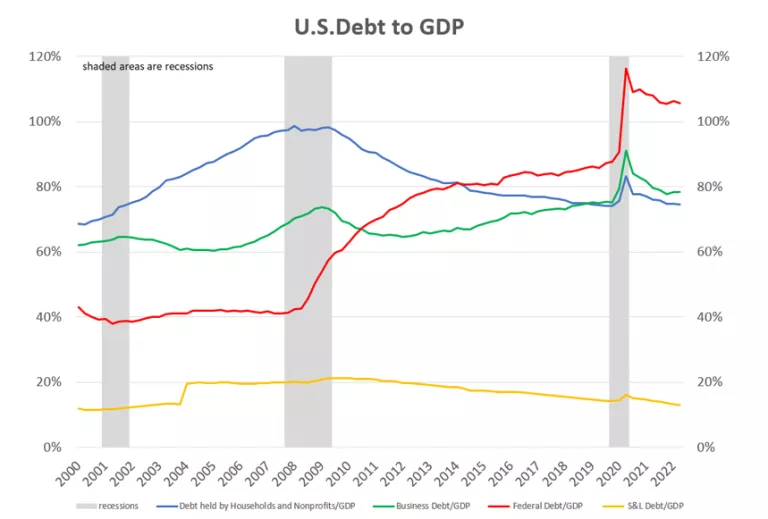

In the near term, the global health crisis and related recession may now be leading us into a global debt crisis. If we head into another recession, this will be an even greater concern. In 2020, we had the largest surge in global debt since World War II. Private and public debt combined has now reached a global record of $305 trillion with the United States holding about $68 trillion. Figure 2 shows the trends in U.S. private and public debt.

Private debt held by U.S. households is a record $126,369 per household. Bigger, however, is the share of federal debt held by the average household. It is now a record $187,226 per household. An environment of high debt and high inflation will make it especially challenging for monetary policymakers all over the world to achieve a graceful landing as they raise interest rates.

In the United States, monetary policy is certainly carrying the additional burden of trying to slow inflation by reducing demand through higher interest rates, while fiscal policy is pushing against this with continued stimulus from very high levels of spending and borrowing. This burden from “backwards fiscal policy” will only get heavier as the rising interest rates both raise public debt and make the extra fiscal stimulus more inflationary.

The Business Cycle

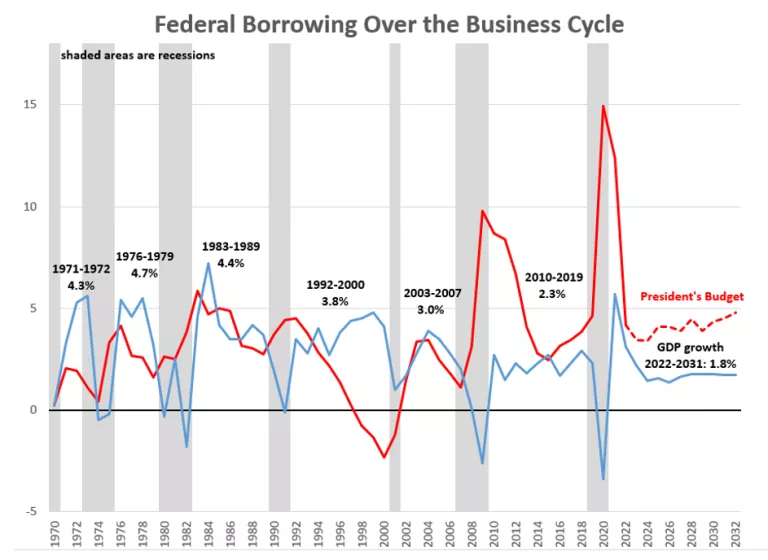

Federal debt is not new. The U.S. government immediately began incurring debt during the Revolutionary War and we have continuously carried some level of debt since (with the brief exception of 1835). For all of our post-World War II history, public debt has surged particularly during recessions. Overall, once we have returned to post-recession economic expansion, we’ve at least slowed our borrowing and sometimes paused it completely. We slowed borrowing after the 1974, 1981, 1990 and 2001 recessions. We even ran a budget surplus from 1998 to 2001 following the 1990 recession(As Figure 3 shows below). If we avoid recession, this is the time to moderate our borrowing, not accelerate it.

I’ll end this short note mentioning that there are many, many others who are alarmed by the level of debt and lack of commitment to fiscal responsibility. A Google search will tell you this. I’ll choose to quote a recent report by the Government Accountability Office called “The Nation’s Fiscal Health,” which recommends “Congress should develop a long-term plan to provide a cohesive picture of the government’s fiscal goals and a road map for achieving them. A fiscal plan would support the difficult policy decisions needed to achieve a more sustainable fiscal policy, one where publicly held debt is stable or declining relative to the size of the economy.”

Now that we may be beginning a period of solid economic growth, the time for this is now.