- | Expert Commentary Expert Commentary

- |

Another Bad Idea

There is a disconnect between proposed stimulus spending and improving economic conditions

Policymakers have been quarreling over the content and size of a proposed new stimulus spending bill for five consecutive months now. In the latest round of discussions, Democratic lawmakers called for at least $2.2 trillion in spending, Republican senators proposed an alternative $500 billion “skinny” stimulus bill, and the president and the Treasury secretary proposed $1.8 trillion in additional spending.

Regardless of the outcome of the election, it seems highly likely that there will be a push to pass another multitrillion-dollar stimulus package. But such a package makes little economic sense and may do more harm than good.

With the passing of the CARES Act in the spring, policymakers of all political stripes came to a broad, if not rash, consensus that $2.2 trillion was an appropriate amount of stimulus spending, given the economic conditions at the time. In hindsight, there were several problems with the rushed-through CARES Act, including the following: (1) an overly generous unemployment insurance expansion that meant most recipients were better off not working; (2) a Paycheck Protection Program that was badly targeted and had little impact on employment levels; and (3) a vast bailout of states that had been deeply irresponsible in managing their finances for many years.

Given all the flaws of the CARES Act, you might be naive enough to believe that several months after passing the initial stimulus bill, policymakers would be more informed about how to better target government support and less apt to simply throw large sums of money at a complex problem such as the COVID-19 pandemic. But you would be wrong. In fact, with the labor market continuing to make a strong recovery from April lows and several economic indicators signaling a V-shaped recovery, policymakers are still dead set on an all-too-familiar figure: $2.2 trillion.

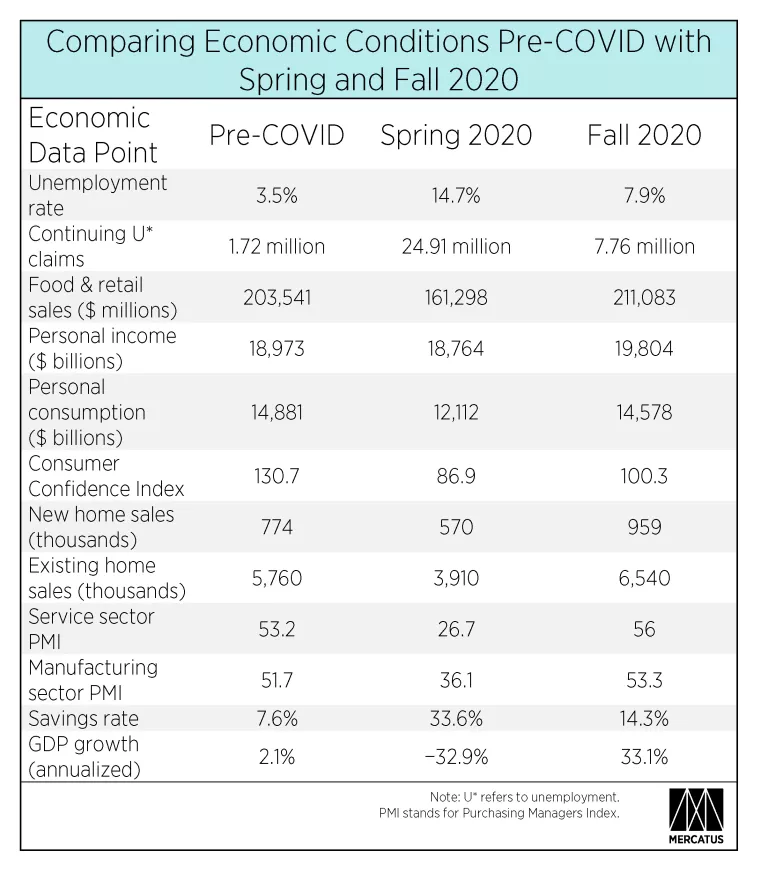

To illustrate why a new stimulus package with spending levels equal to those of the CARES Act makes little economic sense, one only needs to look at a few economic data points in the table below comparing pre-COVID conditions (January/February) with those in spring 2020 (April/May) and fall 2020 (September/October).

While the unemployment rate remains high compared to pre-COVID levels, it has declined significantly since the spring and is forecast to reach its historic norm by January. (The historical average unemployment rate from 1975 to the present is 6.3%.) Meanwhile, continuing unemployment claims have fallen precipitously, declining by over two-thirds from historic highs in May. While there is still significant slack in the labor market, particularly in states such as California and New York, conditions today are not remotely as severe as they were in the spring. These improvements must be accounted for when formulating employment support policies.

As for income, spending and savings patterns, Bureau of Economic Analysis data reveal that personal income levels have not just recovered from March lows but actually exceed January 2020 levels by a notable margin. Personal consumption expenditures have recovered by 89% from April lows, and the savings rate remains at double the historic average level.

In October the monthly Purchasing Managers Index (PMI) noted, “Recovery gains momentum amid sustained upturn in demand.” The latest PMI data show that the services sector grew at its fastest pace in two years, while manufacturing output rose at its steepest rate in 21 months. After contracting in the first two quarters of the year, GDP grew at 33.1% in Q3 (the seasonally adjusted annual rate) and is projected to grow at a respectable 3.5% in Q4.

In spite of all this good news, policymakers who are dug into stimulus package negotiations seem to think that we’re still living in the spring, that unemployment is at historic highs, and that most businesses remain closed.

As the dust settles after the presidential election and politicians return to the negotiating table, they should start by acknowledging the significantly improved economic conditions. More importantly, they should refrain from spending hundreds of billions of taxpayer dollars on bailing out irresponsible state governments or airlines to compensate them for egregious overcompensation of workers and executives and share buybacks.

Meanwhile, continued improvements in labor market conditions should convince negotiators that additional unemployment benefits (especially anything above $200) would be counterproductive. Furthermore, the states with the slackest labor markets today also tend to be the ones with the most generous state unemployment benefits—showing that additional generosity in these states would only further discourage work.

As my colleague Veronique de Rugy points out, “It's right to help those low-income Americans hurt by the pandemic-induced recession. But that relief bill shouldn't cost anywhere near $2 trillion.”

Our political leaders should avoid multitrillion-dollar spending packages that are more akin to election promises than good policy. Instead, they should take a measured and targeted approach that supports those still negatively affected by the pandemic, while avoiding policies that discourage work.

Image Credit: Chuck Savage/The Image Bank/Getty Images