- | Government Spending Government Spending

- | Expert Commentary Expert Commentary

- |

Assumptions Matter for Illinois Pension Buyout

This post has been edited to reflect updated calculations by the author.

Illinois, a state well-known for its severe budget problems, has turned to some creative policy solutions aimed at providing pension buyout options for state workers. Simply passing a budget puts the state leaps and bounds ahead of where they were this time last year; last June they were still about a month away from passing a budget to close out a two-year budget gap. The reforms in this year’s budget show more promise for long-term solutions, but still have a long way to go to fully address Illinois’ financial and transparency issues.

By focusing on reforming pensions in this year’s budget, Illinois policymakers are signaling that they want to get serious about long-term solutions. Doing so moves beyond the mindset that merely increasing taxes will solve the structural funding issues weighing down the state’s pension plans. But up until now, Illinois policymakers have been constrained given the state’s constitutional limits to pension reform.

This is why the new pension reforms are voluntary. Under the bill, there are two buyout options. One is directed at beneficiaries who are vested in one of the pension plans, but are no longer active members. They can voluntarily choose to accept 60 percent of the present value of their vested pension benefit in exchange for dropping out of the system. The other buyout option is for beneficiaries who have not retired yet. They can choose to receive a lump sum payment of 70 percent of their pension balance and a 1.5 percent cost-of-living adjustment (COLA) that is not compounded in exchange for their previous three percent compounded COLA. All beneficiaries who accept the buyouts will roll over their benefits into retirement funds similar to the way that private sector employees roll over their 401(k) benefits when changing jobs.

Are these buyout options a good deal? At first glance, they certainly seem like it from the state’s perspective. The first buyout option for vested members is estimated to save the state $41 million and the second option could save $382 million. The question remains whether this is a good deal from the perspective of state workers.

Beneficiaries who opt into these buyouts only get 60 or 70 percent of what they were originally promised. Opponents of the reforms have called the deal unfair. Indeed, reducing lump sum payouts by such factors has not proven acceptable in buyouts for private-sector plans. The general idea of buyouts, however, has proven successful in the private sector, albeit with larger payments. The practice has been much less common in the public sector, with Missouri being the other only public sector example.

As described in a Mercatus research paper from 2016, workers in especially insolvent and fiscally distressed pension systems may be well-advised to take a buyout deal. In their paper, former Mercatus researchers Mark J. Warshawsky and Ross Marchand write:

“…once the unsustainability of many government plans is apparent, those affected retirees and long-time workers will become legitimately worried that their retirement benefits are highly uncertain and likely subject to one-off arbitrary and chaotic cuts in bankruptcy, insolvency, and political processes operating in a poor fiscal environment…When it becomes clear that many state and local governments cannot pay off their massive underfunded pension obligations – even with increased taxes – these retirees and older workers may be willing to accept a lump-sum that represents a significant, but not necessarily full, share of the actuarial value of their promised benefits.”

Illinois’ lump-sum payment calculations fall short of this recommendation because they rely on interest rate assumptions that do not fully reflect reality.

Illinois ranked 49th overall in the latest edition of our “Ranking our States by Fiscal Condition” report. With revenues that only covered 96 percent of expenses in FY2015 and long-term liabilities making up 317 percent of total assets, or $12,118 per capita, the state finds itself in an ongoing dire fiscal situation. But Warshawsky and Marchand’s lump-sum payout policy recommendation has another key component that Illinois’ buyouts lack. They stress the importance of giving pension plan participants accurate information about the funded status of their pensions. Illinois’ lump-sum payment calculations fall short of this recommendation because they rely on interest rate assumptions that do not fully reflect reality.

Warshawsky and Marchand recommend that when buyout options are appropriate, government plan sponsors should offer a payout equal to the present value of each participant’s retirement benefits accrued to date, reduced by 100 percent minus the funded percentage of the plan at the time of the offer. They also recommend adding five percentage points as a sweetener to provide extra encouragement for retirees and older workers to take up the offer, though policymakers could alter this to be more or less generous.

The best-case scenario would base the “funded percentage” on a market valuation of plan liabilities using economically wise interest rate assumptions. Following this recommendation and using a market valued funded ratio from fiscal year 2016, for example, would assess Illinois’ plans at 21 percent funded. To complete Warshawsky and Marchand’s recommended calculations, we would subtract 21 from 100 to get 79. For a retiree who opts into the buyout, we would subtract 79 percent of their accrued retirement benefits and then add the extra 5 percentage points in order to get to their final lump-sum. Illinois’ buyout options are not based on these numbers, but on rosier funded ratios and less reliable calculations instead.

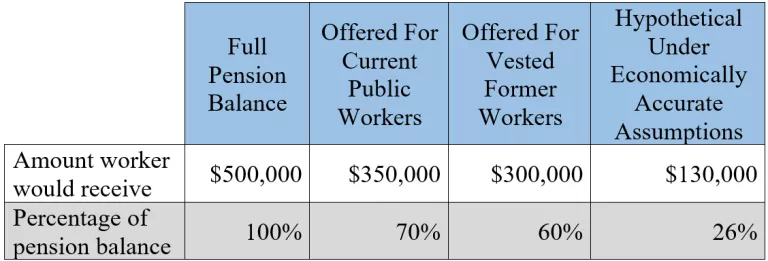

Without fully explaining how the lump-sums are calculated, or which interest rates are used, policymakers are concealing the fact that beneficiaries would receive more than what the state can afford. Suppose I used to be a public worker, but have since retired from service. Let’s also assume that my pension balance is $500,000. Under the bill that just passed, I could choose to receive 60 percent of my balance, or $300,000, as a lump-sum. As previously explained, however, this estimate relies on unrealistic interest rate assumptions.

If I was offered an alternative buyout option that used more economically accurate assumptions, I would be getting a smaller buyout. Under this hypothetical alternative scenario, I would receive a lump-sum of $130,000 or 26 percent of my original balance, rather than the 60 percent currently on the table. The table below compares these buyout options as well as the other buyout option currently available to current public workers.

Public Workers Would Receive Smaller Buyouts under Better Economic Assumptions

The two offered options are based on calculations from pension buyout options presented in the recent Illinois budget. The hypothetical option is based on the recommendation from Warshawsky and Marchand that plan participants be given accurate information. These calculations are based on Illinois' fiscal year 2016 market funded ratio of 21 percent and a combined market unfunded actuarial accrued liability of $445.79 billion. The 15-year treasury rate used for that time period was 1.675 percent.

I am not running these calculations to suggest beneficiaries are receiving more than they deserve, but rather to highlight what exactly goes into their calculation and to suggest that Illinois’ financial situation is even worse than they let on. Depending on what interest rate is used, the nature of the unfunded liability changes, which in turn changes the size of the potential lump-sum. In debates about whether or not Illinois’ pension buyouts are “a good deal,” this is largely ignored.

By using unrealistic interest rates for these buyouts, policymakers are concealing just how severe their financial situation is. For a given buyout option, the terms should reflect the true funded status of the pension plan. Applying more realistic interest rates to Illinois’ recent buyout options reveals that their situation is so bad that being completely transparent with beneficiaries would require significantly cutting lump-sums. It is not surprising that policymakers have decided to go with less honest interest rates.

Some retirees and older workers will find it fitting for their financial situation–and concern about Illinois’ future decisions about pensions–to accept a buyout. Hopefully, though, policymakers will be more transparent so all parties can be more informed before moving forward on such a life-changing decision. The interest rate selection in the latest reforms works in favor of public workers who opt in to receive lump-sums, but only postpones the inevitable for beneficiaries who stick around.

The key essence of Warshawsky and Marchand’s policy recommendations recognize the underlying reality of most pension problems. For some extremely insolvent plans, the more that time passes without reform, the lower the likelihood that the state will be able to pay out their pension liabilities as originally promised. Although no policymaker wants to go back on their promises, the longer they postpone sustainable reform, the more they must deal with the reality of their past mistakes. Buyouts, properly structured, provide a compromise to meet all of these competing priorities. However well-intentioned, Illinois pension buyouts don’t balance these priorities well.

Even if this best case scenario occurs, the savings would still fall short of the $7.1 billion backlog of unpaid bills.

If a significant number of workers take up the recent buyout offers, Illinois could save as much as $432 million. Moody’s Investors Service cited the new budget and these projected savings as a credit-positive move for Illinois. S&P, however, released statements that expressed doubt about the budget’s ability to seriously tackle Illinois’ financial problems. Moody’s predictions rely on at least 22 percent of vested former workers and 25 percent of retiring current workers participating in the buyout programs. Even if this best case scenario occurs, the savings would still fall short of the $7.1 billion backlog of unpaid bills. This, paired with the fact that Illinois is going to use general obligation bonds to fund the buyouts, only further provides evidence to question the fiscal stability of the recently passed budget.

Photo credit: John O'Connor/AP/Shutterstock