- | Housing Housing

- | Expert Commentary Expert Commentary

- |

Because of Housing, All Taxes on Capital Tend to Be Regressive

Part Fourteen of Kevin Erdmann's Housing Affordability Series

In part 13, I discussed two elements of the Tax Cuts and Jobs Act of 2017 (TCJA) related to housing: a reduction in the deductibility of state and local taxes, and a reduction in the mortgage interest deduction.

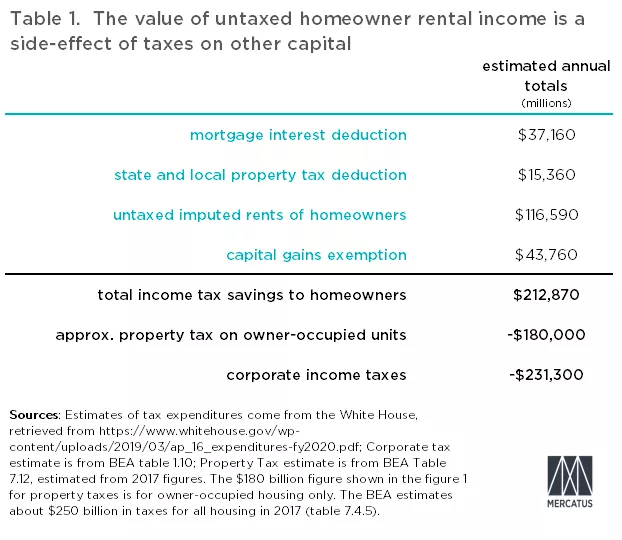

In addition to the mortgage interest deduction and the property tax deduction, homeowners also enjoy an exemption for capital gains on home sales. Additionally, homeowners don’t pay taxes on the rental value of their homes. In fact, the untaxed rental value of owner-occupied homes is a larger tax benefit to homeowners than the mortgage interest deduction and the property tax deduction combined.

Even if all of the tax deductions that appear on tax forms were eliminated, owner-occupiers would be left with an enormous unwritten subsidy, because untaxed rental value is income that never leads to a transaction.

Even though homeowners invest in a property with rental value, and earn that value just as they would if they invested in rental properties, they never actually write a rent check to themselves. Because they never actually write a rent check, there is no measured economic activity for tax purposes.

Don’t be mistaken. This is economic activity. Those homes provide shelter, which has an economic benefit. The Bureau of Economic Analysis (BEA) estimates that value in their measure of economic production. But it would be difficult for the IRS to tax it.

As mentioned in earlier posts in this series, property taxes are a form of public rent payment. But they are applied to both rental properties and owner-occupied properties. In addition to that expense, owners of rental properties also pay income tax on their net rental income, which is passed on to the tenant as part of their gross rental expense.

So, as long as there is any income tax paid on capital, in general, there will be an inherent subsidy to owner-occupiers. They don’t pay tax on the rental value of their homes. Since owner-occupiers are generally households with more wealth, higher incomes, and higher marginal tax rates, non-taxed rental value will inevitably be a regressive element in the income tax code.

This is a selective tax subsidy. It only applies to homeowners. It doesn’t change the rental value of their homes. But as I argued in part 8 of this series, a subsidy for owners is mathematically equivalent to a rent subsidy. Tax subsidies lower their rental costs. Rent is the true measure of housing affordability, and the exemption of homeowner rental value from taxation lowers effective rents for homeowners.

Taxes on corporate and business income, in general, have effects that are harder to pin down. Businesses write the checks that pay business income taxes, in a direct sense. But since those taxes apply more broadly to most economic activity, they lead to changes in prices, wages, and pre-tax returns on investments that are complex.

It is difficult to say how much corporate taxes affect the incomes of laborers vs. owners, prices vs. costs, or the progressivity vs. regressivity of the tax code. The one thing that can be said with confidence is that corporate taxes don’t fall heavily on a single group. In the long run, they lead to some changes in prices, some changes in wages, and some changes in profits. One can argue about the exact weights of those changes, on the margins, but the complexity of all those changes means the relative net long-term effect on workers, owners, and consumers is muddled.

The same complexity is true of property taxes, as has been discussed in earlier posts. Who really pays property taxes depends on the elasticity of housing supply. Where supply is elastic (meaning there are few obstacles to new supply), renters effectively pay the property tax and rents increase. Where supply is inelastic (meaning there are many obstacles to new supply), owners effectively pay the property tax and home prices decrease.

The value of untaxed homeowner rental income is a side-effect of the tax on other capital. In other words, the White House estimates for the untaxed imputed rents of homeowners, shown in Table 1 below, are only listed as tax subsidies because it presumes that, given the opportunity, they are income that would be taxed. If there was no income tax on capital incomes, there would be no tax subsidy to homeowners for the rental value of their homes.

The elimination of a quarter trillion dollars of corporate taxes with an undetermined progressivity would lead to the disappearance of a quarter trillion dollars of homeowner tax benefits that would either automatically disappear or could be eliminated as redundant.

The net effect of those changes would reduce public revenues by a quarter trillion dollars. Eliminating other forms of capital taxation would reduce public revenues even more. The details become too complicated to work out here. For instance, because of the changes to things like wages and price that would be triggered, public revenue from taxing wages would increase.

But two statements can be made with some confidence. Eliminating taxation of income from capital would reduce federal tax revenues by a few hundred billion dollars, and in the process it would make the tax code more progressive.

However, as I noted in part 9, residential property taxes are roughly half the level they were in the early 1970s, depending on how they are measured. Property taxes at levels similar to the 1970s would create a quarter trillion dollars of new tax revenues.

For simplicity, I have focused on corporate income taxes here, but this logic applies to broad-based taxation on any capital that serves as a potential substitute to investments in owner-occupied housing.

For instance, high inflation acts as a generalized tax on many types of capital, because investors have to earn a higher return to make up for the declining value of dollars, and they are taxed on all of that income. High inflation in the late 1970s likely led to rising home prices and increased homebuilding as a result because housing is sheltered from taxes.

Now, these are taxes that exist at various unrelated levels of government, and this discussion is very generalized and broad. My intention here is simply to introduce this point of reference: that the income tax code, as it exists, has regressive effects regarding housing affordability.

Given those effects, it is inaccurate to treat capital taxation in general as a progressive tax. Corporate taxation, in general, creates a regressive rent subsidy. A different tax regime that focused on property taxation rather than generalized capital taxation could plausibly produce public revenue in a way that would be more progressive than a tax code that taxes capital income more generally. This should cast doubt on common presumptions about how and why to change the tax code.

Photo credit: Chip Somodevilla/Getty Images