- | Monetary Policy Monetary Policy

- | Expert Commentary Expert Commentary

- |

The Challenges of Dollar Dominance

Is the US dollar too much of a good thing? Can its success in becoming the main currency of the world also make it a curse for global financial stability? These and other questions about the dollar’s dominance are increasingly being considered by policymakers, academics, and journalists as the reach of the dollar continues to grow. These concerns were also front and center at the Kansas City Federal Reserve Bank’s conference last month in Jackson Hole, Wyoming, an annual gathering of influential voices in central banking.

Concerns over the dollar are not new. In the 1970s, President Richard Nixon’s Treasury secretary, John Connally, once told foreign finance ministers that the dollar is “our currency, but your problem” after they complained about its inordinate sway on their economies.

What is new, however, is that the dollar’s influence has noticeably grown since then as the global economy has become more integrated. The dollar is now a truly hegemonic currency and, as a result, creates challenges not only for other countries but also for the United States.

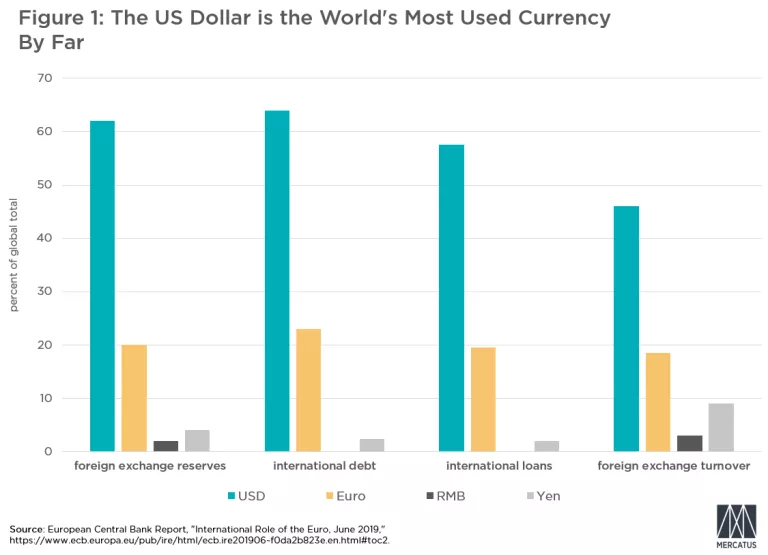

The dollar’s dominance is evidenced by the 50 to 80 percent of international trade being invoiced in dollars, the $28 trillion of relatively liquid, dollar-denominated debt held outside the United States, and the 70 percent of the world economy’s currencies anchored in varying degrees to the dollar. Figure 1 provides further evidence of the dollar’s dominance by comparing it to other currencies across several indicators. The dollar truly is king among currencies.

It’s Not Easy Being King

The first challenge created by the dollar’s dominance is that the global economy is highly susceptible to swings in US monetary policy. The Fed effectively shapes, to varying degrees, monetary policy for the 70 percent of the world economy that links their currency to the dollar. What may be appropriate monetary policy for the US economy could be destabilizing for the rest of the world. This makes the Fed a monetary superpower.

Global economic conditions, are not just swayed by US monetary policy, but are affected by any change in the value of the dollar. A key reason for this vulnerability is the large amount of dollar liabilities held abroad.

Of the $28 trillion of dollar-denominated debt held outside the United States, just over $11 trillion was issued by foreigners. This means there is $11 trillion in dollar obligations from countries where revenue is earned in foreign currencies. This currency mismatch makes these countries vulnerable to sudden dollar appreciations that cause the real burden of the dollar liabilities to grow.

The biggest reason for swings in the dollar’s value, outside of Fed policy, are the changes in global demand for US financial assets. The US is the main producer of safe assets for the world economy and, as a result, whenever demand for safe assets spikes, demand for the dollar also surges. This raises the value of the dollar and induces global financial stress through the dollar channels outlined above.

These linkages give rise to what economist Hélène Rey calls a “global financial cycle,” where shocks to the dollar reverberate across the world and can ricochet back to the United States. The global economy, in short, is highly susceptible to swings in the dollar. This is a key challenge for central bankers across the world and was a central issue discussed at the Jackson Hole conference.

Interestingly, one paper presented at the conference by economists Arvind Krisnamurthy and Hanno Lustig noted that this dollar-dominance problem grows with each financial crisis. During such periods, the demand for dollar-denominated safe assets rises and, as a result, their financing costs fall. This means dollar financing costs decline relative to other currencies during crises. This cheaper financing for dollar assets incentivizes foreigners to issue their own dollar-denominated debt which, consequently, spreads the chokehold of the dollar.

More generally, to the extent the US financial system is not satiating global demand for dollar-denominated safe assets, it will be met with dollar-denominated asset issuance elsewhere in the world, thereby expanding the reach of the dollar. This leads to what Krisnamurthy and Lustig call a “global dollar cycle” that intensifies with each financial crisis.

Another challenge created by the dollar’s dominance is that it creates direct costs for the US economy. First, it causes the dollar to be overvalued more often than not, given the global demand for dollar-denominated safe assets. This tendency, in turn, gives rise to persistent trade deficits that have distributional and political consequences.

Second, ongoing budget deficits are more likely to occur in order to meet the global demand for Treasury securities, the safest of safe assets.

Finally, the favorable financing terms given to dollar-denominated assets encourages more leverage in the US economy than would otherwise be the case. Put differently, the US is suffering its own form of “Dutch Disease,” as noted by the Financial Time’s Brendan Greeley.

Proposed Fixes to Dollar Dominance

So what can be done about challenges of the dollar’s dominance? Bank of England governor Mark Carney’s answer to this question at the Jackson Hole conference was to create a new synthetic digital currency backed by the major central banks of the world. It would be similar in spirit to Facebook’s Libra proposal, but would be based on a basket of central bank digital currencies. This new “synthetic hegemonic currency” or SHC would replace or at least rival the dollar as a new reserve currency and therefore ease the costs of the dollar’s dominance.

While well-intentioned, the SHC is unlikely to see the light of day for several reasons. First, the large network effect of the dollar will be hard to break. As mentioned earlier, there is $28 trillion in relatively liquid dollar-denominated assets held outside the United States. To compete with the dollar, the SHC would have to be issued on a similar-sized scale. That seems doubtful, since it would require a vast expansion of the central bank balances sheets supporting the SHC.

A second reason the SHC seems unlikely is political. The US government would have to voluntarily give up the profit it makes, called seigniorage, from issuing the safest assets on the planet. There would be a similar loss to the private US financial system, which also issues relatively safe assets to the world. Consequently, it seems unlikely that the SHC or any rival to the dollar will emerge anytime soon.

Another attempt to address the challenges of the dollar’s dominance is a bill proposed by Senators Tammy Baldwin (D-WI) and Josh Hawley (R-MO). It would tax foreign purchases of US financial assets. The intent of the proposed legislation is to reduce the demand for the dollar and thereby reduce the US trade deficit. Like Mark Carney’s proposal, this bill is unlikely to succeed in its stated objective. It could also actually worsen the very problem it is trying to solve.

Here is why. The Baldwin-Hawley bill would effectively reduce the supply of safe assets, but not change the global demand for them. The resulting excess demand for safe assets created by the bill would put additional pressure on the existing safe assets, particularly ones from the United States. This would drive up the value of the dollar and push down interest rates even lower.

This is not just a theoretical concern, but one we have seen played out before. During the 2007-09 financial crisis, the stock of private-label dollar-denominated safe assets sharply declined. This reduction in the overall safe asset supply led to an excess demand problem that pushed up the value of the dollar and drove down Treasury interest rates. The Baldwin-Hawley bill, if implemented, would likely lead to the same result and lead to even lower interest rates across the world.

Fed Palliatives for Dollar Dominance

It seems unlikely, then, that there is a comprehensive solution in the near term for the challenges of dollar dominance. There are a few policies, however, that the Fed could unilaterally adopt that could ease some of the costs.

First, the Fed could implement some kind of level target that would make up for past misses of its target. Over the past decade, when US monetary policy persistently undershot its inflation target, such a make-up policy would have eased some of the dollar’s strength.

Second, the Fed could extend currency swap lines to more countries, as proposed by economist Sri Thiruvadanthai. In emergencies, these facilities allow a central bank to temporarily swap their currency to the Fed for dollars. Foreign authorities could then use the dollars to deal with financial crises. If the currency swap lines were available to more countries and made permanent, it would probably ease some of the world’s precautionary demand for dollar assets.

Though both of the proposals would ease some of the dollar pressures, they would be big policy changes for the Fed. Adopting a level target would be changing the Fed’s entire approach to monetary policy. Offering permanent currency swap lines to additional countries would further increase the Fed’s implicit liabilities.

Still, these policies are possible as the Fed is reviewing its monetary framework this year and in the past has extended currency swap lines to certain countries. Maybe this could be the policy space where President Trump and the Fed can come together in agreement.

All Hail the King

No matter what happens moving forward, it is worth remembering that though there are costs to dollar dominance, there are also many benefits that are often taken for granted.

For example, is not hard to imagine a world where the dollar did not emerge as a global medium of exchange, globalization did not happen, and billions of people remain trapped in poverty. Compared to this counterfactual, one can argue that the dollar’s rise to power has been an unmistakable net benefit for the world.

So while there is a place for addressing the costs of dollar dominance, let us not forget all the good our king of currencies has brought to the global economy. Long live the king.