The notion of a recession is actually a narrow way of thinking about economic cost, and it focuses attention too much on short-run, highly visible, and painful burdens. I worry that the spreading out of Brexit costs over time will lead the British people to feel invulnerable, to demand too much from their politicians, and to limit their ties with the EU too much and too quickly.

With the arrival of positive manufacturing and services reports from the U.K., it seems that the British economy is doing fine. There's dwindling talk of a recession caused by the vote the leave the European Union, and British politicians are wondering if a “hard Brexit” option –rapid withdrawal from Europe without a new trade agreement – might be feasible.

The answer is no. Such views rest upon bad economic reasoning and the cost of Brexit remains high, albeit mostly invisible for the time being.

Nations can pay an economic price in many ways, whether or not it takes the form of an actual recession. The term “recession” is an artifact of macroeconomists, and formally a recession is a sequence of two or more quarters with shrinking gross national product. Most of the losses from Brexit will be felt more slowly, though they probably will be worse than a mere recession.

What is unusual about the Brexit scenario is how suddenly it came along. The night before the June 23 vote, prediction markets strongly favored Remain, so the impact of Leave showed up quickly in asset prices, most of all in the form of a currency decline. That moved most of the pain away from a daily to-and-fro debate over economic conditions, and toward a rapidly-arrived understanding of what a new long run would look like.

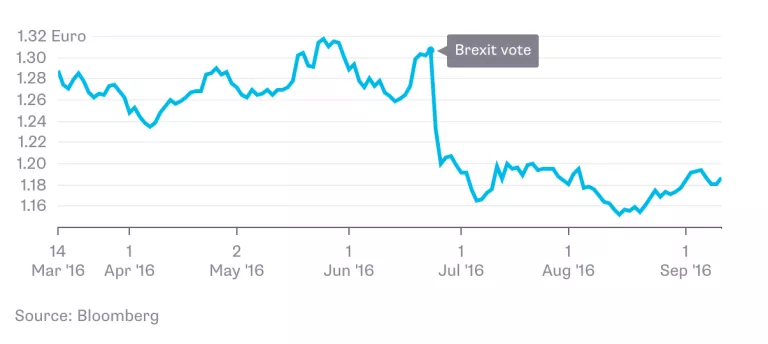

Start with the decline in the British pound. Against the euro, the currency of the U.K.’s main trading partner, the pound has dropped about 9 percent since right before the vote. I will suggest based on my own rough and conservative calculation that an actual Brexit, if it happens (the messy process will take years and could be abandoned or reversed), would would push sterling down a little more, resulting in a total drop of around 10 percent.

There Goes the Currency

That means British assets are worth less by global standards. Let’s continue with the rough calculations. Net household wealth has been estimated at about 9 trillion pounds, and if we add in U.K. government holdings of land and other assets, let’s say this is about 12 trillion pounds.

How much has the value of that wealth gone down? It’s not right to say “10 percent,” because for purely domestic activities the lower value of the pound doesn’t matter much. If you want to buy a used copy of Dickens and go for a walk in the Lake District, that’s no more expensive than before.

Nonetheless imports are almost 30 percent of British GDP, which you can take as one possible measure of what eventually might be spent on the outputs of foreign nations. So plausibly, in the long run that 30 percent becomes 10 percent more expensive because of the weaker British currency. Thirty percent of 12 trillion is 3.6 trillion, and the 10-percent value decline from that figure is 360 billion pounds, or about 5,625 pounds per capita. a pretty steep price for the Brexit vote.

To put that 360 billion pounds in context, that is about 19 percent of 2015 British GDP, much costlier than a typical recession. The bigger loss, however, is less psychologically painful because it is spread out over many years, basically the rate at which the British will spend down their wealth. And if you view the country as a wealth-generating mechanism for the future, in fact the actual costs will be higher because hitherto-unproduced wealth will be worth less too, although those costs are more distant yet.

This isn’t any kind of formal international trade model, with a full set of measurements and moving variables. It's just a simple way of showing that the costs of Brexit can be high without a recession. It is quite possible and indeed likely that various adjustments, including a move away from foreign imports, would lower these costs. On the other side of the ledger, Brexit could help create a negative political and economic momentum that is not captured here either. Nonetheless this is a gross approximation of the first-order hit to British wealth.

In the meantime, don’t be too cheered by the positive reports. For instance, under all plausible economic projections for Brexit, including the most pessimistic, exports should jump in the short run. British production capacity is still in place, and the cheaper British pound will spur more orders from abroad. The real questions about cost are how exports will fare once (if?) Brexit actually occurs and tariffs go up, and also how imports will become more expensive over time.

The notion of a recession is actually a narrow way of thinking about economic cost, and it focuses attention too much on short-run, highly visible, and painful burdens. I worry that the spreading out of Brexit costs over time will lead the British people to feel invulnerable, to demand too much from their politicians, and to limit their ties with the EU too much and too quickly.